Stifel on the recent Vital Energy deal:

"While dilutive to our 2024 EV/EBITDA multiple, the transactions are accretive on FCF, leverage, and inventory metrics and provide management increased scale to drive further value through operational and cost of capital synergies."

I generally agree. I own shares of $vtle, no recommendation, do not rely.

"While dilutive to our 2024 EV/EBITDA multiple, the transactions are accretive on FCF, leverage, and inventory metrics and provide management increased scale to drive further value through operational and cost of capital synergies."

I generally agree. I own shares of $vtle, no recommendation, do not rely.

More from Stifel on Vital:

Valuation and recommendation: We reiterate our Buy rating and 12-month target price of $122.00/share.

Valuation and recommendation: We reiterate our Buy rating and 12-month target price of $122.00/share.

"Protect the downside and the upside will take care of itself"

Relevant for this latest deal, and you won't believe who said it!

Relevant for this latest deal, and you won't believe who said it!

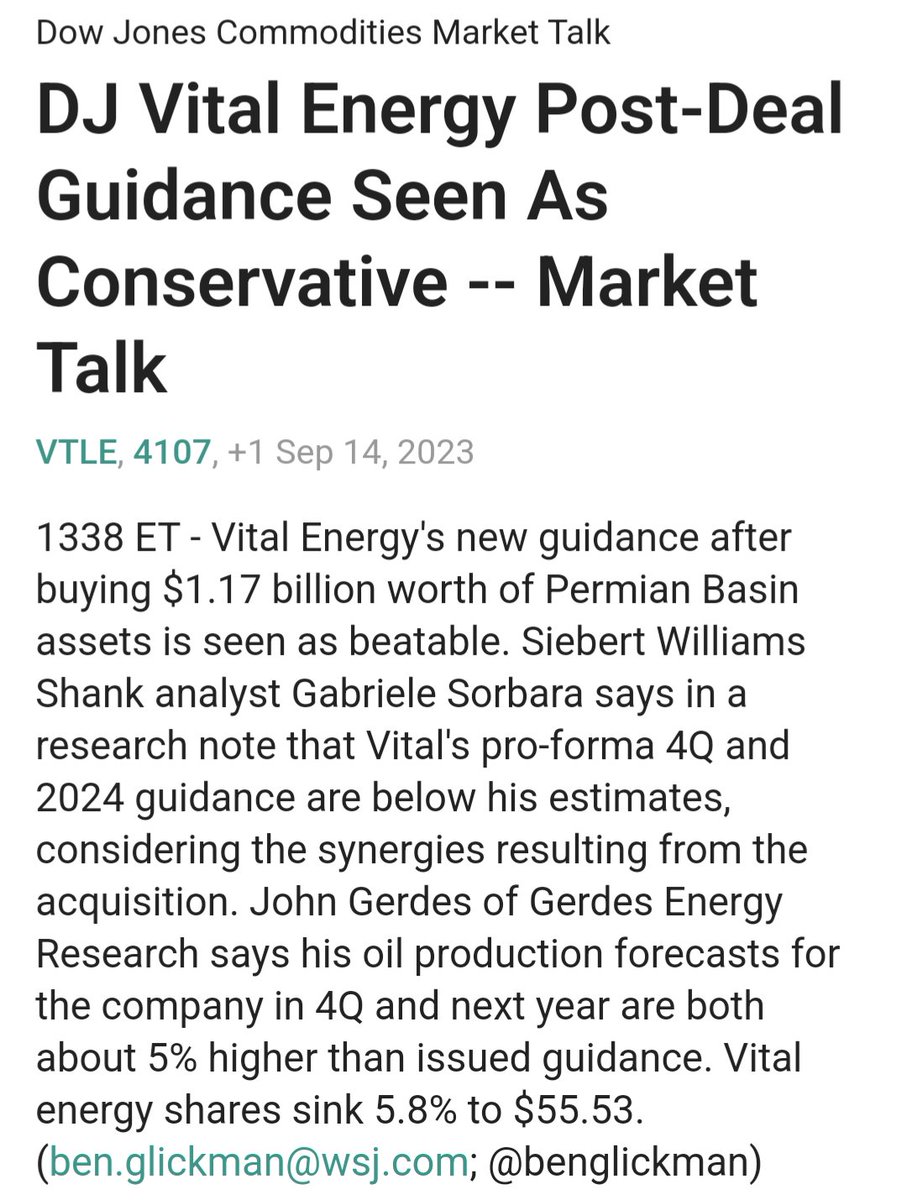

Interesting from Dow Jones on Vital: "new guidance ... is beatable"

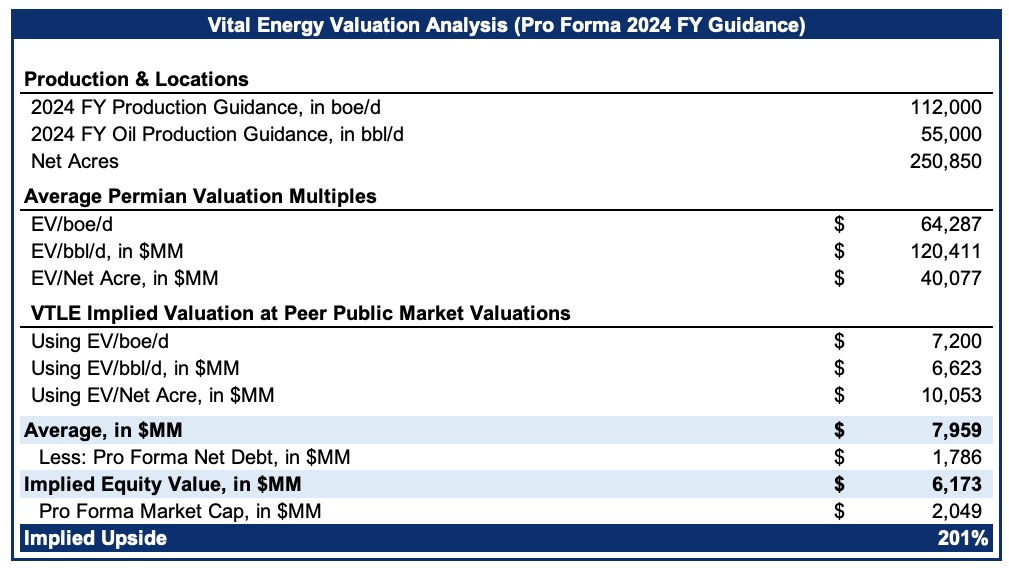

This may be what Vital's management is playing for. Re-rating to the average valuation of publicly traded Permian producer peers implies 200% upside.

I own shares of $vtle, not a recommendation, don't rely.

I own shares of $vtle, not a recommendation, don't rely.

Enverus: $VTLE was down 8% on the day ... The market was likely spooked by the EBITDA dilution as well as the additional issuance of both common and preferred equity. Most buyers funding deals with secondary equity offerings initially saw share price declines that subsequently recovered.

Enverus: "We view the deals as a net positive for VTLE as they increase the firm’s sub-$50 WTI breakeven inventory life.

The transactions should make VTLE more attractive to both investors and, if the stock doesn’t rerate, ultimately large-cap buyers."

I generally agree:

The transactions should make VTLE more attractive to both investors and, if the stock doesn’t rerate, ultimately large-cap buyers."

I generally agree:

@Istateyourname7 @BisonInterests Also, at a very low valuation, there is a substantial margin of safety. The lower the valuation, the less risk to the investor from company under-performance, market downturns, etc.

This is the basis of value investing, as practiced by Buffett, Klarman and others.

This is the basis of value investing, as practiced by Buffett, Klarman and others.

• • •

Missing some Tweet in this thread? You can try to

force a refresh