My Bloomberg Interview Notes - "Can The Rally Hold?"

Bloomberg hosts, Vonnie Quinn and Abigail Doolittle, have invited me on to talk about the macro backdrop I see forming as we head into the 2nd half of 2024.

In a 7 minute segment, no way can I get my perspective across, but in preparation for the interview Tuesday, I put together the following notes which I had sent to clients.

Here's the interview; Below the notes 🧵

Bloomberg hosts, Vonnie Quinn and Abigail Doolittle, have invited me on to talk about the macro backdrop I see forming as we head into the 2nd half of 2024.

In a 7 minute segment, no way can I get my perspective across, but in preparation for the interview Tuesday, I put together the following notes which I had sent to clients.

Here's the interview; Below the notes 🧵

What’s Bullish For Markets Into Year End?

1. Forward earnings growth. Actual earnings have been basically flat for 6 quarters, but EXPECTATIONS have triggered a closed loop of equity outperformance. Stocks have risen on strong forward earnings which are strong because analysts expect a strong economy supported by higher stocks.

1. Forward earnings growth. Actual earnings have been basically flat for 6 quarters, but EXPECTATIONS have triggered a closed loop of equity outperformance. Stocks have risen on strong forward earnings which are strong because analysts expect a strong economy supported by higher stocks.

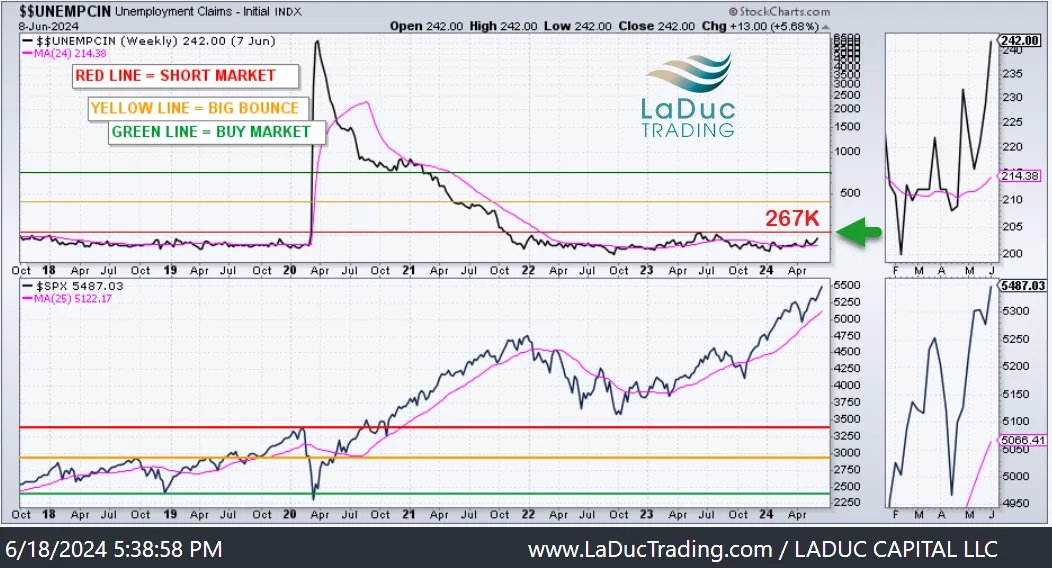

2. Jobs matter to forward earnings & equity returns.

Until we get/stay above 267K Unemployment Claims & 4.2% Unemployment Rate, volatility will stay subdued. And even after we get above, Fed will likely ease and give markets a short-term boost.

Until we get/stay above 267K Unemployment Claims & 4.2% Unemployment Rate, volatility will stay subdued. And even after we get above, Fed will likely ease and give markets a short-term boost.

3. Fed has the market’s back.

Market assumes the “Fed & Treasury Put” will enter on signs of equity or bond weakness or currency volatility. Bears need a macro trigger to interrupt the bullish flows (from CTAs, EM, HF, NAAIM positioning etc), not to mention the continued AI TECH ECOSYSTEM bullish option positioning.

More to the point: Fewest bears in recent history. Why? Equities of late, and bonds most recently, are pricing in economic growth acceleration and/or Fed cut/cuts.

Market assumes the “Fed & Treasury Put” will enter on signs of equity or bond weakness or currency volatility. Bears need a macro trigger to interrupt the bullish flows (from CTAs, EM, HF, NAAIM positioning etc), not to mention the continued AI TECH ECOSYSTEM bullish option positioning.

More to the point: Fewest bears in recent history. Why? Equities of late, and bonds most recently, are pricing in economic growth acceleration and/or Fed cut/cuts.

4. Election Year – by design or default, equities do well leading into an incumbent’s re-election.

Also, the assumed “Fed & Treasury Put” to make sure they keep their jobs.

Also, the assumed “Fed & Treasury Put” to make sure they keep their jobs.

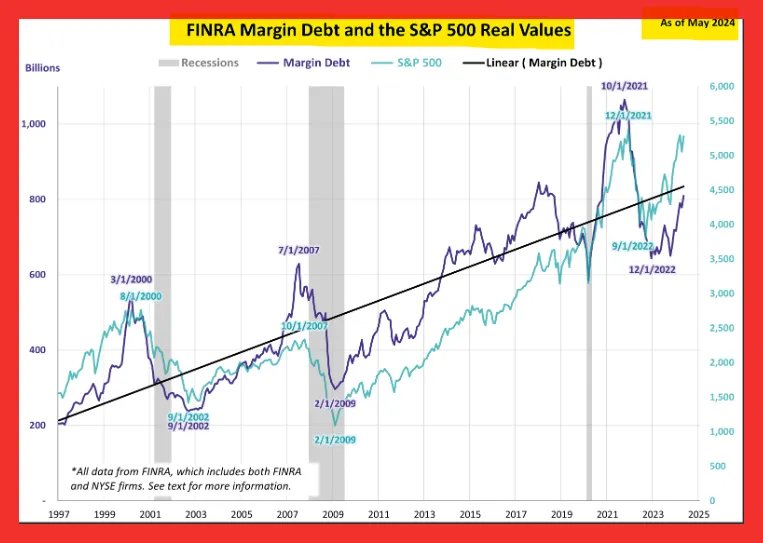

5. Margin Debt has not peaked/rolled over.

This has been a fabulous tell in prior market tops – where margin debt peaks and rolls over as deteriorating fundamentals take hold - versus event like Covid or 2018 Volmagedden/Repo plumbing drama.

This has been a fabulous tell in prior market tops – where margin debt peaks and rolls over as deteriorating fundamentals take hold - versus event like Covid or 2018 Volmagedden/Repo plumbing drama.

Risks To The Market’s Advance:

Aside from above bullish reasons reversing, here’s what is top of mind…

1. Bullish complacency from CONCENTRATION RISK amidst breadth divergences means that if we set aside AI stocks, we are in a declining stock market.

- RSP:SPY – Below 2009 lows

- IWM:SPY – Below 2004 lows

- IYT:SPY – Below 2004 lows

Even NDX:NDXE – very elevated = reversion to mean/profit taking in AI TECH ECOSYSTEM = Rotation into oversold + value plays.

The Risk: Selling can beget more selling.

Either way, defensives win: XLV, XLP, XLU

Aside from above bullish reasons reversing, here’s what is top of mind…

1. Bullish complacency from CONCENTRATION RISK amidst breadth divergences means that if we set aside AI stocks, we are in a declining stock market.

- RSP:SPY – Below 2009 lows

- IWM:SPY – Below 2004 lows

- IYT:SPY – Below 2004 lows

Even NDX:NDXE – very elevated = reversion to mean/profit taking in AI TECH ECOSYSTEM = Rotation into oversold + value plays.

The Risk: Selling can beget more selling.

Either way, defensives win: XLV, XLP, XLU

2. 10Y Yields break below 4.2% and 10Y2Y yield curve inverts more deeply (tags/stays below -.6%).

At first, it will be deemed bullish for equities & help loosen up the frozen housing market.

But then the narrative can change from INFLATION to DEFLATION:

- banks will need to be closely watched this earnings season for any shrinking of their net interest margin - which can lead to less bank lending

- thus forcing more corporate and household self-funding - depleting savings/selling assets

- resulting in reducing labor - and reduced consumer spending

- which triggers higher unemployment - and pulls forward recession risk.

At the same time this is occurring, the fed funds rate has become and will become more restrictive - as real rates rise.

At first, it will be deemed bullish for equities & help loosen up the frozen housing market.

But then the narrative can change from INFLATION to DEFLATION:

- banks will need to be closely watched this earnings season for any shrinking of their net interest margin - which can lead to less bank lending

- thus forcing more corporate and household self-funding - depleting savings/selling assets

- resulting in reducing labor - and reduced consumer spending

- which triggers higher unemployment - and pulls forward recession risk.

At the same time this is occurring, the fed funds rate has become and will become more restrictive - as real rates rise.

3. As Real Rate Rise, Inflation Expectations Fall but USD Rises.

- USD strength is a headwind to equities and carry trades (and delay the recent precious metal advance).

- Don’t be surprised if Fed then tries to talk down the rising USD with “more accommodation”.

- Banks start to roll over – (again, earnings kick off soon 7/17) – which can be precursor to jobless claims increasing with unemployment rate pushing higher.

- Should this play out next month, I would expect the FOMC 7/31 to pull forward rate cut considerations – especially as the YC inverts.

- Volatility also ‘bottoms’, seasonally, in July.

My bet: Bonds continue higher as 10Y yield breaks below 4.2%, but volatility doesn’t appear in earnest until UE breaks above 4.2%. And we know Fed/Treasury will accommodate before that happens. It is an election year after all!

- USD strength is a headwind to equities and carry trades (and delay the recent precious metal advance).

- Don’t be surprised if Fed then tries to talk down the rising USD with “more accommodation”.

- Banks start to roll over – (again, earnings kick off soon 7/17) – which can be precursor to jobless claims increasing with unemployment rate pushing higher.

- Should this play out next month, I would expect the FOMC 7/31 to pull forward rate cut considerations – especially as the YC inverts.

- Volatility also ‘bottoms’, seasonally, in July.

My bet: Bonds continue higher as 10Y yield breaks below 4.2%, but volatility doesn’t appear in earnest until UE breaks above 4.2%. And we know Fed/Treasury will accommodate before that happens. It is an election year after all!

4. Fed Balance Sheet is shrinking from QT, and with it, inflation expectations have fallen from 9.1% to 3.3%. This should continue UNTIL Fed rolls out QT again, because QE IS INFLATIONARY.

Point is: … Fed is behind the curve. Keeping rates at 5.5% with declining YoY CPI, have helped real rates to rise, which could trigger a stronger dollar – stronger than Fed/Treasury want.

Key Takeaway: Higher US real rates relative to other key partner countries will pressure USD higher.

This is what happened in 2007 before the Great Financial Crisis and before the 1997-1998 Asian Financial Crisis. Bears watching.

Point is: … Fed is behind the curve. Keeping rates at 5.5% with declining YoY CPI, have helped real rates to rise, which could trigger a stronger dollar – stronger than Fed/Treasury want.

Key Takeaway: Higher US real rates relative to other key partner countries will pressure USD higher.

This is what happened in 2007 before the Great Financial Crisis and before the 1997-1998 Asian Financial Crisis. Bears watching.

5. Global Credit Demand Matters Most

- Recession bets have dropped to only 5% from 28% just a year ago (BofA) - at the same time…

- Global Central Banks are now cutting rates and the US 10Y2Y yield curve is inverting more deeply - at the same time…

- The 10Y is more than 100 basis points below the Fed Funds Rate.

Translation: Bond market may be growing worried that Global Credit Demand is falling from too-high and higher-for-longer rates so global rate cuts are an economic necessity not political luxury.

- Recession bets have dropped to only 5% from 28% just a year ago (BofA) - at the same time…

- Global Central Banks are now cutting rates and the US 10Y2Y yield curve is inverting more deeply - at the same time…

- The 10Y is more than 100 basis points below the Fed Funds Rate.

Translation: Bond market may be growing worried that Global Credit Demand is falling from too-high and higher-for-longer rates so global rate cuts are an economic necessity not political luxury.

6. Election Uncertainty:

Biden, Trump, RFK – the election is not certain, but market doesn’t know it yet.

Biden, Trump, RFK – the election is not certain, but market doesn’t know it yet.

7. FX Competitive Devaluations:

Funding costs went negative as long bond and dollar went down, so the reverse/unwind/deleveraging could greatly reduce global credit demand - and with it inflation.

Watching banks and the 10Y2Y yield curve flattening a lot more, as well as rising USD which can cause FX yield differentials and credit spreads to widen, will cause that foreign capital that recently entered US equities markets to turn around and leave.

Funding costs went negative as long bond and dollar went down, so the reverse/unwind/deleveraging could greatly reduce global credit demand - and with it inflation.

Watching banks and the 10Y2Y yield curve flattening a lot more, as well as rising USD which can cause FX yield differentials and credit spreads to widen, will cause that foreign capital that recently entered US equities markets to turn around and leave.

Final Thoughts:

Markets are betting on Fed/Treasury policy interference to kick in - Fed Balance Sheet QE additions for example - on signs of true market stress. We seem far away from that point, but my point: THIS is what will excite inflation and higher yields.

At which point, markets will very likely reprice risk assets by pricing out the diminishing returns of policy interference.

But to get there, wouldn't it be ironic if the transmission mechanism is a bond short unwind that results in falling global credit demand which then triggers credit stress?!

Of course, I will never get to express my detailed views and charts in a Bloomberg appearance, but I wanted to layout for clients why the rally can hold AND how it can also be greatly challenged moving forward.

For more insights like these with - detailed macro-to-micro trades across all assets & timeframes - join me & my 10 client-dedicated contributors at !

LaDucTrading.com

laductrading.com

Markets are betting on Fed/Treasury policy interference to kick in - Fed Balance Sheet QE additions for example - on signs of true market stress. We seem far away from that point, but my point: THIS is what will excite inflation and higher yields.

At which point, markets will very likely reprice risk assets by pricing out the diminishing returns of policy interference.

But to get there, wouldn't it be ironic if the transmission mechanism is a bond short unwind that results in falling global credit demand which then triggers credit stress?!

Of course, I will never get to express my detailed views and charts in a Bloomberg appearance, but I wanted to layout for clients why the rally can hold AND how it can also be greatly challenged moving forward.

For more insights like these with - detailed macro-to-micro trades across all assets & timeframes - join me & my 10 client-dedicated contributors at !

LaDucTrading.com

laductrading.com

• • •

Missing some Tweet in this thread? You can try to

force a refresh