While $FND has a fragmented base of over ~240 suppliers, many be unaware of $FND's largest & most important supplier & its high concentration in a particularly key flooring category

Some key notes...

Some key notes...

Per industry calls, $FND's largest supplier is Creative Flooring Solutions (CFL Flooring), previously known as China Floors

CFL serves as $FND's primary supplier of LVT making key private label brands like Nucor, AquaGuard and DuraLux. These are exclusive to $FND

CFL serves as $FND's primary supplier of LVT making key private label brands like Nucor, AquaGuard and DuraLux. These are exclusive to $FND

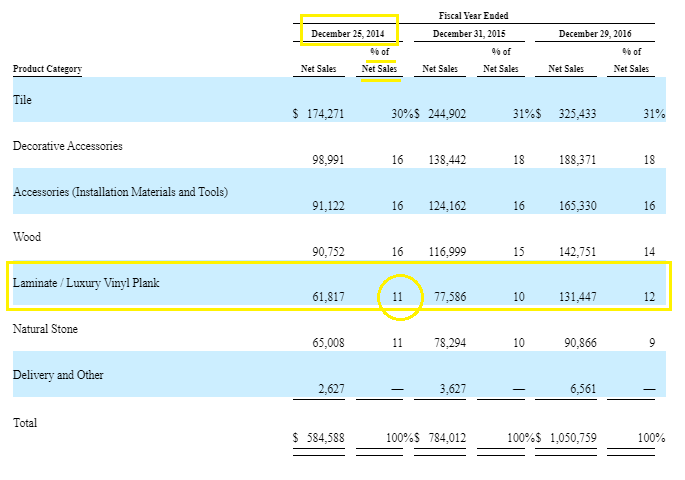

Per the 10-K, CFL makes up ~16% of $FND sales

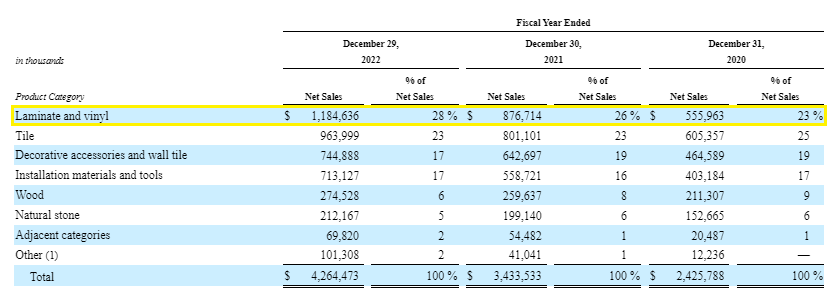

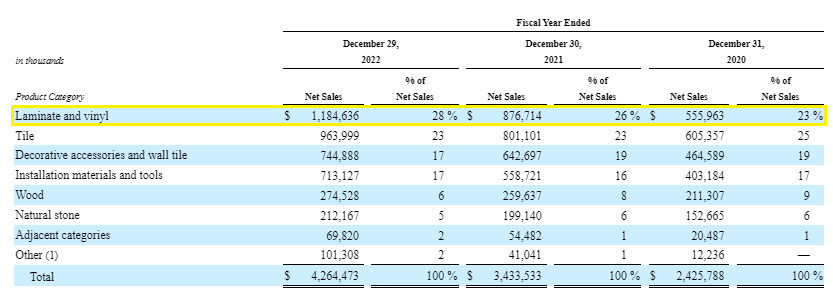

CFL only manufactures/sells LVT product. With LVT at ~28%/sales, this implies CFL supplies around ~60% of $FND's LVT

CFL only manufactures/sells LVT product. With LVT at ~28%/sales, this implies CFL supplies around ~60% of $FND's LVT

Implied est. from the 10-K of CFL at ~60% of LVT sales aligns with industry call commentary

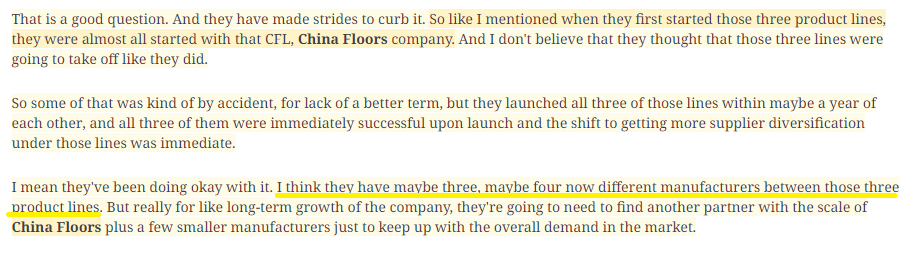

While high, CFL used to make up nearly all of $FND's sourced LVT at initial product launch – $FND now has at least ~3-4 suppliers for its LVT

While high, CFL used to make up nearly all of $FND's sourced LVT at initial product launch – $FND now has at least ~3-4 suppliers for its LVT

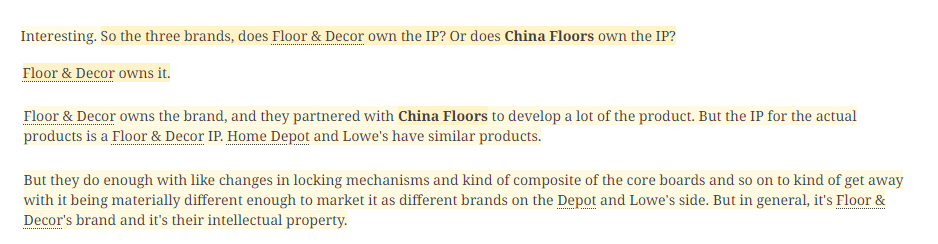

important to note here – $FND partnered with CFL to develop its private label LVT product lines (Nucor, AquaGuard, DuraLux, etc.) – while CFL is the manufacturer – $FND owns the IP, making the product lines exclusive to $FND

In addition, IP ownership allows $FND to contract with multiple other mfg. to make/source their private label LVT products

Some more background on CFL

- founded in 2004 in Shanghai by a group of European entrepreneurs

- while many $FND suppliers are small, CFL is large – having ~4,500 employees & five mfg. facilities that generate 70mln sq meters of flooring output

- founded in 2004 in Shanghai by a group of European entrepreneurs

- while many $FND suppliers are small, CFL is large – having ~4,500 employees & five mfg. facilities that generate 70mln sq meters of flooring output

While initially a fully China based business, CFL began diversifying its manufacturing footprint in 2018, with two new facilities operational in Vietnam and Taiwan in 2019 and a US based facility (Dalton, GA) operational in 2021

floorcoveringweekly.com/main/topnews/c…

floorcoveringweekly.com/main/topnews/c…

In total, CFL has five mfg, facilities:

China – 2

Taiwan – 1

Vietnam – 1

US – 1

China – 2

Taiwan – 1

Vietnam – 1

US – 1

Sources for the Calhoun, GA plant below

an interesting note is its about ~5mi down the road from a key $MHK plant & close to other flooring manufacturers facilities like Novalis (Dalton, GA)

gov.georgia.gov/press-releases…

an interesting note is its about ~5mi down the road from a key $MHK plant & close to other flooring manufacturers facilities like Novalis (Dalton, GA)

gov.georgia.gov/press-releases…

another item – for those unaware, LVT mfg. is more intense/complex then you may realize

CFL has several video snips of their plants in the US & Vietnam that provide some good visuals - see link

(sorry cannot link direct to each one)

vimeo.com/user16440064

CFL has several video snips of their plants in the US & Vietnam that provide some good visuals - see link

(sorry cannot link direct to each one)

vimeo.com/user16440064

CFL continues to scale alongside $FND – recently CFL raised capital from private equity (’21) and noted additional expansions of its Vietnam and US mfg. facilities back in April

cflflooring.com/cfl-flooring-e…

cflflooring.com/cfl-flooring-e…

So, to wrap up, why is the detail on CFL so important – why should you care?

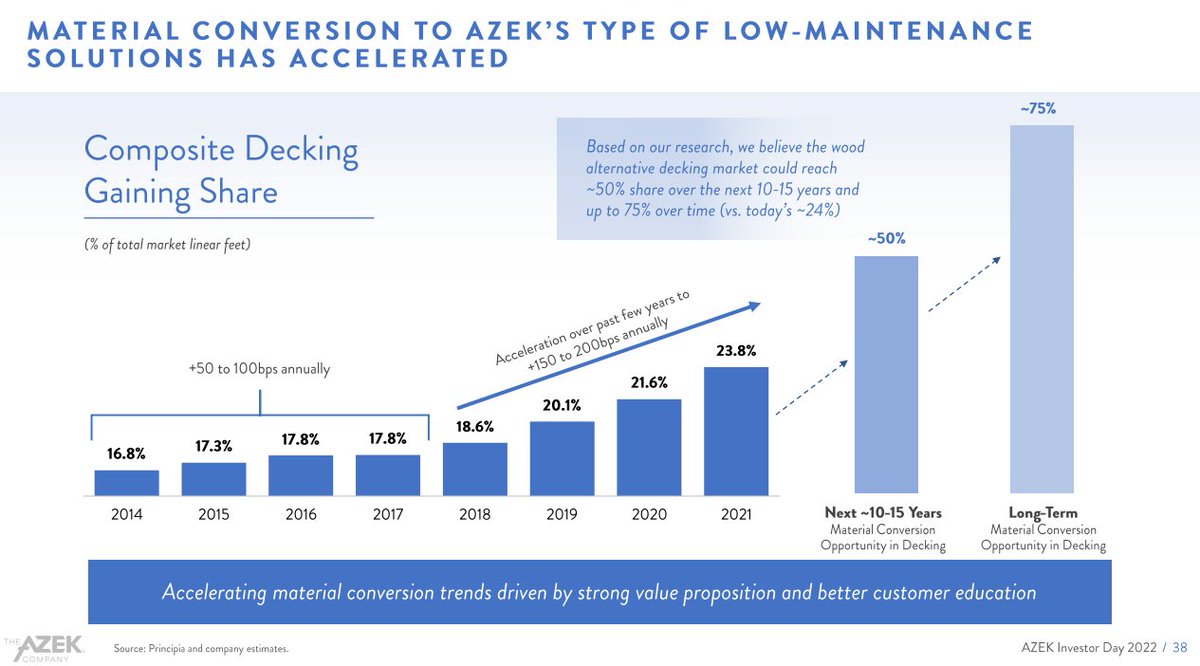

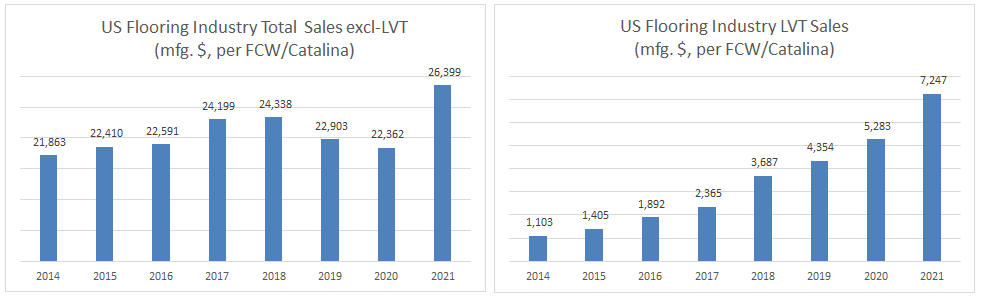

LVT is the most important and fastest growing flooring category – both for $FND and the industry at large

LVT is the most important and fastest growing flooring category – both for $FND and the industry at large

For example, over 2014-2022, $FND LVT sales grew +45%/yr., nearly 2x +25%/yr. growth for all other categories.

As a percent of sales, $FND LVT sales increased from 11% to 28% of sales over 2014-2022

As a percent of sales, $FND LVT sales increased from 11% to 28% of sales over 2014-2022

For the industry as a whole – over 2014-2021 – LVT sales grew +31%/yr – ~10x faster than +3%/yr growth in all other categories, going from ~5% to ~22% of total industry sales

Based on industry data from Floor Covering Weekly (FCW Statistical Reports)

floorcoveringweekly.com/main/research

Based on industry data from Floor Covering Weekly (FCW Statistical Reports)

floorcoveringweekly.com/main/research

LVT’s rapid rise is due to a superior value proposition for consumers:

- half the cost of wood/engineered flooring

- comparable in price to carpet

- attractive aesthetics vs. other categories

- easier to install

- innovative features like waterproofing

- half the cost of wood/engineered flooring

- comparable in price to carpet

- attractive aesthetics vs. other categories

- easier to install

- innovative features like waterproofing

All in, the LVT category is mission critical for a growth retailer like $FND

$FND's reliance and high concentration with a single supplier in the category is an important risk that investors should be fully aware of

$FND's reliance and high concentration with a single supplier in the category is an important risk that investors should be fully aware of

While $FND has diversified exposure to some extent, ~60% category exposure remains high

it seems highly unlikely that CFL would voluntarily drop $FND as a customer, given its rapid growth and LT potential in flooring,

it seems highly unlikely that CFL would voluntarily drop $FND as a customer, given its rapid growth and LT potential in flooring,

nonetheless – replacing lost supply from CFL with $FND's other LVT category suppliers would undoubtedly take substantial time and cause material disruption

• • •

Missing some Tweet in this thread? You can try to

force a refresh