🧵 Thread: Why Starlink's direct-to-cell capabilities is falling behind, further strengthening AST SpaceMobile's $ASTS early mover advantage.

The market isn’t fully considering the possibility that Starlink’s direct-to-cell service might fall short or even fail entirely. Meanwhile, AST is the real leader in this space, and it will take years for others, including Starlink, to catch up.

I'm calling out Starlink’s bluff.

The market isn’t fully considering the possibility that Starlink’s direct-to-cell service might fall short or even fail entirely. Meanwhile, AST is the real leader in this space, and it will take years for others, including Starlink, to catch up.

I'm calling out Starlink’s bluff.

Elon Musk has a history of overpromising moonshot tech.

Look at Tesla: the Roadster and Full Self-Driving (FSD) have been “coming soon” for years, and they still haven’t fully materialized.

This pattern extends to Starlink’s direct-to-cell offering—it could be another example of Musk over-promising without delivering.

Look at Tesla: the Roadster and Full Self-Driving (FSD) have been “coming soon” for years, and they still haven’t fully materialized.

This pattern extends to Starlink’s direct-to-cell offering—it could be another example of Musk over-promising without delivering.

https://x.com/kingtutcap/status/1815881716395040883

Musk’s business approach is simple: come up with big, moonshot ideas, promise the earliest possible launch date, and then scramble to figure out how to deliver.

It’s worked for Tesla in the past, but not everything he promises is going to work out—especially with something as complex as direct-to-cell satellite communication.

money.usnews.com/investing/arti…

businessinsider.com/what-elon-musk…

It’s worked for Tesla in the past, but not everything he promises is going to work out—especially with something as complex as direct-to-cell satellite communication.

money.usnews.com/investing/arti…

businessinsider.com/what-elon-musk…

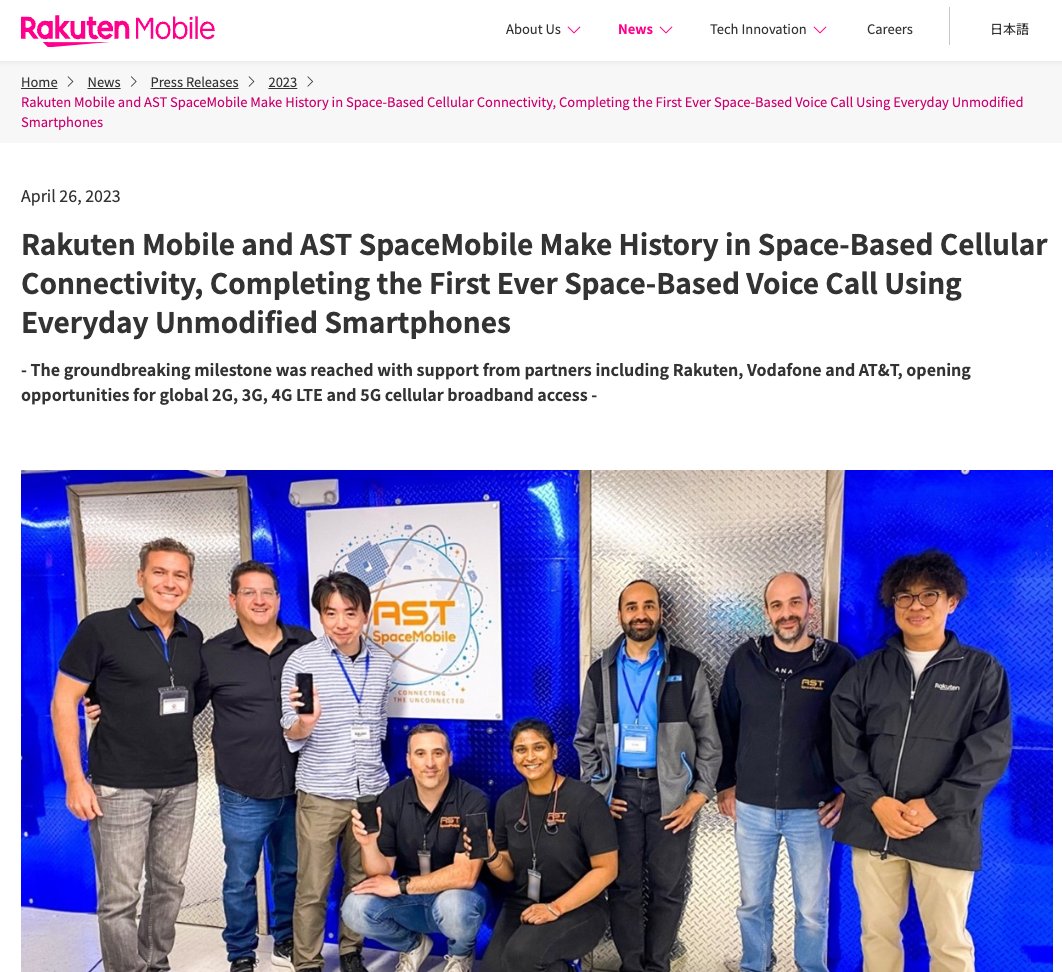

$ASTS has worked closely with mobile network operators (MNOs) like Vodafone, Rakuten, and AT&T from the start, conducting rigorous testing and fine-tuning their technology to meet the needs of MNOs.

Vodafone and Rakuten even participated in AST’s Series A funding, and AT&T has been testing with AST for the past 6 years, as per Chris Sambar.

vodafone.com/news/empowerin…

Vodafone and Rakuten even participated in AST’s Series A funding, and AT&T has been testing with AST for the past 6 years, as per Chris Sambar.

vodafone.com/news/empowerin…

A key question: when did Starlink actually test its service with MNOs prior to the big T-Mobile announcement in August 2022?

Unlike $ASTS, which has years of MNO collaboration under its belt, Starlink seems to have jumped in without any extensive real-world testing.

Unlike $ASTS, which has years of MNO collaboration under its belt, Starlink seems to have jumped in without any extensive real-world testing.

https://x.com/kingtutcap/status/1828578024826007624

Starlink entered the direct-to-cell space through its acquisition of Swarm, a satellite constellation designed for IoT devices. Retrofitting it for cellular use goes against basic engineering principles—“If it doesn’t fit, don’t force it.”

Swarm’s technology wasn't designed for cellular use, and it shows.

Swarm’s technology wasn't designed for cellular use, and it shows.

https://x.com/kingtutcap/status/1824629243831071085

Starlink first promised beta testing of its direct-to-cell service in late 2023. That timeline then shifted to fall 2024, and now T-Mobile’s CEO says it could be late 2024 or even early 2025.

And even then, it’s unclear what kind of service will actually be offered—text, voice, or data?

And even then, it’s unclear what kind of service will actually be offered—text, voice, or data?

https://x.com/kingtutcap/status/1836819268115255530

Starlink’s direct-to-cell announcement in August 2022 felt rushed. At the time, other players like Globalsat with Apple and $ASTS with AT&T were preparing for similar announcements. Musk likely saw this coming and wanted to “beat” them to it with a half-baked announcement.

The timing? Just weeks before Globalsat/Apple and AST’s BW3 launch.

Coincidence of course :)

The timing? Just weeks before Globalsat/Apple and AST’s BW3 launch.

Coincidence of course :)

https://x.com/kingtutcap/status/1808560233544884341

After the T-Mobile deal, Starlink quickly signed up several other MNOs in different countries (Optus, One NZ, Rogers, KDDI, etc.).

Why? Because Starlink nailed satellite internet, and these MNOs assumed they’d do the same with direct-to-cell. It’s Elon Musk, after all!

But as we’ve seen, that confidence might be misplaced.

optus.com.au/about/media-ce…

reuters.com/business/media…

Why? Because Starlink nailed satellite internet, and these MNOs assumed they’d do the same with direct-to-cell. It’s Elon Musk, after all!

But as we’ve seen, that confidence might be misplaced.

optus.com.au/about/media-ce…

reuters.com/business/media…

In November 2023, SpaceX promised a constellation of 840 direct-to-cell satellites to be launched within 6 months.

Nearly a year later, they’ve launched fewer than 200.

Nearly a year later, they’ve launched fewer than 200.

https://x.com/kingtutcap/status/1831079838079414362

Starlink’s hastily launched satellites have caused significant radio interference, exceeding FCC limits (-120 dBW/m/MHz) as set in the Supplemental Coverage from Space (SCS) ruling.

This has triggered pushback from players like Echostar and Omnispace, as well as AT&T and Verizon, who filed complaints to the FCC. The interference could reduce network downlink throughput by 18%.

Starlink and $ASTS initially welcomed the SCS ruling—now Starlink is fighting it.

This has triggered pushback from players like Echostar and Omnispace, as well as AT&T and Verizon, who filed complaints to the FCC. The interference could reduce network downlink throughput by 18%.

Starlink and $ASTS initially welcomed the SCS ruling—now Starlink is fighting it.

https://x.com/kingtutcap/status/1827338630148342261

The pushback wasn't only from space or telco players but also the astronomy community due to its brightness and interference with radio bands protected for astronomy

https://x.com/kingtutcap/status/1820867477623935215

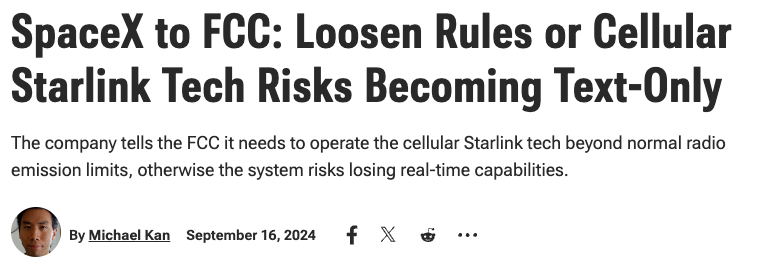

Starlink has filed multiple requests with the FCC to relax its regulations, claiming that the strict power limits would prevent them from delivering a fully functional service.

Starlink's strategy over the last 9 months was to launch as many satellites as possible in orbit and then claim that their service is for public benefit and will help first responders and people in danger so the FCC has to be less stringent and relax the rulings or else they're doing bad for the public and endangering lives.

"Hey we have over 200 satellites and the bad political FCC and telco dinosaurs like Verizon and AT&T aren't allowing us to use them. Stop stifling innovation :( "

So far, the FCC has stood its ground, but Starlink continues to argue for exceptions.

pcmag.com/news/fcc-to-sp…

extremetech.com/mobile/spacex-…

pcmag.com/news/spacex-to…

Starlink's strategy over the last 9 months was to launch as many satellites as possible in orbit and then claim that their service is for public benefit and will help first responders and people in danger so the FCC has to be less stringent and relax the rulings or else they're doing bad for the public and endangering lives.

"Hey we have over 200 satellites and the bad political FCC and telco dinosaurs like Verizon and AT&T aren't allowing us to use them. Stop stifling innovation :( "

So far, the FCC has stood its ground, but Starlink continues to argue for exceptions.

pcmag.com/news/fcc-to-sp…

extremetech.com/mobile/spacex-…

pcmag.com/news/spacex-to…

Starlink has shifted its messaging recently, claiming that its satellites are crucial for public safety and emergency services. They’re pushing the narrative that if the FCC doesn’t relax its rules, they’re endangering lives.

pcmag.com/news/elon-musk…

pcmag.com/news/elon-musk…

Ironically, $ASTS has been testing with first responders for years and has an "unofficial partnership" with the First Responders Public Authority and AT&T’s FirstNet—this relationship is much deeper than Starlink’s marketing pitch.

Video from FirstNet visit to AST:

Video from FirstNet visit to AST:

https://x.com/kingtutcap/status/1827404393081401537

In a recent filing to the FCC, Starlink argued that reducing satellite power to meet the regulations would decrease throughput by 20%, resulting in fewer users being able to access the service simultaneously. Real-time services like video calling, media sharing, and web browsing might not even be possible.

https://x.com/kingtutcap/status/1835076934251814913

But instead of addressing this, Starlink turned to Twitter to push the narrative that emergency alerts would be free for all, and other networks could use them if they wanted, using Elon Musk fanboys and their megaphones to do the job.

It’s an obvious play to sway public opinion and put pressure on the FCC.

It’s an obvious play to sway public opinion and put pressure on the FCC.

https://x.com/ajtourville/status/1828409898217914725

Interestingly, every milestone for Starlink’s direct-to-cell service has been communicated only via tweets from Starlink—no press releases from T-Mobile.

For example, on January 10, just 4 days after launching their first direct-to-cell satellites, Starlink tweeted about texts between two phones. Where was T-Mobile’s official announcement? Go and check T-Mobile's newsroom yourself.

For example, on January 10, just 4 days after launching their first direct-to-cell satellites, Starlink tweeted about texts between two phones. Where was T-Mobile’s official announcement? Go and check T-Mobile's newsroom yourself.

https://x.com/SpaceX/status/1745246204118925711

Look closely at the images of the text exchange Starlink posted in January, and you’ll notice serious lag in the order of sent/received messages.

Ironically, this tweet came just a week before Google joined $ASTS as an investor, alongside AT&T and Vodafone.

Coincidence of course :)

Ironically, this tweet came just a week before Google joined $ASTS as an investor, alongside AT&T and Vodafone.

Coincidence of course :)

https://x.com/kingtutcap/status/1818774451338854900

In May 2024, Starlink posted a video “claiming” to have achieved the first video call via their direct-to-cell network. The video was shot outside their office, and the connection was so pixelated and laggy you could barely see the other person.

No mention of speed, download rates, or any technical details—just a video on X. Where’s the T-Mobile press release celebrating this breakthrough? Nowhere to be found.

This milestone conveniently came exactly a week after $ASTS and AT&T announced a definitive commercial agreement.

Coincidence of course :)

No mention of speed, download rates, or any technical details—just a video on X. Where’s the T-Mobile press release celebrating this breakthrough? Nowhere to be found.

This milestone conveniently came exactly a week after $ASTS and AT&T announced a definitive commercial agreement.

Coincidence of course :)

https://x.com/kingtutcap/status/1831077438337814742

Every major milestone achieved by $ASTS has been announced with its MNO partners through official channels.

Whether it’s the April 2023 space-based voice call with Vodafone, Rakuten, and AT&T, the June 2023 4G connectivity in Hawaii (with download speeds of 10 Mbps), or the September 2023 5G broadband connection from Hawaii to Madrid, each of these milestones has been PR’d with quotes from senior leaders at AT&T, Vodafone, and Nokia.

These companies have way too much on the line to risk lying about their achievements.

April 2023:

June 2023:

September 2023:

Video from Rakuten:

Video from AST:

PR from Rakuten:

PR from Vodafone: feeds.issuerdirect.com/news-release.h…

feeds.issuerdirect.com/news-release.h…

feeds.issuerdirect.com/news-release.h…

corp.mobile.rakuten.co.jp/english/news/p…

vodafone.com/news/technolog…

Whether it’s the April 2023 space-based voice call with Vodafone, Rakuten, and AT&T, the June 2023 4G connectivity in Hawaii (with download speeds of 10 Mbps), or the September 2023 5G broadband connection from Hawaii to Madrid, each of these milestones has been PR’d with quotes from senior leaders at AT&T, Vodafone, and Nokia.

These companies have way too much on the line to risk lying about their achievements.

April 2023:

June 2023:

September 2023:

Video from Rakuten:

Video from AST:

PR from Rakuten:

PR from Vodafone: feeds.issuerdirect.com/news-release.h…

feeds.issuerdirect.com/news-release.h…

feeds.issuerdirect.com/news-release.h…

corp.mobile.rakuten.co.jp/english/news/p…

vodafone.com/news/technolog…

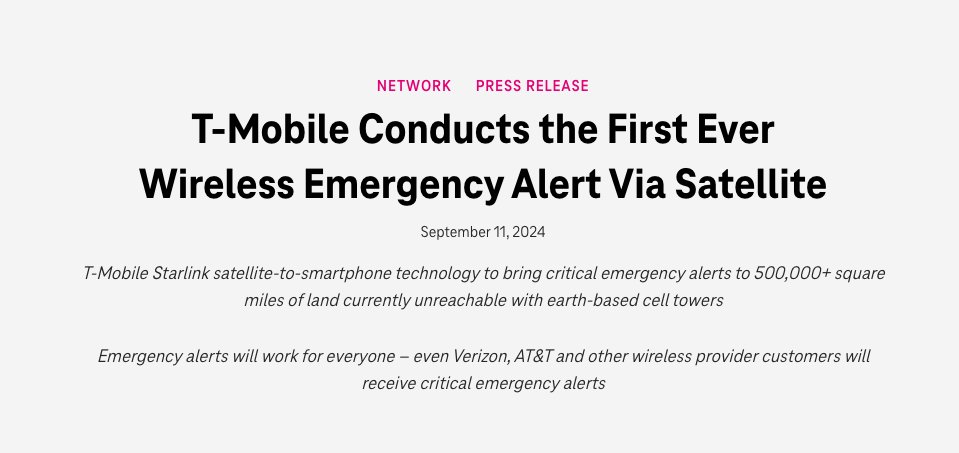

T-Mobile’s first press release acknowledging a technological milestone with Starlink didn’t come until September 11, 2023—more than a year after the partnership was announced. And what was the groundbreaking announcement? An emergency alert.

Yes, you read that right: not a text, not a call, but an emergency alert, similar to the Amber Alerts you get on your phone.

That’s the first technological “breakthrough” T-Mobile has celebrated with Starlink after 9 months of satellite launches.

t-mobile.com/news/network/t…

Yes, you read that right: not a text, not a call, but an emergency alert, similar to the Amber Alerts you get on your phone.

That’s the first technological “breakthrough” T-Mobile has celebrated with Starlink after 9 months of satellite launches.

t-mobile.com/news/network/t…

https://x.com/tmobilenews/status/1833888247342354800

Just a month ago, Elon Musk said that T-Mobile’s exclusivity with Starlink would last only one year. After all the promotion and marketing around the partnership, they’re only getting a one-year deal.

That’s a clear sign that the relationship between the two isn’t as solid as it seems.

That’s a clear sign that the relationship between the two isn’t as solid as it seems.

https://x.com/MarioNawfal/status/1829964590291304712

Additionally, last week T-Mobile hosted their Capital Markets Day. A full day of programming where they released their latest innovations and invited big institutional investors to talk about their future plans.

There where limited to no mention of their satellite to cell service, and haven't even called out Starlink by name.

So in a meeting with the biggest institutional investors on Wall Street, T-Mobile failed to mention more details about this service or even say the word Starlink.

There where limited to no mention of their satellite to cell service, and haven't even called out Starlink by name.

So in a meeting with the biggest institutional investors on Wall Street, T-Mobile failed to mention more details about this service or even say the word Starlink.

https://x.com/spacanpanman/status/1836487857508163906

Even more interesting, Starlink’s MNO partners in Australia (Optus) and New Zealand (One NZ) have recently updated their landing pages for the service.

Previously, they had set timelines for late 2024. Now, those timelines are open-ended, and both MNOs are “re-evaluating” their service timelines.

Thank you Wayback machine!

Previously, they had set timelines for late 2024. Now, those timelines are open-ended, and both MNOs are “re-evaluating” their service timelines.

Thank you Wayback machine!

https://x.com/kingtutcap/status/1837299662300029029

Even more telling, they’ve hinted that Starlink’s service may not work on all smartphones, contradicting Starlink’s original claim that the service would work on any unmodified phone.

https://x.com/kingtutcap/status/1837302782438617578

Optus went a step further, saying that even text messages could take longer to receive compared to 4G or 5G networks. Text messages! So if even basic text messaging won’t be smooth, it sounds like Starlink’s service will struggle to deliver.

On top of that, they mentioned that a clear line of sight to the sky would be required, meaning the service may not work indoors—another major limitation for a service that’s being hyped as revolutionary. It’s starting to sound like the offering will struggle to compete even in basic conditions.

On top of that, they mentioned that a clear line of sight to the sky would be required, meaning the service may not work indoors—another major limitation for a service that’s being hyped as revolutionary. It’s starting to sound like the offering will struggle to compete even in basic conditions.

https://x.com/kingtutcap/status/1837304088343535820

So where does that leave Starlink? Right now, their direct-to-cell service is more aligned with emergency alert systems like those from Skylo or Globalsat, which focus on SOS and low-bandwidth messaging.

Starlink so far hasn't proved they're able to compete in the direct-to-cell cellular broadband space, but rather is left competing in the patchy, emergency-alert space.

Starlink so far hasn't proved they're able to compete in the direct-to-cell cellular broadband space, but rather is left competing in the patchy, emergency-alert space.

The broader market still hasn’t fully realized AST’s potential. AST is frequently dismissed as a small "tiny" SpaceX rival, with many believing that Starlink will simply outspend and outmaneuver them.

However, AST’s multi-year head start, robust partnerships, and proven technological successes show they are far from being a simple underdog in this David vs. Goliath scenario.

However, AST’s multi-year head start, robust partnerships, and proven technological successes show they are far from being a simple underdog in this David vs. Goliath scenario.

There are three likely outcomes for Starlink’s FCC waiver request:

1. FCC Denies the Waiver – If the FCC holds its ground and denies Starlink’s waiver, Starlink will have to redesign its entire satellite strategy from scratch. This would cause massive delays and cast doubt over the MNOs’ trust in their timeline. Will it be worthwhile? Will SpaceX private investors want them to pour hundreds of millions of dollars on this again to get it right after they've messed up?

2. FCC Approves, AT&T & Verizon Sue – If the FCC grants Starlink’s waiver, expect a legal battle. AT&T and Verizon have invested billions in spectrum and won’t tolerate even 1% interference. Terrestrial networks are and will always remain king while direct-to-cell is complimentary or as it's named in the ruling Supplemental Coverage from Space. Supplemental. Meaning it comes second to terrrestrial and it's not even close. They control 70% of the wireless teclo market share in the US. They could sue Starlink and the FCC, sparking a costly legal war that might cripple Starlink’s progress.

3. Starlink Launches, But the Service is Clunky – Even if Starlink gets the waiver and avoids legal challenges, their service could still be subpar—laggy, clunky (as per the words of AT&T CEO John Stankey), unreliable, and vastly inferior to AST’s more refined technology. Ironically though, if the FCC relaxes the power limits for Starlink, that could benefit $ASTS as well, enabling them to push an even stronger service.

Also worth noting this comment from FCC Chairwomen Jessica Rosenworcel last week. The relationship between the FCC and Starlink is also questionable at this point.

1. FCC Denies the Waiver – If the FCC holds its ground and denies Starlink’s waiver, Starlink will have to redesign its entire satellite strategy from scratch. This would cause massive delays and cast doubt over the MNOs’ trust in their timeline. Will it be worthwhile? Will SpaceX private investors want them to pour hundreds of millions of dollars on this again to get it right after they've messed up?

2. FCC Approves, AT&T & Verizon Sue – If the FCC grants Starlink’s waiver, expect a legal battle. AT&T and Verizon have invested billions in spectrum and won’t tolerate even 1% interference. Terrestrial networks are and will always remain king while direct-to-cell is complimentary or as it's named in the ruling Supplemental Coverage from Space. Supplemental. Meaning it comes second to terrrestrial and it's not even close. They control 70% of the wireless teclo market share in the US. They could sue Starlink and the FCC, sparking a costly legal war that might cripple Starlink’s progress.

3. Starlink Launches, But the Service is Clunky – Even if Starlink gets the waiver and avoids legal challenges, their service could still be subpar—laggy, clunky (as per the words of AT&T CEO John Stankey), unreliable, and vastly inferior to AST’s more refined technology. Ironically though, if the FCC relaxes the power limits for Starlink, that could benefit $ASTS as well, enabling them to push an even stronger service.

Also worth noting this comment from FCC Chairwomen Jessica Rosenworcel last week. The relationship between the FCC and Starlink is also questionable at this point.

AST’s head start and technical prowess give them a huge advantage in the direct-to-cell market. Not only has AST already demonstrated real-world 4G and 5G capabilities, but their work with top MNOs like AT&T, Vodafone, and Rakuten also places them in a different league from Starlink.

It's now game on for $ASTS to execute.

Again, I stress that it's now game on for AST to execute flawlessly to capture that market leader position.

It's now game on for $ASTS to execute.

Again, I stress that it's now game on for AST to execute flawlessly to capture that market leader position.

https://x.com/kingtutcap/status/1835463206975820013

Even major financial institutions like Morgan Stanley and Ark Invest, as well as Starlink themselves, have acknowledged the value and potential of the direct-to-cell market.

The key here is that AST SpaceMobile has been building toward this moment for years, while Starlink is still scrambling to catch up.

The key here is that AST SpaceMobile has been building toward this moment for years, while Starlink is still scrambling to catch up.

https://x.com/spacanpanman/status/1817577557551726920

Eventually, the market will recognize $ASTS dominance in this space. As the technological gaps between Starlink and AST widen, and as more successful AST milestones are announced, there will be a significant rerate. $ASTS is poised for a breakthrough that many have yet to see coming, and when it does, the game will change.

https://x.com/kingtutcap/status/1835448163282702453

Disclaimer: This is not financial advice and is purely speculation by connecting the dots. There's a high chance I might be wrong but time will tell.

• • •

Missing some Tweet in this thread? You can try to

force a refresh