Software inflation accounts for over half of core goods inflation in the last four months. (We study four months because that's when software clearly inflected upward, the appropriate period will lengthen as time goes on)

Software inflation accounts for over half of core goods inflation in the last four months. (We study four months because that's when software clearly inflected upward, the appropriate period will lengthen as time goes on)

Summary: changes to Treasury's issuance policies have provided similar economic stimulus as a 1% cut in the Fed Funds rate, usurping core functions of monetary policy and blocking the Fed's efforts to restrain inflation and growth.

Summary: changes to Treasury's issuance policies have provided similar economic stimulus as a 1% cut in the Fed Funds rate, usurping core functions of monetary policy and blocking the Fed's efforts to restrain inflation and growth.  @mtkonczal has given a beautiful decomposition, but I have a somewhat different interpretation

@mtkonczal has given a beautiful decomposition, but I have a somewhat different interpretation

-Significant slowdown in labor markets and potentially consumption, typically thought of as "lagging"

-Significant slowdown in labor markets and potentially consumption, typically thought of as "lagging"

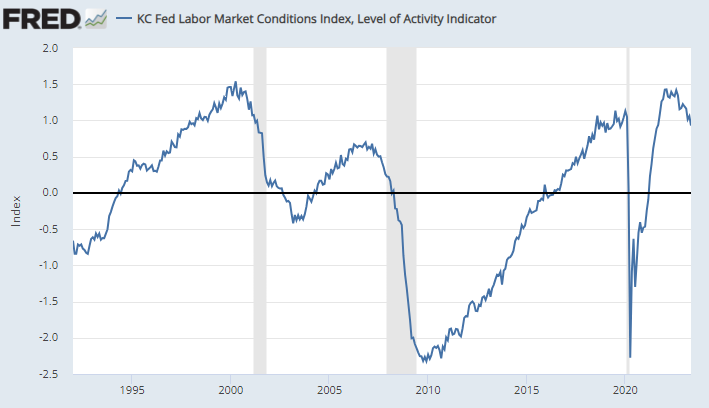

Unemployment is a useful indicator, but it's not the only one. In fact, there are hundreds of labor market series. A particularly helpful tool is the Fed's "Labor Market Conditions Index," which takes 24 important data series and reduces the dimensionality via PCA. (Summarizes)

Unemployment is a useful indicator, but it's not the only one. In fact, there are hundreds of labor market series. A particularly helpful tool is the Fed's "Labor Market Conditions Index," which takes 24 important data series and reduces the dimensionality via PCA. (Summarizes)