The economics profession is still not grappling with the magnitude of the intellectual error in underestimating full employment. I think it is worth rewinding the clock to see how badly the story was missed....

In 2018, Kearney and Abraham wrote a paper about the decline in employment ratios. They used data through 2016, and in it make zero mention of whether the incomplete recovery from the Great Recession was a factor. pinguet.free.fr/nber24333.pdf

Here is their table of what mattered and estimates of how much it mattered. Effects range from food stamps to the minimum wage to robots and trade. But nothing about the incomplete Great Recession recovery

The average prime employment rate in 2016 was 77.9%. Today it is 80.8%, a 2.9 pp improvement.

This is more than half of the 4.5 decline in their data, swamping trade, robots, and any other estimated effects.

This is more than half of the 4.5 decline in their data, swamping trade, robots, and any other estimated effects.

The paper was updated in August, 2019. Given that prime employmen had risen to 80.0, a 2.1 pp increase since the first draft, surely the slow recovery from the Great Recession should be added in to the new draft. nber.org/system/files/w…

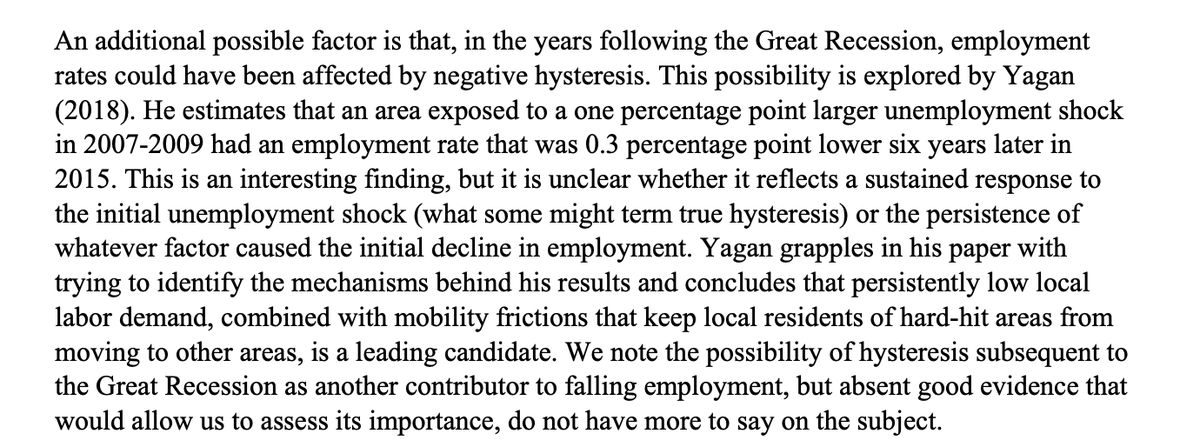

Yet even at this late date, the conventional academic wisdom on this question remained focused on structural stories. This is what they added about the Great Recession.

They note the possibility but given lack of evidence, have nothing more to say.

They note the possibility but given lack of evidence, have nothing more to say.

The paper was finally published in 2020 in the prestigious Journal of Economic Literature. Still at that date, the Great Recession is given a paragraph and "we do not have more to say" given the lack of evidence.

I want to emphasize that Abraham and Kearney are great economists who care a lot about this issue. You can also find the legendary Alan Krueger in 2015 argued "if anything , the standard U-3 measure of the unemployment rate understates the degree of labor market tightness in the current environment." econstor.eu/bitstream/1041…

This was a major failure of the profession, the backdrop for why the Fed began raising rates way too soon. I don't think we have really grappled with it, and the salutary effects of full employment remain underemphasized today.

• • •

Missing some Tweet in this thread? You can try to

force a refresh