In 10 lines of Python code, I can do a full portfolio optimization.

This is wild. Let me show how:

This is wild. Let me show how:

1. Load Python libraries

These are the python packages and functions we'll use.

These are the python packages and functions we'll use.

2. Create a Maximum Sharpe Ratio Portfolio

We create a Maximum Sharpe Ratio model and then fit it on the training set.

portfolio_params are parameters passed to the Portfolio returned by the predict method.

We create a Maximum Sharpe Ratio model and then fit it on the training set.

portfolio_params are parameters passed to the Portfolio returned by the predict method.

3. Create a Benchmark

This is an inverse volatility portfolio that I'll compare my Max Sharpe portfolio against.

This is an inverse volatility portfolio that I'll compare my Max Sharpe portfolio against.

4. Out-Of-Sample Performance

Use Predict Method to get out-of-sample Portfolio Performance

Use Predict Method to get out-of-sample Portfolio Performance

5. Portfolio Composition

The visualizations from skfolio are incredible.

The visualizations from skfolio are incredible.

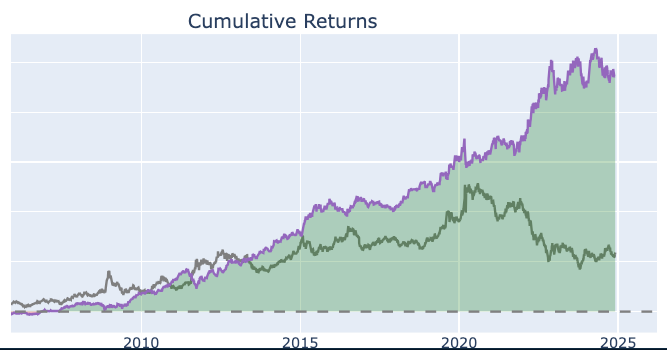

6. Cumulative Returns

In 1 line of code, we can get cumulative returns for our portfolio and benchmark.

In 1 line of code, we can get cumulative returns for our portfolio and benchmark.

7. Performance Tear Sheet

In 1 line of code, I get a comprehensive performance tear sheet to share with clients.

In 1 line of code, I get a comprehensive performance tear sheet to share with clients.

Want to learn how to build algorithmic trading strategies in Python (that actually work)?

👉 Join us live for our free training (500 seats): learn.quantscience.io/python-algorit…

👉 Join us live for our free training (500 seats): learn.quantscience.io/python-algorit…

• • •

Missing some Tweet in this thread? You can try to

force a refresh