It is time to redefine traditional portfolios.

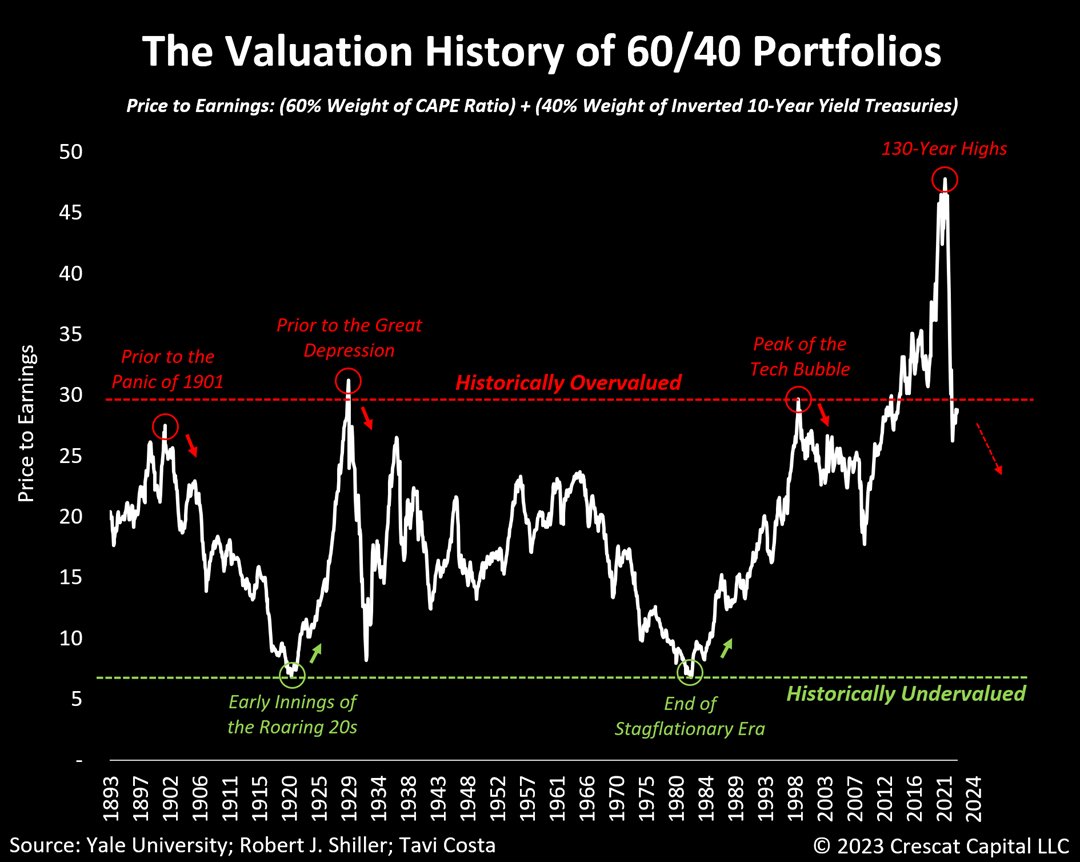

The valuation history of 60/40 portfolios unfolds through extended cycles, and we are now experiencing another critical juncture in this dynamic.

Thread 👇👇👇

The valuation history of 60/40 portfolios unfolds through extended cycles, and we are now experiencing another critical juncture in this dynamic.

Thread 👇👇👇

Conventional investment strategies are poised to undergo a significant restructuring, placing a prominent emphasis on investments in hard assets.

In August 2021, the combined valuation of overall equities and US Treasuries had reached its most expensive level in 130 years.

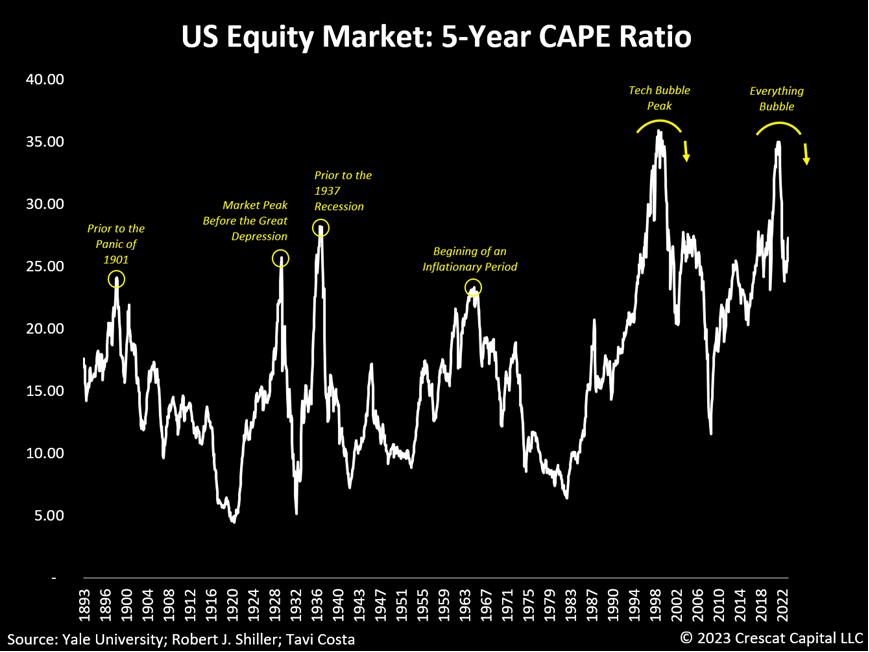

*This chart below is simply the price/earnings version of the first one.

*This chart below is simply the price/earnings version of the first one.

To put the current valuation imbalance into perspective:

Its recent peak was a staggering 61% higher than its previous peak in the early 2000s.

Its recent peak was a staggering 61% higher than its previous peak in the early 2000s.

Although prices have corrected somewhat, particularly in the Treasury market:

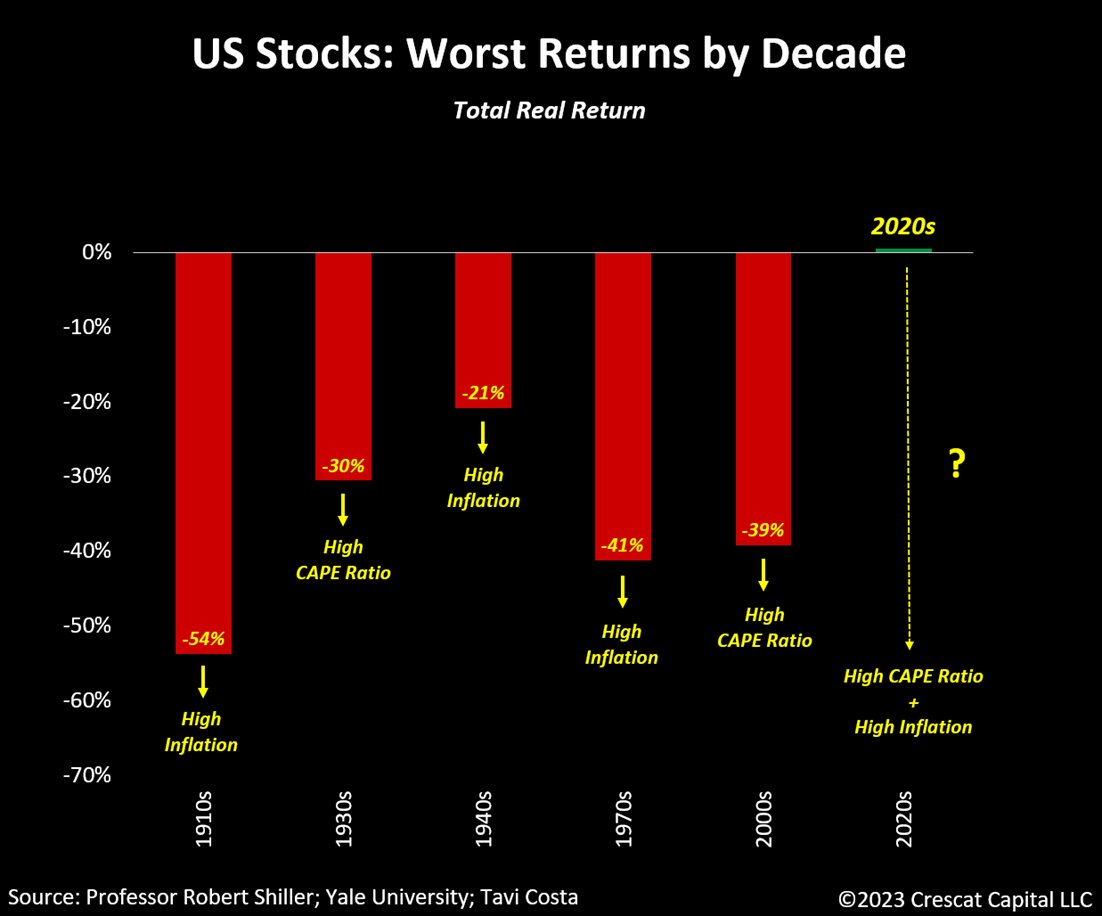

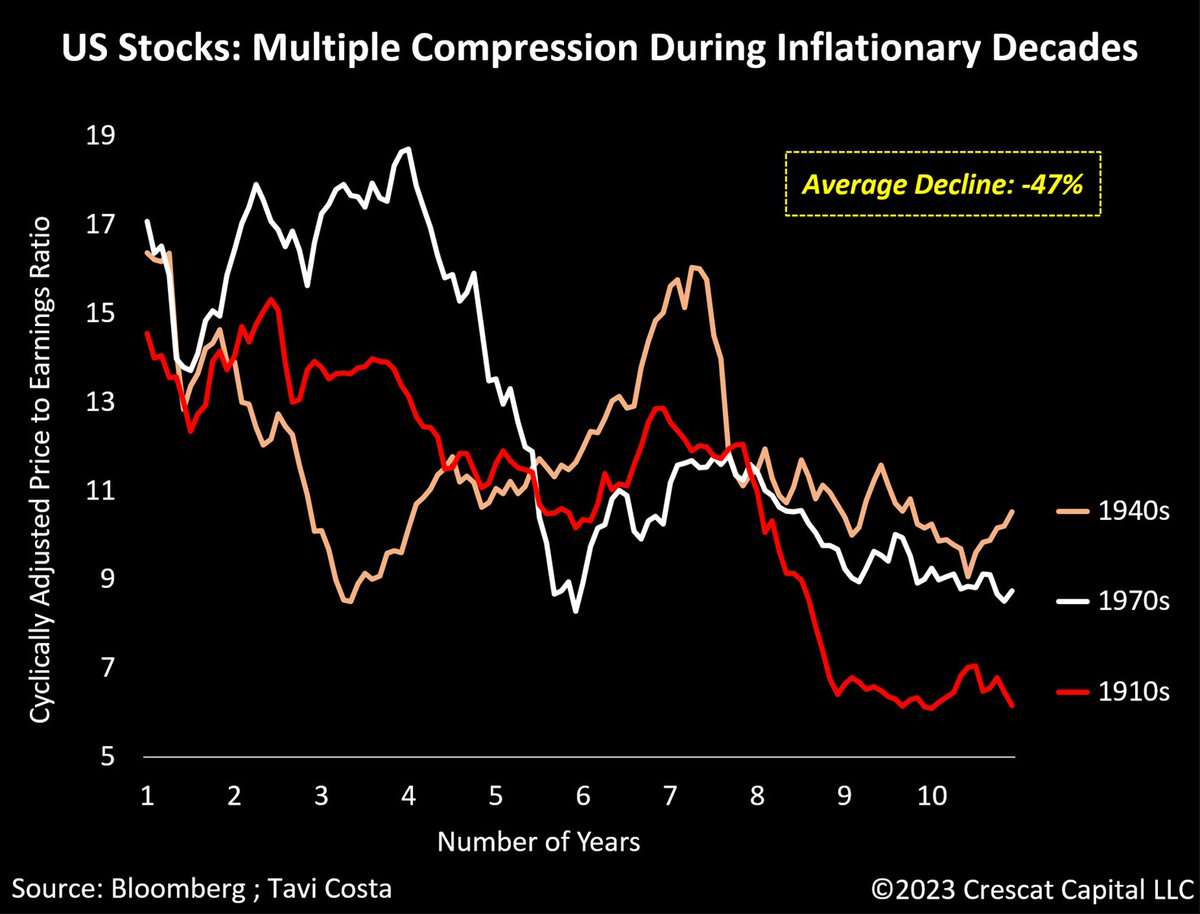

Today’s elevated multiples still bear resemblance to periods that preceded significant economic downturns, such as the Great Depression of 1929 and the Tech Bust of 2001.

Today’s elevated multiples still bear resemblance to periods that preceded significant economic downturns, such as the Great Depression of 1929 and the Tech Bust of 2001.

The rise in popularity and the success of these traditional investment strategies in recent decades can be credited to a period characterized by disinflation, fostering one of the most speculative environments in the history of financial markets.

The shifting dynamics of capital moving away from crowded equity and fixed-income holdings, as investors seek new investment opportunities, could have profound implications in markets.

This is where gold and commodities are poised to play a major role in this transitional phase.

This is where gold and commodities are poised to play a major role in this transitional phase.

As is widely recognized:

The 40% segment of these conventional portfolios, mainly comprised of fixed-income assets, has been facing substantial challenges.

This has led to fundamental questions about the potential need to restructure these allocations.

The 40% segment of these conventional portfolios, mainly comprised of fixed-income assets, has been facing substantial challenges.

This has led to fundamental questions about the potential need to restructure these allocations.

The main reason why investors include this portion in their portfolios is primarily because they are in search of safe-haven assets with minimal downside volatility.

Especially those that tend to perform well during economic downturns.

Especially those that tend to perform well during economic downturns.

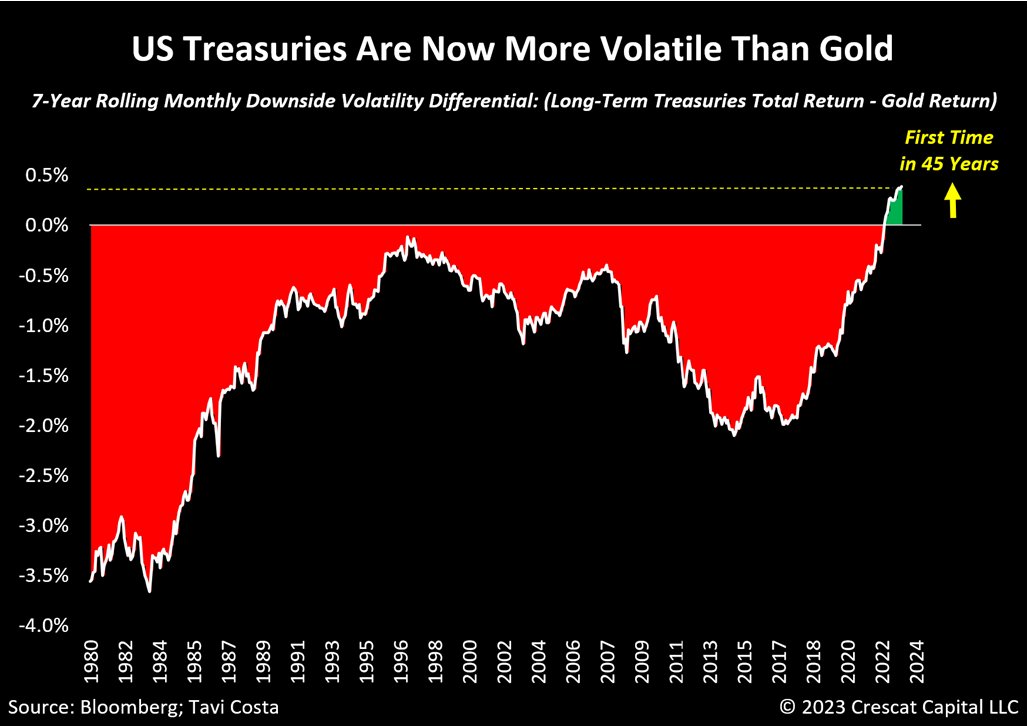

Nevertheless, institutions should deeply reflect upon this crucial analysis:

For the first time in 45 years, US Treasuries have exhibited higher downside volatility than gold.

For the first time in 45 years, US Treasuries have exhibited higher downside volatility than gold.

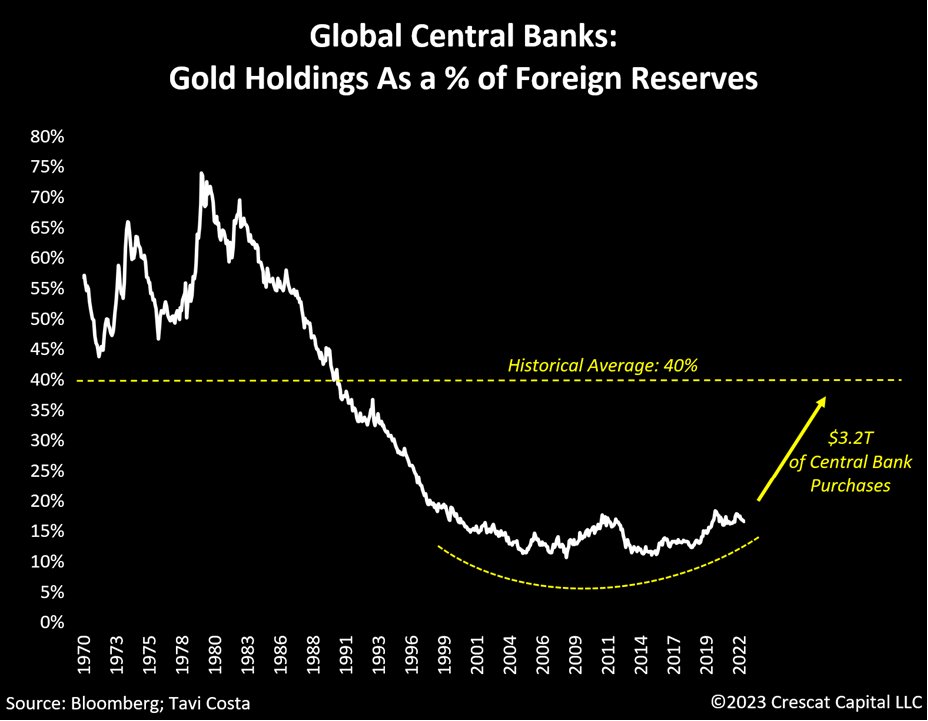

It’s noteworthy that global central banks have already begun to accumulate gold for their own reasons.

This effort is essential in order to elevate the standard of quality for their international reserves after enduring an extended period of imprudent monetary policy decisions.

This effort is essential in order to elevate the standard of quality for their international reserves after enduring an extended period of imprudent monetary policy decisions.

Rather than loading their balance sheets with debt instruments from another historically indebted economy:

It is imperative for central banks to hold a neutral alternative with centuries of proven credibility as a hard asset to become the cornerstone of their monetary systems.

It is imperative for central banks to hold a neutral alternative with centuries of proven credibility as a hard asset to become the cornerstone of their monetary systems.

We anticipate that these policy changes will exert significant influence on other major institutions, which are likely to gradually adopt gold as a haven alternative over time.

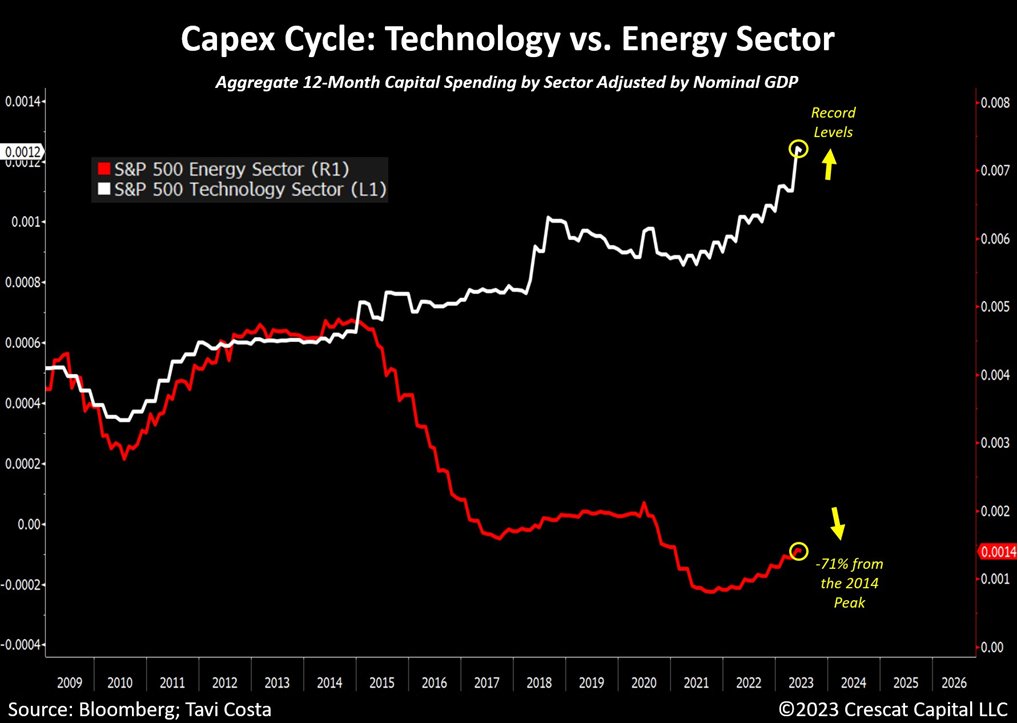

One important reason why inflationary forces persist so prominently today can be attributed to the striking disparity in capital allocation between technology and resource industries, a problem that remains historically notable.

This is indeed a concerning matter, emphasizing the prevailing investor concentration on one sector of the market, often at the expense of businesses that remain fundamental to our economy today.

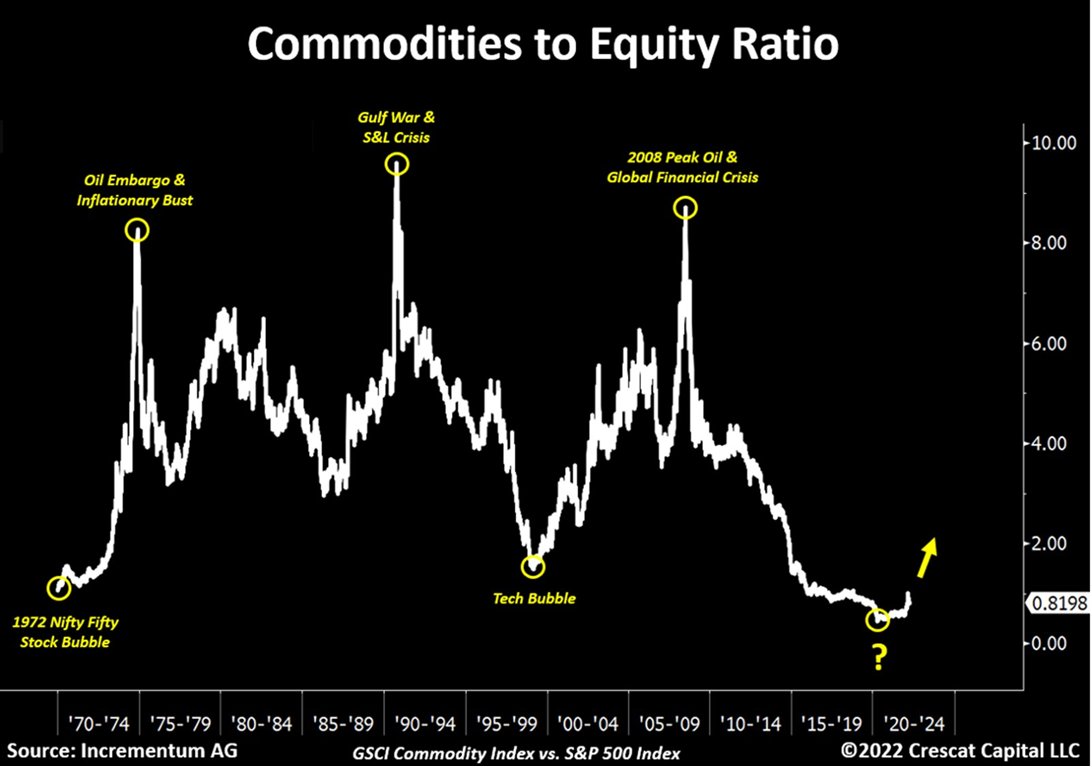

There is a reason why the commodity-to-equity ratio remains near historical lows.

There is a reason why the commodity-to-equity ratio remains near historical lows.

It's crucial to remember that resource industries necessitate sustained, substantial capital investments to address their supply constraints.

This is the primary reason why commodity cycles unfold gradually and often evolve over long-term trends.

This is the primary reason why commodity cycles unfold gradually and often evolve over long-term trends.

If the reshoring trend is real, we are still in the very early stages.

Note on the chart below how manufacturing used to make up almost 30% of the US economy back in the 1950s and today makes up only 10%.

Note on the chart below how manufacturing used to make up almost 30% of the US economy back in the 1950s and today makes up only 10%.

Back to the case of owning tangible assets:

It can be challenging for most people to grasp the idea of hard assets becoming a reliable alternative to traditional portfolios.

Especially when looking at their underperformance during the GFC in contrast to US Treasuries.

It can be challenging for most people to grasp the idea of hard assets becoming a reliable alternative to traditional portfolios.

Especially when looking at their underperformance during the GFC in contrast to US Treasuries.

To fully comprehend this concept:

One needs a deeper understanding of historical patterns, acknowledging that different asset correlations emerge during inflationary periods.

One needs a deeper understanding of historical patterns, acknowledging that different asset correlations emerge during inflationary periods.

An important reminder:

Developed economies are currently facing a chronic debt crisis, with deeply entrenched inflationary pressures propelled by escalating deglobalization, reckless fiscal spending, worsening inequality, and limited access to essential natural resources.

Developed economies are currently facing a chronic debt crisis, with deeply entrenched inflationary pressures propelled by escalating deglobalization, reckless fiscal spending, worsening inequality, and limited access to essential natural resources.

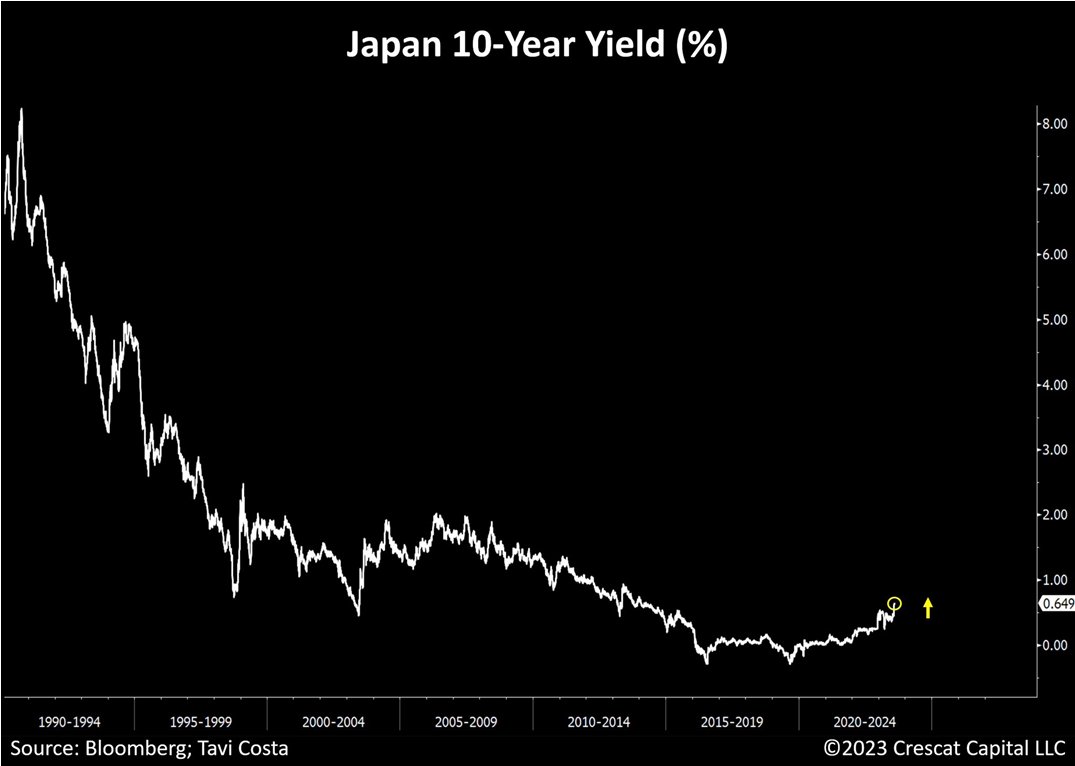

The Japanese economy is a compelling case study of a country that has suffered from a prolonged period of monetary and fiscal indiscipline.

The fact that the Bank of Japan has made repeated attempts to alleviate the mounting cost of debt, even with 10-year interest rates at a mere 0.7%.

That arguably stands as one of the most significant macro events in recent times and is a roadmap for the broader global economy.

That arguably stands as one of the most significant macro events in recent times and is a roadmap for the broader global economy.

The Japanese economy’s reliance on continuous government intervention vividly underscores the magnitude of the present debt crisis.

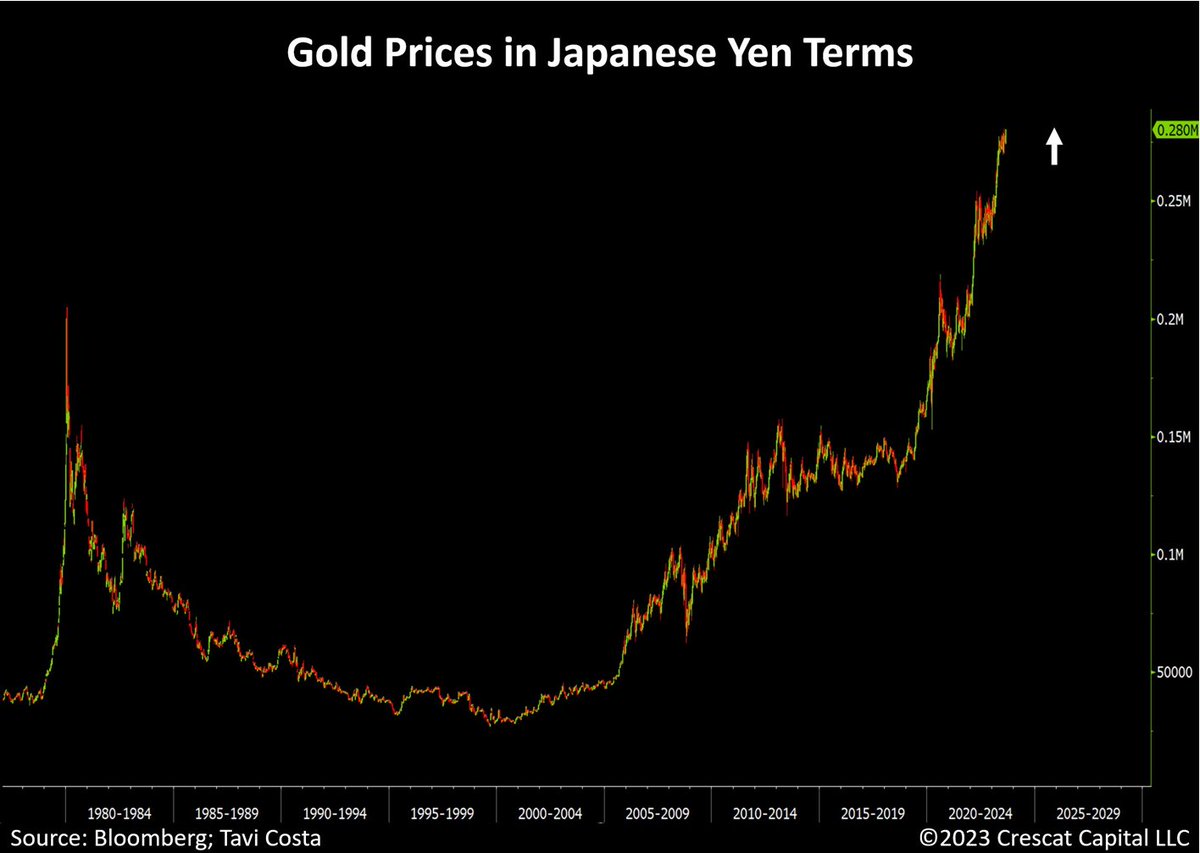

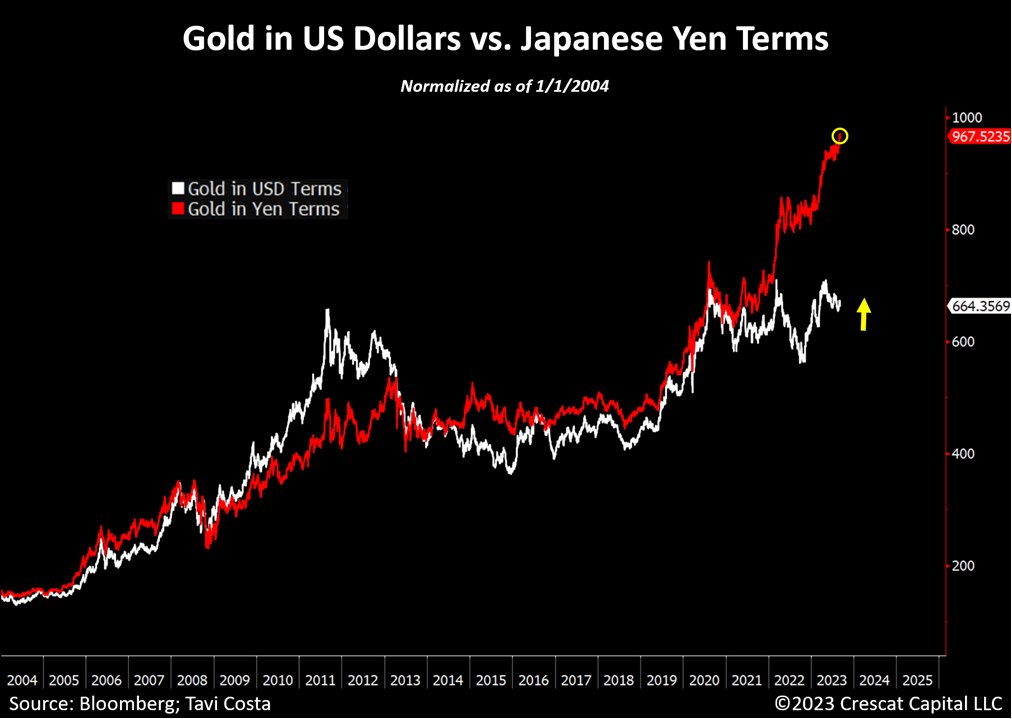

It is no surprise that gold prices in Japanese Yen terms persistently reach record levels.

It is no surprise that gold prices in Japanese Yen terms persistently reach record levels.

Make no mistake; this situation is not exclusive to Japan.

The Fed, the European Central Bank, the Bank of England, the People’s Bank of China, and others are on the brink of confronting the very same predicament.

The Fed, the European Central Bank, the Bank of England, the People’s Bank of China, and others are on the brink of confronting the very same predicament.

In a world burdened by historical levels of debt, it’s important to remember that over time, all paper currencies should lose value against hard assets.

In our strong view, the yen is just an early mover.

In our strong view, the yen is just an early mover.

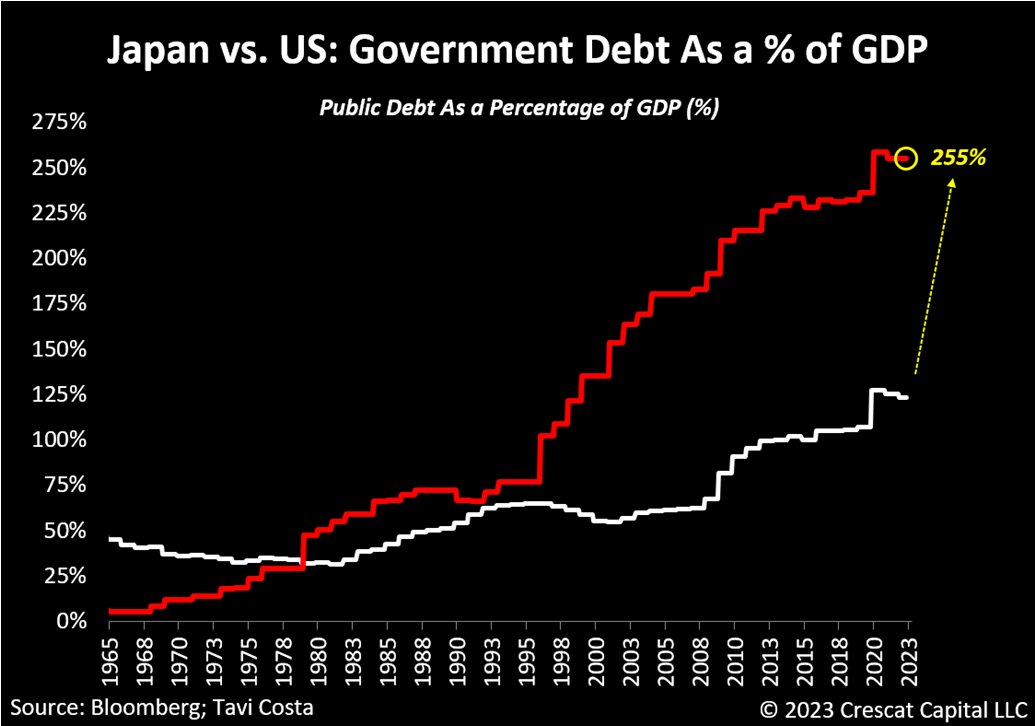

Note that if we use Japan as an example, there is substantial potential for the deterioration of US government debt.

Similar to the steps taken by the Bank of Japan, even in the face of prevailing inflationary pressures:

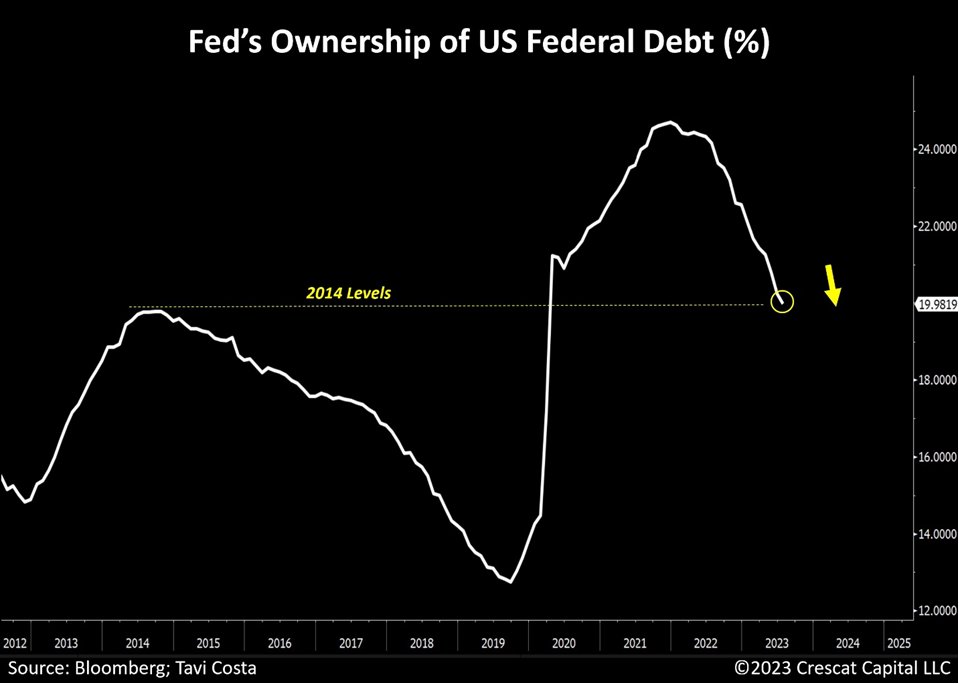

Central banks in heavily indebted economies inevitably find themselves compelled to become the primary purchasers of their own government debt.

Central banks in heavily indebted economies inevitably find themselves compelled to become the primary purchasers of their own government debt.

The current monetary policy in the US is starkly misaligned with the surge in Treasury issuances and the prevailing levels of fiscal irresponsibility.

Another popular argument against the idea of investing in tangible assets, particularly gold, is the challenge posed by rising interest rates, as it may seem less attractive to hold an asset that doesn’t yield anything.

However, historical examples contradict this notion.

However, historical examples contradict this notion.

In fact:

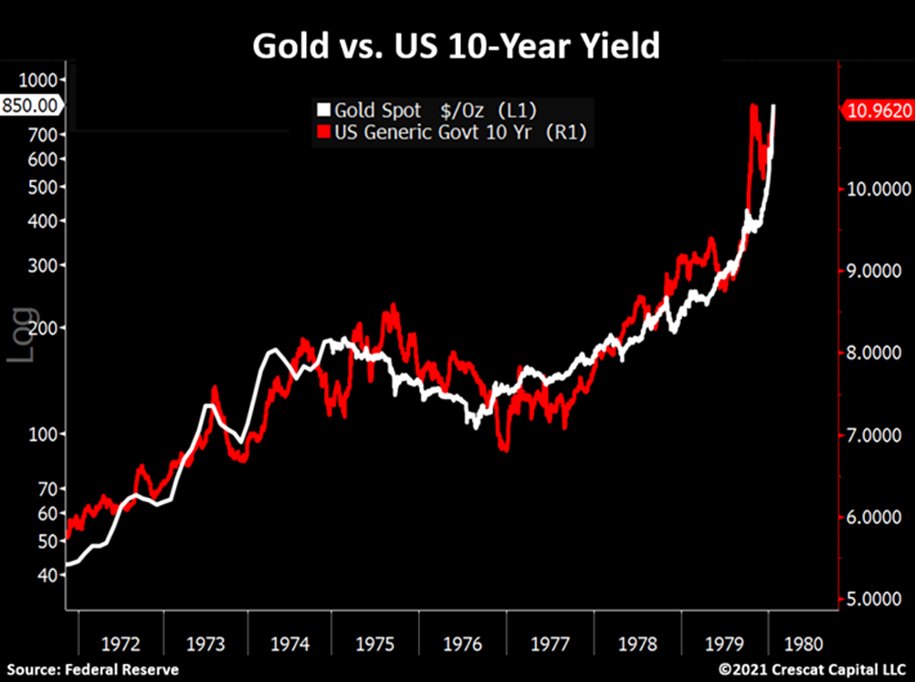

Gold delivered some of its strongest performances during the 1970s, despite the backdrop of increasing interest rates.

Gold delivered some of its strongest performances during the 1970s, despite the backdrop of increasing interest rates.

This trend isn’t limited to that specific decade; you can find similar instances in the 1910s and 1940s.

While gold prices may not have been freely floating during those periods, other tangible assets, such as commodities, demonstrated remarkable performance.

While gold prices may not have been freely floating during those periods, other tangible assets, such as commodities, demonstrated remarkable performance.

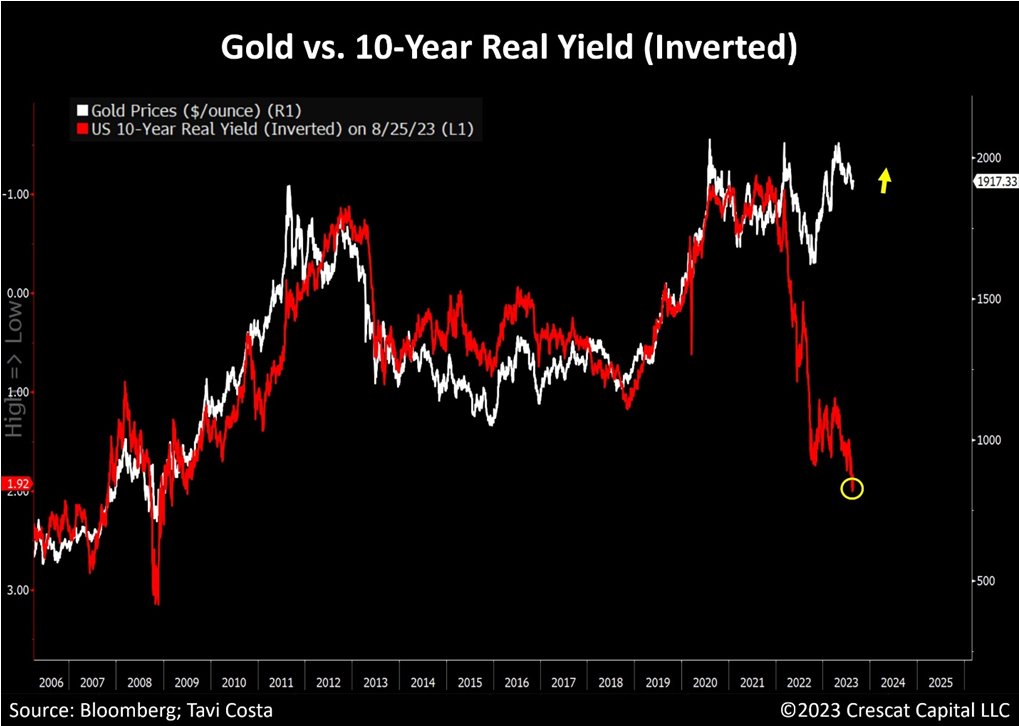

There is a clear and compelling reason why the current price of gold remains impressively resilient despite the pressure from real rates.

The weakening of the correlation between inflation-adjusted yields and precious metals is becoming more apparent.

The weakening of the correlation between inflation-adjusted yields and precious metals is becoming more apparent.

With inflation running hotter than historical standards, gold is highly likely to decouple from Treasury prices, much like it did during the 1970s.

Who would have thought that in such an intricate macro environment, there would be so many skeptics about owning hard assets?

Who would have thought that in such an intricate macro environment, there would be so many skeptics about owning hard assets?

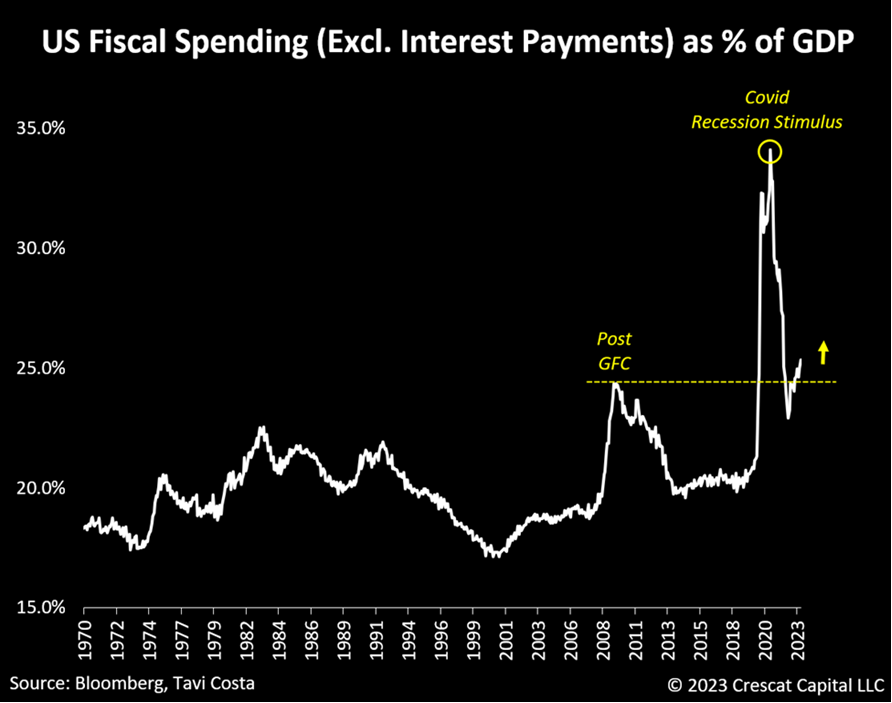

Today’s fiscal spending is indeed highly inflationary.

Many recent articles have suggested otherwise, as a substantial portion of it is driven by the sharp rise in interest payments.

However, it’s important to note that this perspective is not entirely accurate.

Many recent articles have suggested otherwise, as a substantial portion of it is driven by the sharp rise in interest payments.

However, it’s important to note that this perspective is not entirely accurate.

Even without factoring in the cost of servicing the debt, fiscal spending alone represents over 25% of GDP.

Today’s government expenditure has already surpassed the levels seen after the GFC.

The notable distinction is that we haven’t experienced an economic downturn yet.

Today’s government expenditure has already surpassed the levels seen after the GFC.

The notable distinction is that we haven’t experienced an economic downturn yet.

What’s even more important:

Apart from the Covid recession, we have not witnessed such a substantial scale of government stimulus in the past half-century.

The lack of fiscal discipline is likely to persist as a prominent driver of inflation.

Apart from the Covid recession, we have not witnessed such a substantial scale of government stimulus in the past half-century.

The lack of fiscal discipline is likely to persist as a prominent driver of inflation.

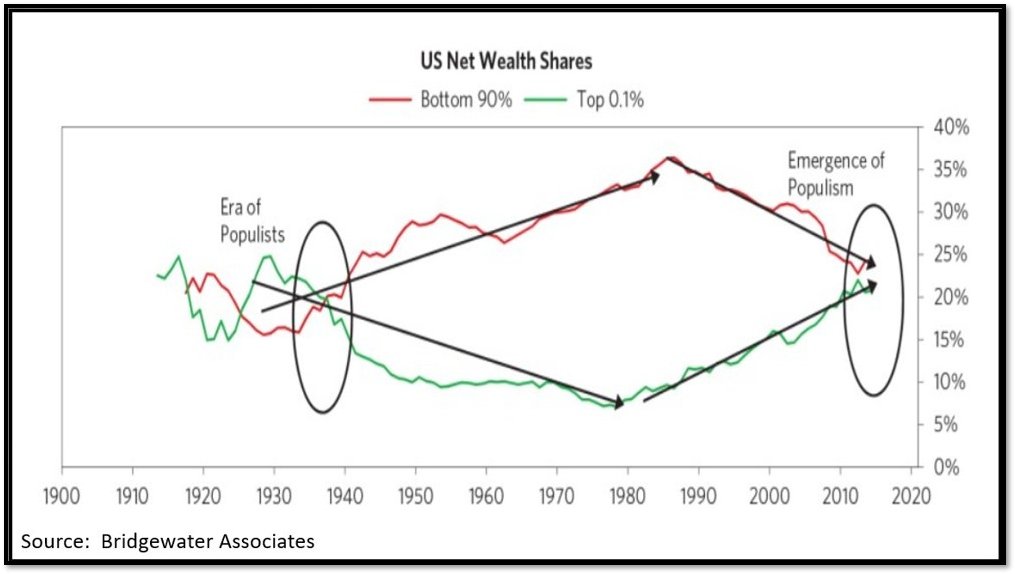

A notable contrast to the inflationary period of the 1970s is the prominence of today’s inequality problem.

That is a fundamental issue that often leads to further social programs, and as a result, an increase in government spending.

That is a fundamental issue that often leads to further social programs, and as a result, an increase in government spending.

Different from the broad wage-price spiral experienced back then:

The convergence of the current wealth gap disparity and a substantially elevated cost of living is set to concentrate growing wage pressure among the broad population in the lower and middle-income groups.

The convergence of the current wealth gap disparity and a substantially elevated cost of living is set to concentrate growing wage pressure among the broad population in the lower and middle-income groups.

This situation mirrors what is often witnessed in emerging markets.

To confront these challenges, governments tend to prioritize extensive fiscal stimulus measures aimed directly at addressing populist social welfare issues, thereby exacerbating the inflationary problem.

To confront these challenges, governments tend to prioritize extensive fiscal stimulus measures aimed directly at addressing populist social welfare issues, thereby exacerbating the inflationary problem.

Developed economies are starting to adopt similar social policies, although these trends are still in their early phases.

This is expected to contribute significantly to increased government spending as time progresses.

This is expected to contribute significantly to increased government spending as time progresses.

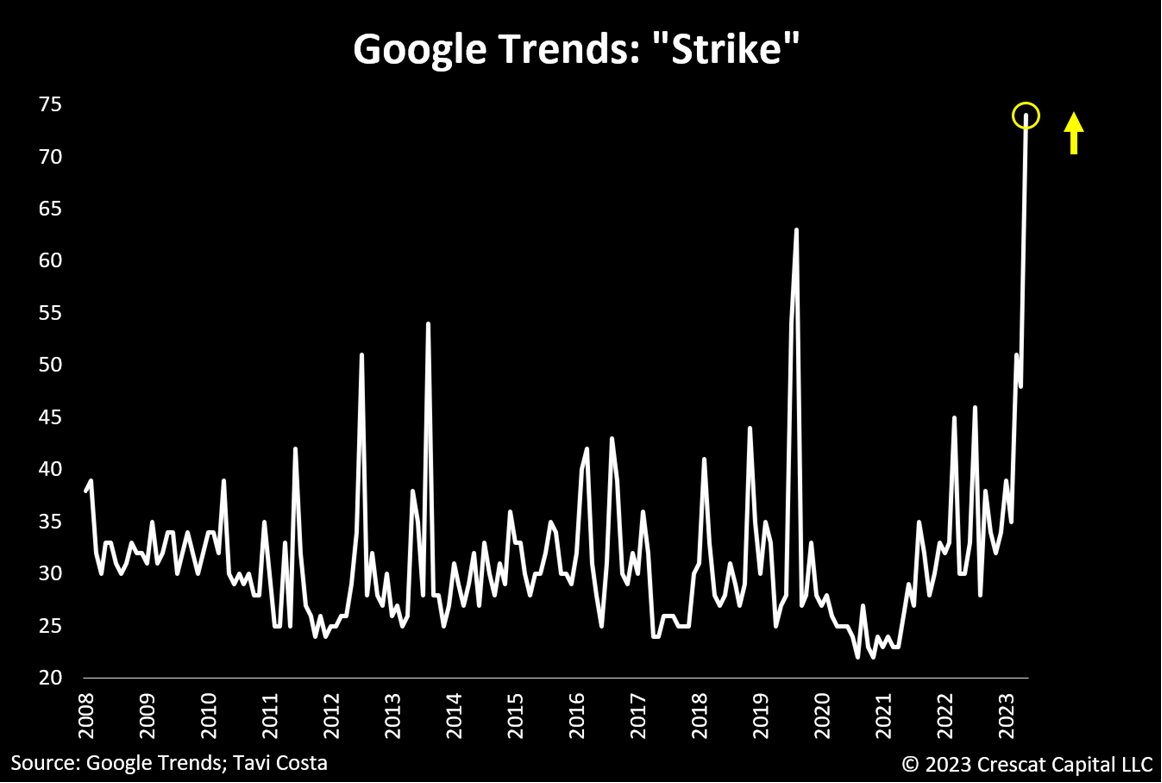

Also, as a result of wealth gap issues:

We are experiencing a proliferation of labor strikes, and the growing wage pressure is becoming increasingly evident.

These are unmistakable signs of an inflationary setting.

We are experiencing a proliferation of labor strikes, and the growing wage pressure is becoming increasingly evident.

These are unmistakable signs of an inflationary setting.

However, today’s wage-price spiral appears to be a global phenomenon.

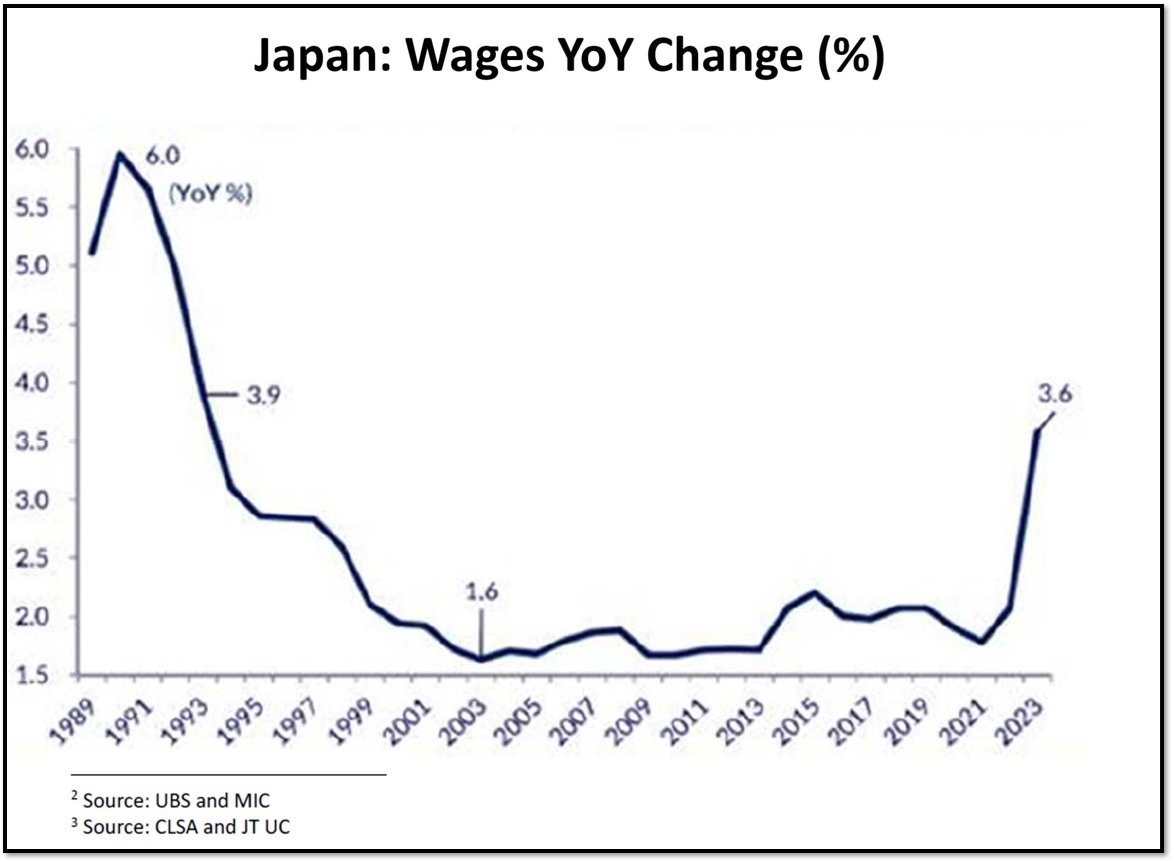

To draw from the example of Japan once again, its economy is undergoing a fundamental shift at its core.

After 30 years of muted wage growth, Japanese workers have finally started demanding higher salaries.

To draw from the example of Japan once again, its economy is undergoing a fundamental shift at its core.

After 30 years of muted wage growth, Japanese workers have finally started demanding higher salaries.

Meanwhile:

Investors expecting inflation to decelerate is the most consensus view in the history of the data, even lower than during the GFC.

Crowded market views are often wrong, the current inflationary forces appear to have a significant underlying structural foundation.

Investors expecting inflation to decelerate is the most consensus view in the history of the data, even lower than during the GFC.

Crowded market views are often wrong, the current inflationary forces appear to have a significant underlying structural foundation.

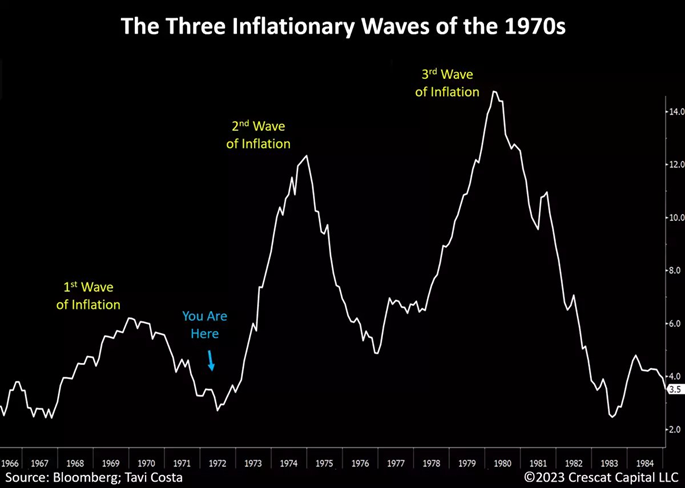

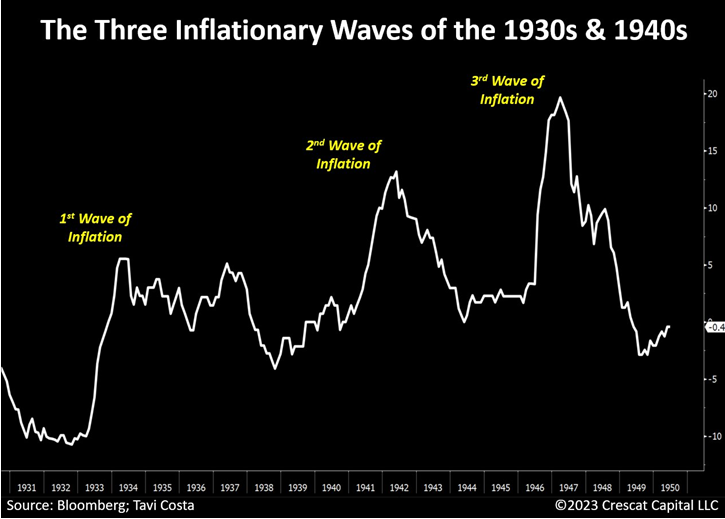

However, if we learned anything from history:

Inflation develops through waves.

Market participants and the Federal Reserve seem to be committing a significant oversight by neglecting past experiences and patterns.

Inflation develops through waves.

Market participants and the Federal Reserve seem to be committing a significant oversight by neglecting past experiences and patterns.

And, to be clear, despite all the debate regarding the 1940s and 1970s:

Inflation turned out to be structural in nature and manifested itself through waves during both periods.

Inflation turned out to be structural in nature and manifested itself through waves during both periods.

Take note of that in perspective of what is unfolding today.

Inflation is likely in a bottoming process, and the recent developments in commodity prices and breakeven rates are adding to that case.

Inflation is likely in a bottoming process, and the recent developments in commodity prices and breakeven rates are adding to that case.

This is not a cyclical issue; instead, the main drivers of today's inflationary regime are:

▪️ Deglobalization,

▪️ Irresponsible levels of government spending,

▪️ Ongoing commodity supply constraints,

▪️ Wage-price spiral, especially among lower-income workers.

▪️ Deglobalization,

▪️ Irresponsible levels of government spending,

▪️ Ongoing commodity supply constraints,

▪️ Wage-price spiral, especially among lower-income workers.

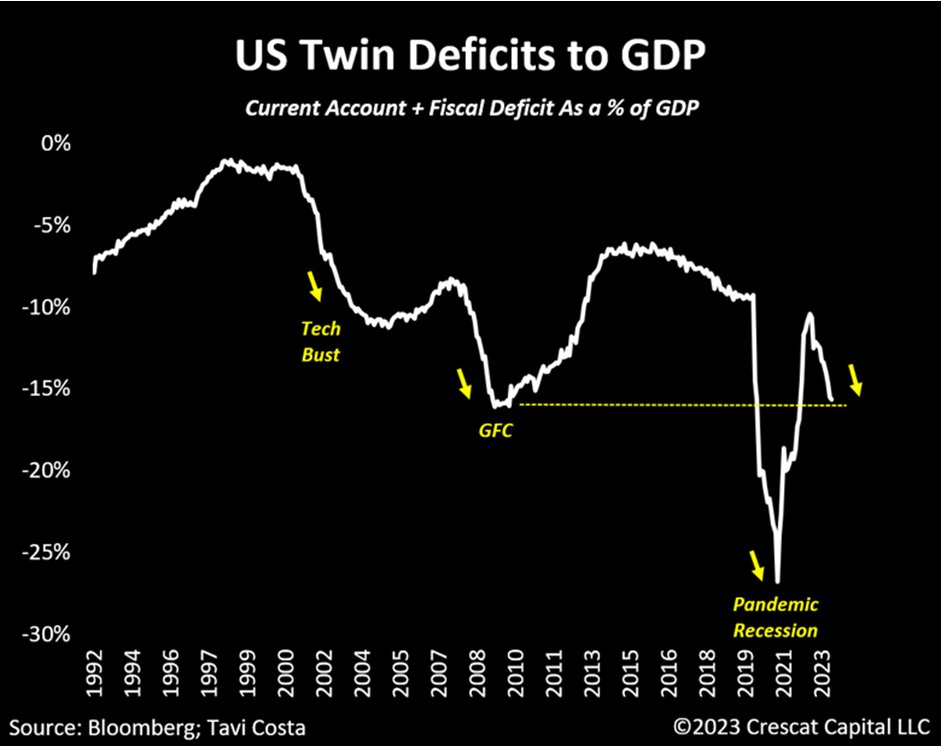

Lastly:

To further emphasize the importance of owning commodities in today’s environment.

The US is now running twin deficits that are as severe as those experienced during the worst parts of the Global Financial Crisis.

To further emphasize the importance of owning commodities in today’s environment.

The US is now running twin deficits that are as severe as those experienced during the worst parts of the Global Financial Crisis.

Of even greater concern is the indication that this represents an ongoing structural issue that is still in the process of evolving.

Note that with each prior recession, this measurement has reached new lows.

Note that with each prior recession, this measurement has reached new lows.

Hope you enjoyed this thread.

If you are looking for a more detailed analysis, consider reading the entire research piece:

crescat.net/redefining-60-…

If you are looking for a more detailed analysis, consider reading the entire research piece:

crescat.net/redefining-60-…

• • •

Missing some Tweet in this thread? You can try to

force a refresh