You still probably don't know what happened

The Fed cut rates by 0.5%, then the $TLT and other bonds like $IEF $SHY saw their yields go UP by over 0.5%

This divergence against the $SPY $SPX, especially to $IWM can't be good

Here's how to play this

A 🧵☕️

The Fed cut rates by 0.5%, then the $TLT and other bonds like $IEF $SHY saw their yields go UP by over 0.5%

This divergence against the $SPY $SPX, especially to $IWM can't be good

Here's how to play this

A 🧵☕️

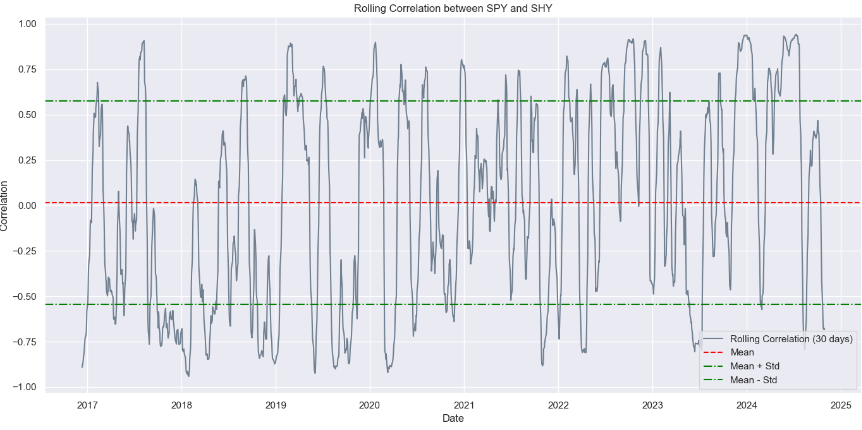

1. Typically, bond prices and stock prices are positively correlated

You can see the below rolling correlation between the $SPY and $SHY, which has been at 75% historically

Correlations breaking down on a long-term basis typically precede a stock market selloff on fundamentals

You can see the below rolling correlation between the $SPY and $SHY, which has been at 75% historically

Correlations breaking down on a long-term basis typically precede a stock market selloff on fundamentals

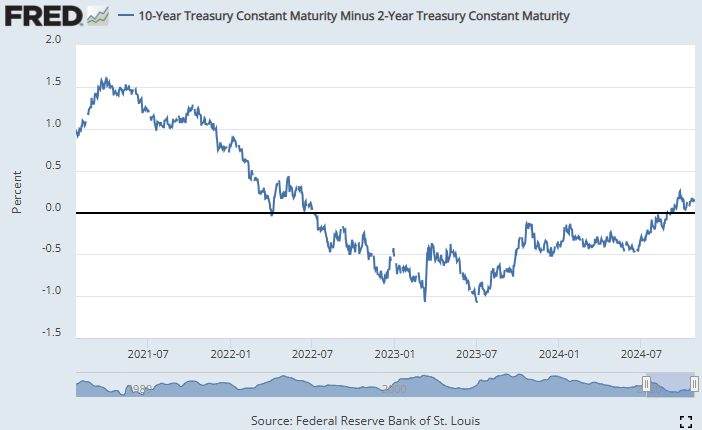

2. But, it's not going to be just one set of bonds, like the $SHY, to consider against the $SPY $SPX

You have to look at the yield curve itself, which considers long-term bonds like $IEF or $TLT against short term bonds

This is a great economic cycle gauge, here it is:

You have to look at the yield curve itself, which considers long-term bonds like $IEF or $TLT against short term bonds

This is a great economic cycle gauge, here it is:

3. Whenever the yield curve comes down, you can be sure that some sort of liquidity boost / money printing will take place

This is the leveraging cycle of an economy, as we saw since the days of COVID-19

Now, the opposite is happening as the curve steepens...

This is the leveraging cycle of an economy, as we saw since the days of COVID-19

Now, the opposite is happening as the curve steepens...

4. But, what does it mean really?

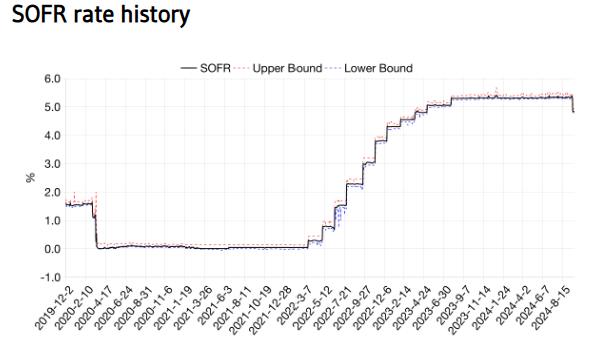

First of all, it means money is being taken out of the market, you can see banks reacting to this by raising SOFR rates and tightening money flows

Even through a cut cycle, liquidity can dry up very quickly such as right now

What can you do?

First of all, it means money is being taken out of the market, you can see banks reacting to this by raising SOFR rates and tightening money flows

Even through a cut cycle, liquidity can dry up very quickly such as right now

What can you do?

5. It means you can place a bet on the yield curve steepening, which can pay you for at least 12 months on a relatively stress-free basis

How?

Steepening = 10-year yields rising faster than 2-year yields

So, buy 2-years in $SHY ETF, short 10-years in $IEF ETF

Boom ☕️

How?

Steepening = 10-year yields rising faster than 2-year yields

So, buy 2-years in $SHY ETF, short 10-years in $IEF ETF

Boom ☕️

6. What about stocks?

Most people are betting against the $SPY $SPX, which absolutely makes sense

But

I think if inflation does hit us in the head, it'll be the $IWM that will see the worst of it

Small-caps have pure domestic exposure, so they can't manage costs as easy 📉

Most people are betting against the $SPY $SPX, which absolutely makes sense

But

I think if inflation does hit us in the head, it'll be the $IWM that will see the worst of it

Small-caps have pure domestic exposure, so they can't manage costs as easy 📉

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh