One of the key arguments that Norway uses to continue oil & gas developments, is that under BAU it is expected that oil & gas production will decline in line with <2°C scenarios, even with continued investment.

Let's look closer at these projections & reality...

1/

Let's look closer at these projections & reality...

1/

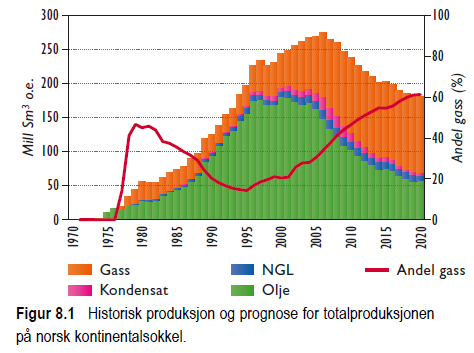

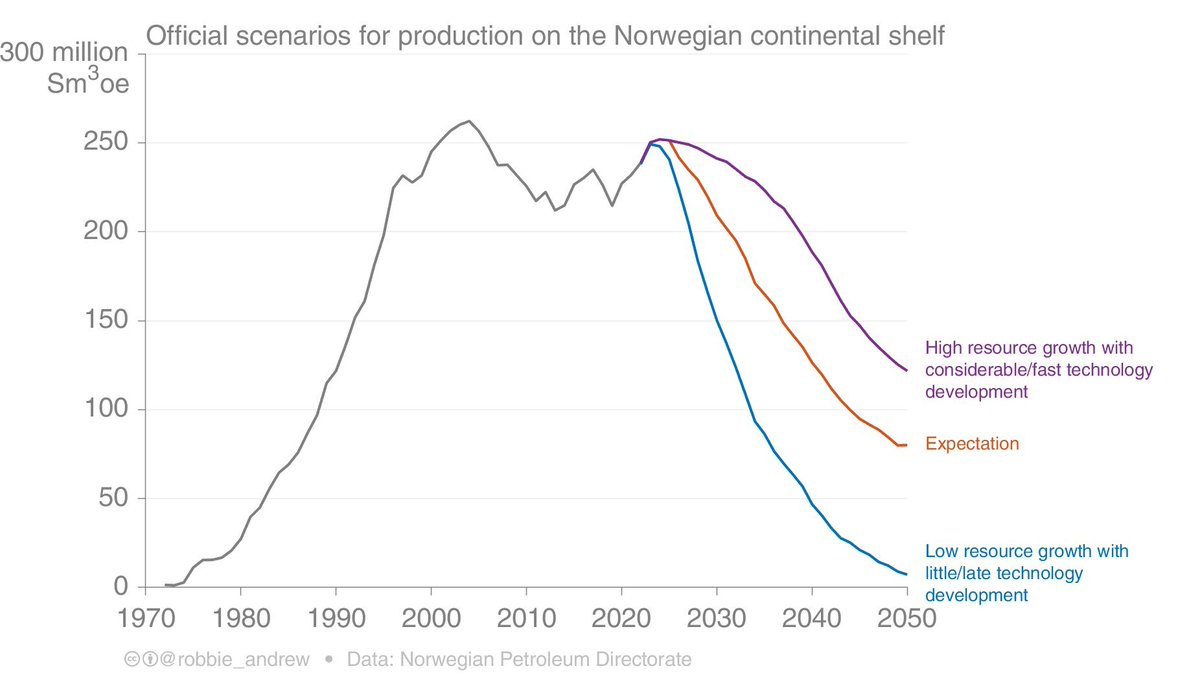

Here is the projections from the 2003 report from the petroleum agency.

In reality (tweet 1) there was a dip around 2010, but production is now up around 250 million cubic again.

The forecast was totally & utterly WRONG!

2/

In reality (tweet 1) there was a dip around 2010, but production is now up around 250 million cubic again.

The forecast was totally & utterly WRONG!

2/

In 2011 there was a forecast for an increase in production to 2020, but then a decline. This is probably since they started to put the Johan Sverdrup field on the books.

The increase in production was way too low, again, they got it wrong.

3/

The increase in production was way too low, again, they got it wrong.

3/

In 2016, the forecast seemed to have lost the peak around 2020, but with a slower decline in production.

Again, according to history, they were wrong, even with a forecast window of only a few years!

4/

Again, according to history, they were wrong, even with a forecast window of only a few years!

4/

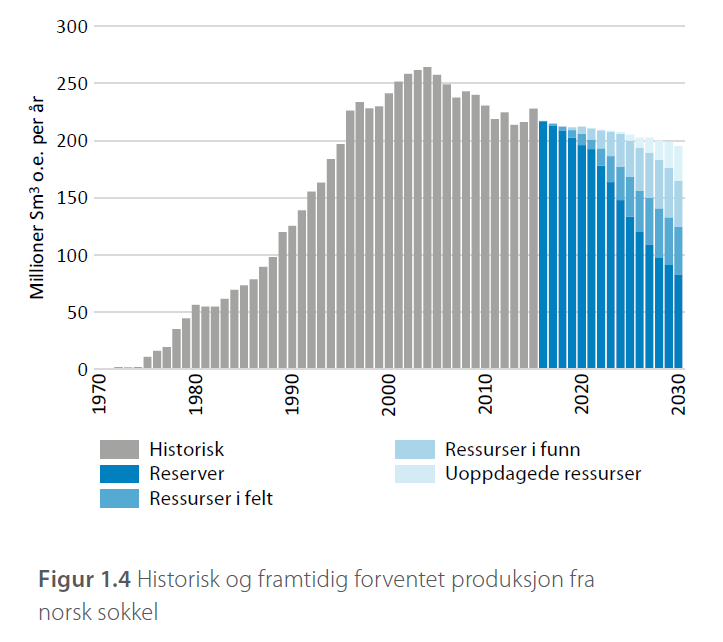

And here we are today. With a new high (local minima), currently over 250 million cubic, but an expectation of a decline afterwards.

The forecasts made have so far all been wrong!

Production has not declined as the petroleum agency has predicted.

5/

The forecasts made have so far all been wrong!

Production has not declined as the petroleum agency has predicted.

5/

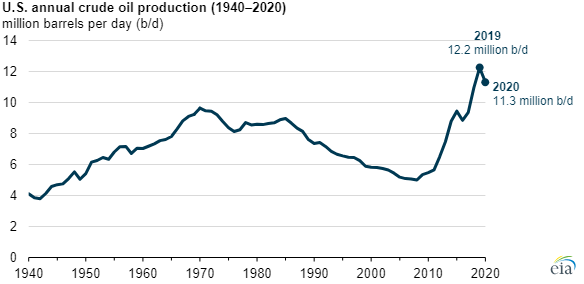

This is not uncommon, Norway is not alone. Everyone thought US oil production had peaked, until they found shale oil / gas.

6/

6/

The important point is that technology constantly proves these forecasts wrong.

Based on history, there is little evidence that Norwegian oil & gas production will fall as forecast.

Continued investment & technology evolution will make these forecasts wrong.

7/

Based on history, there is little evidence that Norwegian oil & gas production will fall as forecast.

Continued investment & technology evolution will make these forecasts wrong.

7/

Norwegian climate policy is currently based on incorrectly telling people these forecasts are accurate, when they know they are not.

8/

8/

See the thread by

and old resource reports can be found here

9/9

npd.no/aktuelt/publik…

and old resource reports can be found here

9/9

https://twitter.com/robbie_andrew/status/1734965127856652471

npd.no/aktuelt/publik…

• • •

Missing some Tweet in this thread? You can try to

force a refresh