A USER'S GUIDE TO RESTRUCTURING THE GLOBAL TRADING SYSTEM

As markets look forward to a second Trump Admin, there are lots of bad predictions that tariffs will cause horrible inflation, or the President can't affect the dollar. Both are false. /1 hudsonbaycapital.com/documents/FG/h…

As markets look forward to a second Trump Admin, there are lots of bad predictions that tariffs will cause horrible inflation, or the President can't affect the dollar. Both are false. /1 hudsonbaycapital.com/documents/FG/h…

There's a variety of tools the Trump Admin can use to procure fairer and more reciprocal international trade, through tariffs or currency policy. Each tool has different potential side effects, but there are steps the Admin can take to mitigate them. /2

Disclaimer: As always, these views are mine alone, and I certainly don’t speak for any of my colleagues, and I’m not affiliated with the Trump transition effort. This is my interpretation of what causes our persistent imbalances, and describing various tools I think could help./3

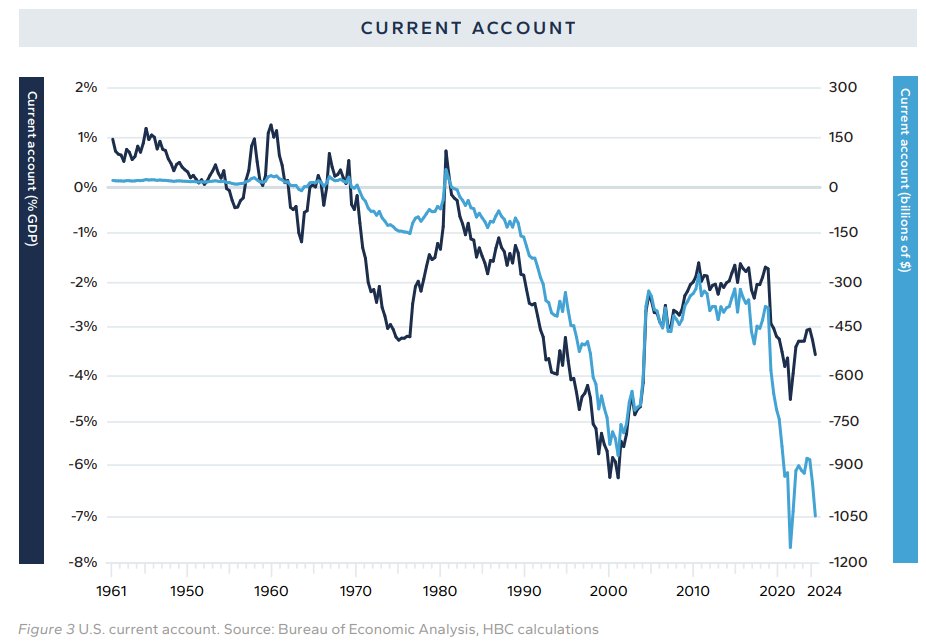

Before devising solutions, it's important to diagnose the source of the trade asymmetries. That lies in the inelastic demand for reserve assets, regardless of price. /4

Treasury securities are bought for reserve purposes--facilitating trade between other countries, or managing another country's currency--they're bought regardless of yield or fundamental return characteristics for the United States. /5

That inelastic demand for Treasurys puts upward pressure on the dollar. As global GDP grows relative to US GDP, the distortion in the currency market that prevents trade flows from balancing grows similarly larger. /6

The burden the overvalued dollar places on the U.S. manufacturing sector drives carnage across the industrial base of the country, and places an enormous drag on our export sector. American workers bear the cost for global reserve provision. /7

Our borrowing isn’t caused by overconsumption, but the reverse—we import too much because we export reserve assets to facilitate global trade and savings. /8

That makes trade deeply unfair to Americans, leaving us to bear the costs of global reserve provision and defense simultaneously (and the two are linked). There are two major ways to address the root problem: tariffs or currency interventions. /9

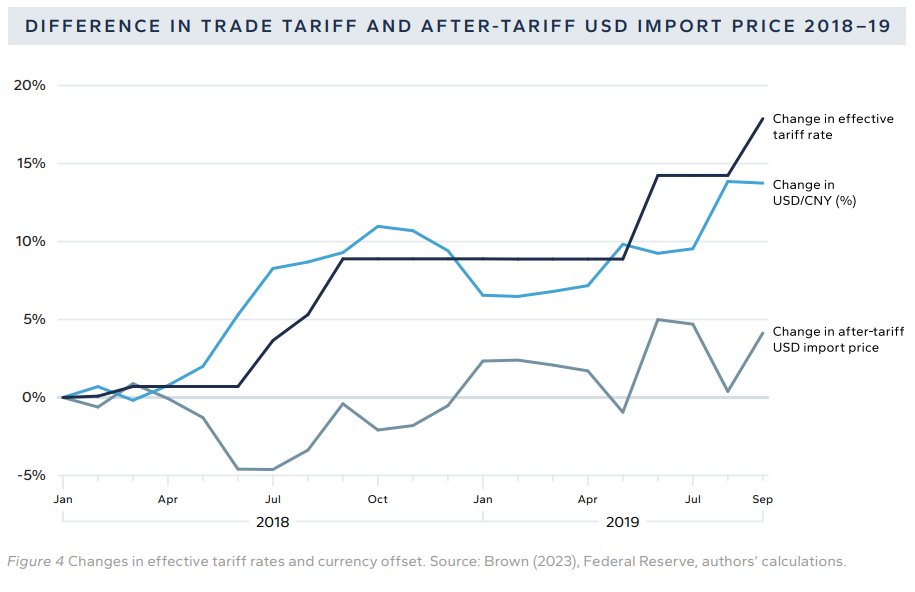

In Trump's first term, there was no discernible rise in inflation or drag on growth. Why?

The answer lies in what economists call "currency offset."

The dollar moved up by almost the exact amount as the tariffs did. After-tariff USD import prices didn't move. /10

The answer lies in what economists call "currency offset."

The dollar moved up by almost the exact amount as the tariffs did. After-tariff USD import prices didn't move. /10

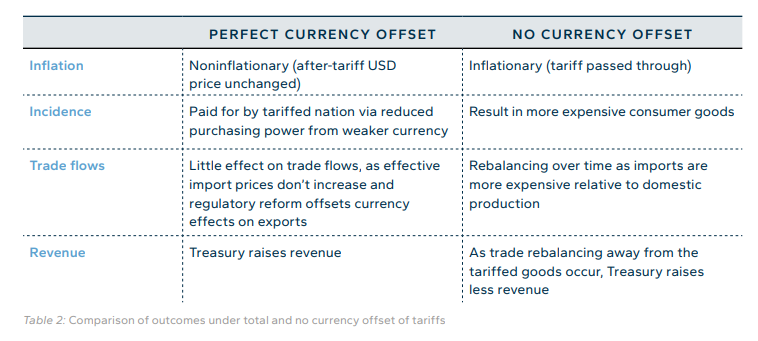

If the currency offsets the tariff, what are the consequences? Prices don’t budge much, so there’s no inflation and Treasury raises a lot of revenue. But the Chinese were made poorer, because their purchasing power declined with the renminbi. In that sense, they paid for the tariff. /11

Because the total revenue raised over a decade of the China tariffs works out to be roughly a third of the cost of the Tax Cuts and Jobs Act of 2017, China effectively paid for a big chunk of the tax cuts for American workers and businesses. /12

Currency offset matters: if there are no material price changes, there’s no inflation or growth drags, but there’s also little incentive to reallocate supply chains out of China.If it doesn’t occur, there’s more incentive to move supply chains, but less revenue. /13

In the paper, I discuss why currency offset occurs, and some of the academic literature on microdata on tariffs and why I think it’s wrong…look into it if of interest! (twitter thread shouldn’t’ be 1000 posts long) /14

Because the tariff levels President Trump has proposed are much higher than what was enacted in his first term, there are greater risks, too. Therefore, an approach of gradualism can be employed to help minimize adverse consequences like market volatility. /15

If the Administration proceeds at a monthly place of tariff increases e.g. 2% until China complies with certain international trading norms like respecting intellectual property and opening its markets, tariffs will slowly ratchet up over time. /16

A clear and gradual but nevertheless inevitable upward path for tariffs will reduce uncertainty and thereby market volatility. The transparent forward guidance will give firms time to adjust their behavior rather than causing upsets in the markets. /17

Such a policy could get to 60% tariffs on China within a couple of years without the negative consequences of sharp and sudden moves.

What about the 10%+ tariffs Trump has proposed for the rest of the world? /18

What about the 10%+ tariffs Trump has proposed for the rest of the world? /18

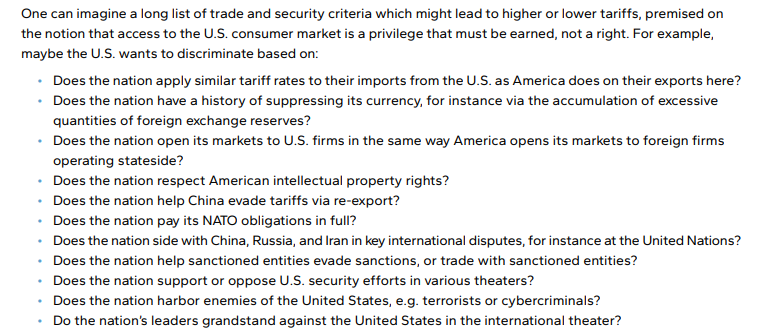

Here again, it could reduce volatility or other side effects by taking a phase-in approach. Moreover, Trump advisor Scott Bessent has recommended creating several buckets of tariff levels, and countries could fall into buckets based on their relationship with the U.S. /19

One can imagine a wide variety of criteria for these buckets, and a large number of buckets tailored at U.S. policy objectives /20

Such buckets would improve burden sharing tremendously. Those that abuse the system get higher tariff rates and pay more revenue to Treasury. Those that pull their weight in defense and trade retain lower tariff rates. Strong outcomes. /21

In sum, tariffs can be implemented with an eye toward minimizing adverse consequences, and incentivizing good behavior from our trading and defense partners.

What about currency policies to address consequences of dollar misvaluation? /22

What about currency policies to address consequences of dollar misvaluation? /22

There are two approaches: multilateral or unilateral. Most currency policy changes have been through multilateral accords. Many analysts argue there are no unilateral policies an administration can take. That’s definitely not true. /23

Multilateral accords work through an agreement with trading partners to raise the value of their currencies closer to fair value. Of course, they’ll require incentives to get there—sticks and carrots.

I discuss what a potential “Mar-a-Lago Accord” could look like. /24

I discuss what a potential “Mar-a-Lago Accord” could look like. /24

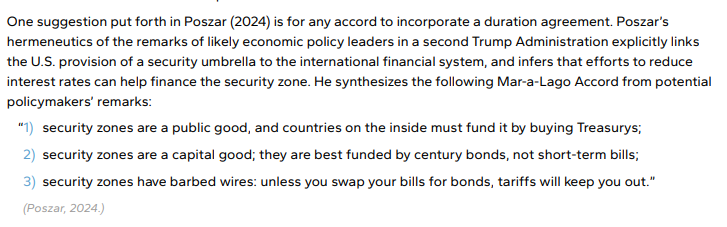

In particular, if you’re telling trading partners to sell dollar assets, you need to come up with a way of preventing unwanted rises in the long end of the yield curve. I discuss some steps for that, with a hat tip to Zoltan Poszar channeling some Trump advisors. /25

Any multilateral accord can extend to duration as well. If countries want to remain inside the U.S. trade and security umbrella, they can help share the burden of reserve asset and defense provision by terming out their Treasury holdings. /26

By buying ultra-long-term Treasury bonds, they can alleviate pressure on U.S. financing for their reserves and defense. It’s a significant improvement on burden sharing relative to all the burden placed on American taxpayers and manufacturers. /27

There are also a variety of unilateral approaches designed either to accumulate foreign currencies and raise their value (an approach taken by many other nations), or to discourage the accumulation of excess Treasury reserves. /28

These approaches would be more experimental, and the set of potential side effects is wider and more uncertain. Still, if the President decides he wants to weaken the dollar unilaterally, there are means of doing so, and ways to mitigate side effects. /29

These approaches include: accumulating our own reserve assets; selling gold reserves; disincentivizing the accumulation of excess reserve assets. They each have different costs or benefits associated with them. /30

I go through some of these approaches in detail. Because currency policy hasn’t been active in decades, and it’s less well understood than tariffs, which the last Trump Admin used extensively, I expect tariffs to get first up at bat. /31

Tariffs also build leverage for future bilateral or multilateral agreements. China only came to the table to negotiate, and then agreed to the Phase 1 deal, because of the leverage that tariffs provided. /32

For these reasons, I expect tariffs to precede currency policy, if it ever comes. Tariffs put upward pressure on the dollar, but currency policy, if it’s used, is likely to put upward pressure on other currencies. /33

That means I expect Trump policy to be strongly dollar positive before reversing, if it ever does. The sequencing matters.

There’s a whole bunch of other market implications I discuss—energy, rates, the Fed, equities… /34

There’s a whole bunch of other market implications I discuss—energy, rates, the Fed, equities… /34

But this thread is long enough as it is. Check out the paper! /END hudsonbaycapital.com/documents/FG/h…

• • •

Missing some Tweet in this thread? You can try to

force a refresh