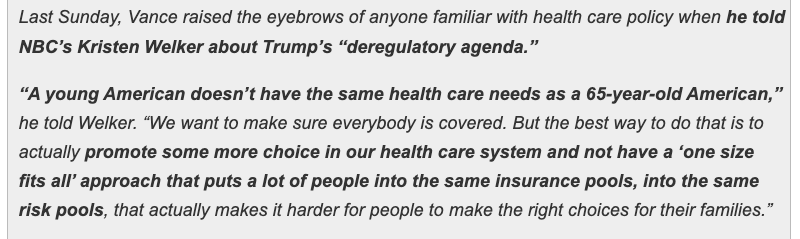

🧵📣 THE DEAD POOL: Since @JDVance wants to Concentrate folks w/pre-existing conditions into separate Camps, let's talk about it. 1/

acasignups.net/24/10/02/dead-…

acasignups.net/24/10/02/dead-…

Let's go back to the pre-ACA healthcare landscape. This is what it looked like in 2012...*before* the ACA's major provisions went into effect.

Half the US had employer coverage. Another third had Medicare or Medicaid. ~11M had "individual" insurance; ~48M had nothing at all. 2/

Half the US had employer coverage. Another third had Medicare or Medicaid. ~11M had "individual" insurance; ~48M had nothing at all. 2/

The ACA had 2 main goals:

1. Reduce the number of uninsured Americans as much as possible by making coverage more affordable & accessible;

2. Provide protections from insurance industry abuses, *especially* for the individual market where the abuses were the most blatant. 3/

1. Reduce the number of uninsured Americans as much as possible by making coverage more affordable & accessible;

2. Provide protections from insurance industry abuses, *especially* for the individual market where the abuses were the most blatant. 3/

Before the ACA, the indy market was the Wild West. Little regulation in most states, few national standards. Some of it was comprehensive but mostly it was a crapshoot...assuming you could get approved for coverage at all. 4/

There was a hodge-podge of indy market plans; "mini-meds," "short term plans," "farm bureau," "association," "sharing ministry," "indemnity" etc. These are still around in most states.

Some aren't even legally defined as "insurance." 5/

Some aren't even legally defined as "insurance." 5/

Even many of the so-called "Major Medical" plans sucked. This one capped maximum benefit claims at no more than $40,000. I'm not sure if that was per year or lifetime, but either way you were SOL if you were hit by any major medical expenses (or by a bus). 7/

Anyone who's ever given birth to a premature baby knows that neonatal care can cost up to $20,000/day, and if the infant requires complex surgeries it could break a million dollars.

Some newborn children wiped out their lifetime limits before they ever left the hospital. 8/

Some newborn children wiped out their lifetime limits before they ever left the hospital. 8/

Then again, many pre-ACA policies didn't cover maternity or neonatal care at all anyway.

Generally, prior to the ACA, individual market carriers could cherry pick who they'd allow to enroll, what they'd cover, and how much of the claims they felt like paying for, if any. 9/

Generally, prior to the ACA, individual market carriers could cherry pick who they'd allow to enroll, what they'd cover, and how much of the claims they felt like paying for, if any. 9/

That brings us to the main point of this thread: RISK POOLS.

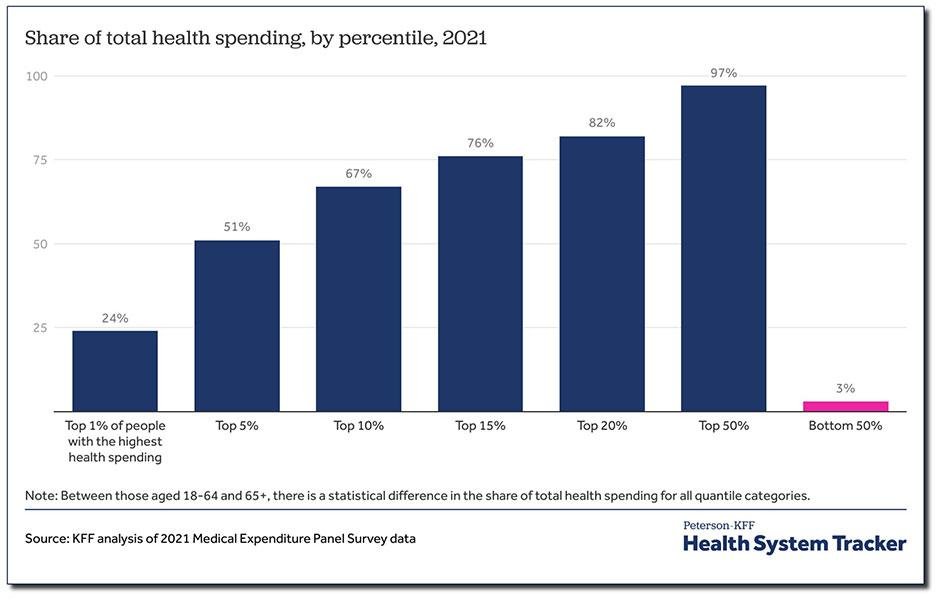

This is probably the single most important graph I want folks to keep in mind: The breakout of total U.S. healthcare spending broken out by highest to lowest utilization bracket. 10/

healthsystemtracker.org/chart-collecti…

This is probably the single most important graph I want folks to keep in mind: The breakout of total U.S. healthcare spending broken out by highest to lowest utilization bracket. 10/

healthsystemtracker.org/chart-collecti…

Generally, the unhealthiest 5% of the population eats up around 50% of total healthcare spending, and 10% of the population accounts for fully 2/3 of it.

In fact, half the population generates 97% of all healthcare spending. 11/

In fact, half the population generates 97% of all healthcare spending. 11/

In 2022, total U.S. healthcare spending from all sources (public & private; federal, state, local) came to $4.5 TRILLION. That's around $13.5K apiece overall on average. 12/

cms.gov/data-research/…

cms.gov/data-research/…

Let's boil down the entire U.S. population to just 100 people. At $13.5K apiece their total healthcare costs would come to $1.35 million. 13/

Half of them would be healthy as a horse. Some would just need some allergy shots. Some might sprain their wrist. Some might need minor surgery; a few would need major surgery, and a handful would require chemo, dialysis, and/or extremely expensive prescription drugs. 14/

Here's what it would look like taking the KFF graph & 2022 spending literally.

50 would cost $800 apiece

30 would cost $6,700 each, and so on.

One poor soul would rack up $324,000 in healthcare costs. 15/

50 would cost $800 apiece

30 would cost $6,700 each, and so on.

One poor soul would rack up $324,000 in healthcare costs. 15/

Now, let's say all 100 were uninsured. They're under 65 so don't qualify for Medicare; their income was too high to qualify for Medicaid; their employer didn't provide coverage; or they were self-employed. That meant they were at the mercy of the pre-ACA indy market. 16/

They'd call up a "non-group" insurance carrier...who would stop them right there and require pretty much their entire medical history.

X-rays, diagnoses, prescriptions, surgeries, hospital stays, lab tests...the works. And it was up to you to collect & provide that info. 17/

X-rays, diagnoses, prescriptions, surgeries, hospital stays, lab tests...the works. And it was up to you to collect & provide that info. 17/

Then, an actuary would go over all your personal medical data and decide whether to give you a 👍 or👎.

If it was 👎, you'd be SOL. You could try a 2nd carrier, or a 3rd, but in some cases you were deemed "uninsurable at any price." 18/

If it was 👎, you'd be SOL. You could try a 2nd carrier, or a 3rd, but in some cases you were deemed "uninsurable at any price." 18/

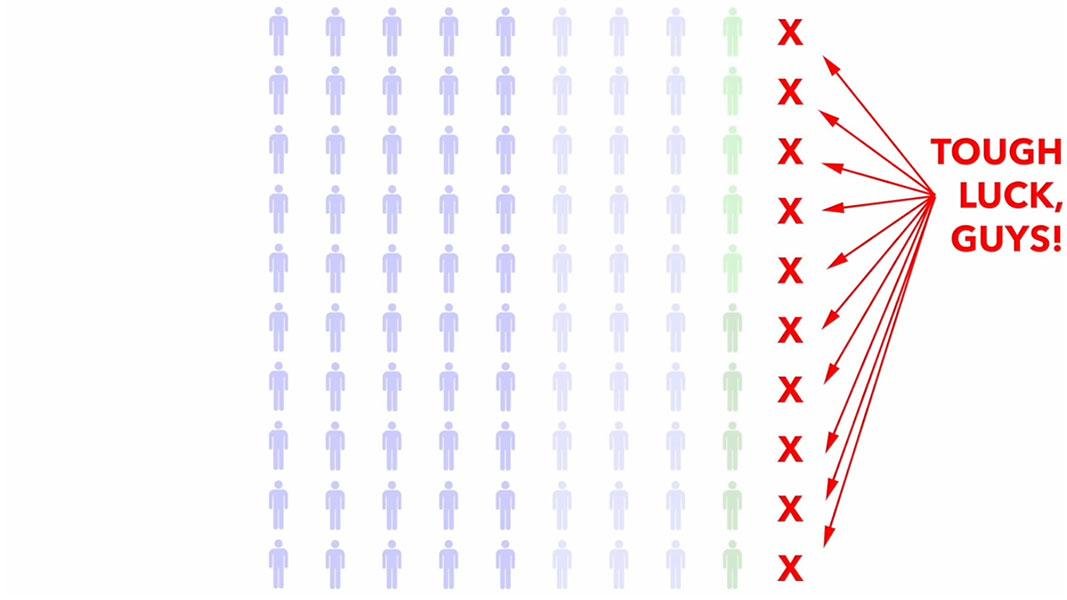

Essentially, the insurance carriers were trying to weed out the, say, 10% of the population which eats up 2/3 of all healthcare spending. This is called "Medical Underwriting."

Cut those 10 out and the other 90 go from $13.5K apiece to just $4,500 each. 19/

Cut those 10 out and the other 90 go from $13.5K apiece to just $4,500 each. 19/

This is the main reason why pre-ACA indy market plans had such low premiums...for those deemed healthy enough to be allowed to enroll in the first place.

But what about the others who were effectively blacklisted by the industry for having "Pre-Existing Conditions?" 20/

But what about the others who were effectively blacklisted by the industry for having "Pre-Existing Conditions?" 20/

So what is a "Pre-Existing Condition?"

Yes, it included obvious red flags like cancer, diabetes, AIDS/HIV, Parkinson's, etc... 21/

kff.org/affordable-car…

Yes, it included obvious red flags like cancer, diabetes, AIDS/HIV, Parkinson's, etc... 21/

kff.org/affordable-car…

...but it also included conditions like...

Acne.

"Back problems."

High cholestrol.

And if you've ever tested positive for COVID (ie, nearly everyone at this point), guess what?

Basically, the short answer is...whatever the fuck the insurance industry decided it included. 22/

Acne.

"Back problems."

High cholestrol.

And if you've ever tested positive for COVID (ie, nearly everyone at this point), guess what?

Basically, the short answer is...whatever the fuck the insurance industry decided it included. 22/

But Wait, There's More!

There was a long list of occupations which would get you denied coverage. Air traffic controllers. Meat packers. Scuba divers. Taxi drivers (which probably would include Lyft/Uber these days). 23/

There was a long list of occupations which would get you denied coverage. Air traffic controllers. Meat packers. Scuba divers. Taxi drivers (which probably would include Lyft/Uber these days). 23/

Sometimes the they'd provide coverage to these folks...at several times the price. Or they might add an exception so it wouldn't cover the very treatment the enrollee was most in need of. Or they wouldn't cover maternity care, prescription drugs or mental health at all. 24/

Now, on paper, a healthy person in a low-risk job might look at this and say "sucks to be them, but that works for me!" since their premiums would be cut by 2/3!

Except for one thing...sooner or later they're gonna be in that 10% as well. 25/

Except for one thing...sooner or later they're gonna be in that 10% as well. 25/

Healthy people get pregnant.

Healthy people get diabetes.

Healthy people get hit by cars.

Healthy people get cancer.

On a long enough timeline, everyone develops a "pre-existing condition." 26/

Healthy people get diabetes.

Healthy people get hit by cars.

Healthy people get cancer.

On a long enough timeline, everyone develops a "pre-existing condition." 26/

Now, there were some "options" for those denied coverage by legit insurance carriers...but many ranged from practically useless "junk plans" to literal fraudulent scam outfits.

Again, many weren't even legally defined as "insurance" and are thus completely unregulated. 27/

Again, many weren't even legally defined as "insurance" and are thus completely unregulated. 27/

I almost forgot about one of the nastiest things that even legitimate insurance carriers used to do: rescission.

This was when a carrier would retroactively cancel your policy & refuse to pay claims over some minor/nominal paperwork error/omission. 28/

publicintegrity.org/health/in-a-co…

This was when a carrier would retroactively cancel your policy & refuse to pay claims over some minor/nominal paperwork error/omission. 28/

publicintegrity.org/health/in-a-co…

In response to all of this, the ACA mandated the following:

1. Guaranteed Issue: Carriers have to sell to anyone regardless of medical/health condition or history.

2. Community rating: They can't charge people more based on medical condition/history, gender, occupation, etc.

1. Guaranteed Issue: Carriers have to sell to anyone regardless of medical/health condition or history.

2. Community rating: They can't charge people more based on medical condition/history, gender, occupation, etc.

3. Essential Health Benefits (EHBs): Policies have to cover, at a minimum, stuff like ER care, hospitalization, outpatient services, naternity/newborn care, mental health, prescription drugs, rehab, lab services & pediatric care. 30/

4. Minimum Actuarial Value (AV): ACA plans have to cover a min. % of healthcare expenses (in aggregate), ranging from 60 - 90% depending on the "metal level" (Bronze, Silver, Gold, Platinum).

Bronze = low premium, high deductible

Platinum = high premium, low deductible 31/

Bronze = low premium, high deductible

Platinum = high premium, low deductible 31/

5. No more annual or lifetime benefit limits.

6. Maximum Out of Pocket Ceiling: To avoid a catastrophic incident bankrupting a family, there's a maximum annual cap on total out of pocket costs to the enrollee (ie, deductible + copays + coinsurance) for in-network care.

6. Maximum Out of Pocket Ceiling: To avoid a catastrophic incident bankrupting a family, there's a maximum annual cap on total out of pocket costs to the enrollee (ie, deductible + copays + coinsurance) for in-network care.

7. No-Cost Preventative Services: The carriers have to cover a list of stuff like annual physicals, mammograms, blood screenings, colonscopies etc. at no out of pocket cost to the enrollee if done in network.

This also includes vaccinations (ie, flu shots, COVID shots etc). 33/

This also includes vaccinations (ie, flu shots, COVID shots etc). 33/

8. Stay on Parents Plan until 26: This actually has nothing to do with the problems upthread, but it's a very popular provision which most states actually already had a version of pre-ACA: Carriers have to allow young adults to remain on their parents policy up until age 26. 34/

When you add all of this stuff up, you get a One Legged Stool.

(again, I forgot to include the making rescission illegal...carriers can now only cancel a policy retroactively if they can prove intentional fraud as opposed to someone accidentally forgetting to check a box) 35/

(again, I forgot to include the making rescission illegal...carriers can now only cancel a policy retroactively if they can prove intentional fraud as opposed to someone accidentally forgetting to check a box) 35/

Now, both NY and WA tried versions of the "One Legged Stool" in the 90's...but both ended in failure for two reasons:

1. Forcing insurance carriers to actually cover sick people really does increase costs (shocking!)..but WA/NY didn't include financial help for enrollees. 36/

1. Forcing insurance carriers to actually cover sick people really does increase costs (shocking!)..but WA/NY didn't include financial help for enrollees. 36/

2. If you let anyone sign up at any time, some people will game the system by waiting until they get sick/injured before signing up.

That's like waiting until you get in a car crash to buy auto insurance or waiting until your house is on fire to buy homeowner's insurance. 37/

That's like waiting until you get in a car crash to buy auto insurance or waiting until your house is on fire to buy homeowner's insurance. 37/

This is why you can't drive a car or get a mortgage without proof of insurance first.

In response to both of these problems, the ACA was designed using the Massachusetts model: The Three-Legged Stool: 38/

In response to both of these problems, the ACA was designed using the Massachusetts model: The Three-Legged Stool: 38/

The Blue Leg includes all the stuff I mentioned above.

The Green Leg is the Carrots: Financial subsidies to cut down on both Premiums and Cost Sharing (deductibles, co-pays, coinsurance), as well as the Insurance Marketplaces/Exchanges & Price Gouging Protection (MLR rule). 39/

The Green Leg is the Carrots: Financial subsidies to cut down on both Premiums and Cost Sharing (deductibles, co-pays, coinsurance), as well as the Insurance Marketplaces/Exchanges & Price Gouging Protection (MLR rule). 39/

The Red Leg is the Sticks.

Originally this consisted of 2 provisions: A limited-time open enrollment period...and the much-derided Individual Mandate Penalty.

I'll talk about that a bit more downthread, and it's not a pretty discussion. 40/

Originally this consisted of 2 provisions: A limited-time open enrollment period...and the much-derided Individual Mandate Penalty.

I'll talk about that a bit more downthread, and it's not a pretty discussion. 40/

Now, this model has mostly worked out, but there were some definite gaps:

--The subsidies weren't generous enough, and cut off entirely for households earning more than 4x the poverty level.

This was solved by the Inflation Reduction Act...but only thru the end of 2025. 41/

--The subsidies weren't generous enough, and cut off entirely for households earning more than 4x the poverty level.

This was solved by the Inflation Reduction Act...but only thru the end of 2025. 41/

--The Max Out of Pocket (MOOP) cap is fine for a once-in-a-lifetime catastrophic expense, but is still a problem for those w/chronic high-expense conditions (imagine getting hit by a bus ever year for decades). The Network Adequacy rules need to be strengthened, and so on. 42/

There have also been several major changes to the law over the years.

One of the most notable was in 2017, when Donald Trump and his GOP-controlled Congress spent the entire year trying to repeal the entire ACA, "root & branch" as McConnell put it. 43/

One of the most notable was in 2017, when Donald Trump and his GOP-controlled Congress spent the entire year trying to repeal the entire ACA, "root & branch" as McConnell put it. 43/

In the end, they failed--just barely--thanks to 46 Democratic Senators, 2 Dem-aligned independents, 2 women Republican Senators, and John McCain's Thumb.

HOWEVER, they were able to eliminate one ACA provision via legislation: The Individual Mandate Penalty. 44/

HOWEVER, they were able to eliminate one ACA provision via legislation: The Individual Mandate Penalty. 44/

Now, technically speaking, the Mandate Penalty still exists...it's just that it was reduced from $695/person (or 2.5% of household income) down to...$0, or 0.0% of your income.

It's been that way since 2019. 45/

It's been that way since 2019. 45/

What happened when the federal penalty for not having ACA-compliant coverage was changed to $0?

Well, carriers raised full-price premiums by an average of around 8% in 2019 to mitigate their estimate of the cost of people dropping coverage. 46/

nytimes.com/2018/12/27/opi…

Well, carriers raised full-price premiums by an average of around 8% in 2019 to mitigate their estimate of the cost of people dropping coverage. 46/

nytimes.com/2018/12/27/opi…

Now, here's where things get very messy: Enrollment did indeed drop in 2019 and again in 2020.

On the other hand, the 8% avg. rate hike due to the mandate being zeroed out wasn't as much as some had predicted. 47/

On the other hand, the 8% avg. rate hike due to the mandate being zeroed out wasn't as much as some had predicted. 47/

On the other hand, 4 states + DC reinstated their own individual mandate penalty.

On the other other hand, there were also a dozen other major factors which contributed to premium hikes...and then COVID hit the country in early 2020 which disrupted everything. 48/

On the other other hand, there were also a dozen other major factors which contributed to premium hikes...and then COVID hit the country in early 2020 which disrupted everything. 48/

The other thing about the "mandate penalty" is that it being effective relies on people knowing it existed...and it being eliminated only had an impact if people knew it DIDN'T exist any longer. 49/

It was zeroed out in December 2017...but was still in effect until January 2019...and even then, most people didn't know they hadn't been charged a penalty until they filed their federal income taxes in spring of 2020.

Gee, anything big going on in March/April 2020? 50/

Gee, anything big going on in March/April 2020? 50/

Here's the punchline of the federal Mandate Penalty being zeroed out:

That 8% rate hike? That wasn't just in 2019; it's been baked into the mix every year since.

Except since most ACA enrollees are subsidized, most of the cost of it is being absorbed by...taxpayers. 51/

That 8% rate hike? That wasn't just in 2019; it's been baked into the mix every year since.

Except since most ACA enrollees are subsidized, most of the cost of it is being absorbed by...taxpayers. 51/

That's right: By zeroing out the mandate penalty, Donald Trump & the GOP Congress of 2017 caused federal spending to increase by a good $5 - $6 billion per year via higher financial subsidies (which they now decry).

I call it the World's Most Expensive Shim®. 52/

I call it the World's Most Expensive Shim®. 52/

Having said that, no, the federal mandate penalty won't be returning, even under a Democratic trifecta.

It was simply too controversial and too poorly understood. Eliminating it increased the cost of the ACA but also removed the biggest gripe people had about the law. 53/

It was simply too controversial and too poorly understood. Eliminating it increased the cost of the ACA but also removed the biggest gripe people had about the law. 53/

Another major change came in 2021 under the Biden Administration, when Democrats finally fixed the subsidy cliff problem via the ARPA (and later the IRA).

In short, the original ACA subsidies were too stingy for those who received them and cut off entirely at 400% FPL. 54/

In short, the original ACA subsidies were too stingy for those who received them and cut off entirely at 400% FPL. 54/

Here's an the problem & solution for a family of 4 living in Henrico County, Virginia at various income levels.

At 401% FPL ($106K/yr at the time), they'd go from paying 9.8% of their income in premiums to over 18.5%.

W/the upgraded subsidies, they only pay 8.5% at most. 55/

At 401% FPL ($106K/yr at the time), they'd go from paying 9.8% of their income in premiums to over 18.5%.

W/the upgraded subsidies, they only pay 8.5% at most. 55/

The end result of all this is that thanks to the ACA, the uninsured population of the U.S. has dropped from 48 million in 2012 to around 26 million today, even as our pop has grown by over 22 million people.

Meanwhile, you don't have to worry about being denied enrollment. 56/

Meanwhile, you don't have to worry about being denied enrollment. 56/

THIS FINALLY BRINGS US TO JD VANCE'S PROPOSAL: RETURNING TO "HIGH RISK POOLS."

57/

57/

Under JD Vance's (ie, Trump's) proposal, we'd go completely the opposite direction:

Separate out the, say, 10% sickest and put them into a "High Risk Pool." Quarrantine them, if you will.

In theory, this would reduce the cost for the other 90% by 2/3, right? 58/

Separate out the, say, 10% sickest and put them into a "High Risk Pool." Quarrantine them, if you will.

In theory, this would reduce the cost for the other 90% by 2/3, right? 58/

Well, problem #1 is that in & of itself, this doesn't do anything to reduce the cost of healthcare.

The total cost is still $1.35M, just chopped into two chunks. It's just a question of where the money comes from...the feds, the states, the carriers or the enrollees. 59/

The total cost is still $1.35M, just chopped into two chunks. It's just a question of where the money comes from...the feds, the states, the carriers or the enrollees. 59/

Let's say you have 24M people (the size of the current ACA indy market in 2024) @ $13.5K/yr. Move the 10% sickest into a HRP @ $90K/ea.

Premiums for the other 21.6M = $4.5K/yr

Charge the HRP folks a similar $4.5K/yr

That leaves an $85.5K/ea HRP tab for the gov't to pick up. 60/

Premiums for the other 21.6M = $4.5K/yr

Charge the HRP folks a similar $4.5K/yr

That leaves an $85.5K/ea HRP tab for the gov't to pick up. 60/

$85.5K x 2.4M HRP enrollees = $205 billion per year.

Guess how much the current ACA subsidies for over 19 million people including the upgraded subsidies of the IRA will total? Around $125 billion.

Would JD Vance really nearly double ACA subsidies? I mean, OK, but... 61/

Guess how much the current ACA subsidies for over 19 million people including the upgraded subsidies of the IRA will total? Around $125 billion.

Would JD Vance really nearly double ACA subsidies? I mean, OK, but... 61/

FWIW, back in 2017, then-House Speaker Paul Ryan proposed a federal High Risk Pool as part of his Repeal/Replace plan.

You know how much funding he was proposing?

$25 billion. Over 10 years.

Even adjusted for inflation that'd still only be $3.2 billion/year. 62/

You know how much funding he was proposing?

$25 billion. Over 10 years.

Even adjusted for inflation that'd still only be $3.2 billion/year. 62/

How about throwing it back to the states, as Republicans are so fond of doing?

Yeah, about that...here's what the state HRPs looked like prior to the ACA:

kff.org/affordable-car…

Yeah, about that...here's what the state HRPs looked like prior to the ACA:

kff.org/affordable-car…

Even the HRPs designed specifically for those with pre-existing conditions...denied those w/pre-existing conditions for up to a year.

They also included annual/lifetime limits, sometimes didn't cover prescription drugs, etc.

And some simply cut off enrollment entirely. 64/

They also included annual/lifetime limits, sometimes didn't cover prescription drugs, etc.

And some simply cut off enrollment entirely. 64/

Oh yeah...also, how are you supposed to separate out the HRP folks from everyone else? Well, you'd have to bring back...indivdual medical underwriting.

Ie, making you provide your entire medical history again...to both the private carriers and the federal government. 65/

Ie, making you provide your entire medical history again...to both the private carriers and the federal government. 65/

Do you really want a Trump/Vance administration to know your entire medical history including the most personal & intimate details of your healthcare situation?

I mean, JD Vance seems to...at least when it comes to womens menstrual cycles, anyway.

talkingpointsmemo.com/edblog/jd-vanc…

I mean, JD Vance seems to...at least when it comes to womens menstrual cycles, anyway.

talkingpointsmemo.com/edblog/jd-vanc…

Anyway, if you made it this far and want to support my work at ACASignups, you can do so here, thanks!

L'shanah Tovah!

paypal.com/donate?hosted_…

L'shanah Tovah!

paypal.com/donate?hosted_…

• • •

Missing some Tweet in this thread? You can try to

force a refresh