As we all get consumed by the US$/Kes exchange, the National Assembly Committee Report on the Affordable Housing Bill 2023 is out & I think we all need to pay close attention.

A number of proposals to amend the Bill have been thrown out, 10.0% deposit has been shelved.

A 🧵

A number of proposals to amend the Bill have been thrown out, 10.0% deposit has been shelved.

A 🧵

First, if you want context on the Affordable Housing Bill 2023 & its proposals in response to the 3-judge bench judgement which pronounced the levy to be unconstitutional, see quoted thread below

https://x.com/AmbokoJH/status/1732759532885934096?s=20

The committee:

· Has rejected the proposal to amend Sec4 to provide that deductions be pegged on basic as opposed to gross salary

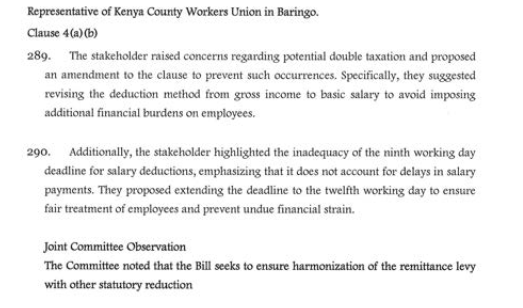

· Has rejected the proposal to extend the window for remittance from the 9th to the 12th working day

· Has rejected the proposal to amend Sec4 to provide that deductions be pegged on basic as opposed to gross salary

· Has rejected the proposal to extend the window for remittance from the 9th to the 12th working day

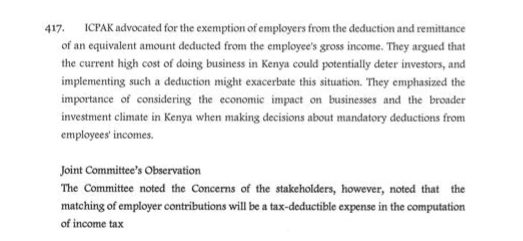

The Committee rejected the proposal to do away Sec5 of the Bill which provides for the mandatory requirement that employers match their employees' contribution with 1.5%. The Committee says the fact that the matching is tax deductible should be sufficient

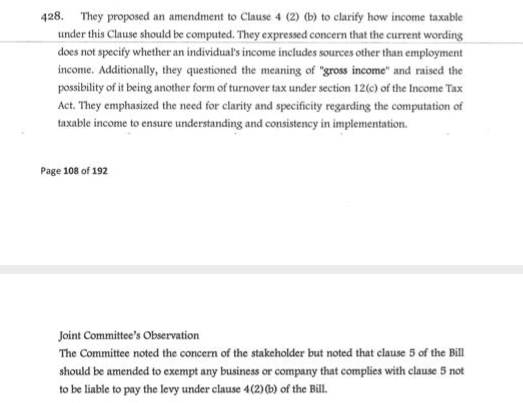

The Committee has endorsed a proposal to clean up the potential conflict between Sec4(2b) targeting non-payslip Kenyans & Sec5 which provides for employer matching. An amendment to be made exempting any business compliant with Sec5 from the obligations of 4(2b)

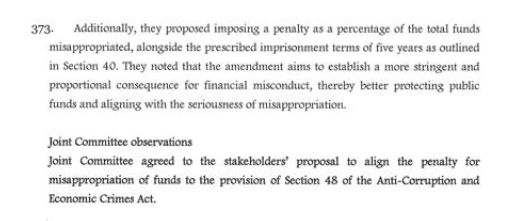

The Committee has endorsed the proposal to amend Sec40 (cii) the penalty imposed on persons who misappropriate the affordable housing levy funds from the fine not exceeding Kes 10.0M or jail term not exceeding 5 years to align with Sec48 of the Anti-Corruption Act

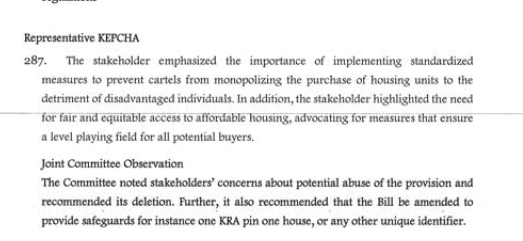

The committee proposes Sec30(2c) of the bill be amended to provide that housing units be allocated pegged on one KRA pin per house (or any other suitable unique identifier).

I am lost, isn't allocation based on consolidated household income? How will couple's incomes be mapped?

I am lost, isn't allocation based on consolidated household income? How will couple's incomes be mapped?

The Committee:

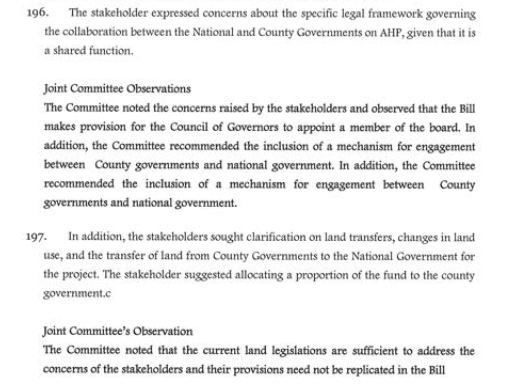

· Has thrown out concerns regarding collaboration between National & County govts. They argue the Bill provides for the Council of Governors to appoint a member to the Affordable Housing Board

· Has thrown out concerns regarding transfer of land

· Has thrown out concerns regarding collaboration between National & County govts. They argue the Bill provides for the Council of Governors to appoint a member to the Affordable Housing Board

· Has thrown out concerns regarding transfer of land

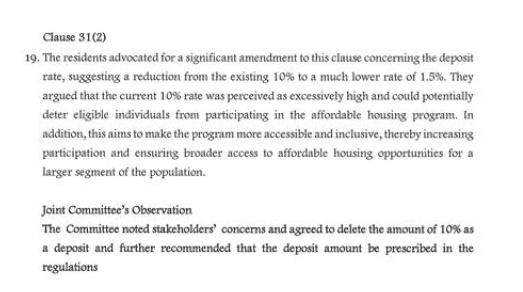

The committee has proposed that Sec31(2a) recommending the 10.0% mandatory deposit for one to be deemed eligible for the affordable housing units be dropped & guidelines be provided in the regulations

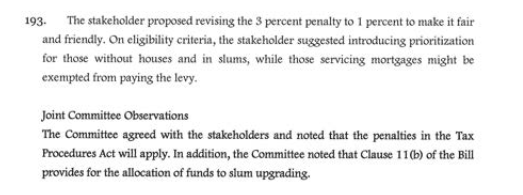

The Committee has recommended that Sec7 of the bill be amended to scale down the 3.0% penalty (of the unpaid amount) for one falling into arrears on remittance to the fund. Tax Procedures Act penalty will apply. The accrued penalties to be for slum upgrading

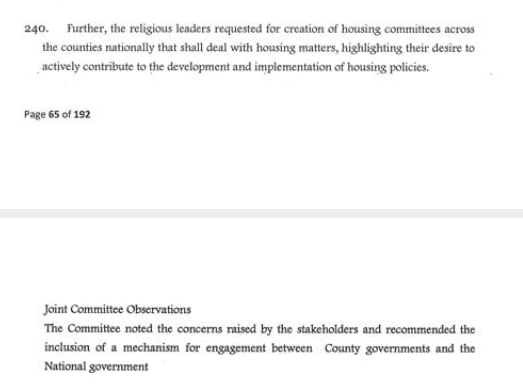

The Committee is proposing the Bill provides for the set up of 47 Housing Committees (one for each county) to provide a framework for engagement between National & County governments on matters housing.

Is this really necessary?

Is this really necessary?

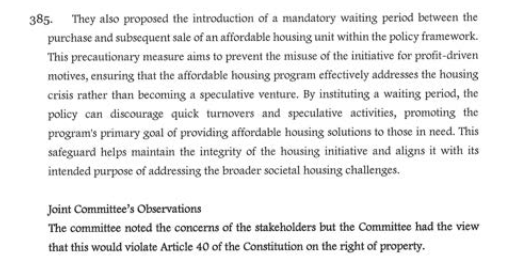

There was a proposal for provision of a mandatory waiting period between the purchase & sale of an affordable housing unit to address the risk of quick turnover & speculative ventures, it has been shot down by the Committee. I am a little surprised by this one

Finally

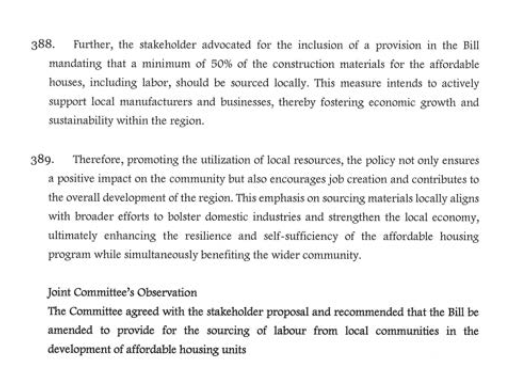

The committee has endorsed the proposal to have at least 50.0% of all material used in affordable housing, including labour, be sourced from local communities.

I just hope there will be standardisation of product.

The committee has endorsed the proposal to have at least 50.0% of all material used in affordable housing, including labour, be sourced from local communities.

I just hope there will be standardisation of product.

• • •

Missing some Tweet in this thread? You can try to

force a refresh