Contrarian small/micro cap investor focused on highly asymmetric event-driven/special situations with catalysts to unlock asset value & earnings power.

@ $3.75, $FF sports a $79M enterprise value with 51% of its cap in cash!!! $FF is off-the-radar aas it conducts no earnings calls, has no wall-street coverage, and has minimal investor engagement, e.g., the market has left for dead.

@ $3.75, $FF sports a $79M enterprise value with 51% of its cap in cash!!! $FF is off-the-radar aas it conducts no earnings calls, has no wall-street coverage, and has minimal investor engagement, e.g., the market has left for dead.

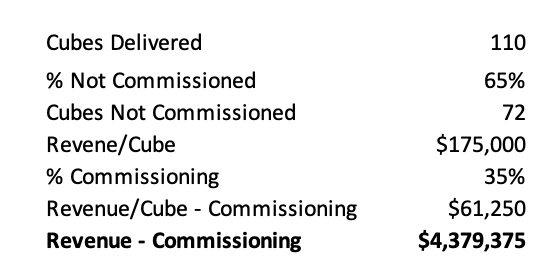

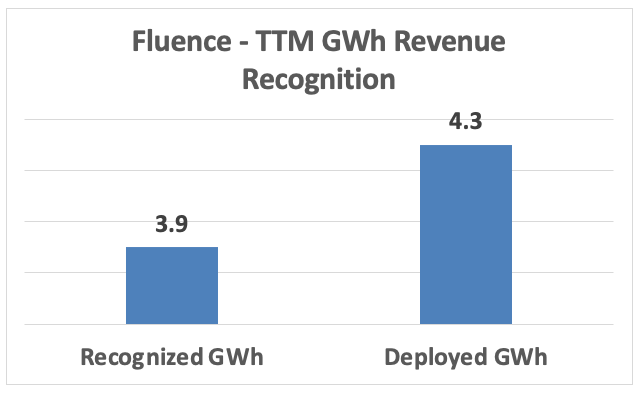

The golden nugget in the PR is this: 65% of cubes have not yet recognized revs. I think thats another ~$4M cash upside in Q2 as these batts get commissioned and CoD'd. - see math.

The golden nugget in the PR is this: 65% of cubes have not yet recognized revs. I think thats another ~$4M cash upside in Q2 as these batts get commissioned and CoD'd. - see math.

@x_times_1 @Umbisam

@x_times_1 @Umbisam

On a quarterly basis, rev rec will be lumpy for Tesla. Over a 12mo rolling period, it will smooth out.

On a quarterly basis, rev rec will be lumpy for Tesla. Over a 12mo rolling period, it will smooth out.