Milestone Furniture - Auditor mil nahi raha h so as Financial data bhi nahi mil raha h

Co running without MD CEO CS

They intimated about the CEO resignation on 25th May-23 who actually resigned on 12th May-23

Promoter stake 0%

#Redflag

Co running without MD CEO CS

They intimated about the CEO resignation on 25th May-23 who actually resigned on 12th May-23

Promoter stake 0%

#Redflag

The same auditor on 26th May-23 signed the financials of Mangalam Organics - bseindia.com/xml-data/corpf…

Zero Revenue of the co #milestonefurniture

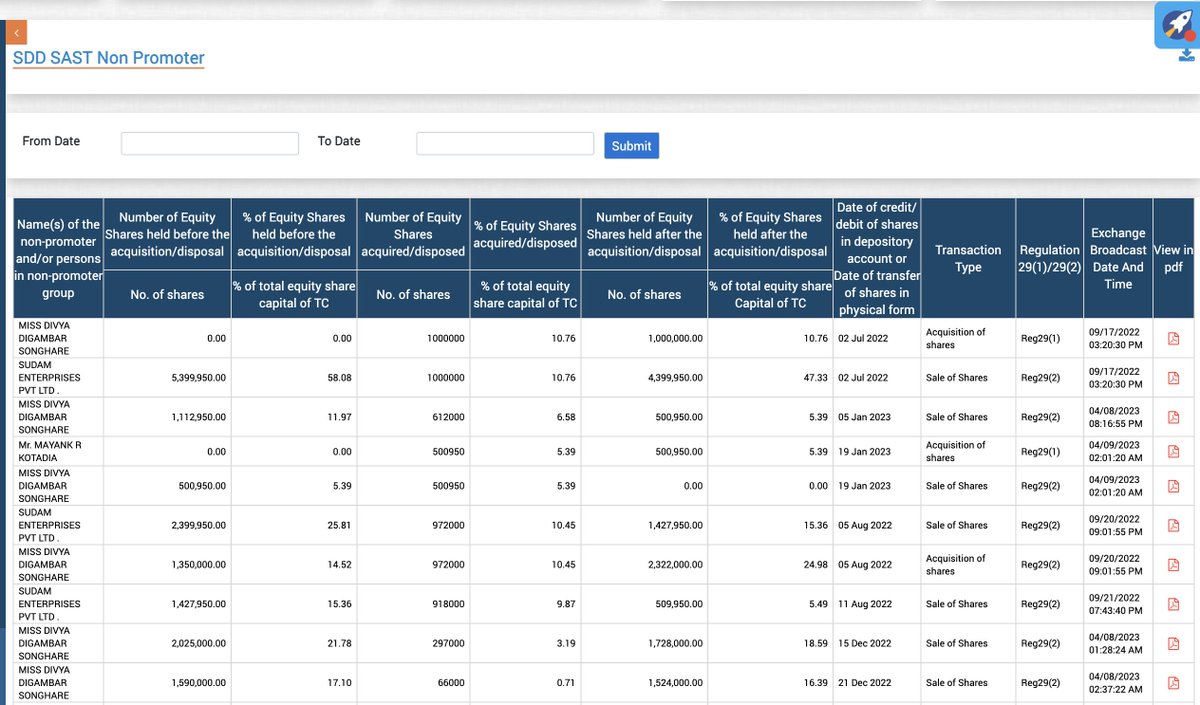

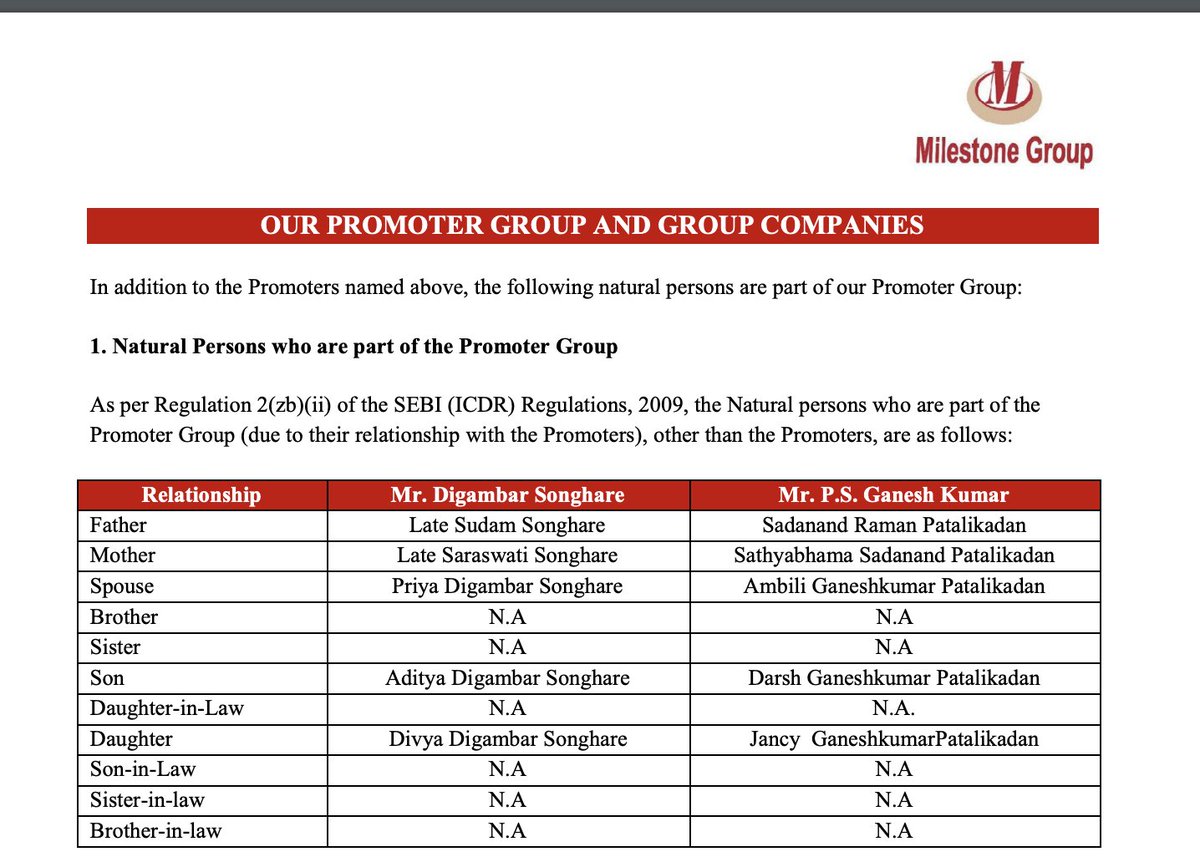

As per DRHP Promoter's daughter forms part of Promoter Group

As per BSE SDD data - its non-Promoter

How its possible when there in reclassification

Also this Sudam Enterprises includes promoter as the director

As per BSE SDD data - its non-Promoter

How its possible when there in reclassification

Also this Sudam Enterprises includes promoter as the director

Near to Zero Cash flows

Company has no CFO also. Already CS, MD, CEO resigned

No detailed shareholding pattern of Public shareholders disclosed for June-18

• • •

Missing some Tweet in this thread? You can try to

force a refresh