#Affordable Robotics🤖

#Thread 🧵

In the latest Investor presentation they came out with revenue projections

Targeting ~5500crs of Rev. in next 5 years from ARAPL & ARAPL RaaS

They are the only listed robotics co. in India with M.cap of just ~500crs

#Thread 🧵

In the latest Investor presentation they came out with revenue projections

Targeting ~5500crs of Rev. in next 5 years from ARAPL & ARAPL RaaS

They are the only listed robotics co. in India with M.cap of just ~500crs

They are currently into three segments

1.Robotic Welding

2.Multi level parking

3.Warehouse Automation ⭐️

Earlier they were mainly into 1st two segments in which they were witnessing reasonable growth.

1.Robotic Welding

2.Multi level parking

3.Warehouse Automation ⭐️

Earlier they were mainly into 1st two segments in which they were witnessing reasonable growth.

🚀But recently they forayed into Warehouse Automation which is going to be a major growth driver ahead.

The warehouse automation buss. is carried out in their WoS ARAPL Raas (80% ownership)

In Nov'21 they raised seed capital from Mr.Vijay Kedia for ARAPL RaaS

VK also holds 12%

The warehouse automation buss. is carried out in their WoS ARAPL Raas (80% ownership)

In Nov'21 they raised seed capital from Mr.Vijay Kedia for ARAPL RaaS

VK also holds 12%

For ARAPL RaaS their major focus is towards Exports rather than domestic markets. (US+Canada)

Bcz labour being cheap in India the demand for Warehouse automation is currently low.

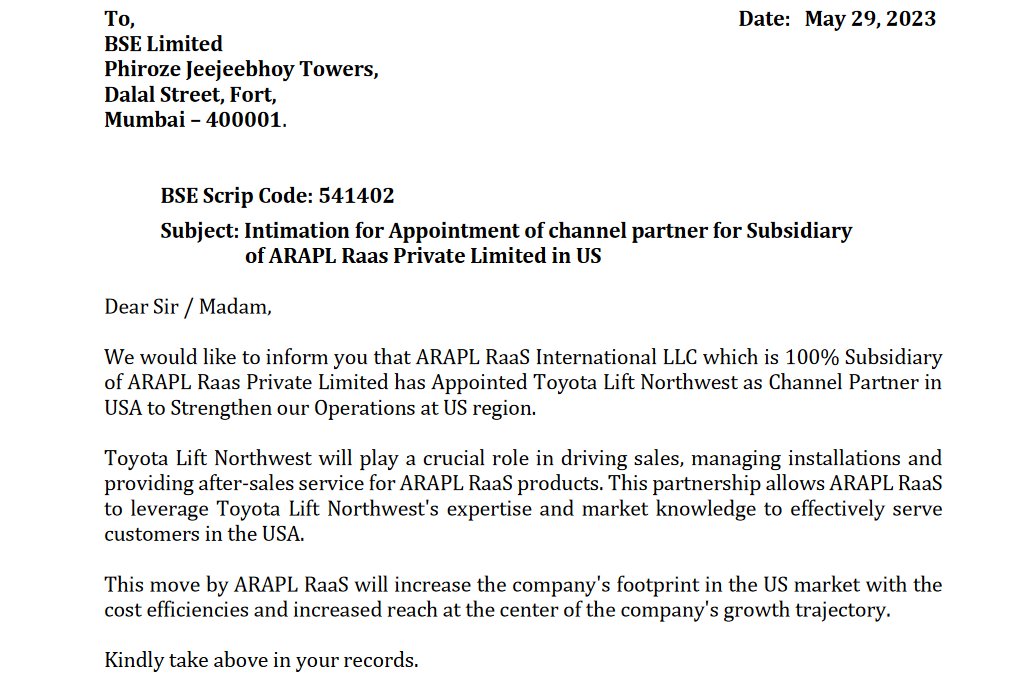

In May'23 they hv tied up with Toyota Lift northwest as channel partner for their US operations

Bcz labour being cheap in India the demand for Warehouse automation is currently low.

In May'23 they hv tied up with Toyota Lift northwest as channel partner for their US operations

In Warehouse robotics the major competition is from China

Chinese are ahead in terms of hardware quality but in terms of Software Indian co.'s are way ahead!!

Grey Orange one their competitors is valued at $2.5bn & is looking for Nasdaq Listing greyorange.com/company/leader…

Chinese are ahead in terms of hardware quality but in terms of Software Indian co.'s are way ahead!!

Grey Orange one their competitors is valued at $2.5bn & is looking for Nasdaq Listing greyorange.com/company/leader…

ARAPL does everything In-house from robot mfg. to software designing

Whereas most of their Indian competitors are importing from China & installing their own software

Whereas most of their Indian competitors are importing from China & installing their own software

Products:

Products like Zeus & atlas,only 3-4 co's in China are making it whereas others are just buying & putting their own software

Atlas - they are the only co. making battery operated autonomous forklift in India

Products like Zeus & atlas,only 3-4 co's in China are making it whereas others are just buying & putting their own software

Atlas - they are the only co. making battery operated autonomous forklift in India

The market opp. available for their products is approx. ~ $346bn which is huge

Even if they are able to capture minuscule share of this opp. the result will be huge

No, doubt this co. perfectly fits investment Style of Mr.Vijay Kedia (SMILE)

Even if they are able to capture minuscule share of this opp. the result will be huge

No, doubt this co. perfectly fits investment Style of Mr.Vijay Kedia (SMILE)

They hv also got patents & Proprietary soft. which shows that they are not a trading co. like their competitors

In March'23 ARAPL RaaS was valued at $30mn (~240crs)

There is a possibility that ARAPL will hv to liquidate more of their stake in ARAPL RaaS in future to raise funds

In March'23 ARAPL RaaS was valued at $30mn (~240crs)

There is a possibility that ARAPL will hv to liquidate more of their stake in ARAPL RaaS in future to raise funds

Apart from sale of Robots there will be another stream of rev. coming up in future.

Once u sell the robots u also need to maintain them & keep them up & working

which opens up the AMC revenue for ARAPL, which will further boost their margins

Once u sell the robots u also need to maintain them & keep them up & working

which opens up the AMC revenue for ARAPL, which will further boost their margins

The rev. from AMC will be lower in initial years bcz they will need to provide it for free but as the time passes they will be getting huge stream of revenue from this buss. & it will be high margin & recurring.

Now ARAPL which is listed entity will be manufacturing the robots

Now ARAPL which is listed entity will be manufacturing the robots

Whereas the ARAPL RaaS will be selling it & providing all the service.

The reason this was done in order to get good valns. & funding for ARAPL RaaS

Currently for FY24 they are targeting Rs.200+crs of rev with ~10% ebitda margins

The reason this was done in order to get good valns. & funding for ARAPL RaaS

Currently for FY24 they are targeting Rs.200+crs of rev with ~10% ebitda margins

Although the stock has run up alot in last 1 year up more than 3.5x

But given the opportunity size & their capabilities it looks like they have a long way to go.

Lastest concall had alot of info. regarding their future plans

Not a reco. https://t.co/sEW8AHVNuParapl.co.in/videos/

But given the opportunity size & their capabilities it looks like they have a long way to go.

Lastest concall had alot of info. regarding their future plans

Not a reco. https://t.co/sEW8AHVNuParapl.co.in/videos/

• • •

Missing some Tweet in this thread? You can try to

force a refresh