‼️ Russian Railway October Loading Update Thread

It got worse EVEN Worse

Let me explain….

(Note: Loading is in Millions of Tons, and please read the thread before you ask why the chart looks the way it does)

It got worse EVEN Worse

Let me explain….

(Note: Loading is in Millions of Tons, and please read the thread before you ask why the chart looks the way it does)

https://twitter.com/prune602/status/1841192822692520191

I’ve been having issues with threads posting correctly recently, so I’m just going to have to do this one post at a time.

So, it’s not over until I say it’s over.

So, it’s not over until I say it’s over.

This is the 4th thread of this type. If you follow to quote tweet at the top you can go back to the beginning and read about how these were made and I give a good description in the first thread about how any why I made the top graph the way I did.

It is a rolling daily average

It is a rolling daily average

I do recommend you read the previous threads. They aren’t that long (comparatively speaking) and if you are familiar, I think that last months thread will be helpful to review because I pointed out some things we needed to watch.

I want you to keep in mind that this October has 31 days in it, while September only had 31.

We’ll need to remember that when looking at the data. You need to account for the extra day.

In addition there is seasonality to some cargo.

Prepare yourself for a lot of charts!

We’ll need to remember that when looking at the data. You need to account for the extra day.

In addition there is seasonality to some cargo.

Prepare yourself for a lot of charts!

Here is the total loading data. If you look at the YTD data, you can see that things remain MUCH lower than usual.

On a per month basis, September loading was 94.5 million tons while October is 96.9 million tons

This may lead you to believe that things have improved.

Nope.

On a per month basis, September loading was 94.5 million tons while October is 96.9 million tons

This may lead you to believe that things have improved.

Nope.

You have to account for the extra day.

Here, I took the Loading Data (Per Month) for September, divided it by 30 to get a “per day” loading rate, then multiplied by 31 to give a projected value of Loading for October if remained the same.

Projected

👉97.7

Actual

👉96.9

WORSE

Here, I took the Loading Data (Per Month) for September, divided it by 30 to get a “per day” loading rate, then multiplied by 31 to give a projected value of Loading for October if remained the same.

Projected

👉97.7

Actual

👉96.9

WORSE

It is also worth AGAIN pointing out that some of these segments are impacted by seasonality.

Which is why this graph is so beneficial. It accounts for the variation in days of the month, the additional day added by leap year AND seasonality.

And overall THINGS ARE MUCH worse.

And overall THINGS ARE MUCH worse.

Now some of you may be going back and taking a look at January’s data again. Why is it so low, and why did I say LAST month was the worst if January has 31 Days.

Well…

Well…

January is when Russia takes its biggest holiday. Here is the proposed 2025 calendar of days off for reference.

Russian Orthodox Christmas is celebrated in JANUARY not December, and New Year’s kicks off their holiday season.

This is why January always starts low.

Russian Orthodox Christmas is celebrated in JANUARY not December, and New Year’s kicks off their holiday season.

This is why January always starts low.

https://twitter.com/prune602/status/1816577106064941284

What we’re looking at now is record low loading in one of the months that USUALLY had some of the HIGHEST loading of the year.

Look at 2019. March had the highest loading, but second place went to October.

October 2019 👉 109.5 Million Tons

October 2024 👉 96.9 Million Tons

Look at 2019. March had the highest loading, but second place went to October.

October 2019 👉 109.5 Million Tons

October 2024 👉 96.9 Million Tons

I’ve got a lot of tables to show you, but when you’re looking remember about the extra day in October and also seasonality.

Here we go!

Here we go!

Here is Coal & Coke.

Coal is actually down in comparison to September when you look at it on a per day loading basis. This is notable because Coal loading usually increases in October even when looking at the per day loading.

Not this year.

Coal is actually down in comparison to September when you look at it on a per day loading basis. This is notable because Coal loading usually increases in October even when looking at the per day loading.

Not this year.

This is an important topic as the Russia Coal industry has been in significant trouble this year.

I went into a lot of detail in this thread (worth reading if you haven’t already) and since then, things have not improved.

I went into a lot of detail in this thread (worth reading if you haven’t already) and since then, things have not improved.

https://twitter.com/prune602/status/1843460379122569598

In this thread I discussed how Russian Railways was looking to reduce coal shipments in favor of more profitable cargo.

Definitely read this thread

Definitely read this thread

https://twitter.com/prune602/status/1848387130545840276

But notably, the coal producers are asking for MORE shipping capacity, not less.

So although coal is having trouble financially now, that isn’t what is reducing loading. It’s Russian Railways!

So although coal is having trouble financially now, that isn’t what is reducing loading. It’s Russian Railways!

https://twitter.com/prune602/status/1848387197000417773

That means that the option of making up low margins by increasing output isn’t available to Russian Coal. In fact, output is limited because Russian Railways can’t provide the desired quantities of shipping capacity.

Here is the October 2024 YTD mix of loading (remember, it’s measured by tons)

As you can see, Coal is still the largest segment by far. This is why Coal and the Railways in Russia are so heavily connected.

As you can see, Coal is still the largest segment by far. This is why Coal and the Railways in Russia are so heavily connected.

Here is Oil & Oil products

This is a handy metric, since Russia has been classifying statistical data related to this segment.

This is a handy metric, since Russia has been classifying statistical data related to this segment.

Iron & Manganese Ore

Ferrous Metals

Ferrous Scrap Metal

Ferrous Metals

Ferrous Scrap Metal

Chemical & Mineral Fertilizers

This is one of the few segments that has been doing well (relatively speaking)

Note: This does not mean that the prices have gotten cheaper for farmers in Russia.

This is one of the few segments that has been doing well (relatively speaking)

Note: This does not mean that the prices have gotten cheaper for farmers in Russia.

Cement

Timber

Grain

It’s been a bad year for Russian Agriculture

It’s been a bad year for Russian Agriculture

Construction Cargo

Non-ferrous Ore & Sulfur Raw Materials

Chemicals & Soda

Industrial Materials & Molding Materials

Industrial Materials & Molding Materials

Others, including Containerized Cargo

(Note: They didn’t specify these in the reports I have until the end of 2020, that’s why it’s blank)

(Note: They didn’t specify these in the reports I have until the end of 2020, that’s why it’s blank)

And here’s a giant spreadsheet!

Hopefully you read last month’s thread.

Currently, I still assess that the thing that is driving reduced railway loading is Russian Railways NOT the Economy (although that could change in the future)

Currently, I still assess that the thing that is driving reduced railway loading is Russian Railways NOT the Economy (although that could change in the future)

One of the main drivers for this reduced Railway Loading is still likely to be the reduced Locomotive availability.

This stems from an aging & poorly maintained fleet of locomotives.

This stems from an aging & poorly maintained fleet of locomotives.

One of the drivers for this is when Russian Railways, A MONOPOLY, eliminated their entire maintenance department.

I guess the thought there would be cost savings. This happened YEARS ago, they started in 2013. They also got rid of the experienced staff.

I guess the thought there would be cost savings. This happened YEARS ago, they started in 2013. They also got rid of the experienced staff.

https://twitter.com/prune602/status/1768496315397227000

They figured out it was bad, but they didn’t fix it.

As a result of this, Russian Railways has never been able to properly maintain its fleet (no matter the age) of Locomotives.

Which is bad.

As a result of this, Russian Railways has never been able to properly maintain its fleet (no matter the age) of Locomotives.

Which is bad.

https://twitter.com/prune602/status/1768502654584426854

I do recommend you read through this thread for an idea of how they got to where they are now. It’s been years in the making, sanctions made things worse.

https://twitter.com/prune602/status/1780998055187111970

They have put off replacing locomotives so long that it’s likely that it would be impossible for anyone build new ones at the rate that old ones stop working. And you’ve basically got a bottle neck in the maintenance shops.

The labor shortages are hitting everyone. Russian Railways itself already reported that it was not offering competitive wages.

With other businesses offering 50-70% higher wages, it seems bonkers that they’re debating CUTTING the pay raises in order to keep prices low.

With other businesses offering 50-70% higher wages, it seems bonkers that they’re debating CUTTING the pay raises in order to keep prices low.

https://twitter.com/prune602/status/1839074374315630975

But considering the other decisions Russian Railways has made in the past, maybe not THAT surprising.

The labor shortage is only worsening Locomotive availability.

In addition, things like, traffic jams due to insufficient infrastructure in the east cause problems.

The labor shortage is only worsening Locomotive availability.

In addition, things like, traffic jams due to insufficient infrastructure in the east cause problems.

Russian Railways appears to have issues related to dispatch of locomotives as well, and changes to the flow of things causes chaos. This includes things like adding or removing gasoline export bans, Ukraine striking refineries, etc.

Considering the Russian Railways appears to still be operating at maximum capacity (even though it’s shrinking) even small things will add up to make the situation worse

- Derailments

- Partisan Attacks

- Weather

Will all lower Russian Railways loading…for now.

- Derailments

- Partisan Attacks

- Weather

Will all lower Russian Railways loading…for now.

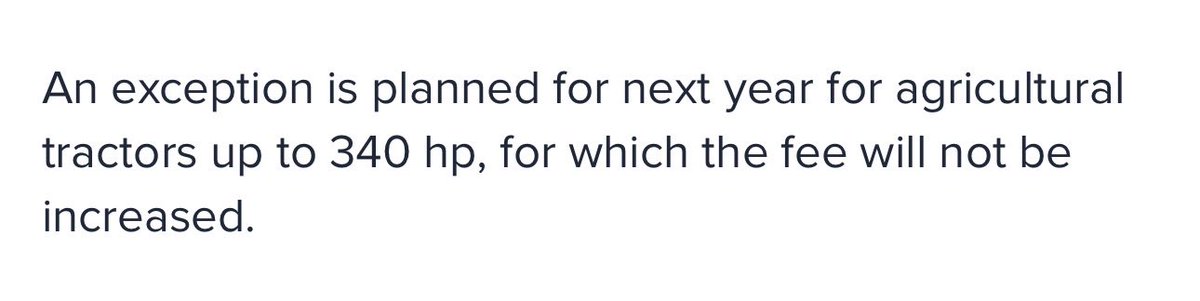

Cement and Construction Cargo have not yet had the significant drop in shipping that may come as a result of the increased cost of lending, government spending cuts, and reductions in mortgage subsidies.

The new key rate of 21% with the Russian Central Banks warning that it could go higher in December and that there is no limit on how high the Key Rate could go is going to be challenging from the Russian Economy moving forward.

https://twitter.com/prune602/status/1849913258410492278

This thread on Freight Car Maintenance supported some of things I warned about in last month’s thread.

https://twitter.com/prune602/status/1850709359572992089

Like this part.

https://twitter.com/prune602/status/1850709445484978309

Railway Loading Capacity continues to shrink because problems with Russian Railways. It’s currently doing everything it can, and there is no excess capacity not being utilized.

But that doesn’t mean that the economy couldn’t take a significant dive.

But that doesn’t mean that the economy couldn’t take a significant dive.

As I currently do not see any signs that the issues leading to the Railway Loading decrease improving, that means that if there suddenly IS available Railway Loading capacity…things have gotten much MUCH worse in Russia.

It would mean the economy is taking a dive.

It would mean the economy is taking a dive.

A Dive so big that surpasses the currently level at which Russian Railways is currently shrinking.

Let’s set that economy aside again, and focus on just Russian railways performance. Does this mean that Russian Railways will collapse tomorrow?

No, but…

No, but…

I do want to remind you of my beloved bathtub curve.

These things can compound. That’s why large corporations often stagger purchases of new equipment so this line can be flattened overall. (Russian Railways didn’t do that, or maintain their equipment)

en.wikipedia.org/wiki/Bathtub_c…

These things can compound. That’s why large corporations often stagger purchases of new equipment so this line can be flattened overall. (Russian Railways didn’t do that, or maintain their equipment)

en.wikipedia.org/wiki/Bathtub_c…

On this spreadsheet in the column on the right labeled “Diff” i took the YTD loading from 2023 and subtracted the YTD loading for 2024.

And here I graphed it. Now go back and look that the Bathtub Curve. 😊

People will say… “but it’s just [insert percentage]”

They don’t seem to comprehend how exponential growth occurs. And it has to start somewhere where. It’s like that game where you say you’ll pay one penny the first day and the 2 pennies the next day, then 4 pennies, then 8.

They don’t seem to comprehend how exponential growth occurs. And it has to start somewhere where. It’s like that game where you say you’ll pay one penny the first day and the 2 pennies the next day, then 4 pennies, then 8.

8 Pennies might not seem like a lot, but it will grow.

But also, Railways are Russia’s backbone. Switching to Road traffic just isn’t feasible in a lot of places due to not only the condition of the roads, and the increased cost, but also the lack of drivers.

But also, Railways are Russia’s backbone. Switching to Road traffic just isn’t feasible in a lot of places due to not only the condition of the roads, and the increased cost, but also the lack of drivers.

There’s no point in producing products if you can’t ship them. The lack of shipping will constrain the economy (if they other things don’t get them first).

All of Russia’s discussions of huge growth in the future don’t make sense if your shipping capacity is shrinking.

All of Russia’s discussions of huge growth in the future don’t make sense if your shipping capacity is shrinking.

And according to this, the Ministry of Economy to didn’t consider the issue of transportation in their strategic forecasts.

Which seems like their reports are either disingenuous or incompetent. Russian Railways is a monopoly with one shareholder, the Russian Government.

Which seems like their reports are either disingenuous or incompetent. Russian Railways is a monopoly with one shareholder, the Russian Government.

https://twitter.com/prune602/status/1779920541773672563

It’s not like it was hard to go the MONOPOLY that YOU OWN to get the data that shows that things are bad.

All of this leads to the overall conclusion:

IT WILL GET WORSE

~ The End ~

All of this leads to the overall conclusion:

IT WILL GET WORSE

~ The End ~

• • •

Missing some Tweet in this thread? You can try to

force a refresh