It’s a common complaint that the UK tax system is much too complicated.

Some complication is inevitable (modern life is complicated). Some is a response to avoidance. Some is driven by policy choices.

But some of the complication really is unnecessary. My nerdiest ever thread:

Some complication is inevitable (modern life is complicated). Some is a response to avoidance. Some is driven by policy choices.

But some of the complication really is unnecessary. My nerdiest ever thread:

Complexity has become a source of uncertainty. And this isn't a one off - the last decade has seen a series of new rules, each more complex than the last.

Businesses struggle to achieve the "obvious" result from the rules. HMRC struggles to apply them.

Businesses struggle to achieve the "obvious" result from the rules. HMRC struggles to apply them.

We should stop being so dogmatic, and adopt a principles-based approach when that is going to be easier for both business and HMRC to apply. Prof @JudithFreedman has written persuasively on this point. papers.ssrn.com/sol3/papers.cf…

Advice: in theory this should be fine given that Waystar Finco is ultimately borrowing from the market, but the detail will take a significant amount of work. Easily 15 pages of analysis.

Conclusion: scrap the UK rules and guidance and adopt a simpler EU-style approach.

3. Hybrid mismatch rules

Here's a classic way to avoid tax: cunningly craft the Waystar Finco/Waystar UK loan so that the UK tax system thinks it's a loan, but the US tax system thinks it's a preference share, or even doesn't exist at all.

The result? Tax relief in the UK, and either no tax in the US or even, if the CEO is greedy, tax credits.

The loan is a "hybrid" - taxed differently in two different countries.

The loan is a "hybrid" - taxed differently in two different countries.

The hybrid rules were created to stop this kind of thing - they're another part of the BEPS Project. That yielded 39 pages of really difficult legislation (in microfilm, again).

And OMG the guidance (nanofilm). 484 pages.

I don't want to be unfair to HMRC here. The horribleness of the legislation means people begged HMRC to clarify this point, that point, and the other point, and before you know it: 484 pages.

I believe the longest guidance ever created by any tax authority in human history for one single tax rule.

One of humanity's great achievements, up there with the pyramids. hmrc.gov.uk/gds/intm/image…

One of humanity's great achievements, up there with the pyramids. hmrc.gov.uk/gds/intm/image…

Most of the time, HMRC ignores the rules entirely, and only actually cares when it sees something avoidancey - but, for large loans, and large risk-averse businesses, you can't count on that.

So expensive advisers (me, in a past life) occasionally spend weeks locked in a dark room making sure that highly complex, but innocent, structures aren't caught.

That same complexity means that guilty structures can sometimes escape scot-free.

Advice: Waystar's commitment to high ethical standards mean it's inconceivable they'd try to create a hybrid. But US tax rules, and typical US corporate structures, are so complicated that I can't just assume the rules won't apply.

Significant time will need to be spent analysing the whole structure, with US tax and accounting input. This is potentially a big job.

Conclusion: Again, principles-based drafting is the answer. The EU rules are about 13 pages, split between ATAD and ATAD 2. Let's do that.

4. Reasonable commercial return

(I'm not even half way through. Sorry. Hate the game not the player)

(I'm not even half way through. Sorry. Hate the game not the player)

Paragraph E of section 1000(1) CTA 2010 denies a deduction if securities are "non-commercial", defined as follows:

This is a pretty reasonable rule. But why does it exist? If the securities are paying more than a reasonable commercial return, they can hardly be at arm's-length, so the transfer pricing rules would be engaged. Wouldn't they?

It's not that easy, and I could write a 10 page memo on the subtle differences between the two tests, but that memo should not exist. We don't need two rules doing almost exactly the same thing.

My excerpt above could mislead you into thinking section 1005 is just a simple one sentence rule. There are, however, nine lengthy sections that follow, putting various glosses it. .legislation.gov.uk/ukpga/2010/4/p…

My favourite: section 1013 is an exception to an exception to an exception to an exception to s1005.

I am not exaggerating: s1007 is an exception to s1005, s1008 is an exception to s1007, then s1012 is an exception to section s1008, and s1013 is an exception to s1012.

I am not exaggerating: s1007 is an exception to s1005, s1008 is an exception to s1007, then s1012 is an exception to section s1008, and s1013 is an exception to s1012.

Advice: the easy approach is for me to say to the client that everything is fine provided the interest under the loan is no more than a "reasonable commercial return". But the client will probably ask what that means, and how it's different from the transfer pricing test.

Cue a lengthy memo, and an unhappy client walking away with the distinct impression that the UK is not a great place to do business.

Conclusion: abolish the rule. If parties are related then it adds nothing to transfer pricing. If parties aren't related then the rate should de facto be commercial; if it isn't then something weird is going on, which one of the gazillion anti-avoidance rules will surely counter.

"Reasonable commercial return" is a fossil, and belongs in a museum.

5. Results dependency

Here's Condition C section 1015:

"Depends on the results of the company's business" is a test that used again and again in tax legislation. So it's a bit sad that nobody knows what it means.

There is a sensible meaning: "don't pretend something's a loan when it's really shares, just so you can get a tax deduction". Do we really need a rule like that? Wouldn't one of the other many, many anti-avoidance rules kill something as obvious as dressing equity up as debt?

It's worse, because there's also a crazy meaning. HMRC think Condition C also means: "don't create a loan where the borrower only has to pay interest if it can afford to pay interest". This is often called a "limited recourse" or "non-recourse" loan. And HMRC say you can't do it.

That's a problem, because there are many commercial scenarios in which you want limited recourse funding, particularly if you have multiple projects (power stations, housing developments, investments) where each is funded by a different lender.

From a policy perspective, I've no clue why HMRC think this is a bad thing. Every other country in the world, I believe, permits it.

HMRC's approach has two consequences. First, it's super easy, barely an inconvenience, to get around the rule by establishing each new project in a new company. Second, if you can't do that, or it's too much effort, you just go to another country.

So this is a rule that serves no purpose, creates complexity, and pushes business out of the UK. Excellent.

Advice: should be fine. Although, like many advisors, I've often seen loan documents where some helpful US advisor added a non-recourse clause at the last minute, not realising that it would mess up the tax. Another dangerous and pointless "gotcha".

Conclusion: abolish the rule - it's a fossil from the days when avoidance was easy.

Make clear in guidance that any debt which really behaves like equity is, by definition non-arm's length, and will lose deductibility under the transfer of pricing rules. But limited recourse shouldn't offend anyone.

6. Equity notes

Section 1006 bars deductibility for an "equity note" (meaning, broadly, a security that can stick around for longer than 50 years) if it's held by an "associated person" or someone funded by an "associated person".

US companies have sometimes issued 100 year bonds. Perhaps Waystar Royco wants to, and then lend the proceeds into the UK?

Well, tough - the equity note rule means it can't.

Why? I've no clue. If it's a market instrument, and satisfies the transfer pricing rules, then what's the problem with having a very long term? This is an obscure rule, and I've occasionally seen it catch people out.

Advice: don't have a term of 50 years.

Conclusion: another fossil - abolish it.

Conclusion: another fossil - abolish it.

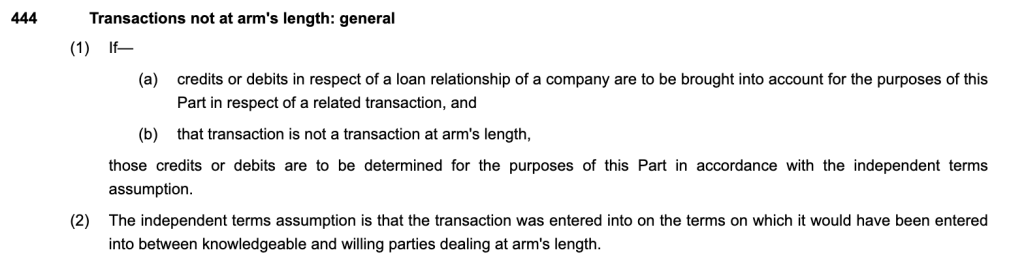

7. Section 444

Remember the transfer pricing rules, about 200 posts up in this thread?

Spot the difference between that, and this:

Spot the difference between that, and this:

A completely unnecessary rule which creates complexity and uncertainty (not least because working out the consequence of that "independent terms assumption" is hard).

s444 shouldn't apply where the transfer pricing rules potentially apply, but there are weird scenarios where you're not sure which case you're in.

Advice: in this case reasonably clear it won't apply. In other cases, that's more difficult, but probably yields the same result as the transfer pricing result. If you want better than "probably", that memo will cost £5,000.

Conclusion: scrap s444.

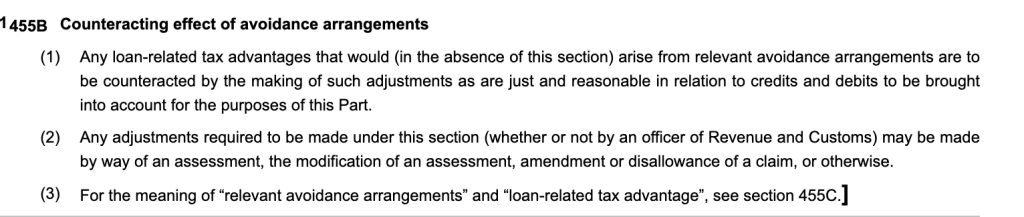

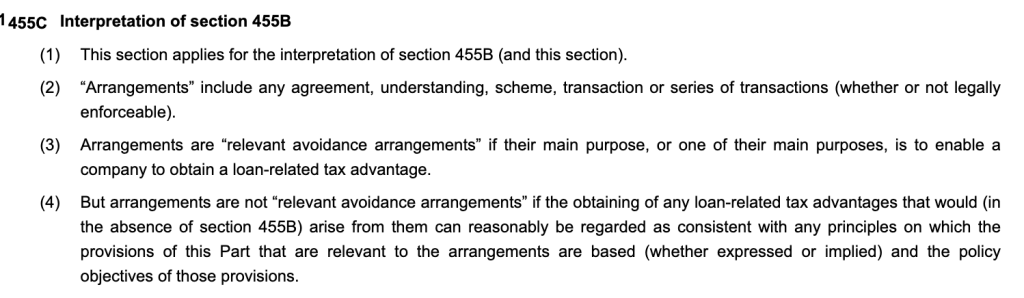

8. Anti-avoidance counteraction

Debt is taxed under the "loan relationships" regime, which contains a broadly drafted anti-avoidance rule:

And then:

So if you get a tax advantage in a way that's contrary to the principles of the rules, then... you don't.

The precise scope of this is unclear, but that's not a bad thing for an anti-avoidance rule - it means people have a powerful incentive to steer clear of grey areas.

(unless they're idiots)

(unless they're idiots)

Advice: yes, one of the reasons to choose to fund Waystar UK with debt rather than equity was to get a tax deduction for the interest. Waystar could have funded with equity; that would have meant more tax.

But I would say the "principles" of the rules envisage a choice between equity and debt, and so s455C doesn't apply. This will run to several pages of analysis.

Conclusion: all tax regimes need an anti-avoidance rule of some kind, and this is a pretty good one.

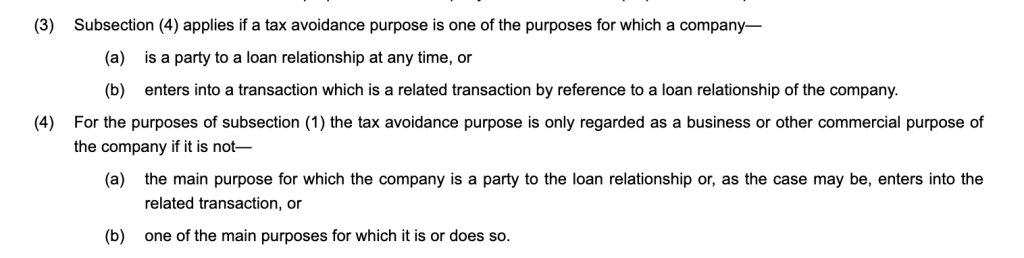

9. Unallowable purposes

There's a much older anti avoidance rule in section 442:

and

This rule therefore does two things:

- If debt is borrowed for a non-business purpose then interest is not tax-deductible. So, for example, there's a problem if Waystar UK is going to use all the funds to buy a yacht for its chairman. Fine.

- If debt is borrowed for a non-business purpose then interest is not tax-deductible. So, for example, there's a problem if Waystar UK is going to use all the funds to buy a yacht for its chairman. Fine.

- And if the main purposes include a "tax avoidance purpose" then the interest is not tax-deductible.

The fact the test assesses subjective "purpose" has an important but odd consequence.

Say that Wayco's CFO sends a memo saying "hey, let's use debt to get a juicy tax deduction". There's a clear tax main purpose and s442 applies.

Say that Wayco's rival PGM establishes a precisely identical structure, but their CFO's memo doesn't mention tax (and instead speaks of the convenience of extracting profits through interest payments). Then it's looking much better.

A rule that treats two identical businesses differently is not a good rule. A rule that can be beaten by carefully controlling communications is a terrible rule.

Advice: something like "You have told me the debt is being advanced for commercial (i.e. non-tax) reasons, the tax benefit of interest deductibility is ancillary and you would have lent to the UK even if there was no deduction. On that basis section 442 won't apply"

Conclusion: we don't need two overlapping anti-avoidance rules in the loan relationship regime. s442 did valuable duty for many years, but should be put out to pasture.

The cost

This complexity has a cost. HMRC and advisers spend money building expertise to police it. Clients pay lawyers and accountants large sums to advise on it. This is not a good use of anybody's resources, and it makes the UK a worse place to do business.

I'm convinced we wouldn't lose £1 in tax revenues if we scrapped/dramatically simplified the seven bad rules above (and put HMRC's freed-up resources into anti-avoidance).

And this is just one tax question for one common business structure. There are dozens more areas just as ripe for simplification.

The first step would be the easy one: identify and repeal the "fossils".

The second step, moving towards principles-based-drafting, would be significantly harder - but we can't continue as we are, with hugely complex new rules added every few years. Let's stop making generic complaints about tax complexity, and tackle some of the root causes.

If that was too short for you, or you really like footnotes, there's a more detailed write-up of this thread here: taxpolicy.org.uk/2023/10/23/com…

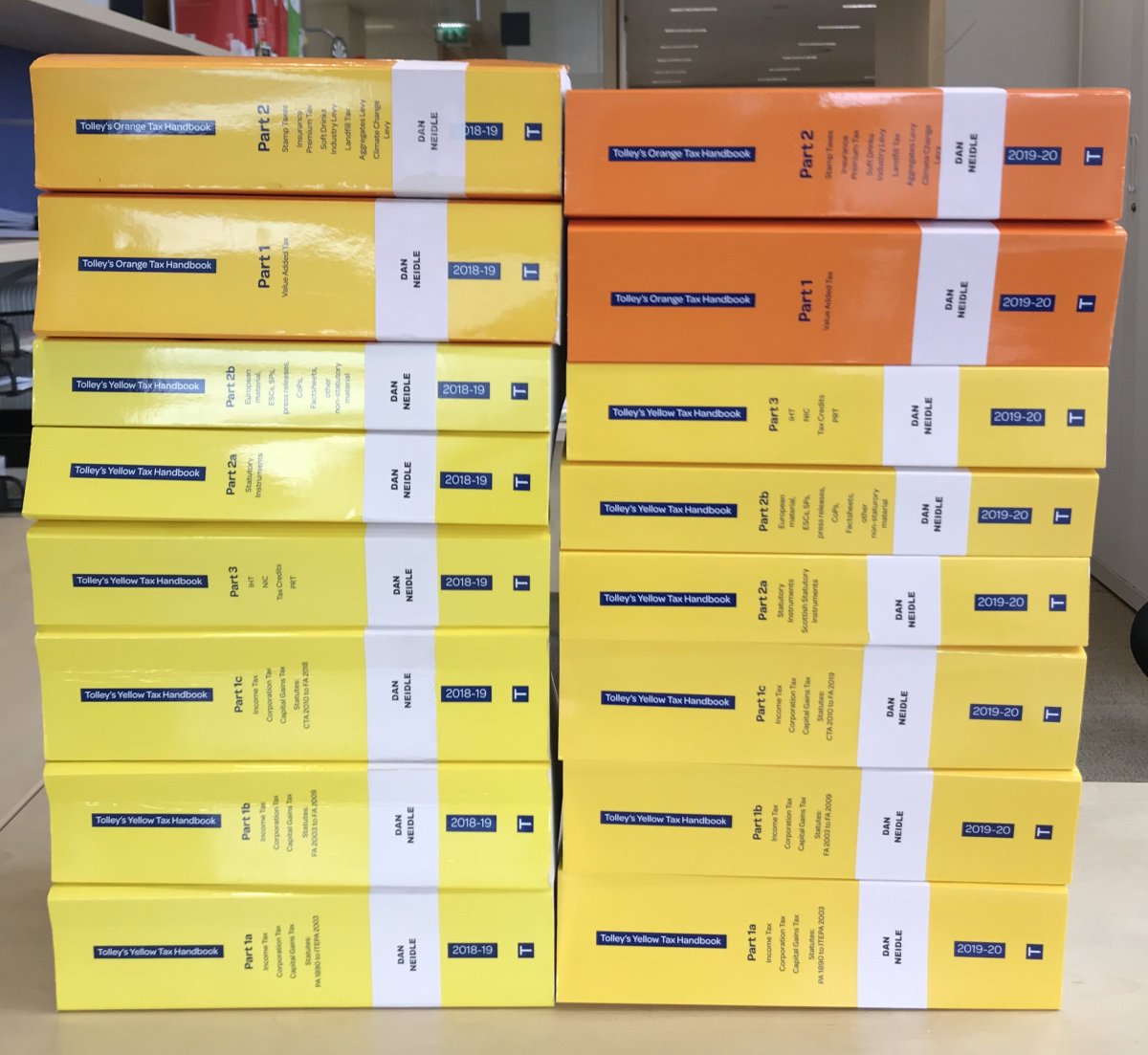

@netera101 It's more about taking individual rules out of very commonly used taxes. But if you push me, perhaps 1/4 of one book?

• • •

Missing some Tweet in this thread? You can try to

force a refresh