Telling insurers they can't do denials is a surefire way to waste money on quack "cures" and to get millions of Americans devastatingly addicted to medications that end up killing them.

We know this is true because it's happened before.

Let's talk quacks. Thread about boobs.

We know this is true because it's happened before.

Let's talk quacks. Thread about boobs.

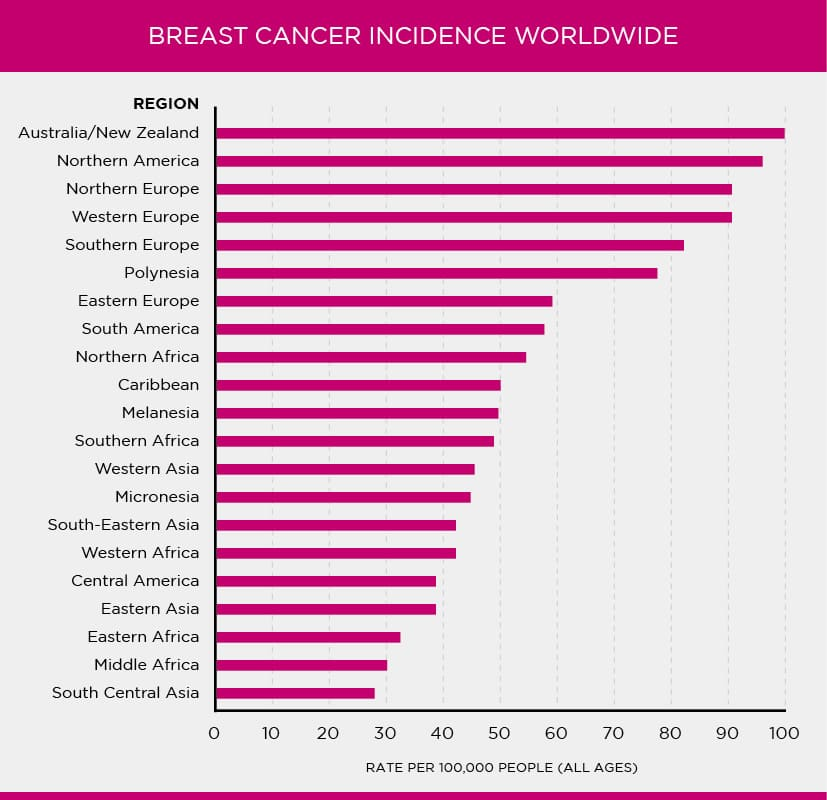

Breast cancer is an unfortunately common condition worldwide.

In 2021, more than 270,000 American women were diagnosed with it and some 42,000 died from it and it affects almost 1-in-8 American women in their lifetimes.

In short, it's bad.

In 2021, more than 270,000 American women were diagnosed with it and some 42,000 died from it and it affects almost 1-in-8 American women in their lifetimes.

In short, it's bad.

Each year in the U.S., more than 100,000 women undergo some form of mastectomy, often to treat, and sometimes to prevent breast cancer, among other things.

Unsurprisingly given how much everyone loves breasts and living, people have been seeking a cure for breast cancer.

Unsurprisingly given how much everyone loves breasts and living, people have been seeking a cure for breast cancer.

In the late-1960s, it was demonstrated that allogeneic (from someone else) marrow transplantation could be used in the treatment of leukemia.

In the 1970s, autologous (from the same person) transplantation for lymphoma was shown to work.

These then became widespread.

In the 1970s, autologous (from the same person) transplantation for lymphoma was shown to work.

These then became widespread.

The TL;DR way that these transplants help with cancerous tumor treatment is by allowing chemotherapy or radiation at much higher, and indeed supralethal doses, that the transplant "rescues" the patient from, since radiation will otherwise destroy their bone marrow.

Naturally, people were enthusiastic to use autologous bone marrow transplantation in the treatment of breast cancer, allowing them to subject solid breast tumors to higher radiation doses, thus hopefully achieving greater success in cancer elimination without more drastic means.

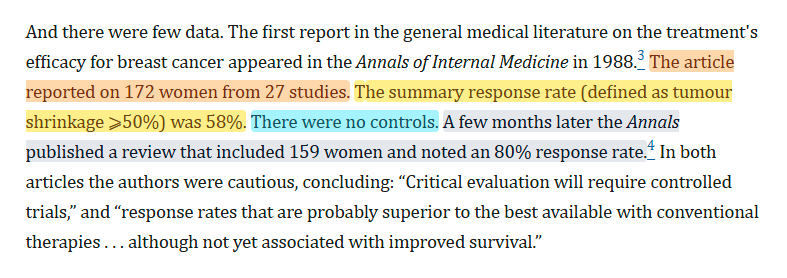

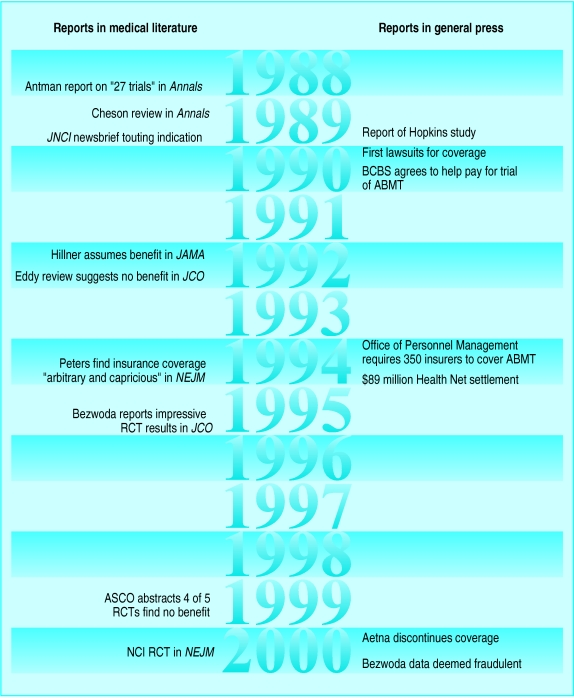

The first reports on this procedure came out in 1988, a few years after it started being discussed by its early proponents.

The reports in Annals of Internal Medicine... were not very detailed or reassuring about the procedure. They weren't even about controlled trials:

The reports in Annals of Internal Medicine... were not very detailed or reassuring about the procedure. They weren't even about controlled trials:

Notice, for example, that the two reports had similar, modest sample sizes, and massively different response rates. That suggests a lack of precision at the very least, and something certainly in need of follow-up.

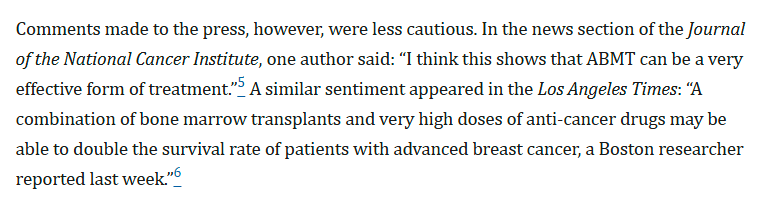

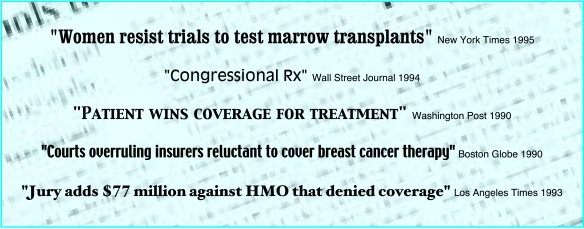

Nevertheless, some doctors ate it up and the press rejoiced:

Nevertheless, some doctors ate it up and the press rejoiced:

Breast cancer is so feared and so common that the press ate this up, and the Washington Post ran a story on it.

A few months later, a Maryland woman sued her insurer to get the extremely expensive, at-that-point highly experimental treatment.

A few months later, a Maryland woman sued her insurer to get the extremely expensive, at-that-point highly experimental treatment.

She won, and she won... curiously.

The federal judge declared "To require the plaintiff... wait until somebody chooses to present statistical proof... that would satisfy all the experts means that plan members would be doomed to receive... procedures that are not [SotA]."

The federal judge declared "To require the plaintiff... wait until somebody chooses to present statistical proof... that would satisfy all the experts means that plan members would be doomed to receive... procedures that are not [SotA]."

That judgment was a dam breaking.

Later the same month, a judge ordered an insurer in Massachusetts to pay for an autologous bone marrow transplant for another woman.

Insurers argued: "We view [this procedure] as... experimental... it has not proved safe and effective."

Later the same month, a judge ordered an insurer in Massachusetts to pay for an autologous bone marrow transplant for another woman.

Insurers argued: "We view [this procedure] as... experimental... it has not proved safe and effective."

Insurers said they would not pay for experimental treatments.

Courts, newspapers, politicians, and doctors did not like this, and patients were incensed. Understandably, no one wanted to be denied care because it was "experimental."

So BCBS acquiesced and agreed to fund a trial

Courts, newspapers, politicians, and doctors did not like this, and patients were incensed. Understandably, no one wanted to be denied care because it was "experimental."

So BCBS acquiesced and agreed to fund a trial

Before the trial was through, articles started coming out claiming autologous bone marrow transplant (ABMT) might work, that it could provide substantial therapeutic benefits at a high cost, and, ultimately, the press ran with "High cost... treatment helps fight breast cancer."

Women started taking their doctors to court to get the treatment.

Suddenly, dozens of cases were being filed. One particular well-known one involved a woman from Riverside, CA, who sued Health Net for refusing to cover.

She won, got the treatment, and died a few months later.

Suddenly, dozens of cases were being filed. One particular well-known one involved a woman from Riverside, CA, who sued Health Net for refusing to cover.

She won, got the treatment, and died a few months later.

The family claimed that the coverage was too late, and the woman would have lived had Health Net paid up sooner.

They won the largest judgment "ever levied against an insurance company for refusing to provide health coverage benefits." They got a whopping $89.1 million.

They won the largest judgment "ever levied against an insurance company for refusing to provide health coverage benefits." They got a whopping $89.1 million.

Some insurers started giving in, and doctors went to bat for patients.

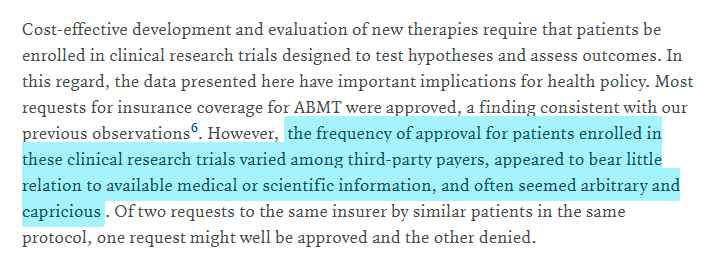

In the New England Journal of Medicine, one of the nation's most prominent transplanters asserted that denials of ABMT were "arbitrary and capricious."

Newspapers loved that.

In the New England Journal of Medicine, one of the nation's most prominent transplanters asserted that denials of ABMT were "arbitrary and capricious."

Newspapers loved that.

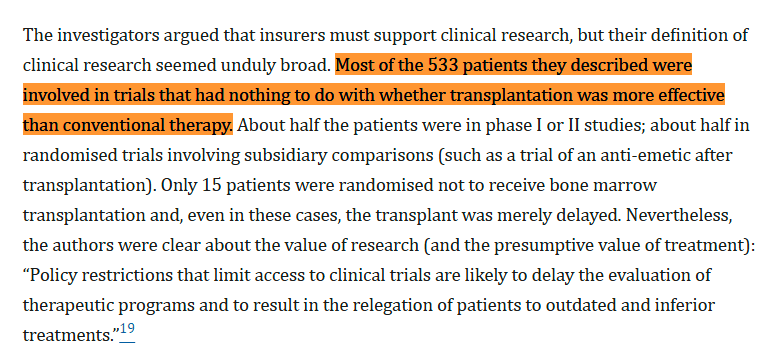

These doctors argued that insurers had a duty to support clinical research for the good of those they insure.

But their evaluation upon which they rendered their judgments?

Total rubbish. Generally not even relevant evidence, in fact!

But their evaluation upon which they rendered their judgments?

Total rubbish. Generally not even relevant evidence, in fact!

Nevertheless, the presumption of benefit had set in.

Doctors worked with lawyers to compel insurers to pay for coverage of ABMT, and the government even started to weigh in, hastily.

The Office of Personnel Management forced all federal employees' health plans to cover ABMT.

Doctors worked with lawyers to compel insurers to pay for coverage of ABMT, and the government even started to weigh in, hastily.

The Office of Personnel Management forced all federal employees' health plans to cover ABMT.

There was immense political pressure to force insurers to cover ABMT, and doctors in seven states managed to mandate their states' insurers pay for the procedure.

Doctors even sent in data to Congress, with the claim that the procedure worked wonders.

Insurers lost this fight.

Doctors even sent in data to Congress, with the claim that the procedure worked wonders.

Insurers lost this fight.

In 1995, Journal of Clinical Oncology published a report by W.R. Bezwoda, claiming substantial benefits to the therapy.

Finally, a randomized, controlled trial!

This image contains a spoiler.

Finally, a randomized, controlled trial!

This image contains a spoiler.

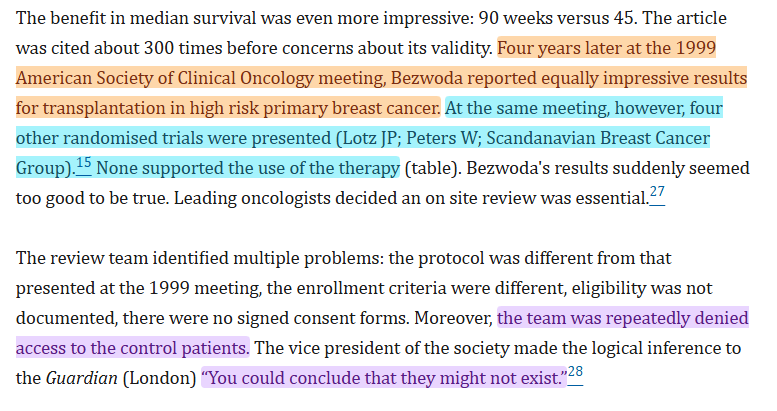

Four years later, Dr. Bezwoda spoke about similarly impressive results at the annual meeting of the American Society of Clinical Oncology.

This time, however, there were four similar trials and they all found nothing.

So Bezwoda's work was reviewed. Problems found:

This time, however, there were four similar trials and they all found nothing.

So Bezwoda's work was reviewed. Problems found:

Suddenly, the world knew that ABMT's sole RCT evidence was fraudulent, and the therapy did not actually work.

But by now, it was huge. It was a top-line procedure many physicians recommended to breast cancer patients for a decade.

Tens of thousands had used ABMT!

But by now, it was huge. It was a top-line procedure many physicians recommended to breast cancer patients for a decade.

Tens of thousands had used ABMT!

Not only had people wasted their time with a therapy that was expensive and didn't work, it was highly invasive--far more than alternative options--and it was actually harmful unless it had the presumed cancer-fighting benefits it never actually had!

Cui bono?

Physicians, to a lesser extent lawyers, and definitely not patients.

For a decade, insurers were bullied by the media, courts, and doctors into covering something that sucked for patients and didn't help them in the slightest.

Physicians, to a lesser extent lawyers, and definitely not patients.

For a decade, insurers were bullied by the media, courts, and doctors into covering something that sucked for patients and didn't help them in the slightest.

It sucks not knowing if you're going to live to see tomorrow, but let's not forget that we still have to make socially wise decisions about healthcare.

Insurers most often make those decisions, and they suffer for saying "no".

"No" may feel wrong, but it's very often right.

Insurers most often make those decisions, and they suffer for saying "no".

"No" may feel wrong, but it's very often right.

There's also a lesson in here about how doctors are generally very bad at statistics and their pronouncements on statistical matters are often really bad.

Ask any hospital stats guy for confirmation.

Sources:

cdc.gov/united-states-…

brighamandwomens.org/surgery/surgic…

acsjournals.onlinelibrary.wiley.com/doi/full/10.33…

archive.md/l9nAC

nejm.org/doi/10.1056/NE…

pmc.ncbi.nlm.nih.gov/articles/PMC11…

Ask any hospital stats guy for confirmation.

Sources:

cdc.gov/united-states-…

brighamandwomens.org/surgery/surgic…

acsjournals.onlinelibrary.wiley.com/doi/full/10.33…

archive.md/l9nAC

nejm.org/doi/10.1056/NE…

pmc.ncbi.nlm.nih.gov/articles/PMC11…

• • •

Missing some Tweet in this thread? You can try to

force a refresh