Pt 1 🧵TLDR: Two calls w/ Mike Gravely at the CEC have exponentially increased my conviction in staying heavily long EOSE with leverage. ~30% short interest unaware of the underlying forces driving the decision making in the CA long duration storage market.

Summarized notes from call #2 this afternoon:

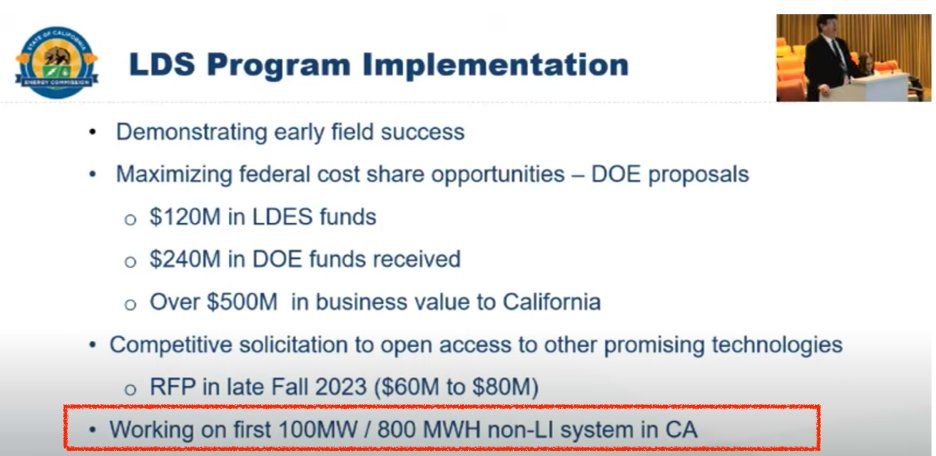

This 100 MW/800 MWh pending order [*SEEN BELOW IN RED, REVEALED LAST FRIDAY*] is a BIG DEAL and has second, and third order effects.

This 100 MW/800 MWh pending order [*SEEN BELOW IN RED, REVEALED LAST FRIDAY*] is a BIG DEAL and has second, and third order effects.

According to Mike, this first order is ~10x larger than anything Eos has ever booked. The renewable investor contacted the CEC inquiring about which OEM could fulfill a non-L-ion/LDES order of this magnitude.

The CEC recommended Eos because 1) Eos is the ONLY OEM that will have mfg capacity to ensure commissioning for desired 2025 timeframe (DOE loan), 2) Eos is the lowest-cost provider in the entire market (LDES/SDES) pricing well below L-Ion,

3) Long-term performance of Z3 equal to, if not better, than L-Ion, 4) no thermal runaway/fire risk, 5) ~100% US sourced materials.

This investor performed a 6-mo. independent assessment and has officially decided to go with Eos for a 20-year PPA. Further, it was concluded that no other OEM has the system maturity with deployments in the field or technology testing like Eos.

Right now, The CEC is trying to figure out which utility will accept this PPA and both parties are working thru how they get this project in the ISO queue where it can operate on the grid. The plan is to get this order finalized by September for mid-2025 commissioning.

They don’t have a site yet, or interconnection approval, and still need to do an environmental assessment, so still some work to be done. It was made clear Eos is much further ahead than ANY competitor in the LDES space, and the consensus opinion among renewable investors

seeking non-L-ion batteries is no other LDES is ready to ramp, and that Eos is the only credible solution for bigger systems > 100MW – the lion-share of utility-scale order size where nobody else can compete.

According to Mike, the significance of this 100 MW FIRST EVER non-L-ion order in CA is monumental because it would likely lead to at least two more 100 MW+ deals by ‘25. If this materializes, it equates to ~$500M in revenue at $300/KWh.

Mike said if Eos is able to get this deal across the finish line, Eos would be the most prominent technology out in the field. Mike also said once the DOE funds Eos’ capacity expansion, he believes Eos can get their book-to-bill conversion on a typical 100 MW/800 MWh system down

from 12-24 months to 6-9 months. He hinted Eos could DELIVER 1 GWh of storage in ’24 and 2+ GWh in ’25, equating to $300M and $500M+ respectively, just in California alone. He said with ~4 GWh of planned capacity (funded by DOE), Eos becomes competitive w/ incumbent L-Ion

We spoke about Form Energy, the private market darling of battery storage, who has raised a ton of money and is one of four key technologies that graduated from CA’s EPIC program w/ Eos. Mike said Form will undeniably be a big player in LDES, but they can’t “work the system”

like Eos can, and that Eos provides “significantly better value” to the grid for investors. In fact, 2.4 TW was curtailed last year because there was “nowhere to send it” and Form’s system “eats up too much energy”. Mike emphatically said CA needs POWER first, not ENERGY.

He believes Form will have a very hard time competing in 100 MW RFP’s vs. Eos. Mike cited a big order Form recently won but criticized their inability to deliver product until 2029! And that Form has not started to ramp up capacity to meet current market needs.

Mike reiterated CA’s 2035 goal of 19.5 GW of total battery storage, vs. 5 GW installed today (100% L-ion). He said the target split is ~70% L-ion (14 GW)/~30% non-lithium (6 GW). If Eos can capture 1/3 of the 6 GW TAM with an 8 hour system, equates to 16 GWh and close to

$5B in 1x product revenue and excludes high margin software and other services. Right now, the entire state of CA is running primarily 4 hr. battery systems. Why? because it’s the only available product. Mike & his team are currently working on researching the cost/benefit of

8 hr systems (Eos’ sweet spot). He said there was no market > 4 hr duration up until right now. Eos is unique because the Z3 can compete in the 2-4 hr market, and also 8-12 hr market. He said Eos is technically “mid duration”

storage and this is what sets their go-to-market strategy apart from other OEM’s who only target 10+ hours. In other words, Eos can aggressively penetrate 2 TAM’s with the dual use case of the Z3.

Mike hopes Eos is successful and strongly believes there is a high probability of success with executing on ramping up capacity given his relationship w/ Joe. He believes Eos is shaping up to be the industry leader and said Eos is on the path to becoming the “GE of LDES”.

Demand in CA for Z3 might be so strong, he foresees Eos potentially having to bring manufacturing capacity to CA after DOE helps build out Turtle Creek. Mike also believes L-ion prices are only going up, and that Eos over-time will have pricing power in the $300-350/KWh range.

Mike said Eos is essentially blitzing the market early as the lowest cost provider to rapidly gain share and influence adoption. Importantly, Mike sees a situation where the current installed base of L-ion battery systems are REPLACED by technologies like Eos Z3 due

to 1) better performance, and 2) lower cost curve. Mike said NYSERDA, the CEC-equivalent of CA to New York, is working in tandem with the CEC on analyzing/testing LDES technologies. Mike updates NYSERDA on decision making in CA and plans to introduce Eos

to the powers that be at NYSERDA. The CEC and NYSERDA currently work together on many solicitations, and “score” each other’s LDES orders. With the influence of the CEC, it appears there is a huge opportunity in the NY utility-scale market – the third biggest market behind

CA and TX – for Eos to blitz the market and gain share. As it relates to the DOE, Mike said direct to DOE: “if you can loan Eos the money, I can personally get them the grid-level orders”.

Pt 2🧵Mike hammered it home that Eos’ product maturity is superior, and in order to be ready to manufacture 1 GWh orders, one needs to have field experience to learn from. In his 30-year experience, he has never seen a battery OEM that didn’t change their entire technology/system

before the 2nd system was built. Eos has improved upon their technology 4 times already, and Mike said the Z3 is ready for commercialization.

I asked Mike if he owned Eos stock. He said No because he cant own it for conflict of interest reasons given he is making recommendations to renewable developers and for state legislature. I asked him if he COULD own it, would he? He said YES.

He went on to say “look at how low the price is!” and “I would not be surprised to see Eos “SUBSTANTIALLY HIGHER” as long as Joe can run the co. properly and scale up w/ DOE loan”.

Further, “if they go the way they’re going, they’re going to dominate the 100 MW order world” and that “Eos is the first one to walk thru the door, and there will be many more doors to open in CA if they can prove they can handle this order…

the rest of the world will see this 100 MW order signed, and they’ll want to go with Eos as a result of this investor being the first move…everyone will start to compare prices, and will see Eos as the lowest cost alternative”.

Lastly, “other competitors must get their price down to match Eos, or they are NOT going to make it”.

The end.

🔋🔋🔋🔋

The end.

🔋🔋🔋🔋

$EOSE

• • •

Missing some Tweet in this thread? You can try to

force a refresh