This is a deep dive on @GM General Motors' 2Q financials released 2 hours ago.

Key takeaway: the numbers and trend looks good until you look at cash flow.

I'll provide a more indepth analysis once the 10-Q filings is out.

GM is up +2.5% pre-market (market is flat).

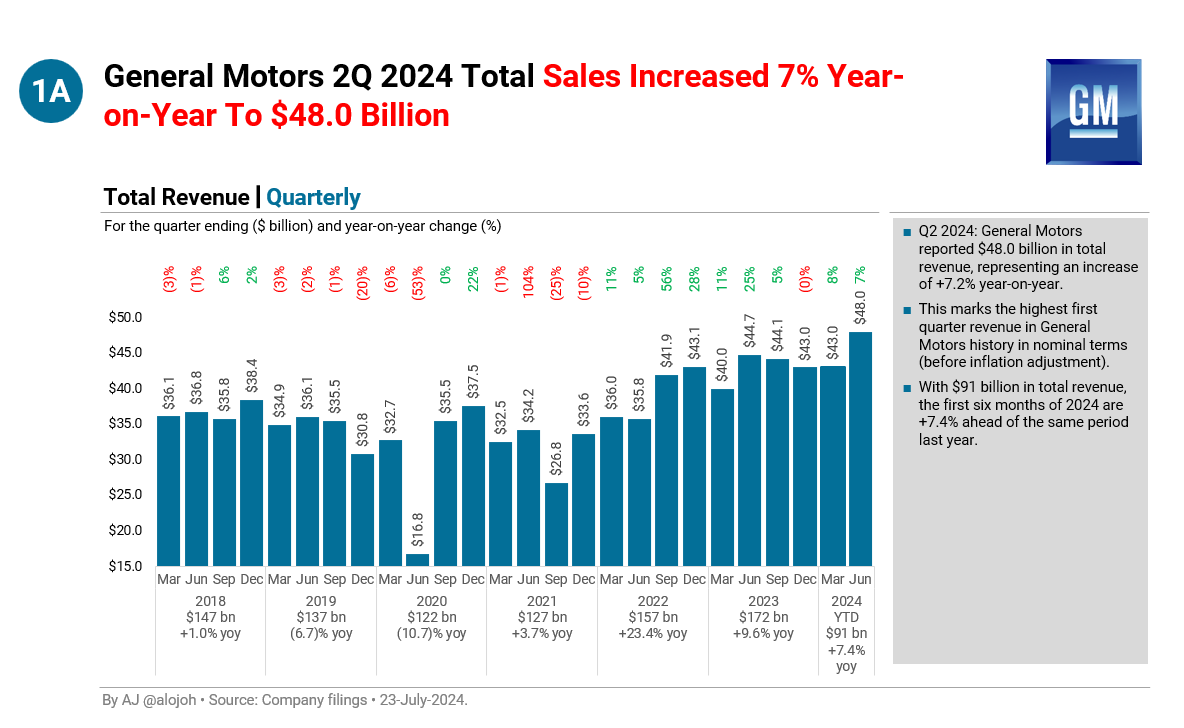

1A. General Motors 2Q 2024 Total Sales Increased 7% Year-on-Year To $48.0 Billion.

Key takeaway: the numbers and trend looks good until you look at cash flow.

I'll provide a more indepth analysis once the 10-Q filings is out.

GM is up +2.5% pre-market (market is flat).

1A. General Motors 2Q 2024 Total Sales Increased 7% Year-on-Year To $48.0 Billion.

1B. General Motors Lost All Growth Delivered In The 15 Years Post 2009 Bankruptcy. Current Revenu Level Remains Near The Level 15 Year Ago Adjusted For Inflation.

1C. GM's Main Segments Automotive And Financial Services Contribute 92% And 8% Of Revenue.

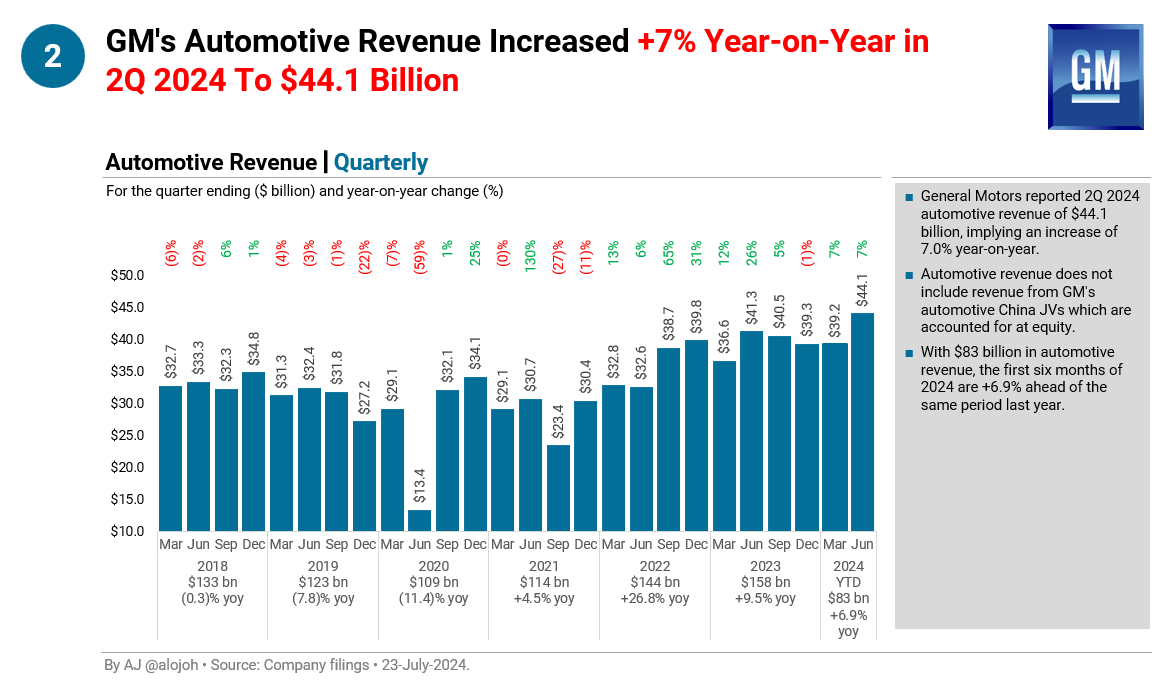

2. GM's Automotive Revenue Increased +7% Year-on-Year in 2Q 2024 To $44.1 Billion.

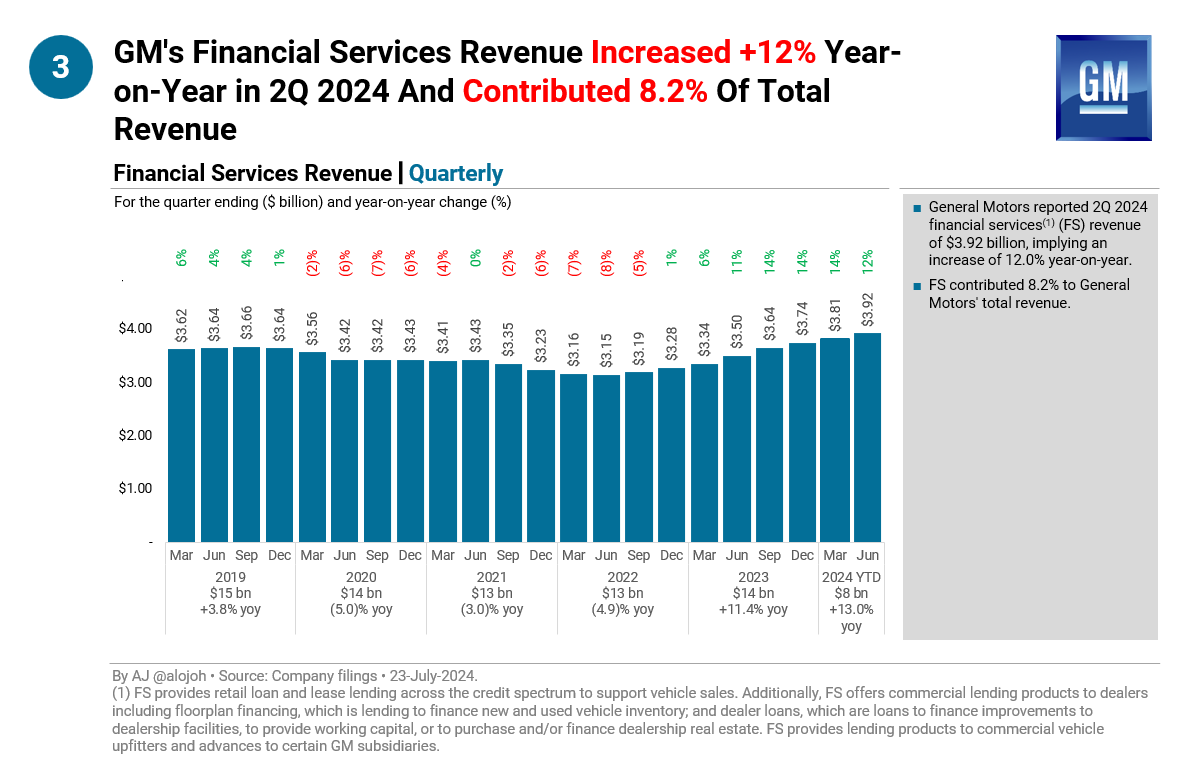

3. GM's Financial Services Revenue Increased +12% Year-on-Year in 2Q 2024 And Contributed 8.2% Of Total Revenue.

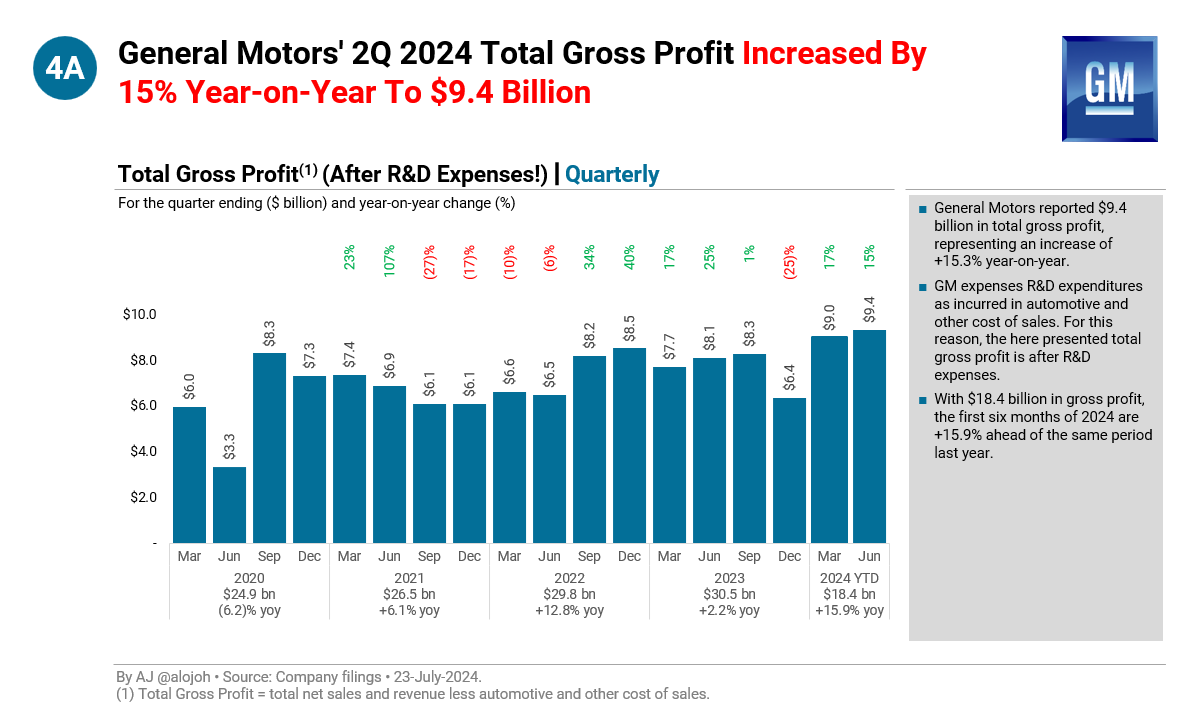

4A. General Motors' 2Q 2024 Total Gross Profit Increased By 15% Year-on-Year To $9.4 Billion.

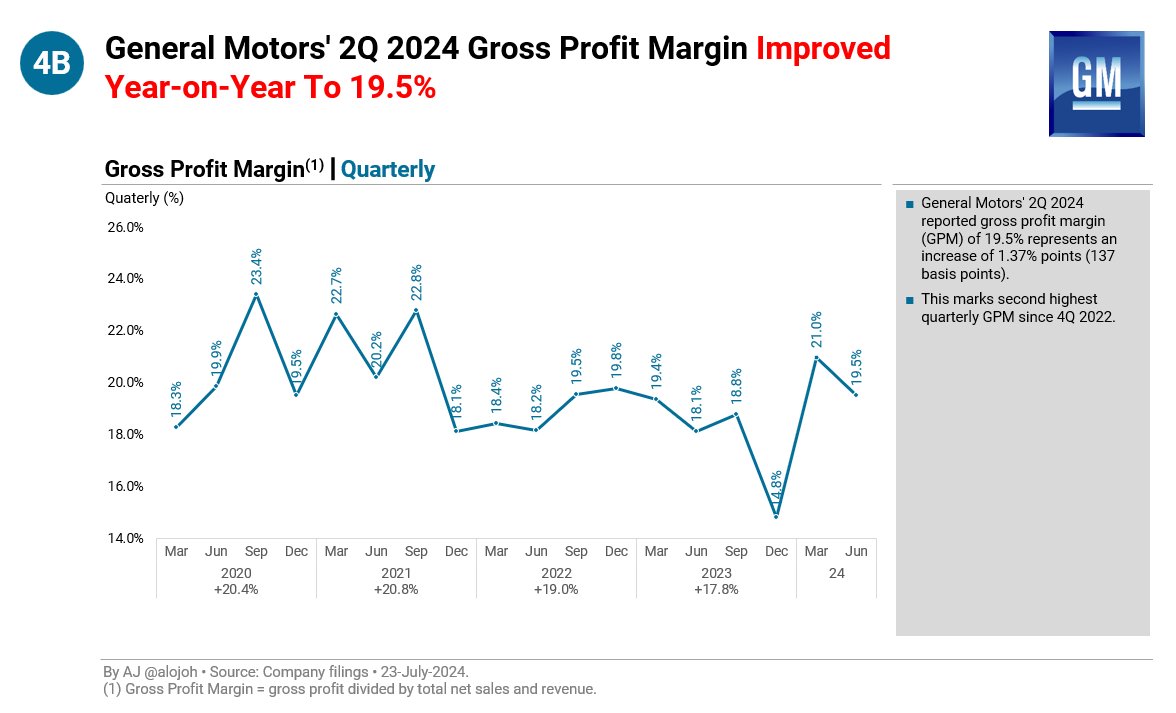

4B. General Motors' 2Q 2024 Gross Profit Margin Improved Year-on-Year To 19.5%.

5A. General Motors' 2Q 2024 SG&A Expenses Decreased By 7% Year-on-Year To $2.4 Billion.

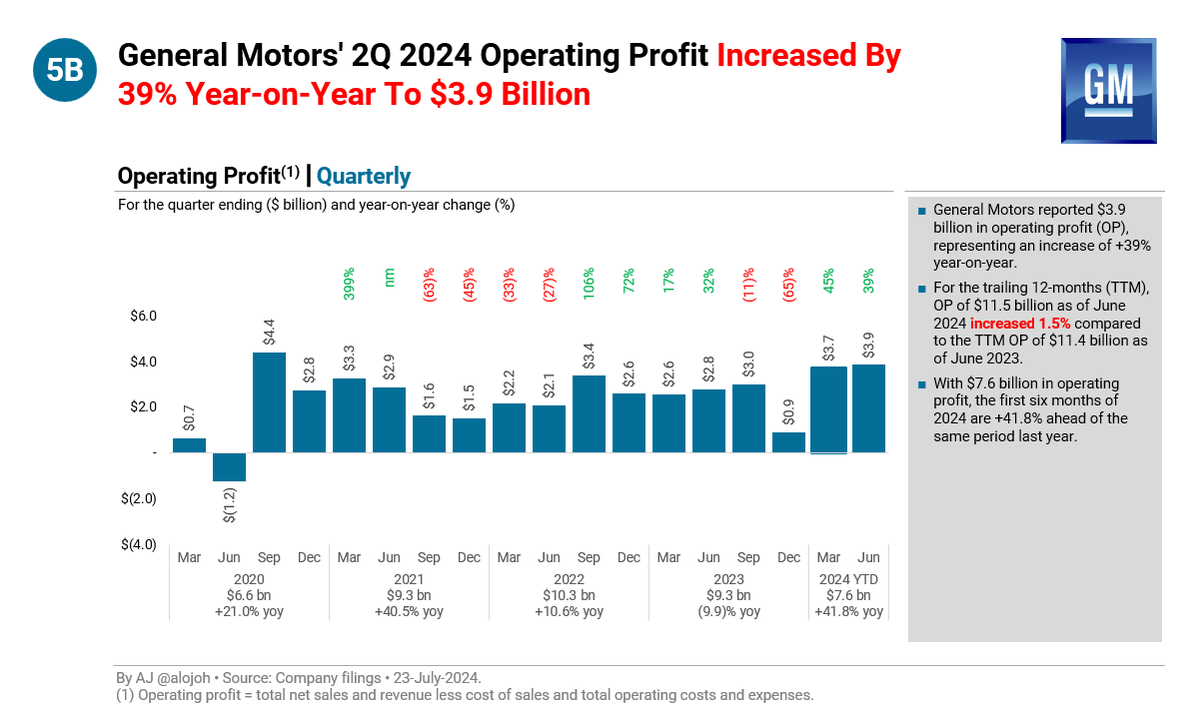

5B. General Motors' 2Q 2024 Operating Profit Increased By 39% Year-on-Year To $3.9 Billion.

5C. In 2Q 2024 GM's Operating Profit Margin Increased By 184 BPS To 8.1%.

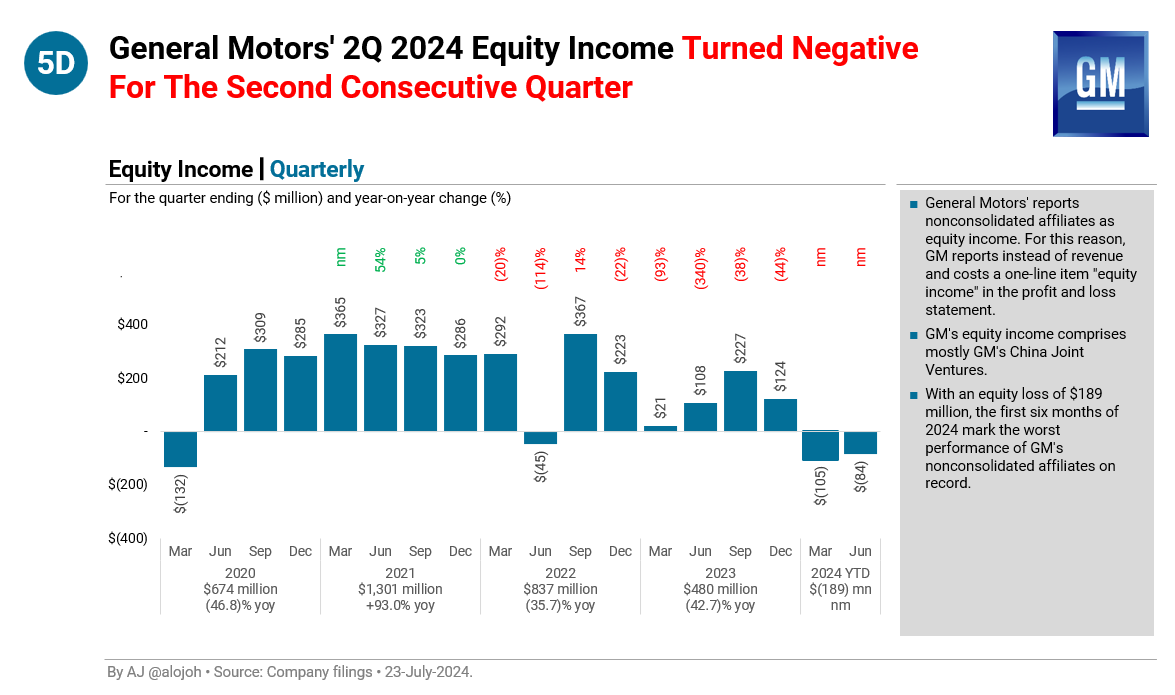

5D. General Motors' 2Q 2024 Equity Income Turned Negative For The Second Consecutive Quarter.

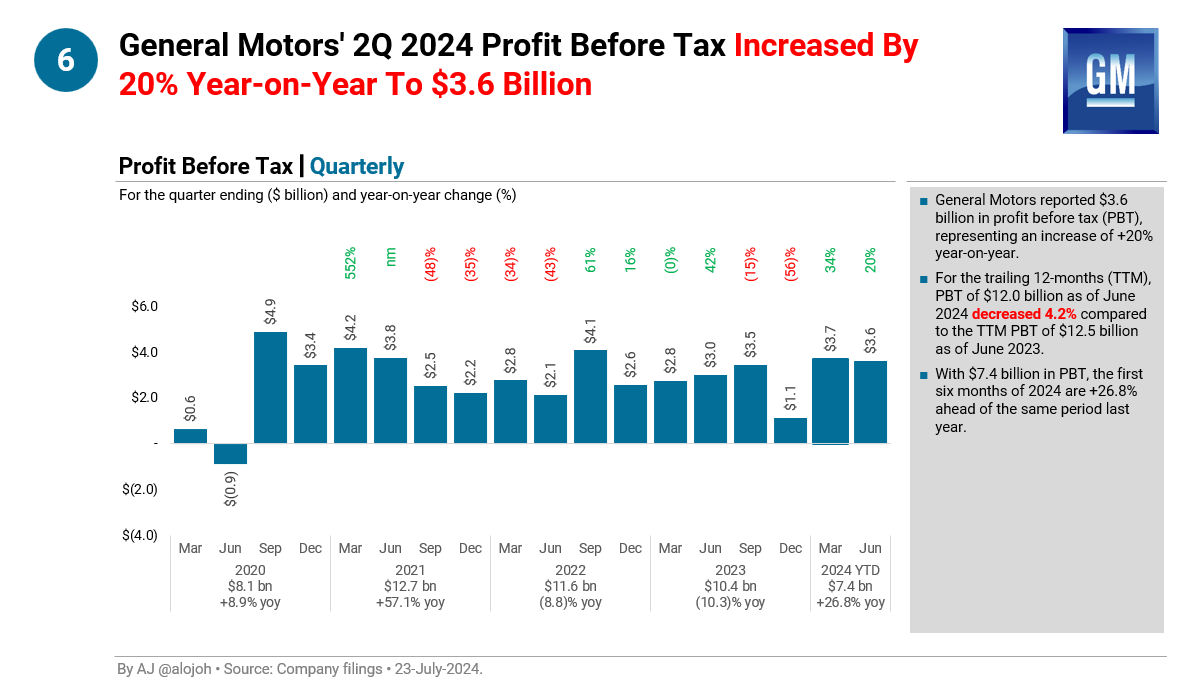

6. General Motors' 2Q 2024 Profit Before Tax Increased By 20% Year-on-Year To $3.6 Billion.

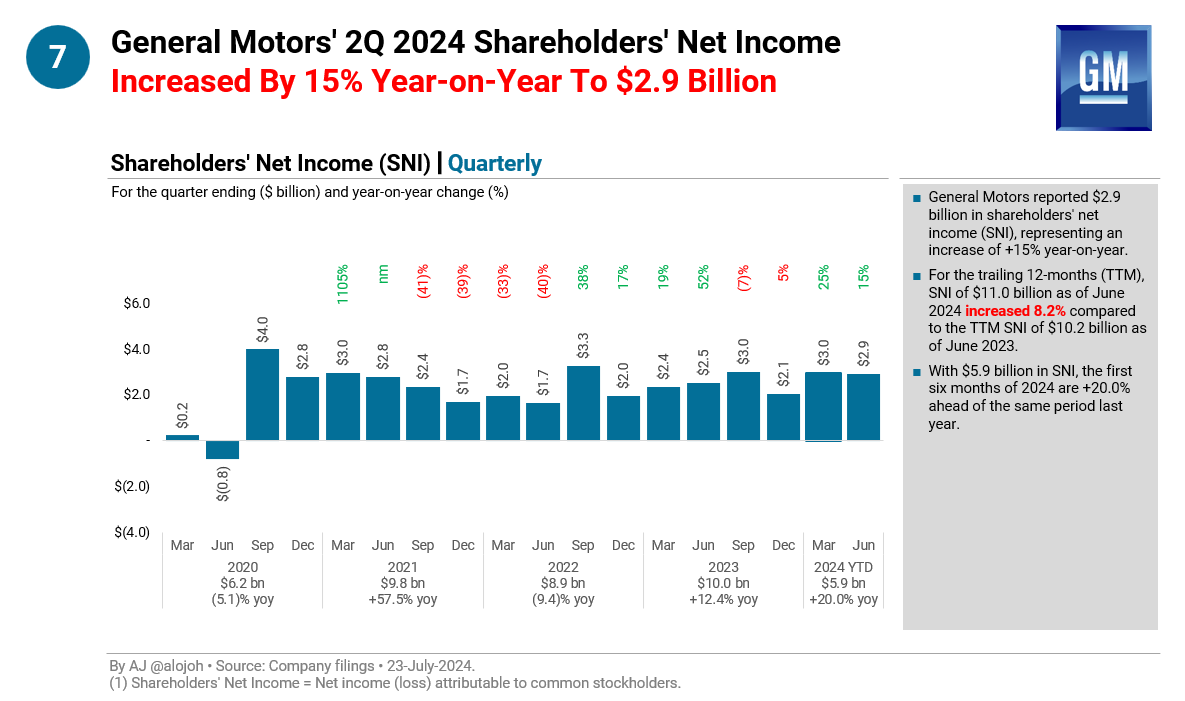

7. General Motors' 2Q 2024 Shareholders' Net Income Increased By 15% Year-on-Year To $2.9 Billion.

8A. General Motors' 2Q 2024 Free Cash Flow Decreased By 36% Year-on-Year To $3.4 Billion.

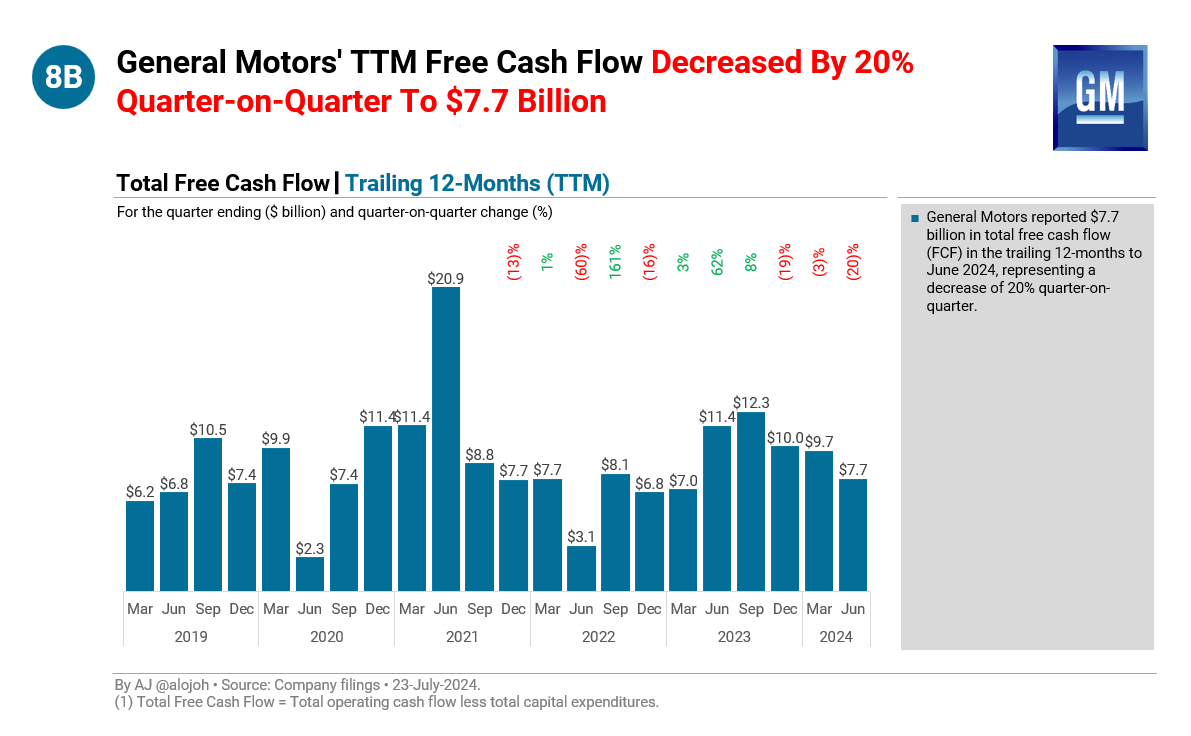

8B. General Motors' TTM Free Cash Flow Decreased By 20% Quarter-on-Quarter To $7.7 Billion.

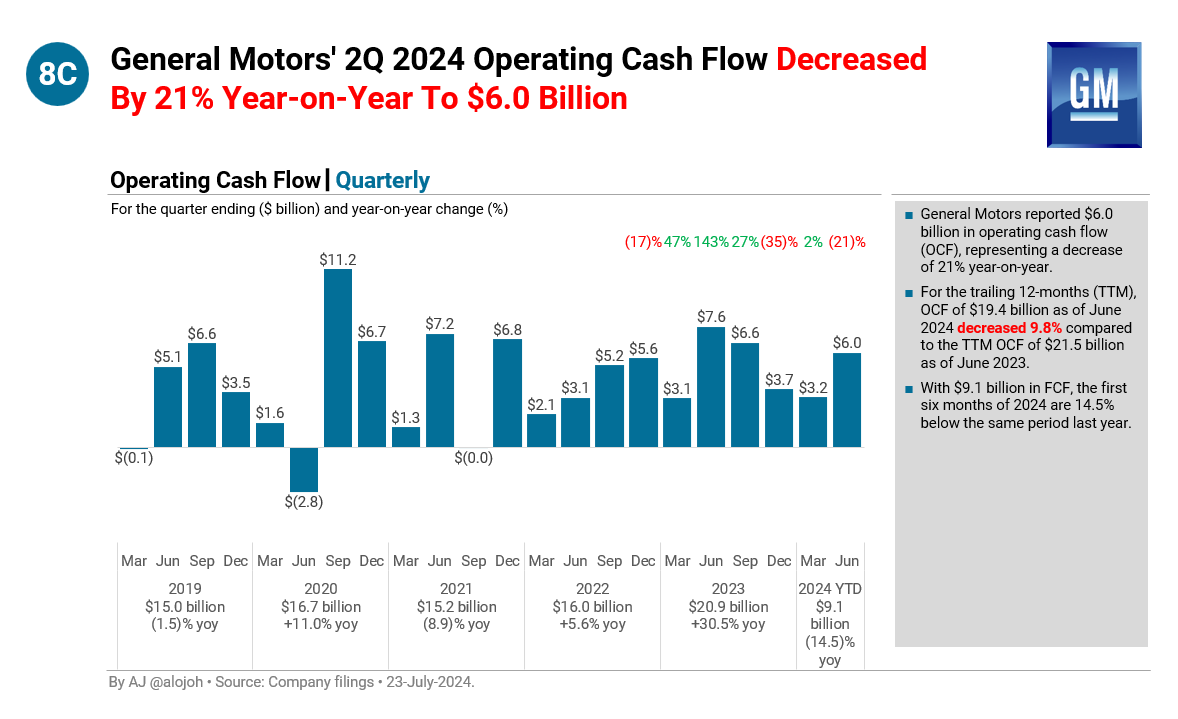

8C. General Motors' 2Q 2024 Operating Cash Flow Decreased By 21% Year-on-Year To $6.0 Billion.

8D. General Motors' TTM Operating Cash Flow Decreased By 7.7% Quarter-on-Quarter To $19.4 Billion.

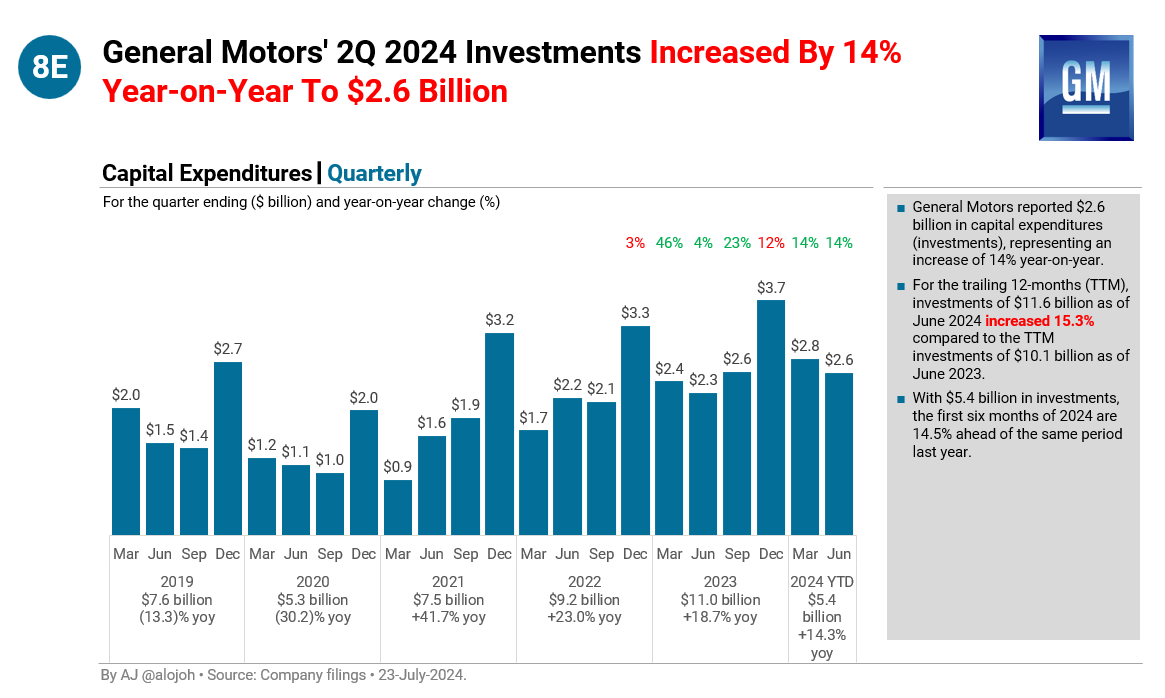

8E. General Motors' 2Q 2024 Investments Increased By 14% Year-on-Year To $2.6 Billion.

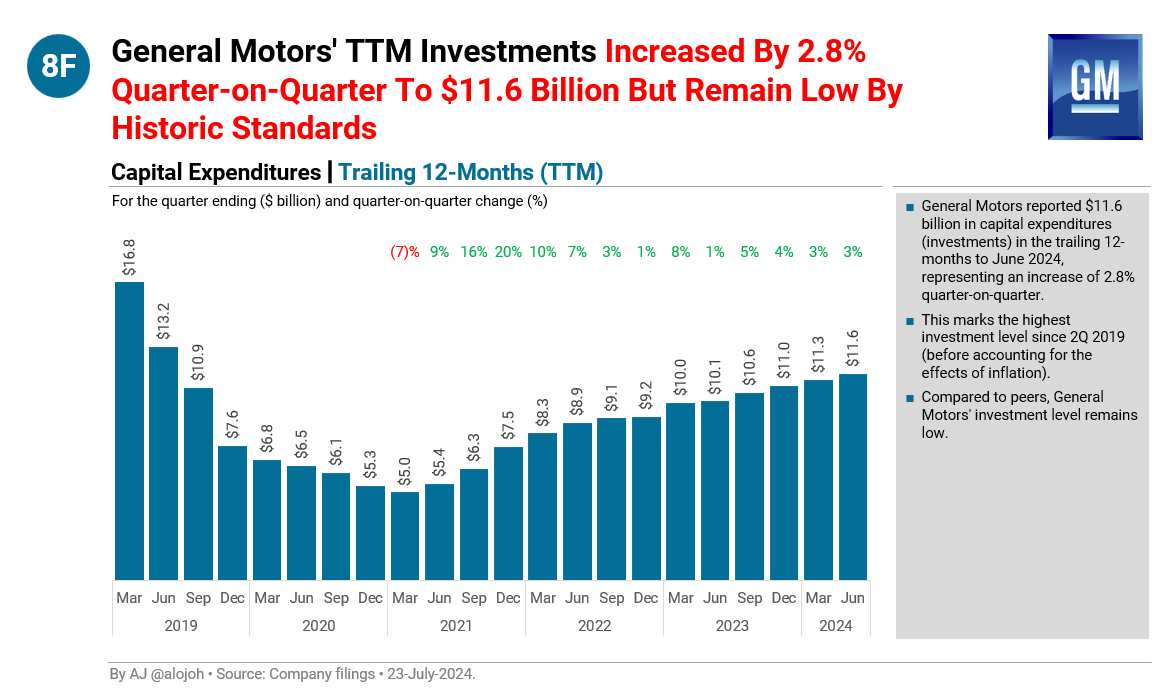

8F. General Motors' TTM Investments Increased By 2.8% Quarter-on-Quarter To $11.6 Billion But Remain Low By Historic Standards.

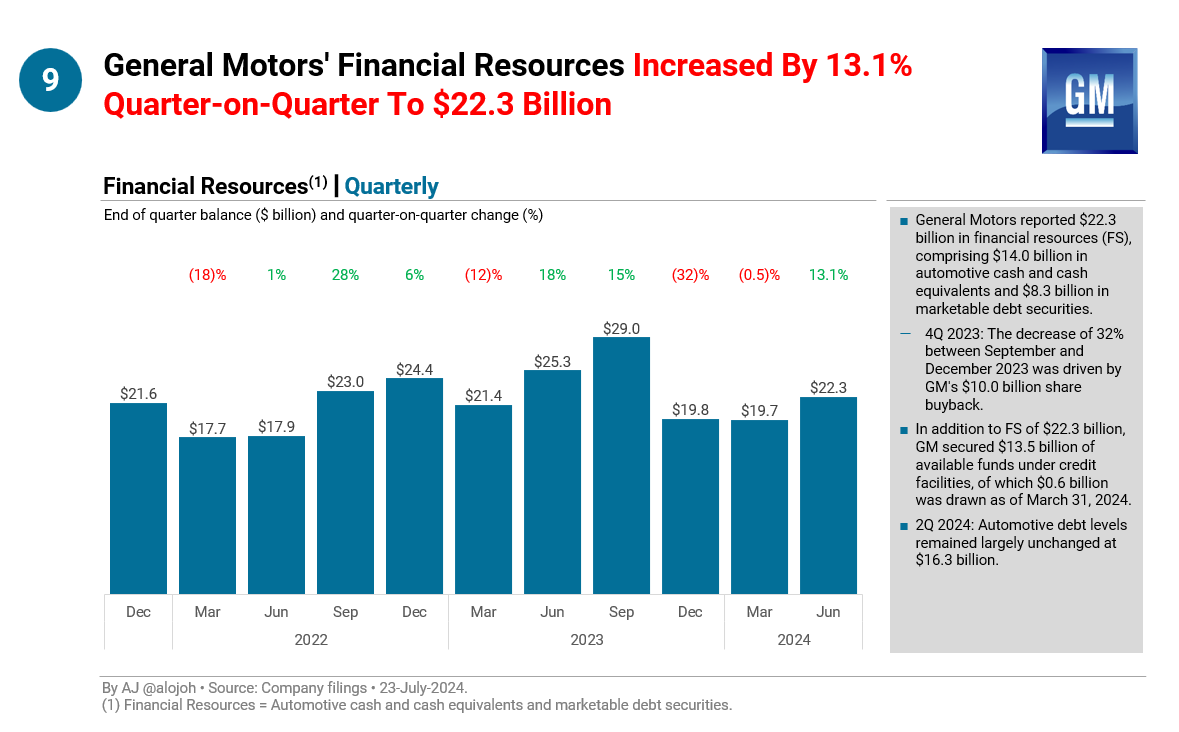

9. General Motors' Financial Resources Increased By 13.1% Quarter-on-Quarter To $22.3 Billion.

• • •

Missing some Tweet in this thread? You can try to

force a refresh