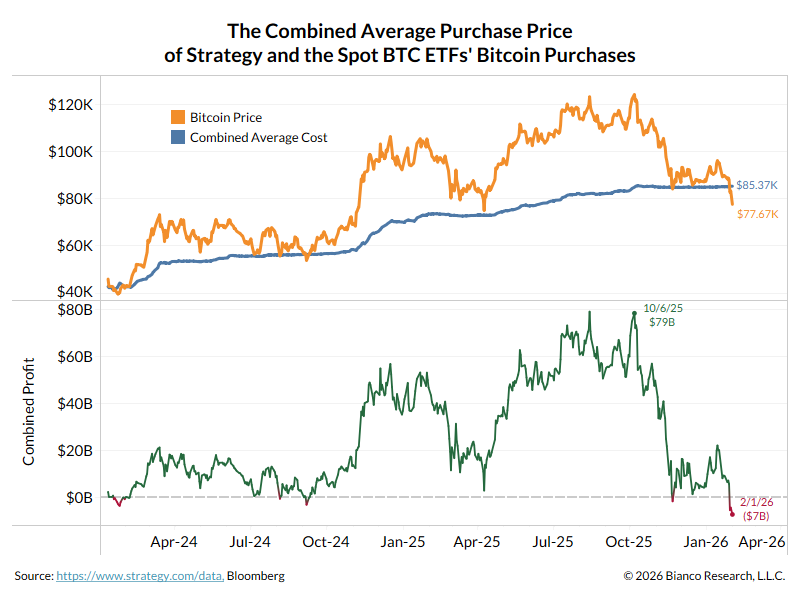

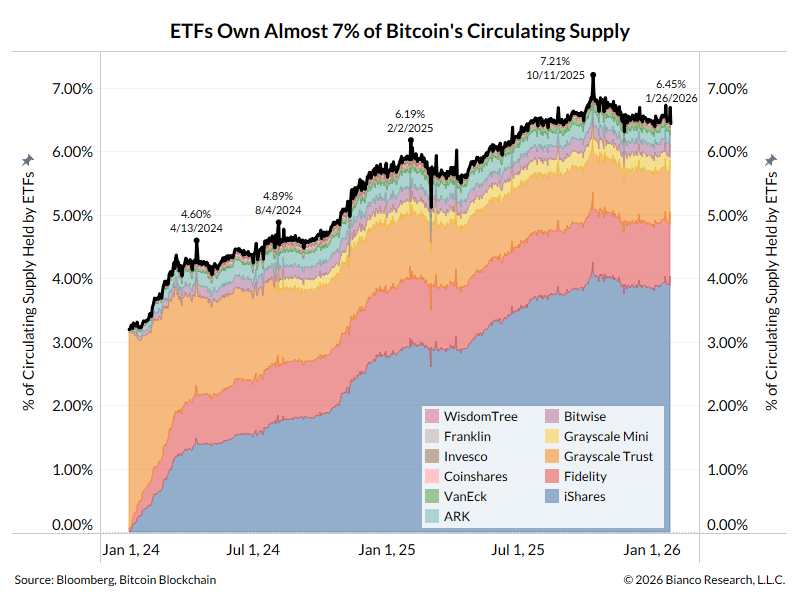

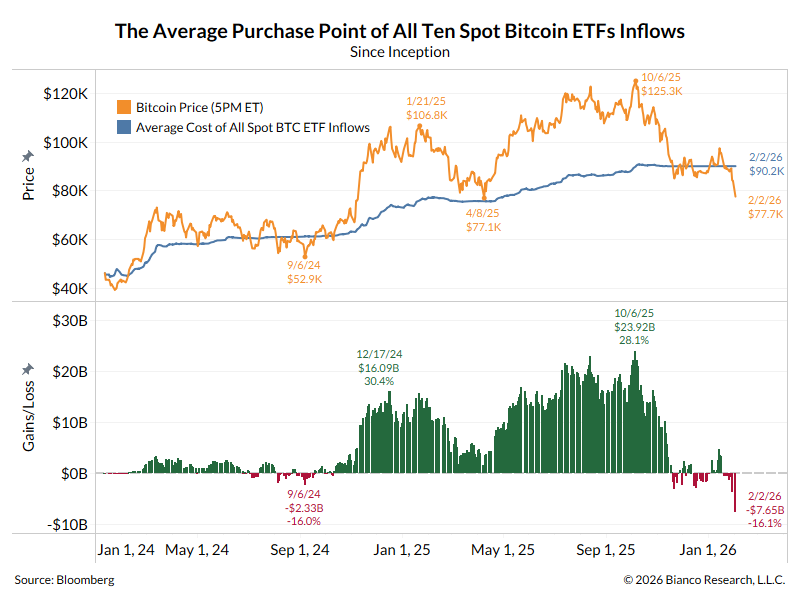

1/12

🧵on my take on what is happening in financial markets.

tl:dr:

Not all sharp moves in financial markets are driven by rapid changes in the economic outlook. Unexpected changes in the financial structure of the markets can also force repricing.

The most recent move in the markets has been driven by the Bank of Japan’s larger-than-expected hike last week, which led to a subsequent unwinding of the yen carry trade.

In other words, everyone is right to be mad at the central bank. The problem is that most blame the wrong central bank; they should focus on the Bank of Japan.

This is the Fed's dilemma. The catalyst for the yen carry trade unwind is the narrowing of the interest rate spread between Japan and the US, which has been caused by the Bank of Japan's hike. But if the Fed succumbs to market demands and cuts rates, it will narrow this spread further and worsen it.

(see post 12/12 for its implications for the U.S. economy)

🧵on my take on what is happening in financial markets.

tl:dr:

Not all sharp moves in financial markets are driven by rapid changes in the economic outlook. Unexpected changes in the financial structure of the markets can also force repricing.

The most recent move in the markets has been driven by the Bank of Japan’s larger-than-expected hike last week, which led to a subsequent unwinding of the yen carry trade.

In other words, everyone is right to be mad at the central bank. The problem is that most blame the wrong central bank; they should focus on the Bank of Japan.

This is the Fed's dilemma. The catalyst for the yen carry trade unwind is the narrowing of the interest rate spread between Japan and the US, which has been caused by the Bank of Japan's hike. But if the Fed succumbs to market demands and cuts rates, it will narrow this spread further and worsen it.

(see post 12/12 for its implications for the U.S. economy)

2/12

Last Wednesday, July 31, the Bank of Japan hiked rates to 0.25%, Its highest rate since 2008. This marked the second hike this year.

Last Wednesday, July 31, the Bank of Japan hiked rates to 0.25%, Its highest rate since 2008. This marked the second hike this year.

3/12

The surge in Japan’s inflation drove this decision. While inflation has decreased over the past year, the concern is it will persist near current levels.

The surge in Japan’s inflation drove this decision. While inflation has decreased over the past year, the concern is it will persist near current levels.

4/n

Note only 29% of respondents to a Bloomberg poll expected a Bank of Japan hike on July 31.

Note only 29% of respondents to a Bloomberg poll expected a Bank of Japan hike on July 31.

5/12

Overnight Index Swaps market (OIS) discounted just five basis points of hiking.

When the Bank of Japan surprised with a 15 basis point hike (chart above), the post-meeting spike shown below indicates how much of a surprise this move was (last two labels).

Overnight Index Swaps market (OIS) discounted just five basis points of hiking.

When the Bank of Japan surprised with a 15 basis point hike (chart above), the post-meeting spike shown below indicates how much of a surprise this move was (last two labels).

6/12

The surprise Bank of Japan hike led to one of the biggest unwinds of the yen carry trade.

First, how big is this trade?

No definitive statistic shows its size, so we have to infer it from the size of the Bank of Japan’s balance sheet.

The chart below shows the Bank of Japan’s balance sheet is larger than the country’s GDP, at 127.5% of GDP. By comparison, the Fed’s balance sheet is 25% of GDP.

If you think the Fed matters to markets, the Bank of Japan has a 5x larger influence on their economy.

The surprise Bank of Japan hike led to one of the biggest unwinds of the yen carry trade.

First, how big is this trade?

No definitive statistic shows its size, so we have to infer it from the size of the Bank of Japan’s balance sheet.

The chart below shows the Bank of Japan’s balance sheet is larger than the country’s GDP, at 127.5% of GDP. By comparison, the Fed’s balance sheet is 25% of GDP.

If you think the Fed matters to markets, the Bank of Japan has a 5x larger influence on their economy.

7/12

Here are the absolute sizes of the central bank balance sheets.

Here are the absolute sizes of the central bank balance sheets.

8/12

What Is the Yen Carry Trade?

Japan’s short-term funding rates (shown above) were the lowest globally. They still are.

However, short-term Japanese rates were also perceived to be predictable and would remain near zero for some time. When the time to hike rates eventually arrived, it would not look like last week: a surprise move with promises of more moves to come.

With the cost of funding rising, we see massive liquidations of positions using this cheap money.

Naturally, the biggest positions using the yen carry trade are in the Japanese markets. In the last three trading days, or since the surprise Bank of Japan hike on July 31, the Japanese stock market has crashed by 20%, even bigger than the three worst three-day moves during the October 1987 crash!

If you’re looking for an indication of this trade’s size, this is as close to a smoking gun as you will find. Remember, the Japanese stock market does not crash because U.S. payrolls missed expectations.

What Is the Yen Carry Trade?

Japan’s short-term funding rates (shown above) were the lowest globally. They still are.

However, short-term Japanese rates were also perceived to be predictable and would remain near zero for some time. When the time to hike rates eventually arrived, it would not look like last week: a surprise move with promises of more moves to come.

With the cost of funding rising, we see massive liquidations of positions using this cheap money.

Naturally, the biggest positions using the yen carry trade are in the Japanese markets. In the last three trading days, or since the surprise Bank of Japan hike on July 31, the Japanese stock market has crashed by 20%, even bigger than the three worst three-day moves during the October 1987 crash!

If you’re looking for an indication of this trade’s size, this is as close to a smoking gun as you will find. Remember, the Japanese stock market does not crash because U.S. payrolls missed expectations.

9/12

The yen carry trade is also behind the funding of many markets outside Japan. But the Bank of Japan’s surprise move has strained these trades.

The bottom panel of the next chart shows the dollar has lost 5% of its value against the yen over the last three trading days, again going back to the July 31 Bank of Japan meeting.

Why? Global yen carry trades are being unwound in a big way. This involves existing positions in foreign markets, like the dollar, and bringing these funds home to Japan to close these funding positions. This causes massive buying of yen.

The yen carry trade is also behind the funding of many markets outside Japan. But the Bank of Japan’s surprise move has strained these trades.

The bottom panel of the next chart shows the dollar has lost 5% of its value against the yen over the last three trading days, again going back to the July 31 Bank of Japan meeting.

Why? Global yen carry trades are being unwound in a big way. This involves existing positions in foreign markets, like the dollar, and bringing these funds home to Japan to close these funding positions. This causes massive buying of yen.

10/12

This is causing a slump in foreign markets, such as the U.S. stock market, which is seeing one of its biggest corrections since the October 2022 bear market low.

This is causing a slump in foreign markets, such as the U.S. stock market, which is seeing one of its biggest corrections since the October 2022 bear market low.

11/12

As the next chart shows, the world is running to risk-off markets like U.S. Treasuries, as all markets worldwide are under stress.

As the next chart shows, the world is running to risk-off markets like U.S. Treasuries, as all markets worldwide are under stress.

12/12

Conclusion

We would argue that much of the recent market chaos concerns financial issues around the yen carry trade. The Bank of Japan’s surprise move to increase funding rates, coupled with the belief that more such hikes are coming, spooked markets and led to an unwinding of this global trade.

As this happens, we see plenty of stories attributing this move to the U.S. economy. The Sahm Rule has been triggered, so there is concern the U.S. economy is already in a recession.

We frequently quote the late MIT economist Rudi Dornbusch:

Economic expansions do not die of old age; they are murdered.

Such financial moves can potentially “murder” the economy into recession. The last such concern of a financial “murder” occurred in March 2023, around the failure of Silicon Valley Bank. The economy was able to avoid this murder.

We would guess the U.S. economy can withstand the current yen carry unwind. Hence, we remain in the "no-landing" camp.

But there is a real risk the economy will not succumb to market volatility. Markets will remain chaotic until this unwind is done.

Conclusion

We would argue that much of the recent market chaos concerns financial issues around the yen carry trade. The Bank of Japan’s surprise move to increase funding rates, coupled with the belief that more such hikes are coming, spooked markets and led to an unwinding of this global trade.

As this happens, we see plenty of stories attributing this move to the U.S. economy. The Sahm Rule has been triggered, so there is concern the U.S. economy is already in a recession.

We frequently quote the late MIT economist Rudi Dornbusch:

Economic expansions do not die of old age; they are murdered.

Such financial moves can potentially “murder” the economy into recession. The last such concern of a financial “murder” occurred in March 2023, around the failure of Silicon Valley Bank. The economy was able to avoid this murder.

We would guess the U.S. economy can withstand the current yen carry unwind. Hence, we remain in the "no-landing" camp.

But there is a real risk the economy will not succumb to market volatility. Markets will remain chaotic until this unwind is done.

• • •

Missing some Tweet in this thread? You can try to

force a refresh