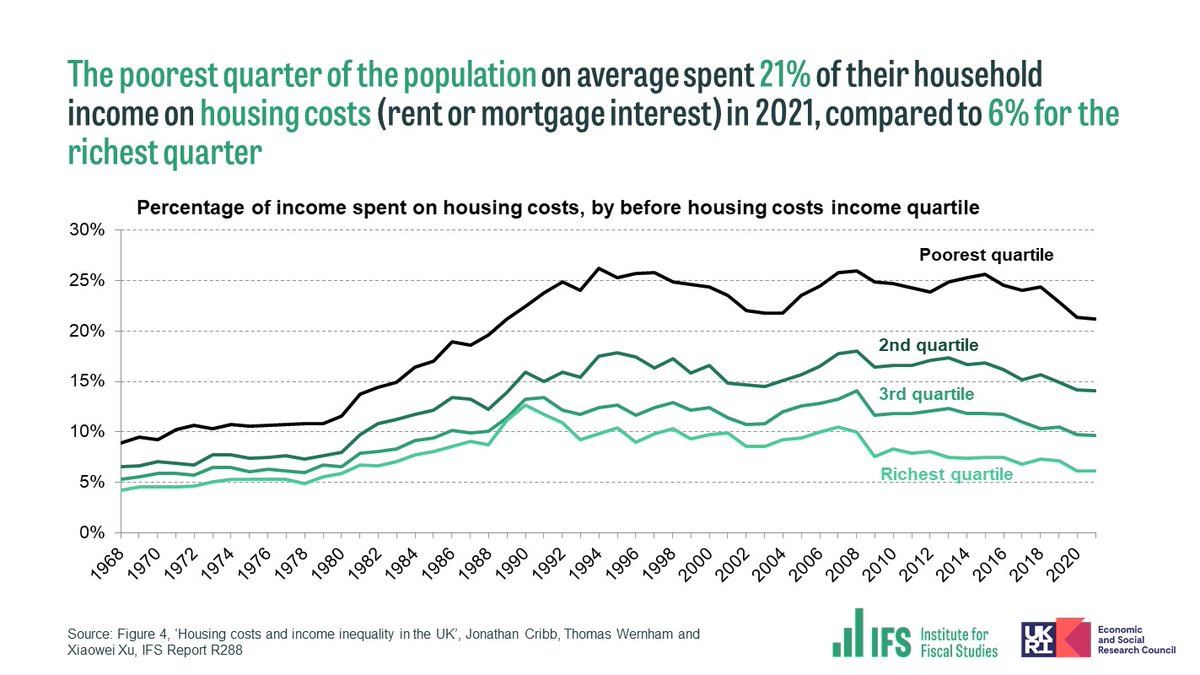

NEW: Housing costs take up three-and-a-half times as much of the budgets of the poor as of the rich.

We need to take housing costs into account to understand income poverty.

THREAD on @JCribbEcon, Tom Wernham & @xiaoweixu_’s new report on housing costs and incomes: [1/5]

We need to take housing costs into account to understand income poverty.

THREAD on @JCribbEcon, Tom Wernham & @xiaoweixu_’s new report on housing costs and incomes: [1/5]

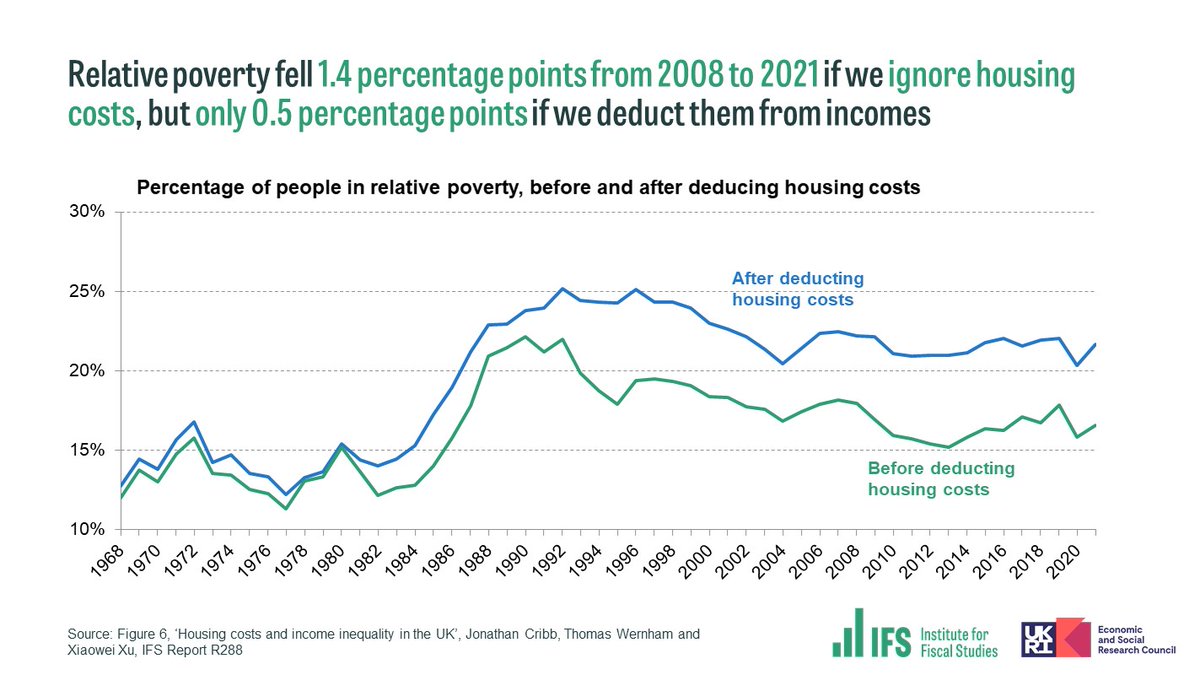

Whether we deduct housing costs from incomes makes a big difference to poverty measurement – the poverty rate is around 17% ignoring housing costs, but 22% if we deduct them.

Trends over time also look very different when housing costs are deducted from incomes.

[2/5]

Trends over time also look very different when housing costs are deducted from incomes.

[2/5]

Accounting for housing costs when measuring poverty makes a big difference to who we think of as poor.

Many older adults are outright owner-occupiers with very low housing costs, so when we deduct housing costs, they are much less likely than children to be in poverty.

[3/5]

Many older adults are outright owner-occupiers with very low housing costs, so when we deduct housing costs, they are much less likely than children to be in poverty.

[3/5]

Measures of poverty which ignore housing costs are less effective at identifying those with low living standards.

Those in poverty after deducting housing costs are more likely to be deprived of essential items such as warm winter coats or fresh fruit and veg.

[4/5]

Those in poverty after deducting housing costs are more likely to be deprived of essential items such as warm winter coats or fresh fruit and veg.

[4/5]

“Now more than ever, with rising mortgage interest rates and rising private rents for new lets, we need to take account of these housing costs and how they affect people’s disposable incomes.”

Read the full report:

[5/5] ifs.org.uk/publications/h…

Read the full report:

[5/5] ifs.org.uk/publications/h…

• • •

Missing some Tweet in this thread? You can try to

force a refresh