Mortgage rates back to 7%.

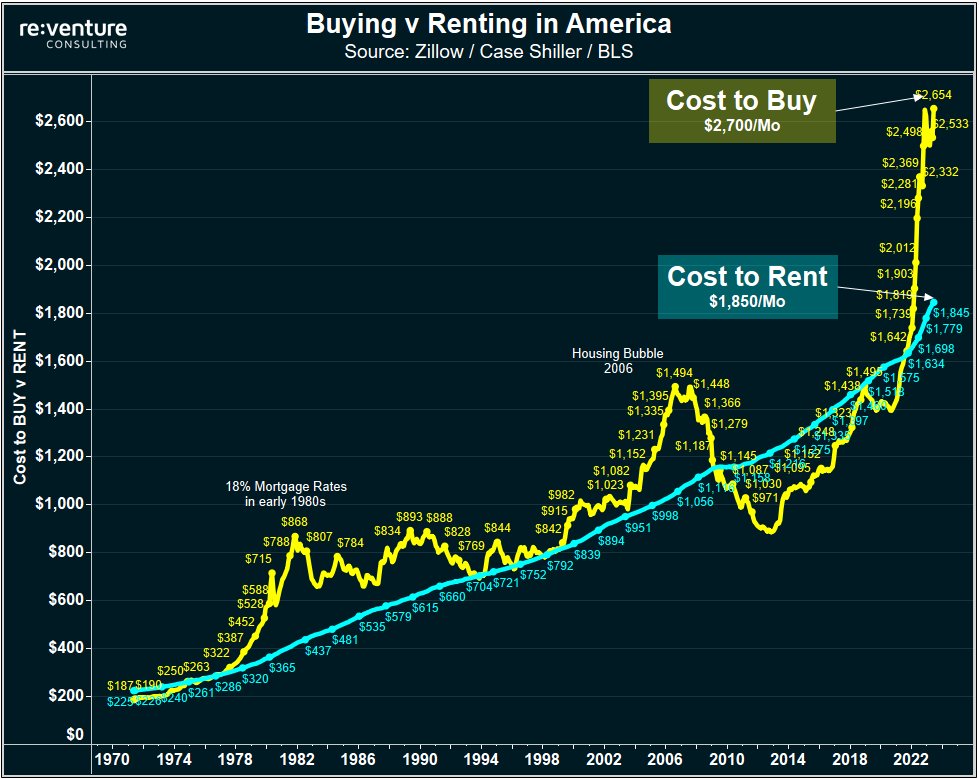

Meaning that the cost to buy a house in America is now approaching $2,700/month when including mortgage, tax, insurance, and maintenance.

Meanwhile, cost to rent is $1,850.

Biggest gap we've ever seen. Something has to break.

Meaning that the cost to buy a house in America is now approaching $2,700/month when including mortgage, tax, insurance, and maintenance.

Meanwhile, cost to rent is $1,850.

Biggest gap we've ever seen. Something has to break.

1) the easiest thing to "break" is Mortgage Rates going back down.

The next easiest thing to break is Home Prices coming down.

Likely some combination of the two will be required to save the US Housing Market from another massive collapse in buyer demand.

The next easiest thing to break is Home Prices coming down.

Likely some combination of the two will be required to save the US Housing Market from another massive collapse in buyer demand.

2) Mortgage applications to buy a house in mid-May were already at lowest level in 20 years.

Now they will likely decline further due higher mortgage rates.

I mean - how low can homebuyer demand in the US Housing Market go before something in the economy breaks?

Now they will likely decline further due higher mortgage rates.

I mean - how low can homebuyer demand in the US Housing Market go before something in the economy breaks?

3) In the end I don't think 7% mortgage rates will stay for long.

Because the housing market can't handle it. Transaction volume is already far too low.

If it goes down further, layoffs in associated industries like construction, manufacturing & retail will follow.

Because the housing market can't handle it. Transaction volume is already far too low.

If it goes down further, layoffs in associated industries like construction, manufacturing & retail will follow.

4) The banking system might also have problems.

The last time mortgage rates hit 7% in early March, Silicon Valley Bank happened.

(There's still lots of unrealized losses on the books for banks, so these spikes in rates are very destabilizing to the banking system)

The last time mortgage rates hit 7% in early March, Silicon Valley Bank happened.

(There's still lots of unrealized losses on the books for banks, so these spikes in rates are very destabilizing to the banking system)

5) The US consumer will also have problems.

Higher rates means not only will mortgages be more expensive, but so will credit cards and car loans.

Occurring just as wage growth is stagnating. And even going negative for higher income groups.

(Source: Bank of America)

Higher rates means not only will mortgages be more expensive, but so will credit cards and car loans.

Occurring just as wage growth is stagnating. And even going negative for higher income groups.

(Source: Bank of America)

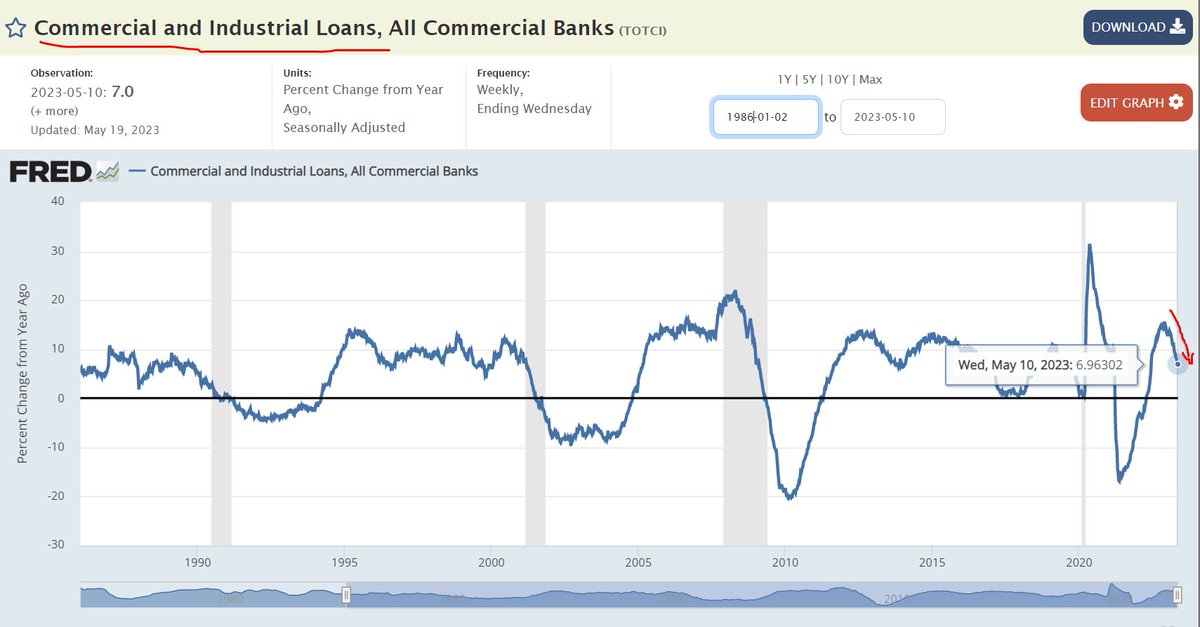

6) Rates are also going up just as bank lending is declining.

Take a look at Commercial & Industrial loan growth (loans to businesses).

Down from 15% to 7% growth YoY. And will likely keep falling.

Historically a big recession signal.

Take a look at Commercial & Industrial loan growth (loans to businesses).

Down from 15% to 7% growth YoY. And will likely keep falling.

Historically a big recession signal.

7) So yeah - hard to see how see higher rates don't break the economy and housing market.

And eventually result in lower rates.

Check out the blog post I wrote on the Reventure App website for more analysis. Free to read and subscribe!

reventure.app/blog/mortgage-…

And eventually result in lower rates.

Check out the blog post I wrote on the Reventure App website for more analysis. Free to read and subscribe!

reventure.app/blog/mortgage-…

• • •

Missing some Tweet in this thread? You can try to

force a refresh