IDFC First Bank is a red-hot stock on Social Media!

After the merger,

V Vaidyanathan has worked tremendously hard to clean up the legacy issues

The Bank reported record profits in the last 2 quarters

A thread🧵on the progress of IDFC First Bank and the wat forward

Lets go👇

After the merger,

V Vaidyanathan has worked tremendously hard to clean up the legacy issues

The Bank reported record profits in the last 2 quarters

A thread🧵on the progress of IDFC First Bank and the wat forward

Lets go👇

The background:-

IDFC FIRST Bank was created by the merger of Erstwhile IDFC Bank and Erstwhile Capital First on December 18, 2018.

IDFC FIRST Bank was created by the merger of Erstwhile IDFC Bank and Erstwhile Capital First on December 18, 2018.

Erstwhile IDFC Bank started its operation as a Bank after demerger from IDFC Ltd, a premier, successful infrastructure Financing domestic Financial Institution since 1997.

The loan assets and borrowings of IDFC limited were transferred to IDFC Bank at inception of IDFC Bank.

The loan assets and borrowings of IDFC limited were transferred to IDFC Bank at inception of IDFC Bank.

Erstwhile Capital First was a successful consumer and MSME financing entity since 2012 with strong track record of growth,profits and asset quality.

• On merger, the Bank was renamed IDFC FIRST Bank.

• On merger, the Bank was renamed IDFC FIRST Bank.

Problems of the Erstwhile IDFC Bank

1.Lent to infrastructure industry which meant huge bad loans

2.High cost borrowing

proper strategy3.No

1.Lent to infrastructure industry which meant huge bad loans

2.High cost borrowing

proper strategy3.No

V Vaidyanathan took over the bank and now the bank has turned around

The bank reported record quarterly profits in its Q4

The legacy of the erstwhile IDFC bank is now completely gone!

Lets us look at the performance of the bank now:-

The bank reported record quarterly profits in its Q4

The legacy of the erstwhile IDFC bank is now completely gone!

Lets us look at the performance of the bank now:-

Loan growth:-

🏦The Bank reported a loan growth of 24%.

🏦Predominantly a retail asset bank.

🏦Unsecured loans remained 60% of the book.

🏦Credit cards book has started to grow sharply

🏦Home loans are now growing well

🏦The Bank reported a loan growth of 24%.

🏦Predominantly a retail asset bank.

🏦Unsecured loans remained 60% of the book.

🏦Credit cards book has started to grow sharply

🏦Home loans are now growing well

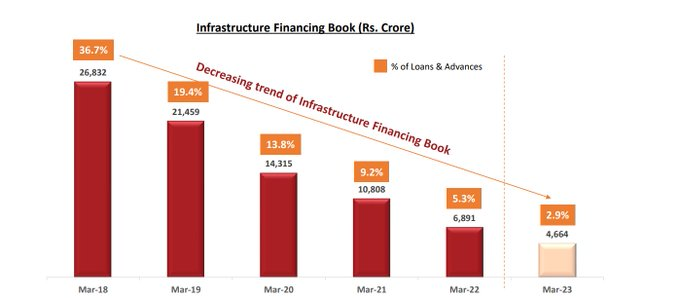

Legacy IDFC Book is as good as gone!

The legacy book is now at just 2.9%

The Bank holds enough provisions on the book and over the 2-3 quarters the bank should complete the running down of the book

The legacy book is now at just 2.9%

The Bank holds enough provisions on the book and over the 2-3 quarters the bank should complete the running down of the book

Deposit Growth:-

Deposit growth remains robust at 25%.

CASA ratio is on the higher side and the bank must do more to increase the term deposits.

Ramp up of the deposit franchise makes IDFC stronger

Deposit growth remains robust at 25%.

CASA ratio is on the higher side and the bank must do more to increase the term deposits.

Ramp up of the deposit franchise makes IDFC stronger

Run down of higher-cost bonds should help the bank.

However, creating a stable liability franchise is a long-term project.

Slow and steady progress will be made.

However, creating a stable liability franchise is a long-term project.

Slow and steady progress will be made.

Asset Quality:-

Collections continue to be extremely strong for the bank.

Gross NPA is at a multi-quarter low of 1.53%

NPAs are no longer the problem as of now

Collections continue to be extremely strong for the bank.

Gross NPA is at a multi-quarter low of 1.53%

NPAs are no longer the problem as of now

Strong Provision Coverage Ratio for the Bank

The bank has been on a mission to increase PCR

IDFC First Bank now has one of the highest Provision Coverage Ratios.

The bank has been on a mission to increase PCR

IDFC First Bank now has one of the highest Provision Coverage Ratios.

Capital Adequacy:-

The Bank is eating capital fast.

The Bank ate up 66bps of TIER-1 capital

TIER-1 Capital Adequacy is now at 15.30%.

Given the high pace of loan growth.

Frequent dilution is a key concern

The Bank is eating capital fast.

The Bank ate up 66bps of TIER-1 capital

TIER-1 Capital Adequacy is now at 15.30%.

Given the high pace of loan growth.

Frequent dilution is a key concern

Control of Unsecured loans below Rs 50,000:-

V Vaidyanathan clearly explains the pain point in Unsecured loans

BNPL loans and Credit card loans are the places where there is clear problem!

IDFC has little exposure their

V Vaidyanathan clearly explains the pain point in Unsecured loans

BNPL loans and Credit card loans are the places where there is clear problem!

IDFC has little exposure their

The Bank has guided for:-

🏦20-25% Loan growth

🏦Gross NPAs at 2%

🏦 Double-digit ROEs

We are at the bottom of a credit cycle.

While the commentary is aggressive,it could be possible as the system credit grows in double-digit.

🏦20-25% Loan growth

🏦Gross NPAs at 2%

🏦 Double-digit ROEs

We are at the bottom of a credit cycle.

While the commentary is aggressive,it could be possible as the system credit grows in double-digit.

The strong leader V Vaidyanathan:-

Banking is all about the Management.

V Vaidyanathan was responsible for building out Capital First.

Honesty, Being humble and the ability to turn out the organization are key traits of a leader like Vaidyanathan.

Banking is all about the Management.

V Vaidyanathan was responsible for building out Capital First.

Honesty, Being humble and the ability to turn out the organization are key traits of a leader like Vaidyanathan.

Curious case of Cricket deal:-

The company closed Team India's sponsorship for nearly 400cr

The Bank is now raising 3000cr of precious equity capital

Equity capital is basically financing the Team India deal.

The company closed Team India's sponsorship for nearly 400cr

The Bank is now raising 3000cr of precious equity capital

Equity capital is basically financing the Team India deal.

A smaller growing bank guzzles capital very very fast and they must use capital very judiciously,

Otherwise, they will end up diluting equity capital every year.

Otherwise, they will end up diluting equity capital every year.

IDFC Bank has a Book Value of Rs 41

The Bank trades at 2.14x P/B.

We are now peak ROEs for almost all banks

This valuation is not cheap!

The Bank trades at 2.14x P/B.

We are now peak ROEs for almost all banks

This valuation is not cheap!

So how is the outlook?

We are at the bottom of a credit cycle with most Banks having cleaned up the balance sheet

Most lenders should do well from here on

IDFC Bank will also grow well..however, the seasoning of the book must be seen

Mr Vaidyanathan is a great leader

We are at the bottom of a credit cycle with most Banks having cleaned up the balance sheet

Most lenders should do well from here on

IDFC Bank will also grow well..however, the seasoning of the book must be seen

Mr Vaidyanathan is a great leader

Smaller banks do have much bigger challenges than Larger private sector Banks

If there is one leader who can overcome the challenges...it can be V Vaidyanathan.

However, the progress must be constantly monitored

If there is one leader who can overcome the challenges...it can be V Vaidyanathan.

However, the progress must be constantly monitored

Keep following me -@AdityaD_Shah as I write daily to make you aware around:

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

Disclaimer:-

This is my own study.

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

This is my own study.

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

• • •

Missing some Tweet in this thread? You can try to

force a refresh