What we don’t know: how much will the Fed ease, and will it be for the wrong reasons?🧵

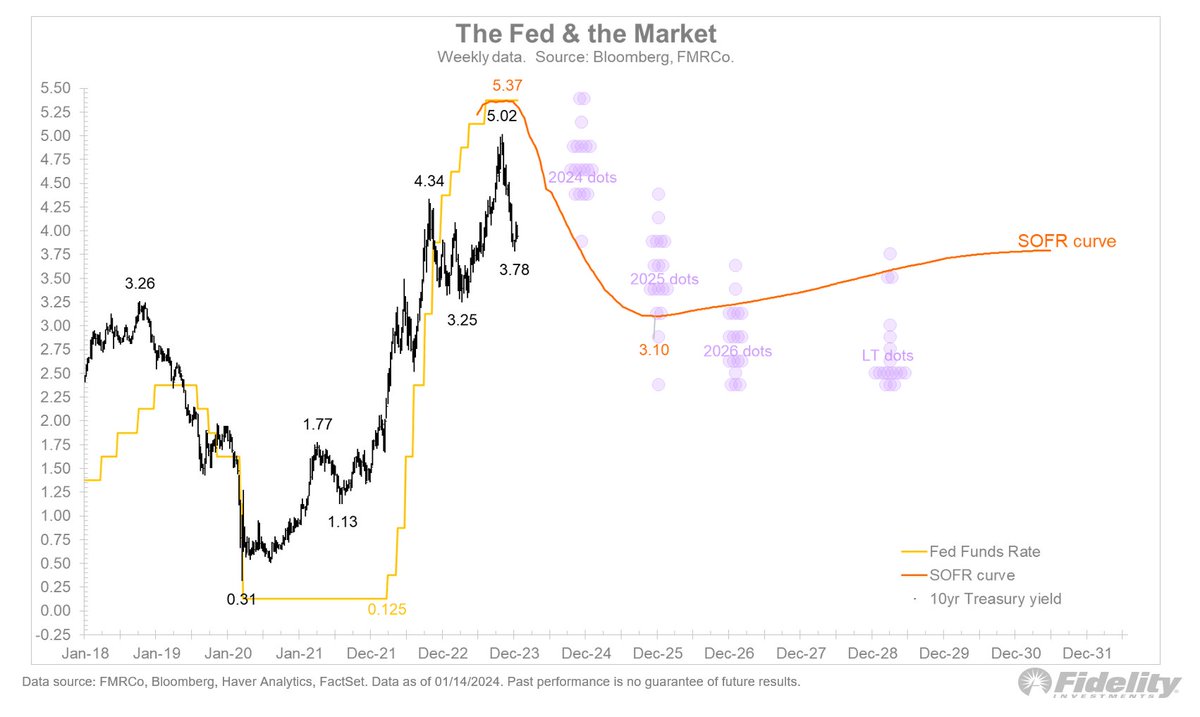

An easing bias doesn’t tell us when the rate cuts are coming or how many there will be. In my view, the market is a bit delusional in expecting 6 or 7 rate cuts this year, unless we get a recession. But the stock market is priced for a soft landing, which doesn’t reconcile with the bond market’s view on rates. Somebody is wrong, and my guess is that it’s the bond market. /2

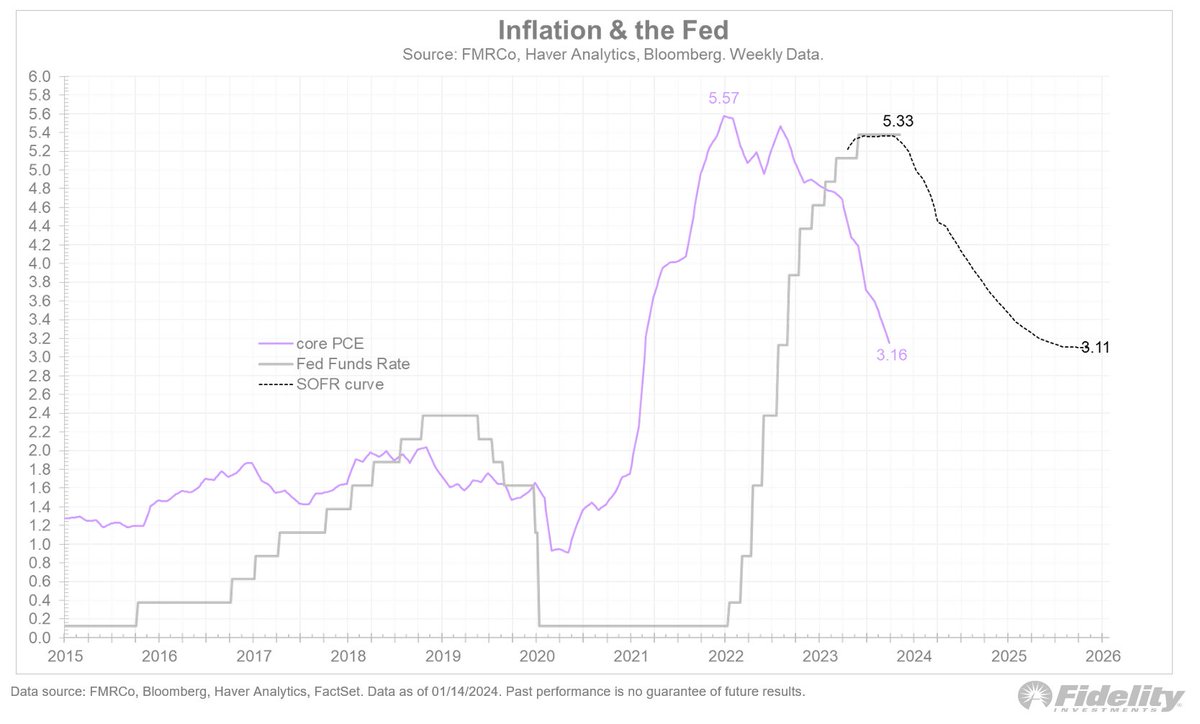

With core-PCE at 3.2% and the forward curve dipping to 3.1%, the market is essentially saying that the Fed will drop real rates to zero. A zero real rate in a soft landing makes little sense, unless inflation keeps dropping (which could happen of course). /3

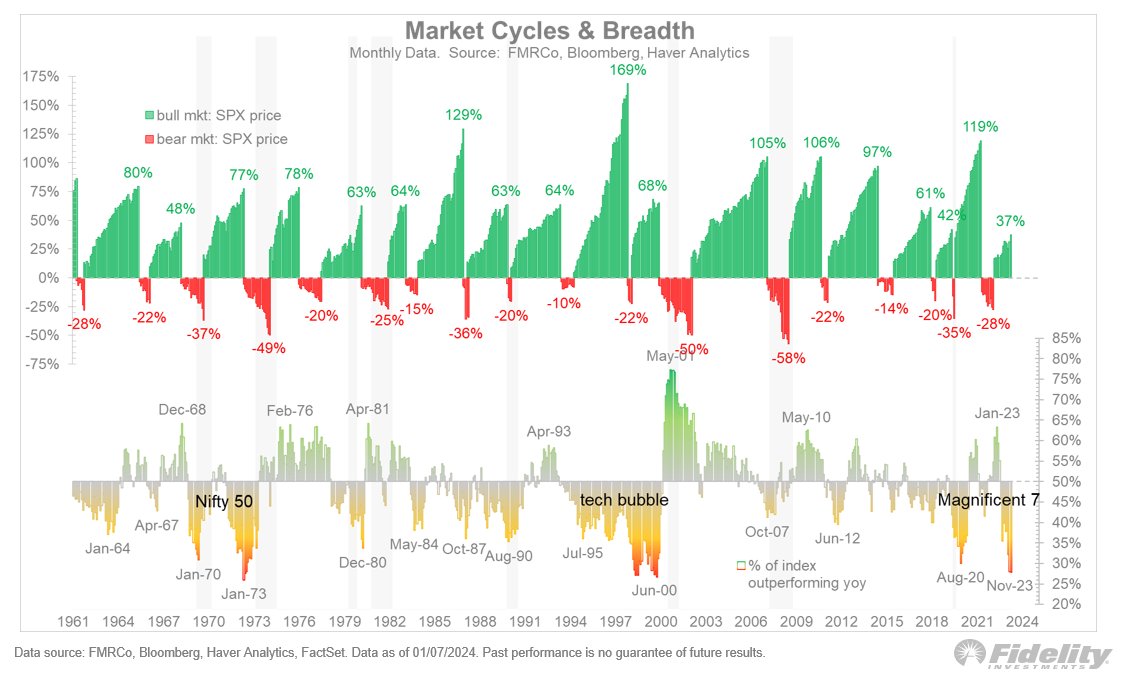

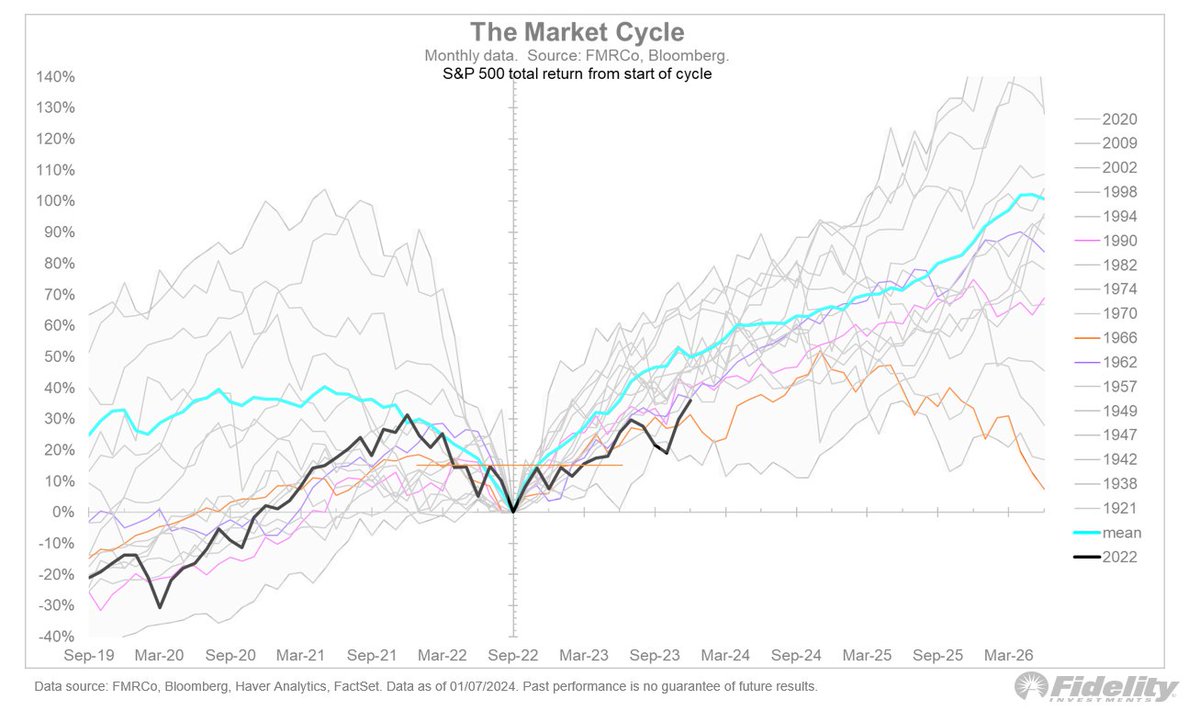

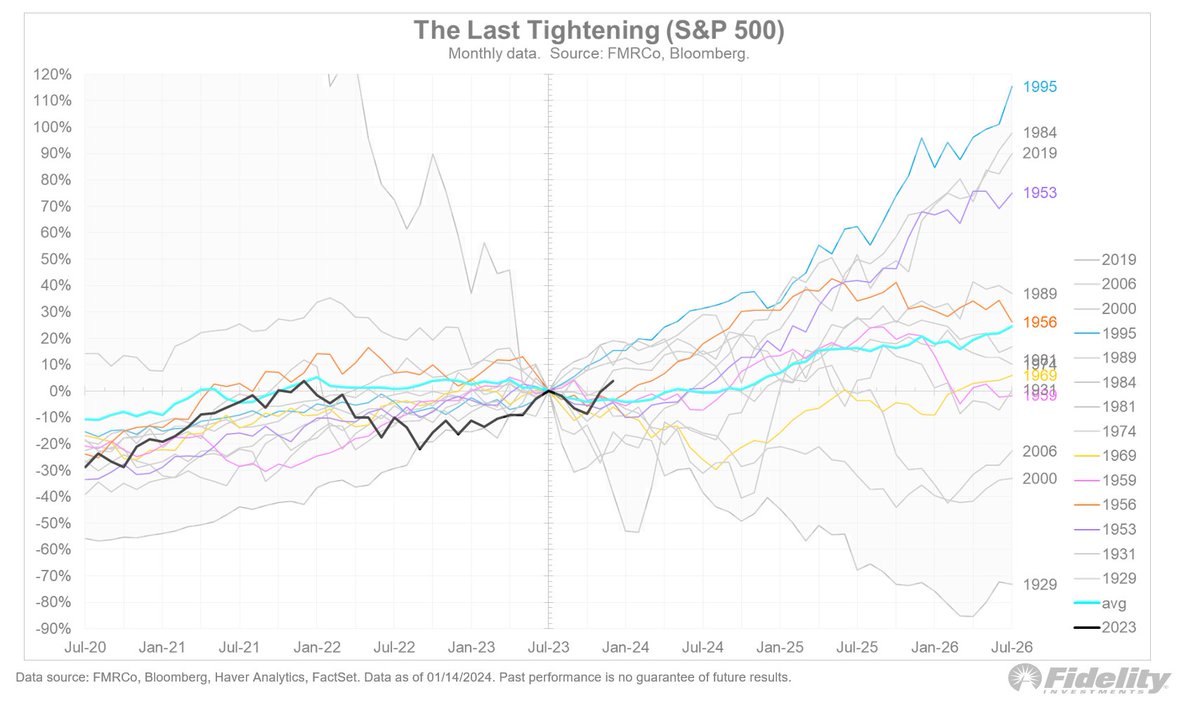

If the Fed has stuck the (soft) landing and drops rates back towards neutral, that bodes well for equities and supports the narrative of a bullish broadening in 2024. But as the chart shows below, the range of outcomes for the S&P 500 index following the last tightening is all over the place. It’s a messy playbook. /4

For now, Goldilocks is winning the battle, and with the Fed pivoting the market is taking a page from the 1994-1995 cycle. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh