"MPT was here..."

Leaving a trail of wreckage across multiple continents. $MPW

Leaving a trail of wreckage across multiple continents. $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"Silver Point was here..." as well!

"Silver Point was here..." as well!

"MPT was here..." $MPW

"MPT was here..." $MPW

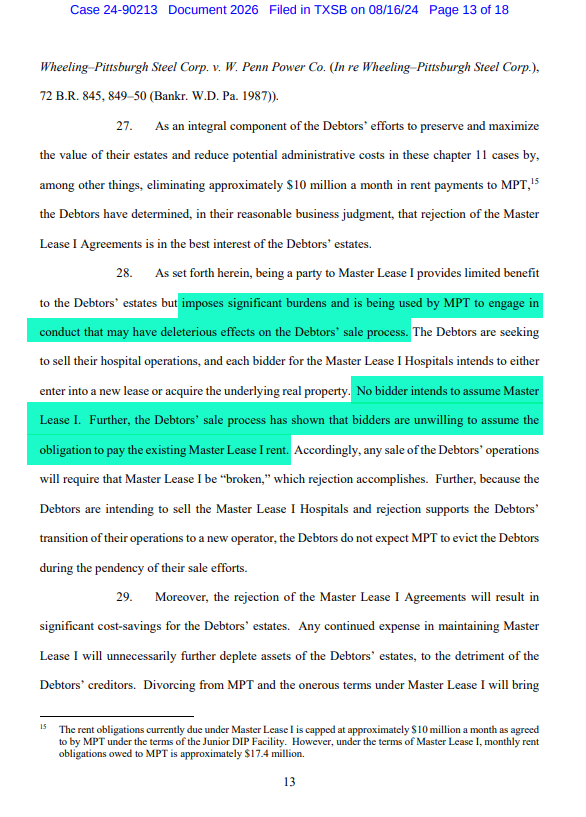

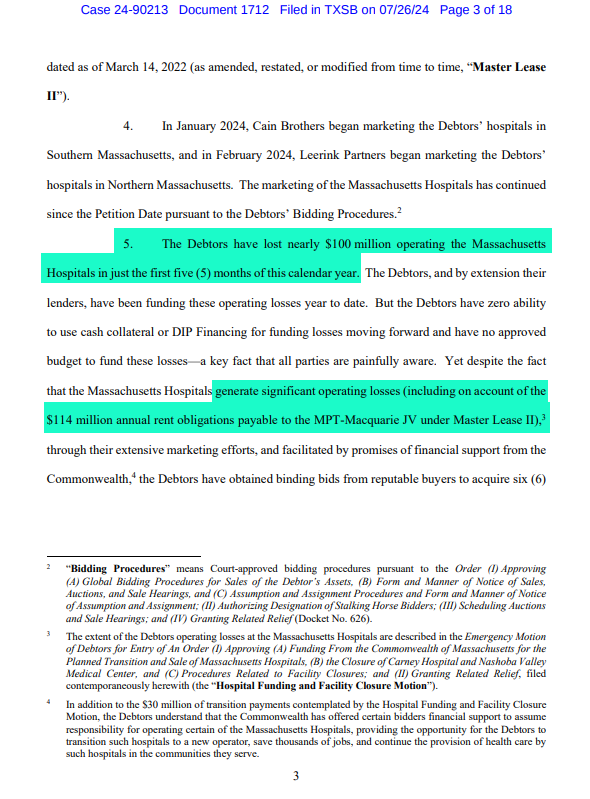

The PA hospitals have "experienced significant losses" since 2014.

MPT bought the real estate in 2019 for $421MM. MPT "underwrote" in place "Adjusted EBITDAR" of $4.7MM. Year 1 cash rent was $31.6MM. 2023 cash rent would have been approx. $35.5MM.

Annual EBITDA losses (before rent) are now tracking towards approx. $184MM.

"We underwrite the real estate..."

The PA hospitals have "experienced significant losses" since 2014.

MPT bought the real estate in 2019 for $421MM. MPT "underwrote" in place "Adjusted EBITDAR" of $4.7MM. Year 1 cash rent was $31.6MM. 2023 cash rent would have been approx. $35.5MM.

Annual EBITDA losses (before rent) are now tracking towards approx. $184MM.

"We underwrite the real estate..."

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..."

or is it "MPT is here...?"

This sounds very similar to Steward's "extreme financial hardship" from late-2022 through mid-2023...

Or Prospect's cyber attack in mid-2023...

When in reality, AHS just doesn't have any money. Only MPT's money! $MPW

or is it "MPT is here...?"

This sounds very similar to Steward's "extreme financial hardship" from late-2022 through mid-2023...

Or Prospect's cyber attack in mid-2023...

When in reality, AHS just doesn't have any money. Only MPT's money! $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

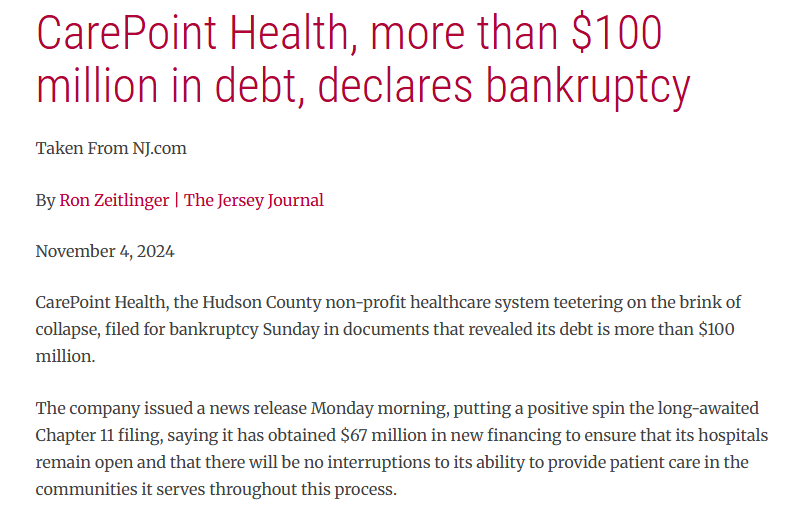

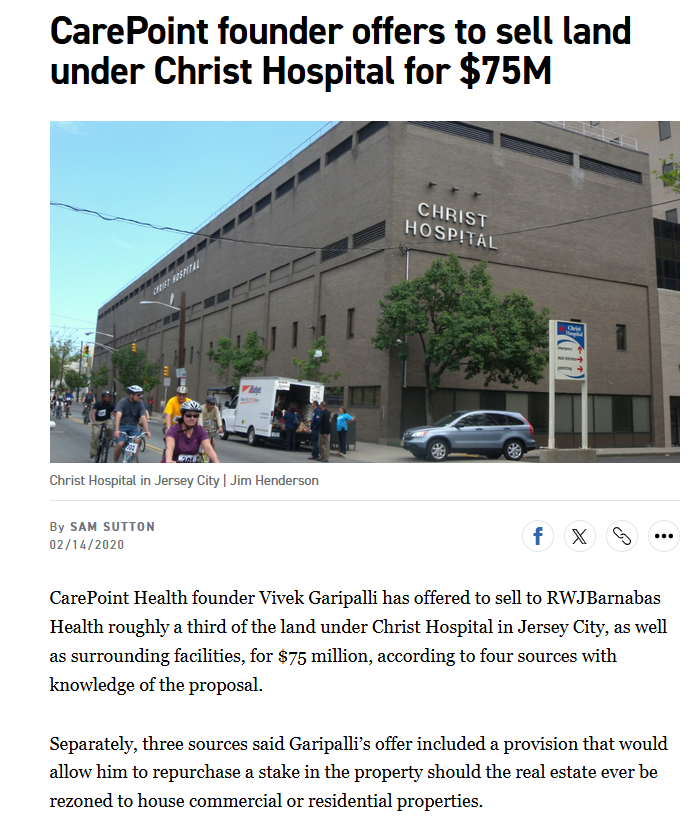

"MPT was here..." at Carepoint.

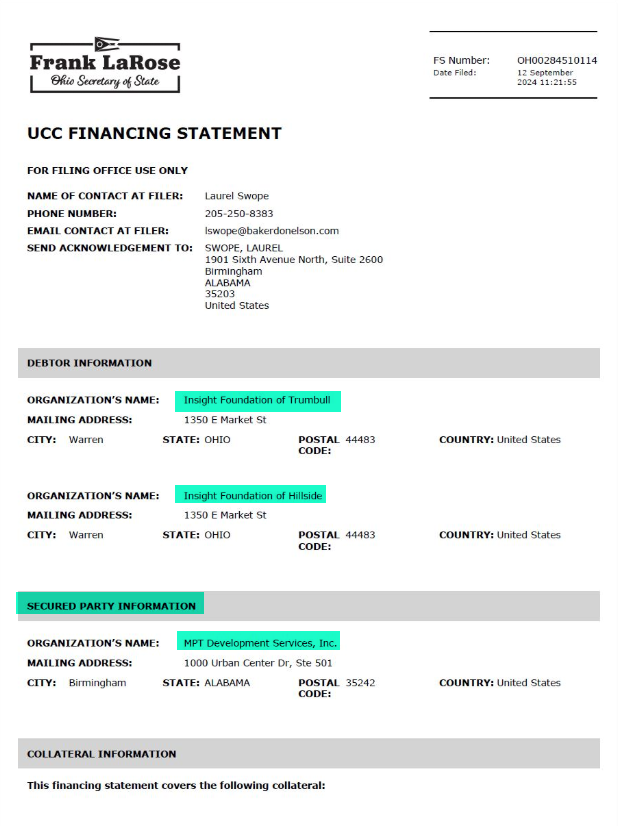

"MPT is here..." with Insight! Another manager of former Steward ML1 hospitals along with HSA, who seems to be strapped for cash... $MPW

"MPT is here..." with Insight! Another manager of former Steward ML1 hospitals along with HSA, who seems to be strapped for cash... $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..." $MPW

"MPT was here..."

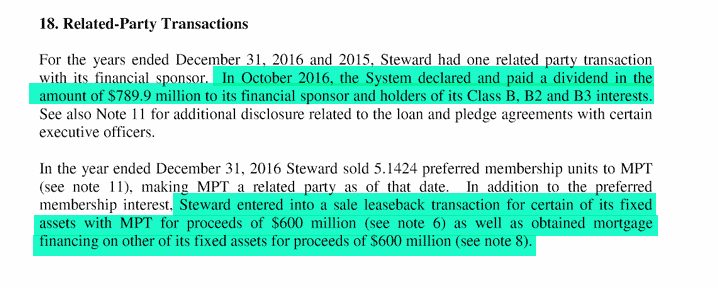

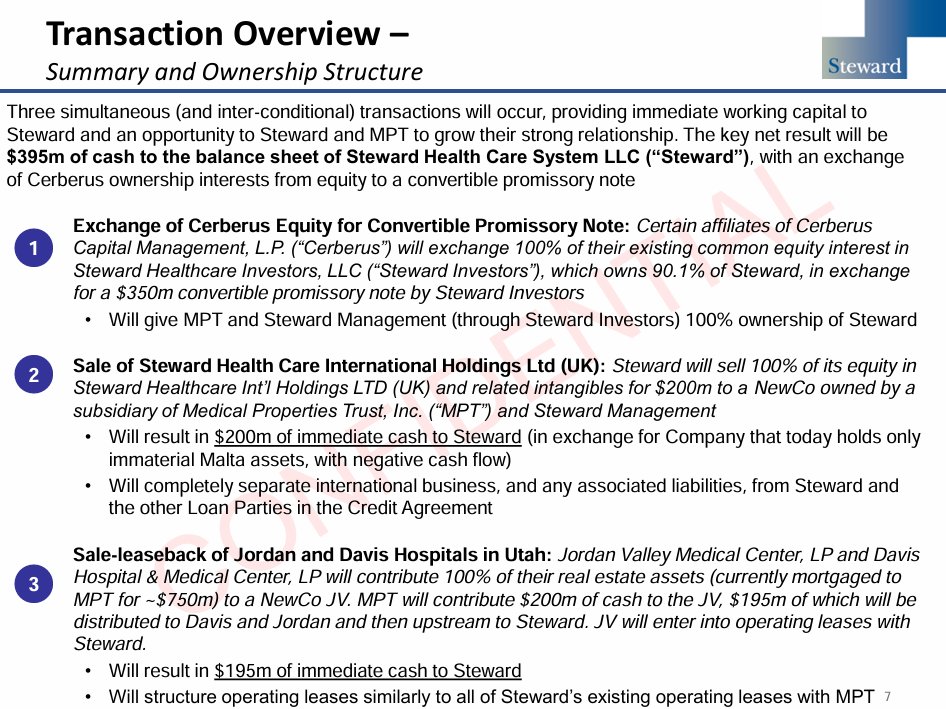

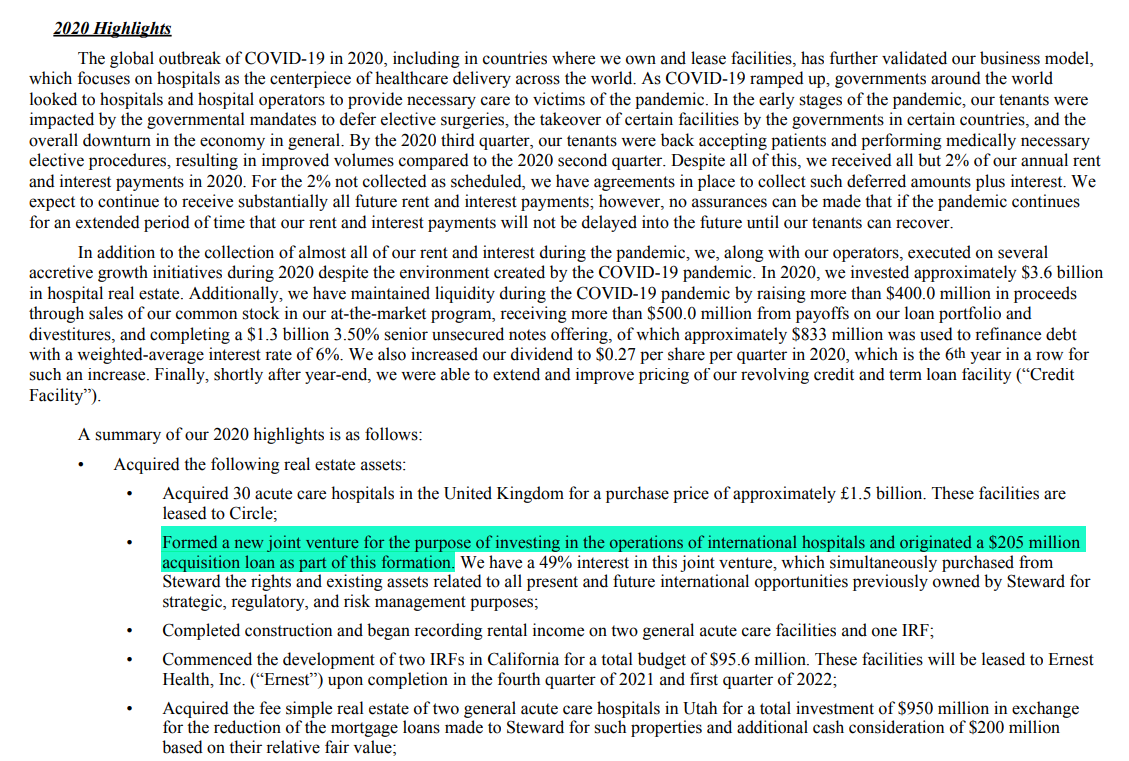

MPT received "time and effort and infrastructure in place" for their $205MM! The JV was "formed... for the purpose of investing in the operations of international hospitals...," according to the 31/12/20 10-K!

Actually, MPT received a 49% interest (despite putting up 100% of the capital!) in a shell company that "holds only immaterial Malta assets, with negative cash flow."

What MPT really received was rent from SHCS... originating from itself! They exceeded the max threshold on "NFFO" for 2020! Cash bonuses for all! $MPW

MPT received "time and effort and infrastructure in place" for their $205MM! The JV was "formed... for the purpose of investing in the operations of international hospitals...," according to the 31/12/20 10-K!

Actually, MPT received a 49% interest (despite putting up 100% of the capital!) in a shell company that "holds only immaterial Malta assets, with negative cash flow."

What MPT really received was rent from SHCS... originating from itself! They exceeded the max threshold on "NFFO" for 2020! Cash bonuses for all! $MPW

"MPT was here..." $MPW

"MPT was here..."

"Coming clean," without actually coming clean. Steward really needed that MPT plane at the height of the COVID emergency! $MPW

"Coming clean," without actually coming clean. Steward really needed that MPT plane at the height of the COVID emergency! $MPW

"MPT was here..."

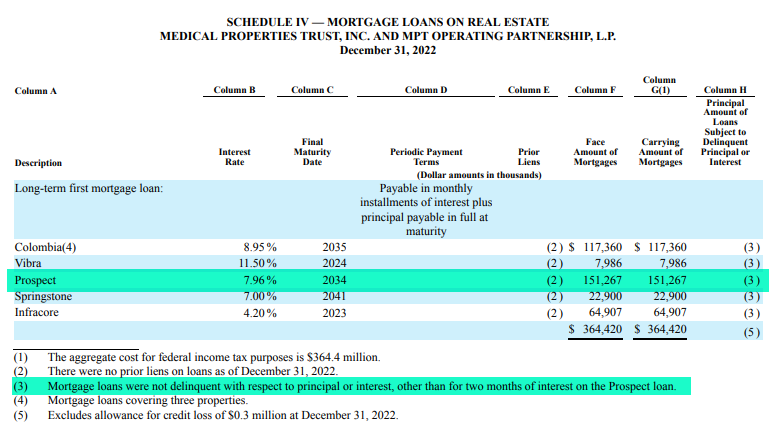

2014 - Prospect paid $15MM for the Foothill RE + ops

2019 - MPT originated a $51.3MM mortgage against RE

2022 - MPT advanced add. $100MM "mortgage" on RE

2025 - $ASTH buys RE + ops for $18.6MM

Go it. Where did the money go? $MPW

2014 - Prospect paid $15MM for the Foothill RE + ops

2019 - MPT originated a $51.3MM mortgage against RE

2022 - MPT advanced add. $100MM "mortgage" on RE

2025 - $ASTH buys RE + ops for $18.6MM

Go it. Where did the money go? $MPW

"MPT was here..."

or shall we say, "MPT is here..." $MPW

or shall we say, "MPT is here..." $MPW

https://x.com/BigRiverCapita1/status/1899661333982818572

"MPT was here..."

or shall we say, "MPT is here..." $MPW

or shall we say, "MPT is here..." $MPW

https://x.com/BigRiverCapita1/status/1899658113516491117

"MPT was here..." $MPW

Six months...

Six months...

"MPT was here..." $MPW

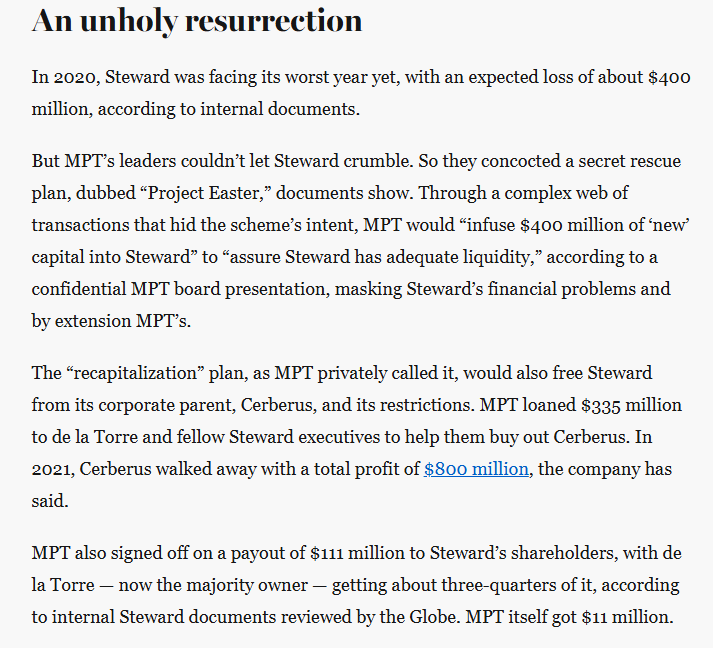

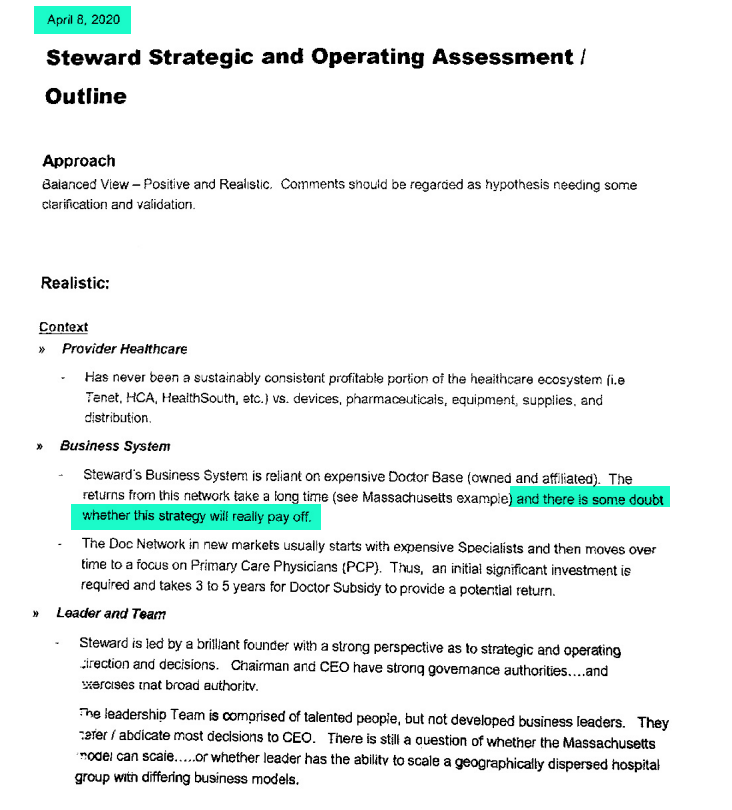

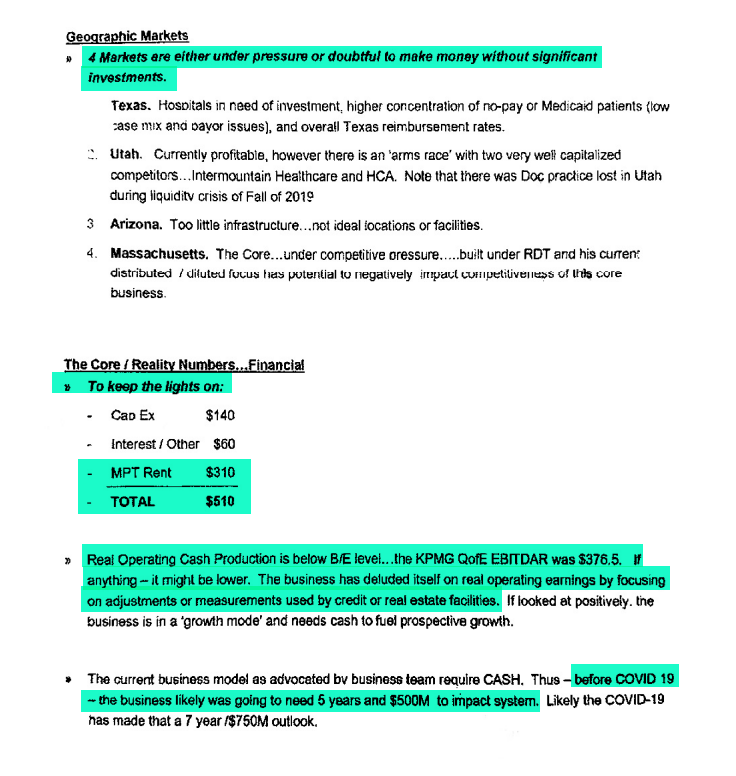

Steward was "below break-even" BEFORE Covid, per Cerberus in April 2020. This was one month before the "Project Easter" recap by MPT completed in May 2020.

$376.5MM of corporate EBITDAR vs. $310MM of MPT rent, $60MM of interest and $140MM of required CAPX. Steward required $500MM in cash BEFORE Covid. per its sponsor.

"Deluded itself," indeed!

How can the MPT coverages by trusted?

Steward was "below break-even" BEFORE Covid, per Cerberus in April 2020. This was one month before the "Project Easter" recap by MPT completed in May 2020.

$376.5MM of corporate EBITDAR vs. $310MM of MPT rent, $60MM of interest and $140MM of required CAPX. Steward required $500MM in cash BEFORE Covid. per its sponsor.

"Deluded itself," indeed!

How can the MPT coverages by trusted?

"MPT was here.."

And here, and there, and there... $MPW

"Indeed, the Insight deal underscores what has become a vicious cycle: A hospital sells its real estate to MPT, pockets the proceeds, slashes care, and spirals into financial distress. At that point, the property is so troubled that MPT has to pay a buyer, sometimes one with few scruples, to take over the hospital and continue paying rent — which will, in turn, drive the new buyer out of business as well. The only winners are the investors who figure out ways to extract money from dying hospitals — and MPT, which gets to continue collecting rent."

businessinsider.com/american-hospi…

And here, and there, and there... $MPW

"Indeed, the Insight deal underscores what has become a vicious cycle: A hospital sells its real estate to MPT, pockets the proceeds, slashes care, and spirals into financial distress. At that point, the property is so troubled that MPT has to pay a buyer, sometimes one with few scruples, to take over the hospital and continue paying rent — which will, in turn, drive the new buyer out of business as well. The only winners are the investors who figure out ways to extract money from dying hospitals — and MPT, which gets to continue collecting rent."

businessinsider.com/american-hospi…

"MPT was here..." $MPW

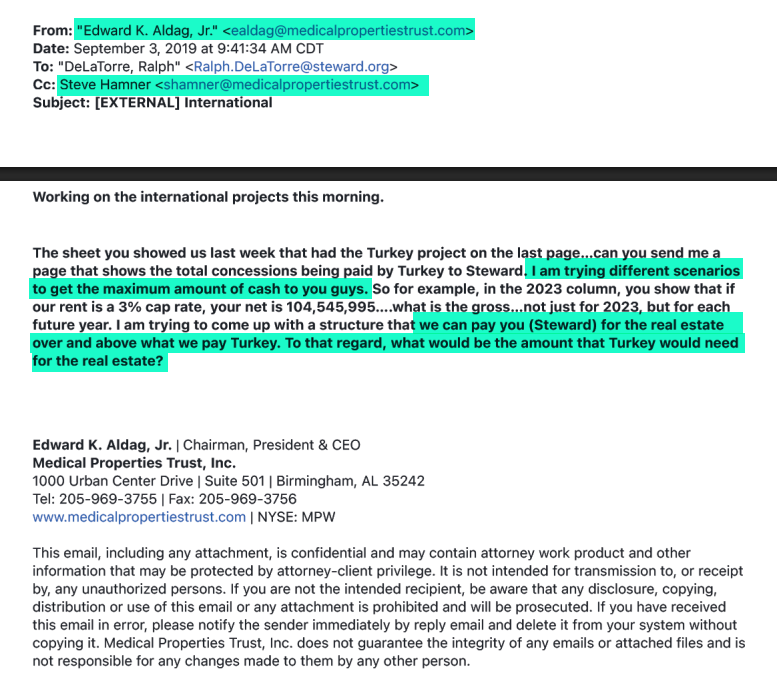

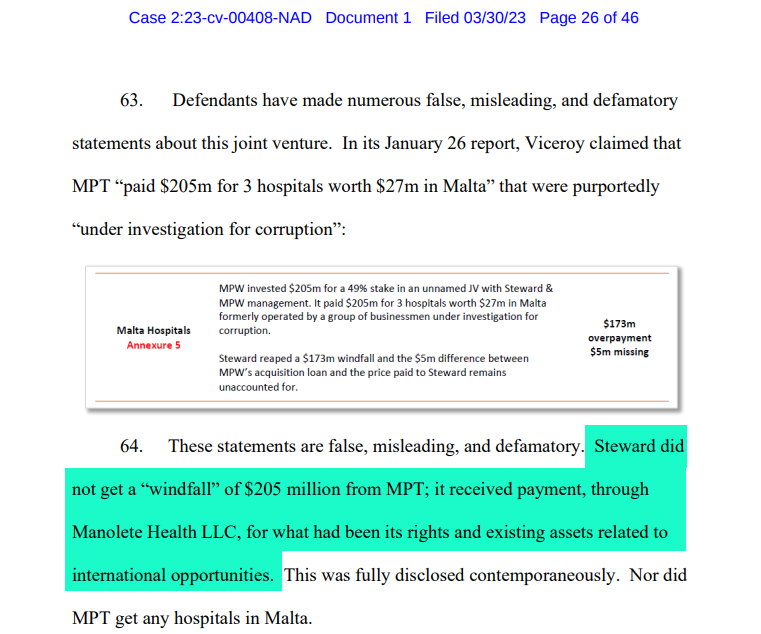

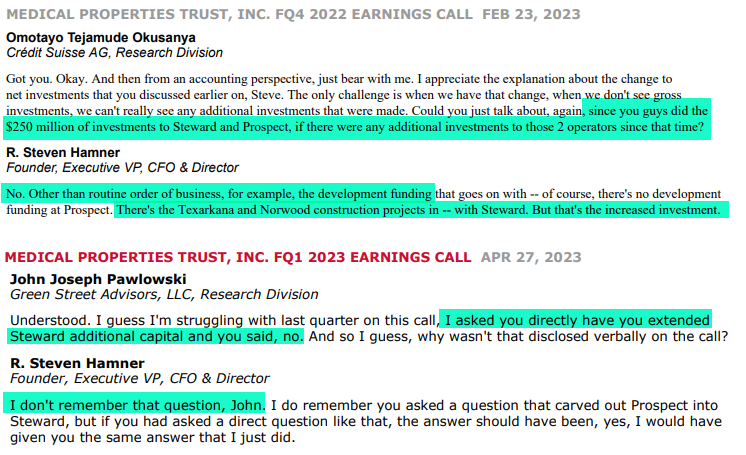

No, Steward did in fact receive a windfall of $205MM from MPT. And then MPT lied about its intended use and concealed that the funds were for working capital to an insolvent Steward as part of the "Project Easter" recap.

Why relieve Cerberus of any "fraudulent conveyance" claims, if Steward was not insolvent?

No, Steward did in fact receive a windfall of $205MM from MPT. And then MPT lied about its intended use and concealed that the funds were for working capital to an insolvent Steward as part of the "Project Easter" recap.

Why relieve Cerberus of any "fraudulent conveyance" claims, if Steward was not insolvent?

"MPT was here..." $MPW

"MPT was here..." $MPW

"Virtually wherever MPT has acquired health care facilities, you will find a trail of bodies..."

prospect.org/health/2025-03…

"Virtually wherever MPT has acquired health care facilities, you will find a trail of bodies..."

prospect.org/health/2025-03…

"MPT was here..." $MPW

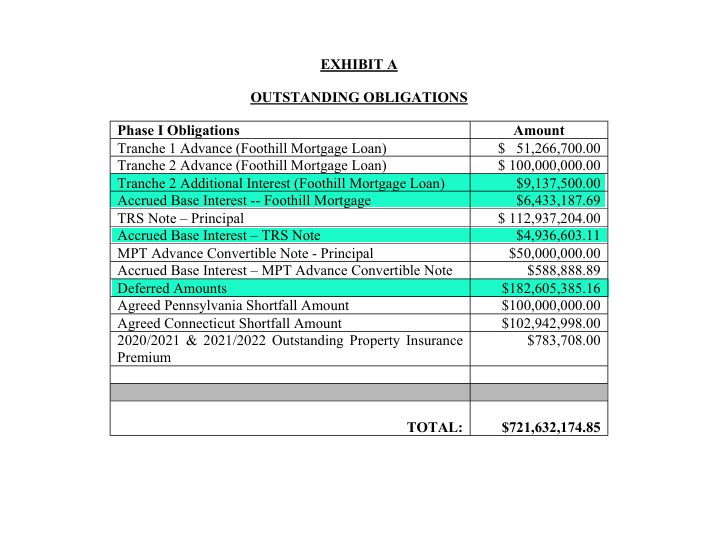

Make sure to give "clear instructions" to the appraiser, the "value" must be +$200MM higher so that Steward can get that amount as a working capital infusion!

Make sure to give "clear instructions" to the appraiser, the "value" must be +$200MM higher so that Steward can get that amount as a working capital infusion!

"MPT was here..." $MPW

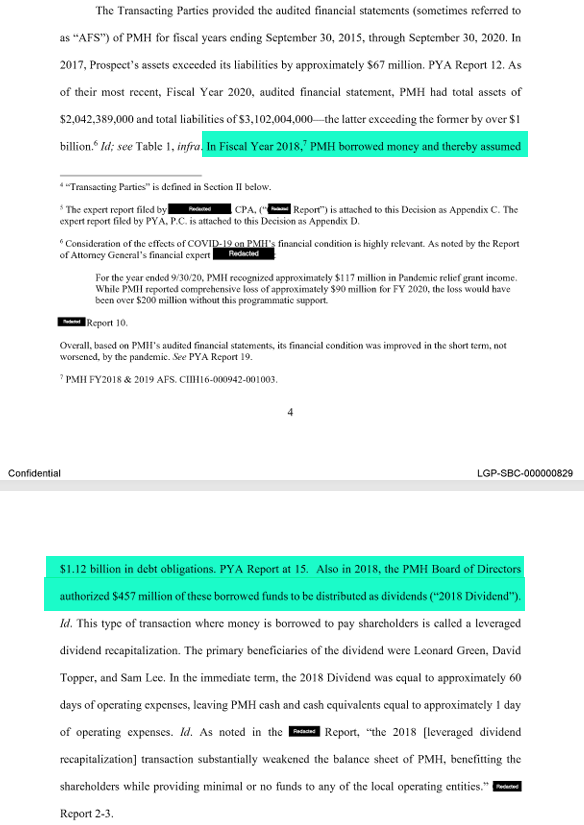

2019 MPT price for PMH CT RE: $457MM, which set most recent rents; 3.3x prior price paid 3 years earlier by PMH. Equaled LGP /Lee/Topper dividend in 2018 dollar-for-dollar, with SLB proceeds used to finance TL debt from dividend recap. So "leveraged looting" of a hospital system, unequivocally.

2016 PMH Price Allocated to RE: $140MM

2024 Revised YNHH Offer for WholeCo: just $150MM; YNHH later sued to invoke breach/MAC, noting "hospitals no longer financially viable"

Current MPT NBV for CT RE: Approx. $175MM

Proceeds, to the extent there are any, now need to go through a waterfall with hundreds of millions of senior claims above MPT's RE, including from state of CT.

PMH tracking towards a 60-70%+ total loss for MPT. Sound familiar? Think MAM JV. What else was acquired since 2019?

2019 MPT price for PMH CT RE: $457MM, which set most recent rents; 3.3x prior price paid 3 years earlier by PMH. Equaled LGP /Lee/Topper dividend in 2018 dollar-for-dollar, with SLB proceeds used to finance TL debt from dividend recap. So "leveraged looting" of a hospital system, unequivocally.

2016 PMH Price Allocated to RE: $140MM

2024 Revised YNHH Offer for WholeCo: just $150MM; YNHH later sued to invoke breach/MAC, noting "hospitals no longer financially viable"

Current MPT NBV for CT RE: Approx. $175MM

Proceeds, to the extent there are any, now need to go through a waterfall with hundreds of millions of senior claims above MPT's RE, including from state of CT.

PMH tracking towards a 60-70%+ total loss for MPT. Sound familiar? Think MAM JV. What else was acquired since 2019?

"MPT was here..." $MPW

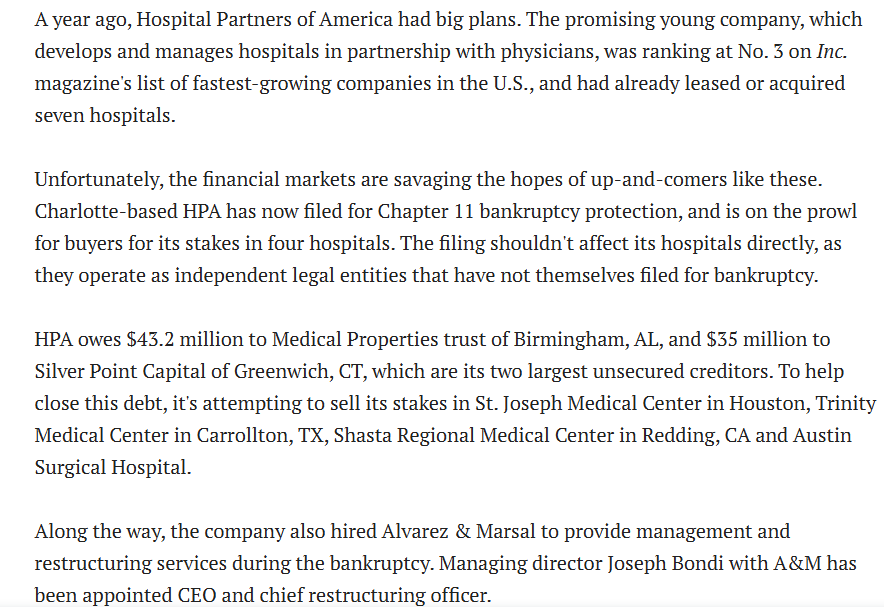

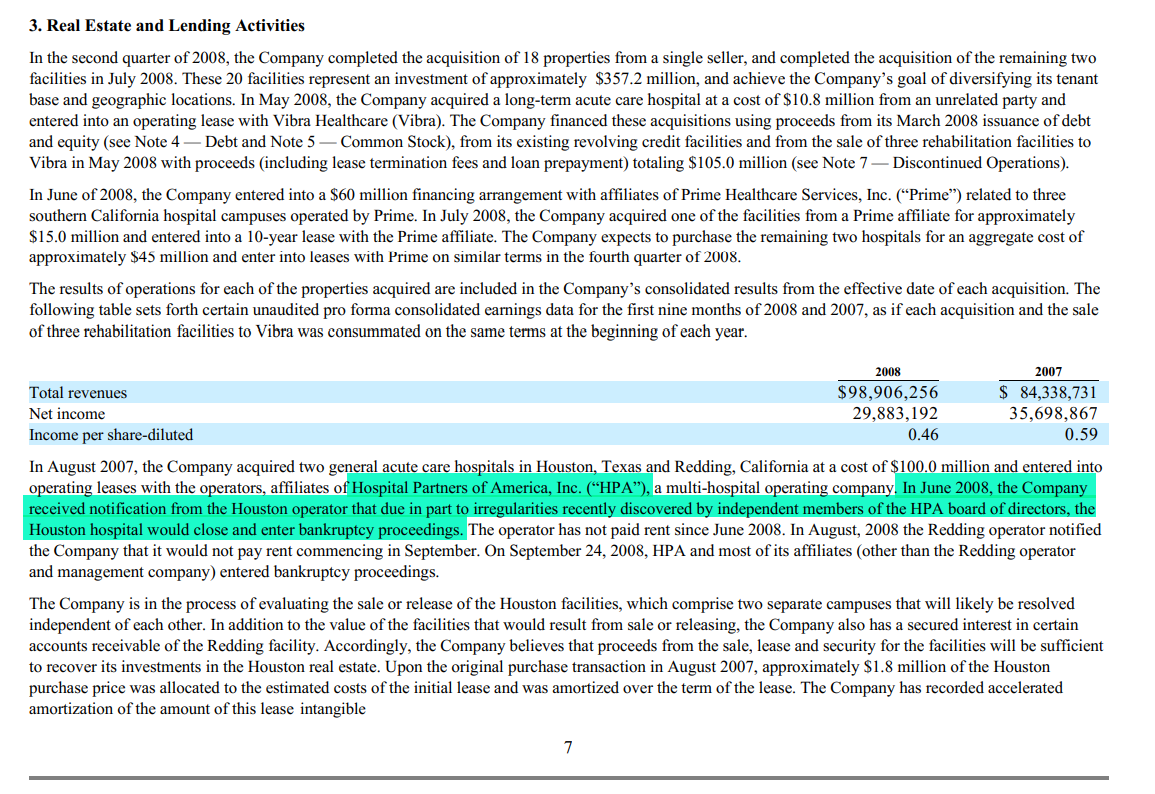

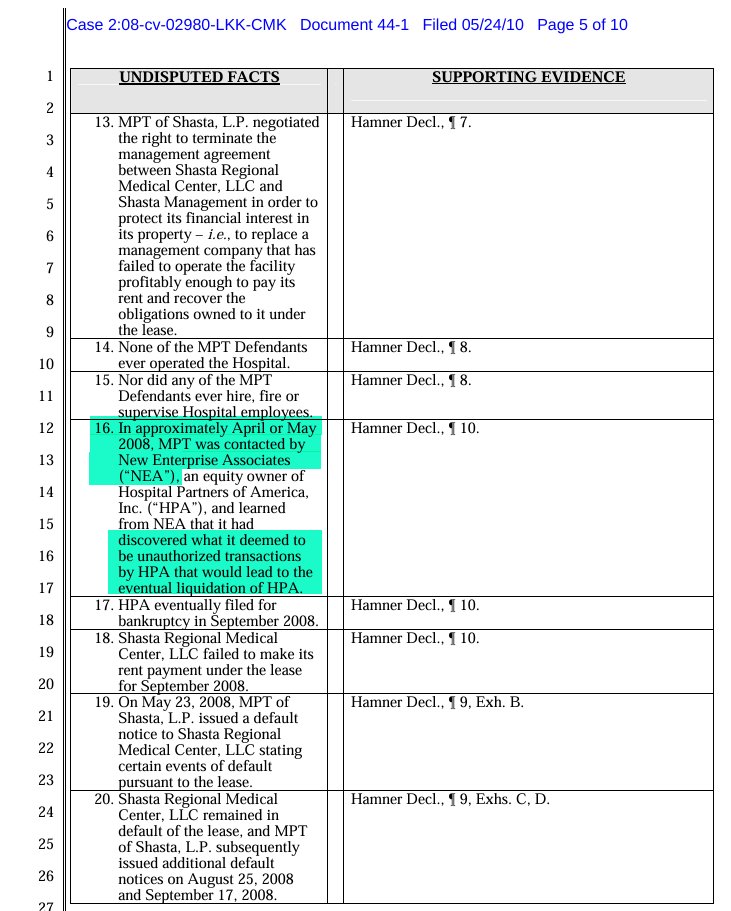

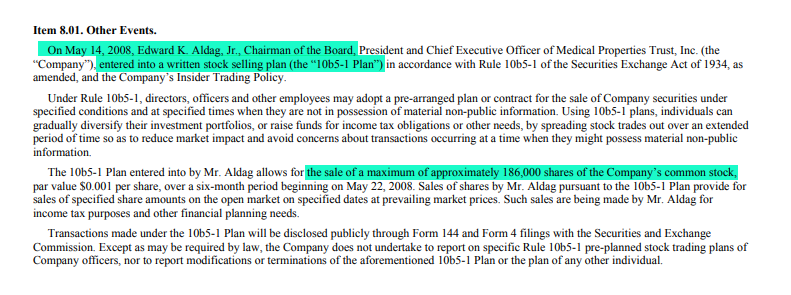

HPA was another MPT hospital operator fraud. One of several. MPT claimed in its Q3:08 10-Q filed with the SEC that it received notice of the fraud in June 2008. HPA later filed for BK in September 2008. Coincidentally, Silver Point Capital was the second largest HPA creditor behind MPT.

CFO Hamner claimed different timing under oath, saying MPT was notified in "approximately April or May 2008."

In between this timing "discrepancy," in mid-May 2008 CEO Aldag was able to file his first ever 10b5-1 to sell just under 15% of his shares. Shares were sold consistently through to the end of 2008.

Similar to how Aldag/Hamner got one more large stock sale off in April 2022, before the Prospect and Steward frauds blew up and destroyed untold shareholder wealth (along with their reputations). MPT made its first $75MM emergency WC loan advance to Steward on 12/4/22, and the first $50MM Tustin/Foothill "mortgage" advance on or about 3/5/22.

HPA was another MPT hospital operator fraud. One of several. MPT claimed in its Q3:08 10-Q filed with the SEC that it received notice of the fraud in June 2008. HPA later filed for BK in September 2008. Coincidentally, Silver Point Capital was the second largest HPA creditor behind MPT.

CFO Hamner claimed different timing under oath, saying MPT was notified in "approximately April or May 2008."

In between this timing "discrepancy," in mid-May 2008 CEO Aldag was able to file his first ever 10b5-1 to sell just under 15% of his shares. Shares were sold consistently through to the end of 2008.

Similar to how Aldag/Hamner got one more large stock sale off in April 2022, before the Prospect and Steward frauds blew up and destroyed untold shareholder wealth (along with their reputations). MPT made its first $75MM emergency WC loan advance to Steward on 12/4/22, and the first $50MM Tustin/Foothill "mortgage" advance on or about 3/5/22.

"MPT was here..." $MPW

Steward stopped paying "rent" altogether within 6-7 months of Aldag making these statements. A year later Steward filed for BK.

Utah was the only cash flow-positive market, from which funds were "swept" to subsidize all the losses elsewhere.

The SE Florida assets failed to sell in H2:23, were "no bid" in the BK, and are now run by disaster HSA (to which MPT has already lent approx. $62.5MM).

Steward stopped paying "rent" altogether within 6-7 months of Aldag making these statements. A year later Steward filed for BK.

Utah was the only cash flow-positive market, from which funds were "swept" to subsidize all the losses elsewhere.

The SE Florida assets failed to sell in H2:23, were "no bid" in the BK, and are now run by disaster HSA (to which MPT has already lent approx. $62.5MM).

"MPT was here..." $MPW

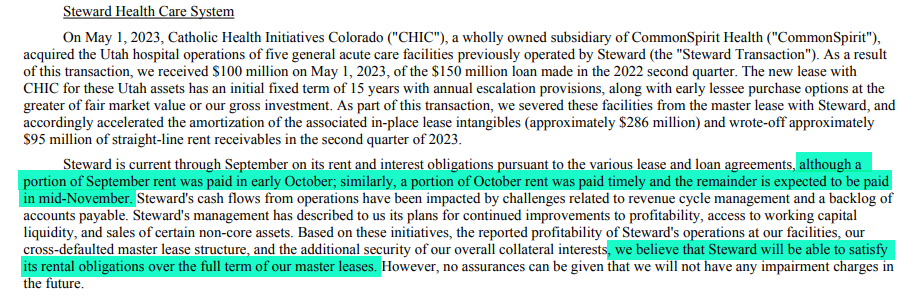

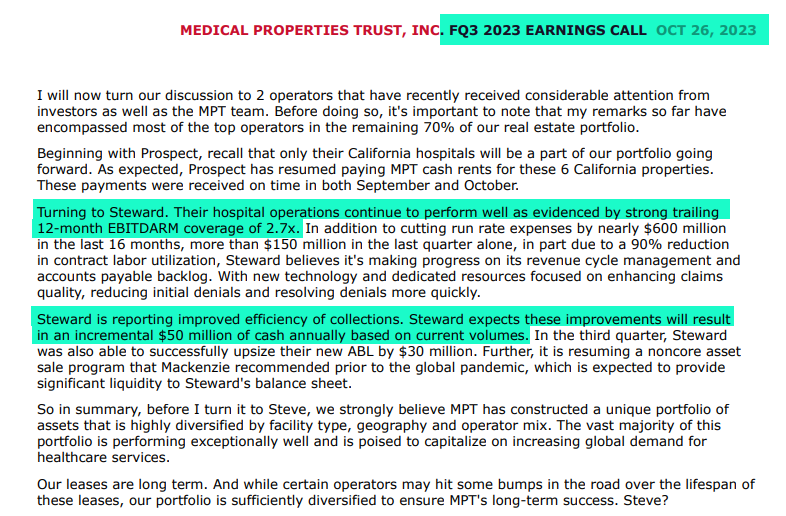

As Steward stopped paying "rent" (had it ever?), keep in mind that MPT management opted not to mention this on the Q3:23 earnings call held on 26/10/23.

Instead, it was "improving" and generating "strong coverage."

It was not until 2 weeks later in the Q3:23 10-Q that MPT alerted investors Steward was late on both September and October rent. Meanwhile both Steward and MPT would continue their online disinformation campaigns, utilize spy firms to attempt to intimidate critics, and CREF would continue pulling money out.

Steward would file for Ch. 11 within six months.

Clearly a credible management team worth of investors' trust...

As Steward stopped paying "rent" (had it ever?), keep in mind that MPT management opted not to mention this on the Q3:23 earnings call held on 26/10/23.

Instead, it was "improving" and generating "strong coverage."

It was not until 2 weeks later in the Q3:23 10-Q that MPT alerted investors Steward was late on both September and October rent. Meanwhile both Steward and MPT would continue their online disinformation campaigns, utilize spy firms to attempt to intimidate critics, and CREF would continue pulling money out.

Steward would file for Ch. 11 within six months.

Clearly a credible management team worth of investors' trust...

"MPT was here..." $MPW

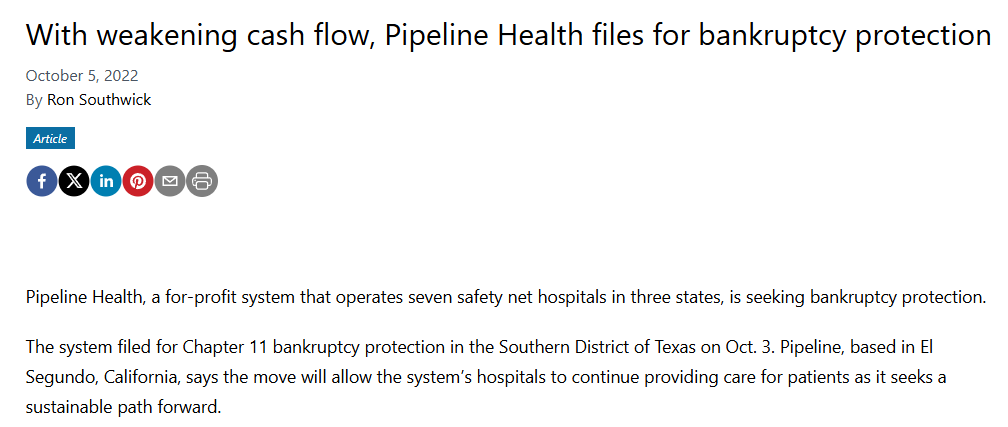

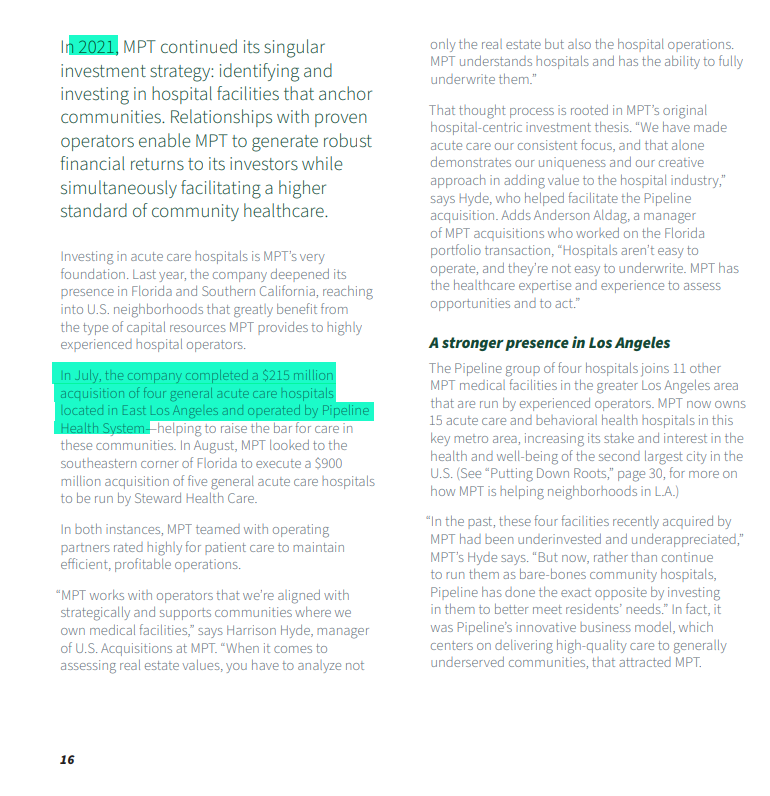

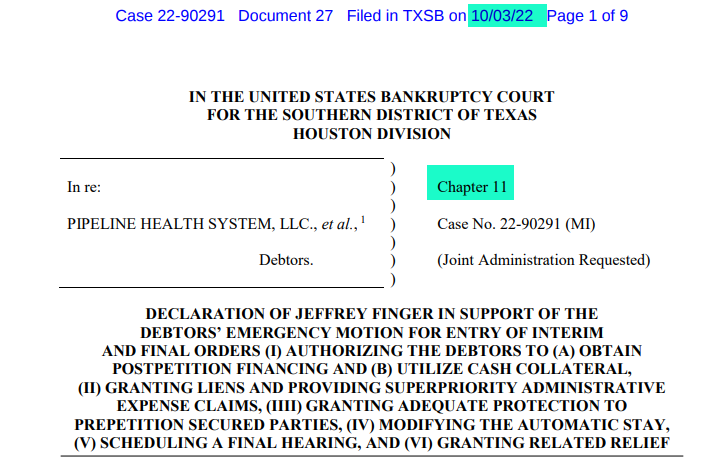

The MPT acquisitions department underwrote the $220MM acquisition of Pipeline Health's CA hospitals in July 2021.

It filed for Ch. 11 BK protection just over a year later. One year.

At the time of the filing, again just one year later, the CA hospitals were generating less than $3MM of facility-level EBITDAR against $18MM of annual cash rent.

The deposit still has not been released for repayment of deferred rent as of 31/12/24, which was not consistent with the plan.

The MPT acquisitions department underwrote the $220MM acquisition of Pipeline Health's CA hospitals in July 2021.

It filed for Ch. 11 BK protection just over a year later. One year.

At the time of the filing, again just one year later, the CA hospitals were generating less than $3MM of facility-level EBITDAR against $18MM of annual cash rent.

The deposit still has not been released for repayment of deferred rent as of 31/12/24, which was not consistent with the plan.

"MPT was here..." $MPW

"MPT was here..." $MPW

In May 2020, as part of the "Project Easter" recap of an insolvent Steward, MPT:

- removed Cerberus as owner (and in the process relieved this third-party of any "fraudulent conveyance" concerns using MPT shareholder capital; why did they have these concerns if Steward was financially healthy?),

- "acquired a substantial equity interest in Steward operations" after several attempts despite being a REIT, and

- infused said insolvent tenant with $400MM of working capital, rather than restructuring the leases.

To arrive at the $350MM "value" of this interest in Steward, MPT applied EBITDA multiples of select publicly-traded and better capitalized hospital operators ( $HCA, $UHS, $THC) to Steward's EBITDAR.

In other words, a capital structure-affected trading metric (via leases, which are financial leverage) was applied to Steward's capital structure-neutral/independent earnings, which were heavily burdened by MPT's unaffordable leases. So "apples-to-oranges" and arbitrary "cherry-picking."

MPT management and the BoD either are financially illiterate, violating basic principles of corporate finance, or deliberately fraudulent and misleading. The latter is much more likely. They are not stupid.

In May 2020, as part of the "Project Easter" recap of an insolvent Steward, MPT:

- removed Cerberus as owner (and in the process relieved this third-party of any "fraudulent conveyance" concerns using MPT shareholder capital; why did they have these concerns if Steward was financially healthy?),

- "acquired a substantial equity interest in Steward operations" after several attempts despite being a REIT, and

- infused said insolvent tenant with $400MM of working capital, rather than restructuring the leases.

To arrive at the $350MM "value" of this interest in Steward, MPT applied EBITDA multiples of select publicly-traded and better capitalized hospital operators ( $HCA, $UHS, $THC) to Steward's EBITDAR.

In other words, a capital structure-affected trading metric (via leases, which are financial leverage) was applied to Steward's capital structure-neutral/independent earnings, which were heavily burdened by MPT's unaffordable leases. So "apples-to-oranges" and arbitrary "cherry-picking."

MPT management and the BoD either are financially illiterate, violating basic principles of corporate finance, or deliberately fraudulent and misleading. The latter is much more likely. They are not stupid.

"MPT was here..."

Rather "is here..." $MPW

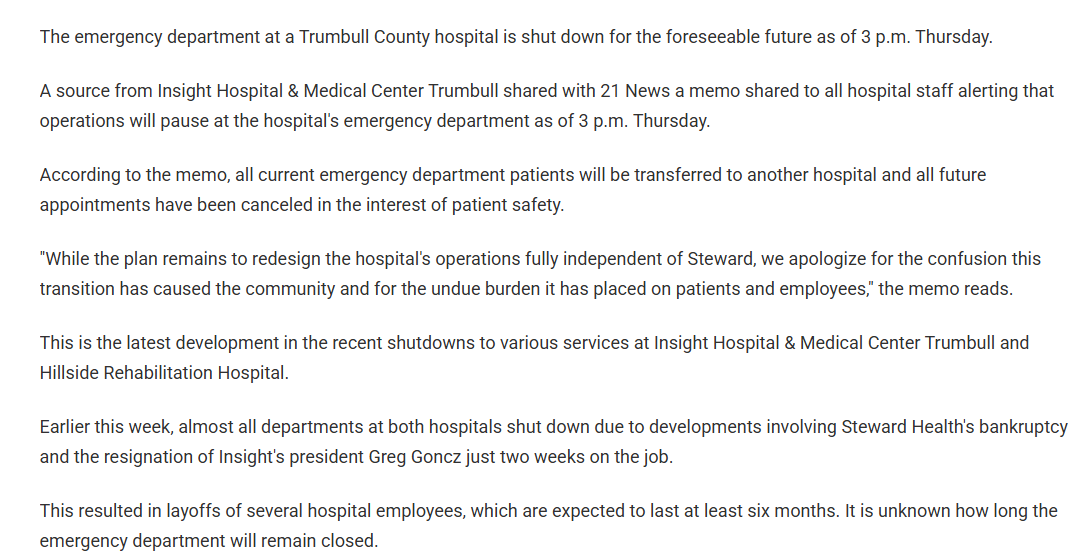

Trumbull CEO resigns after just two weeks. Trumbull run by "quality operator" Insight, which is pausing almost all inpatient/outpatient.

wfmj.com/story/52615154…

Rather "is here..." $MPW

Trumbull CEO resigns after just two weeks. Trumbull run by "quality operator" Insight, which is pausing almost all inpatient/outpatient.

wfmj.com/story/52615154…

"MPT was here..." $MPW

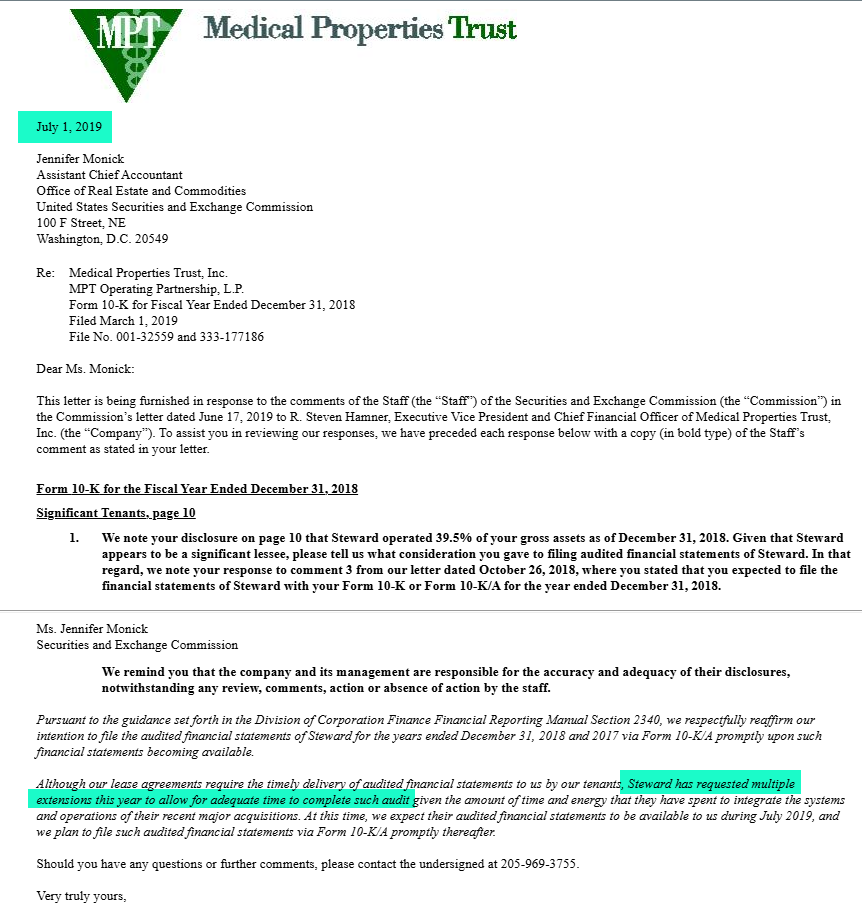

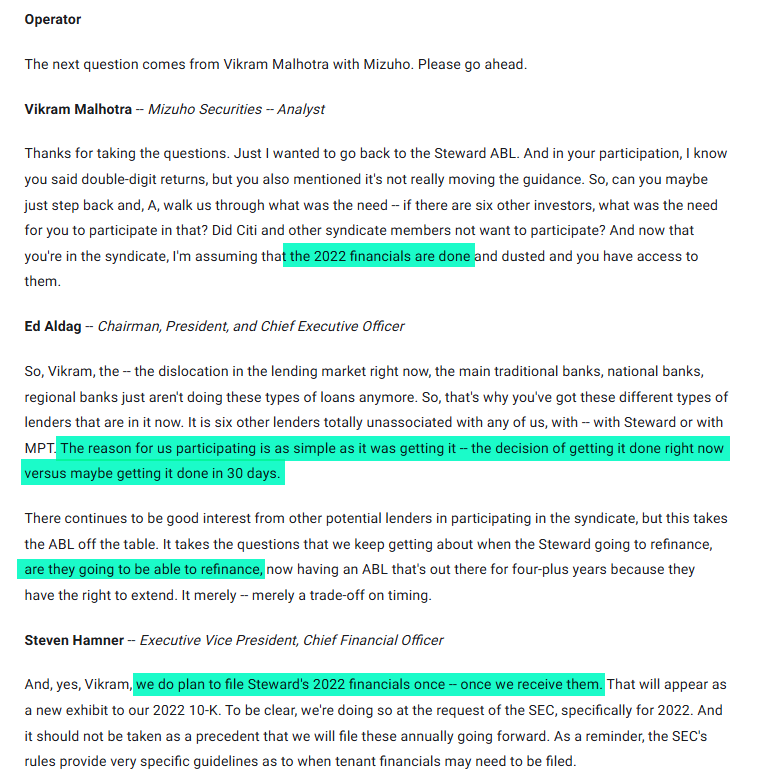

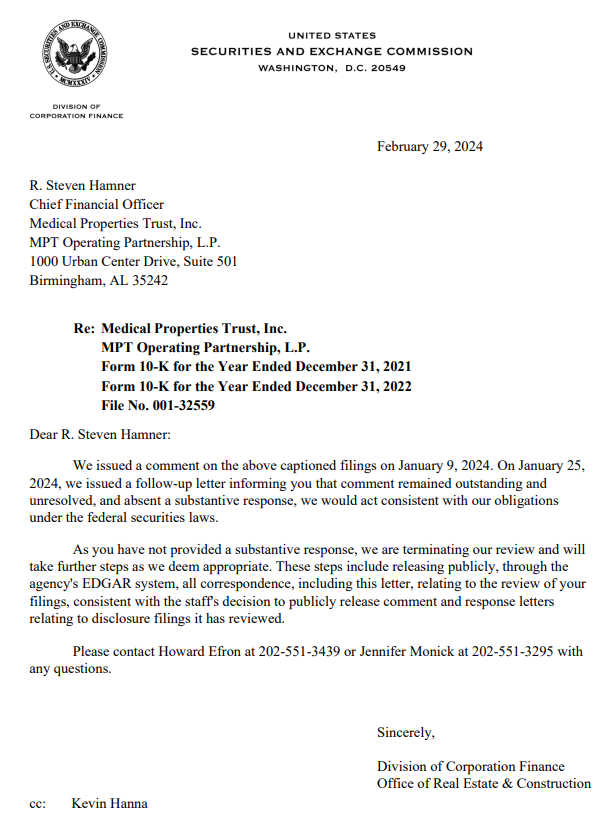

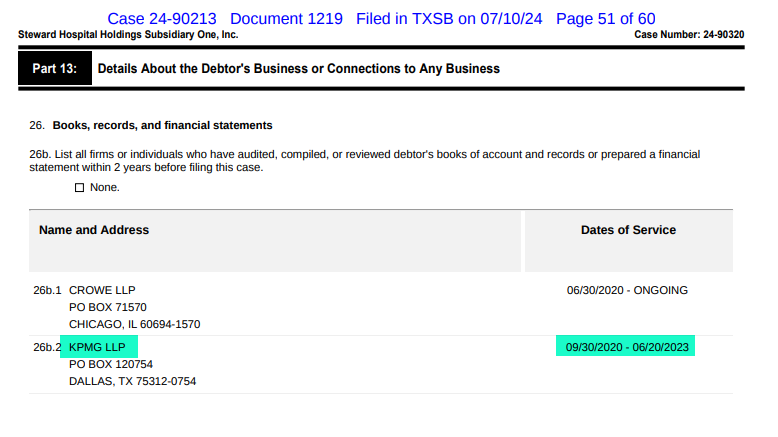

EY was Steward's auditor until late-2020 following "Project Easter." EY was delayed in completing the 2019 Steward audit prior to that. EY quit and KPMG took over for 2020.

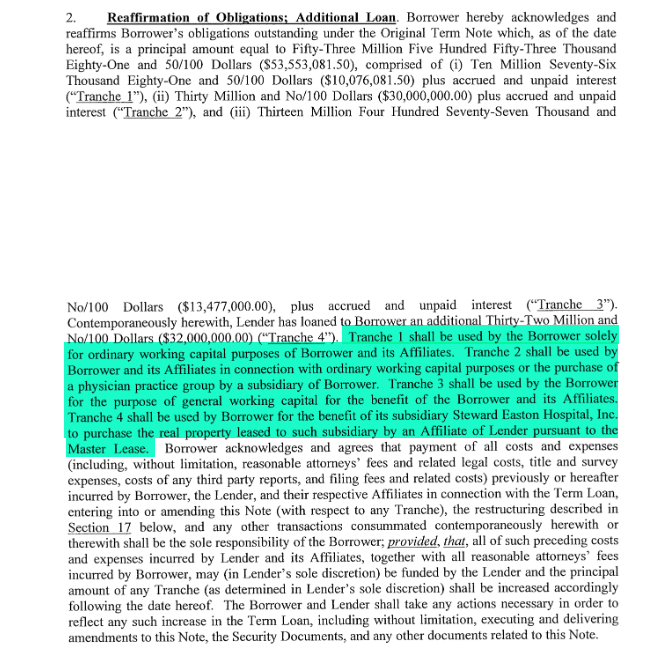

In late-2022 the delayed Steward 2021 audit by KPMG interfered with refinancing of Steward's ABL, leading to just a 1-year extension. MPT claimed a "lease accounting issue" and that "all of the bad at Steward in the past." Meanwhile, hundreds of millions of unpaid vendor $ piled up. Meanwhile, MPT lent Steward $28MM via Tranche 6 + >$100MM in "MPT advances." MPT management lied about making Tranche 6. MPT had already lent $150MM via Tranche 5.

KPMG then apparently quit in June 2023 and Crowe took over. MPT never alerted anyone to this fact, and meanwhile told both analysts (and the SEC) they intended to file the financials upon receiving them. Never happened. MPT said Steward "improving" and "performing well."

Three audit firms in three years at Steward. MPT management always telling investors that Steward improving. MPT management stonewalling the SEC. MPT loaning money to Steward for WC and deferring rent throughout. Steward insolvent the entire time.

Were the 2023 ABL lenders told about KPMG quitting, or were they defrauded as well?

EY was Steward's auditor until late-2020 following "Project Easter." EY was delayed in completing the 2019 Steward audit prior to that. EY quit and KPMG took over for 2020.

In late-2022 the delayed Steward 2021 audit by KPMG interfered with refinancing of Steward's ABL, leading to just a 1-year extension. MPT claimed a "lease accounting issue" and that "all of the bad at Steward in the past." Meanwhile, hundreds of millions of unpaid vendor $ piled up. Meanwhile, MPT lent Steward $28MM via Tranche 6 + >$100MM in "MPT advances." MPT management lied about making Tranche 6. MPT had already lent $150MM via Tranche 5.

KPMG then apparently quit in June 2023 and Crowe took over. MPT never alerted anyone to this fact, and meanwhile told both analysts (and the SEC) they intended to file the financials upon receiving them. Never happened. MPT said Steward "improving" and "performing well."

Three audit firms in three years at Steward. MPT management always telling investors that Steward improving. MPT management stonewalling the SEC. MPT loaning money to Steward for WC and deferring rent throughout. Steward insolvent the entire time.

Were the 2023 ABL lenders told about KPMG quitting, or were they defrauded as well?

"MPT was here..." $MPW

Rents originally set by MPT via 2019 SLB. Assets sold in 2023 to new landlord facilitated by rent cut + CAPX commitments/rate cap purchase by MPT. MPT levered portfolio up 100% and lost money all in vs. its gross cost.

Tenant bust within 5 years of original SLB. New landlord cuts distribution.

Caveat emptor.

afr.com/life-and-luxur…

afr.com/property/comme…

Rents originally set by MPT via 2019 SLB. Assets sold in 2023 to new landlord facilitated by rent cut + CAPX commitments/rate cap purchase by MPT. MPT levered portfolio up 100% and lost money all in vs. its gross cost.

Tenant bust within 5 years of original SLB. New landlord cuts distribution.

Caveat emptor.

afr.com/life-and-luxur…

afr.com/property/comme…

"MPT was here..." $MPW

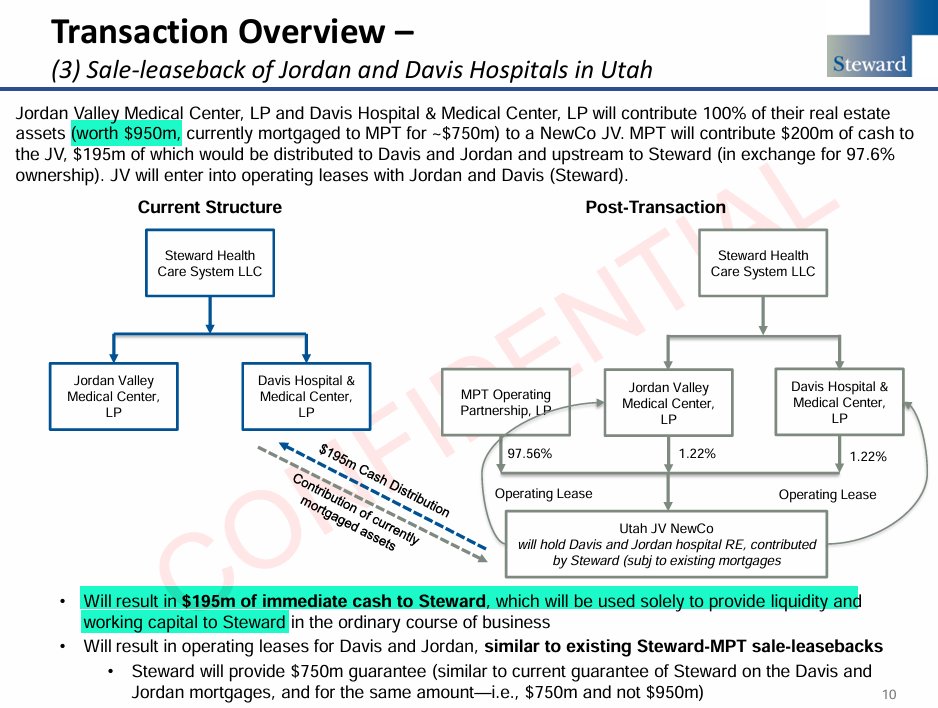

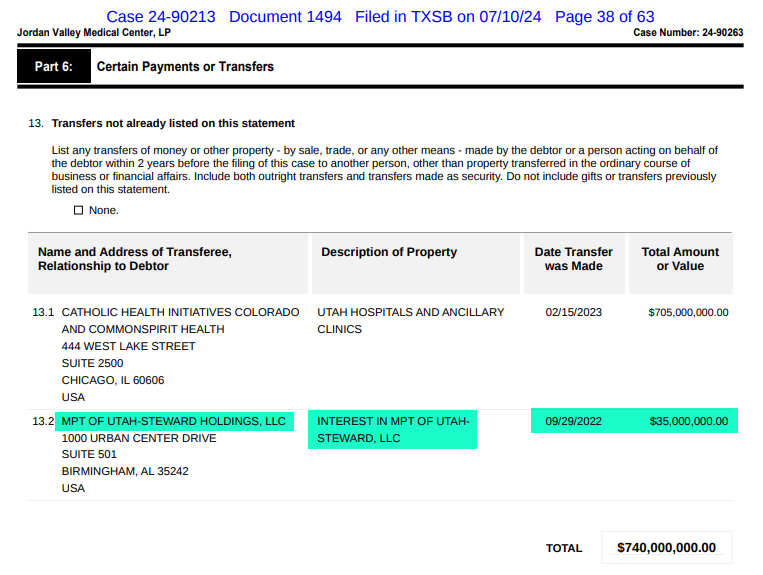

Which line item in MPT's Q3:22 statement of cash flows contains the $35MM purchase of the approx. 2.44% interest in "Utah JV NewCo"/MPT of Utah-Steward, LLC PropCo JV that MPT did not own. This PropCo entity sold in early-2024 for much less than this implied $1.5BN gross valuation.

This $35MM equaled approx. 50% of the qtrly. ML1 rent due to MPT at the time. Apparently it must have been approved by MPT's BoD in late-Q3:22 and paid to Steward on 29/9/22.

Why didn't MPT disclose this "loan" to its largest tenant? Why didn't Hamner mention this support, alongside the Tranche 5 loan below, when it was claimed on 27/10/22 that "Steward has weathered the cash strain?" Neither this $35MM nor the Tranche 5 loan were fully recovered.

This would make known 2022 support to Steward = $150MM Tranche 5 in Q2:22, this $35MM in Q3:22, $28MM Tranche 6 in Q4:22 and approx. $100MM "MPT advances" = approx. $313MM.

Vs. annual ML1 rent was ~$300MM at the time.

How is the MPT BoD also not complicit or implicated in the round-tripping/fraud? Both Hamner and Aldag sit on the BoD.

Which line item in MPT's Q3:22 statement of cash flows contains the $35MM purchase of the approx. 2.44% interest in "Utah JV NewCo"/MPT of Utah-Steward, LLC PropCo JV that MPT did not own. This PropCo entity sold in early-2024 for much less than this implied $1.5BN gross valuation.

This $35MM equaled approx. 50% of the qtrly. ML1 rent due to MPT at the time. Apparently it must have been approved by MPT's BoD in late-Q3:22 and paid to Steward on 29/9/22.

Why didn't MPT disclose this "loan" to its largest tenant? Why didn't Hamner mention this support, alongside the Tranche 5 loan below, when it was claimed on 27/10/22 that "Steward has weathered the cash strain?" Neither this $35MM nor the Tranche 5 loan were fully recovered.

This would make known 2022 support to Steward = $150MM Tranche 5 in Q2:22, this $35MM in Q3:22, $28MM Tranche 6 in Q4:22 and approx. $100MM "MPT advances" = approx. $313MM.

Vs. annual ML1 rent was ~$300MM at the time.

How is the MPT BoD also not complicit or implicated in the round-tripping/fraud? Both Hamner and Aldag sit on the BoD.

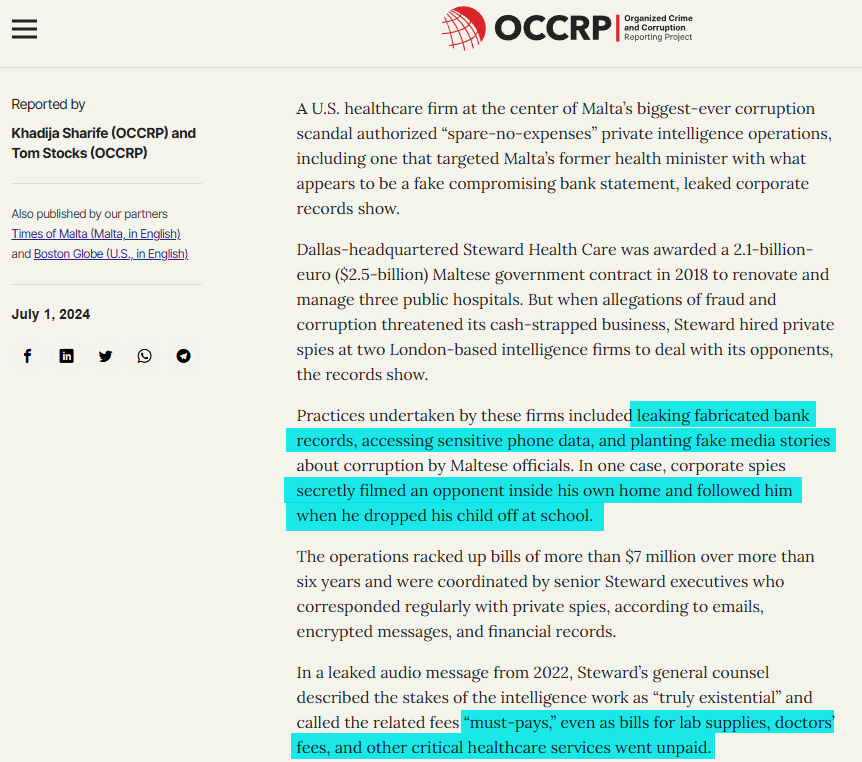

"MPT was here..." $MPW

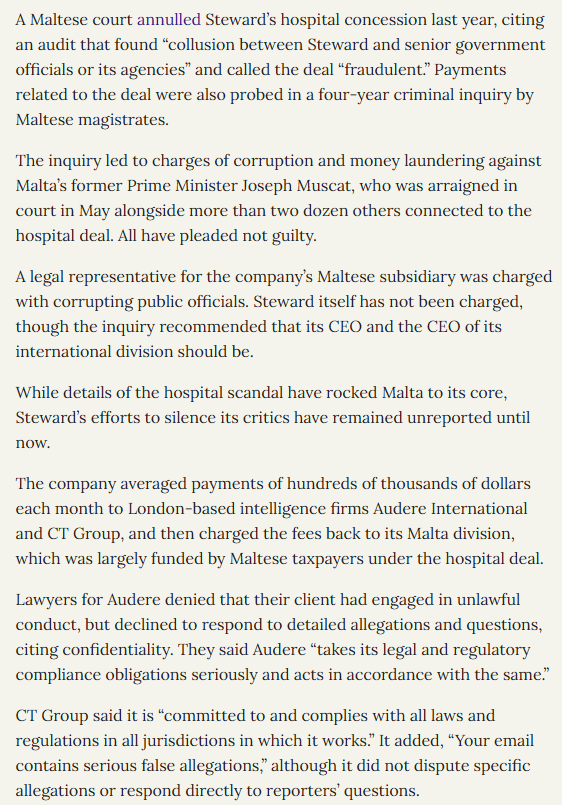

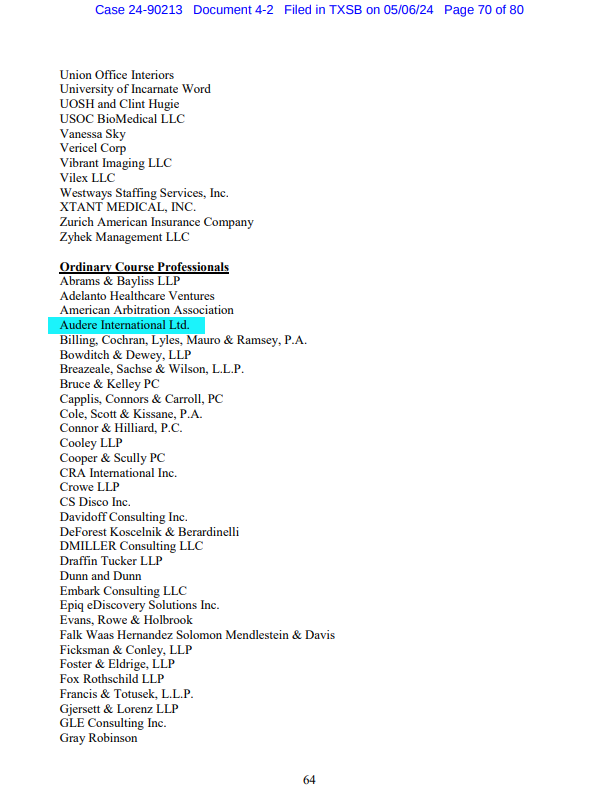

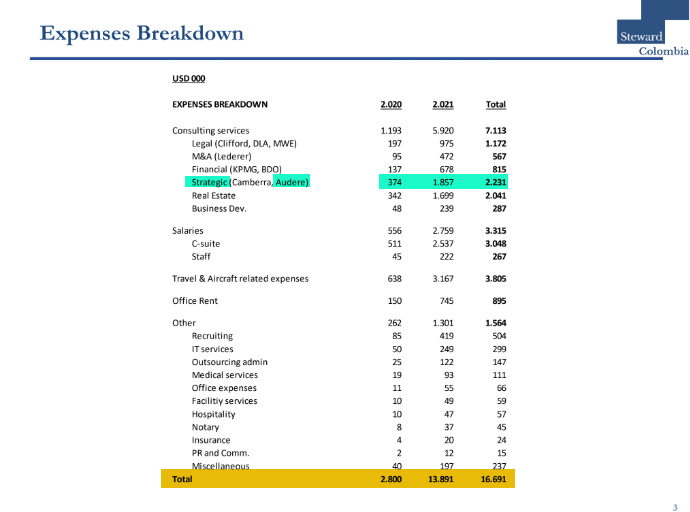

MPT admitted it hired same spy firm as largest tenant SHCS in October 2022. The "Audere Report" was prepared for MPT management in late-2022.

Work performed by Audere for Steward included, without limitation, fabricating bank records, inventing fake stories, following/filming opponents, conducting "false flag" operations and online impersonation/harassment.

MPT claims "no cost sharing or cost shifting or reimbursement agreement with anyone..."

Oh really? How much of the Audere cost was passed through the "International Joint Venture," since its formation in mid-2020? In which MPT maintained a 49% equity stake.

Quote from OCCRP: The company averaged payments of hundreds of thousands of dollars each month to London-based intelligence firms Audere International and CT Group, and then charged the fees back to its Malta division, which was largely funded by Maltese taxpayers under the hospital deal.

"Taking the high road" and "at the very heart of healthcare!"

Reference: occrp.org/en/investigati…

MPT admitted it hired same spy firm as largest tenant SHCS in October 2022. The "Audere Report" was prepared for MPT management in late-2022.

Work performed by Audere for Steward included, without limitation, fabricating bank records, inventing fake stories, following/filming opponents, conducting "false flag" operations and online impersonation/harassment.

MPT claims "no cost sharing or cost shifting or reimbursement agreement with anyone..."

Oh really? How much of the Audere cost was passed through the "International Joint Venture," since its formation in mid-2020? In which MPT maintained a 49% equity stake.

Quote from OCCRP: The company averaged payments of hundreds of thousands of dollars each month to London-based intelligence firms Audere International and CT Group, and then charged the fees back to its Malta division, which was largely funded by Maltese taxpayers under the hospital deal.

"Taking the high road" and "at the very heart of healthcare!"

Reference: occrp.org/en/investigati…

"MPT was here..." $MPW

Correction, "MPT is here..." As is "quality operator" Insight.

Reference: wfmj.com/story/52634609…

Correction, "MPT is here..." As is "quality operator" Insight.

Reference: wfmj.com/story/52634609…

"MPT was here..." $MPW

Actually "MPT is here..."

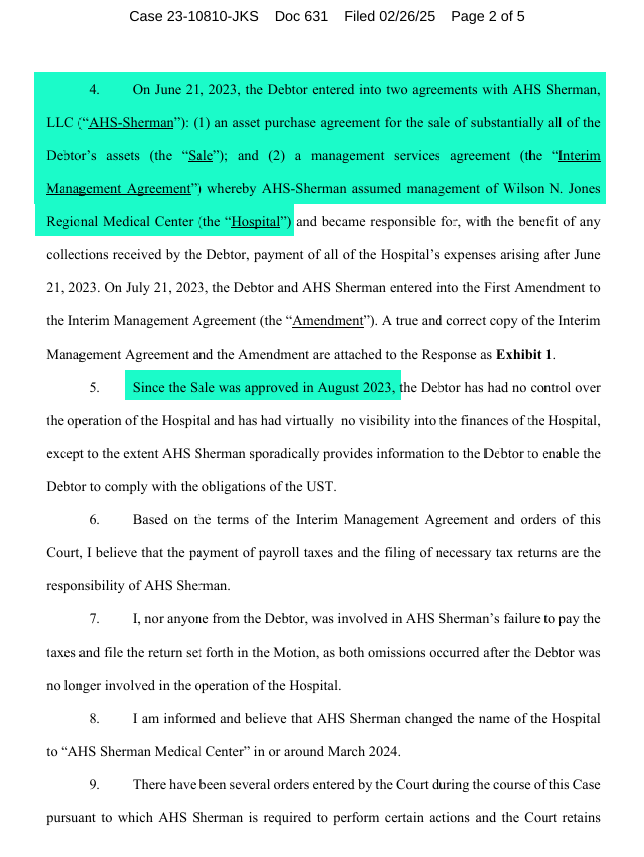

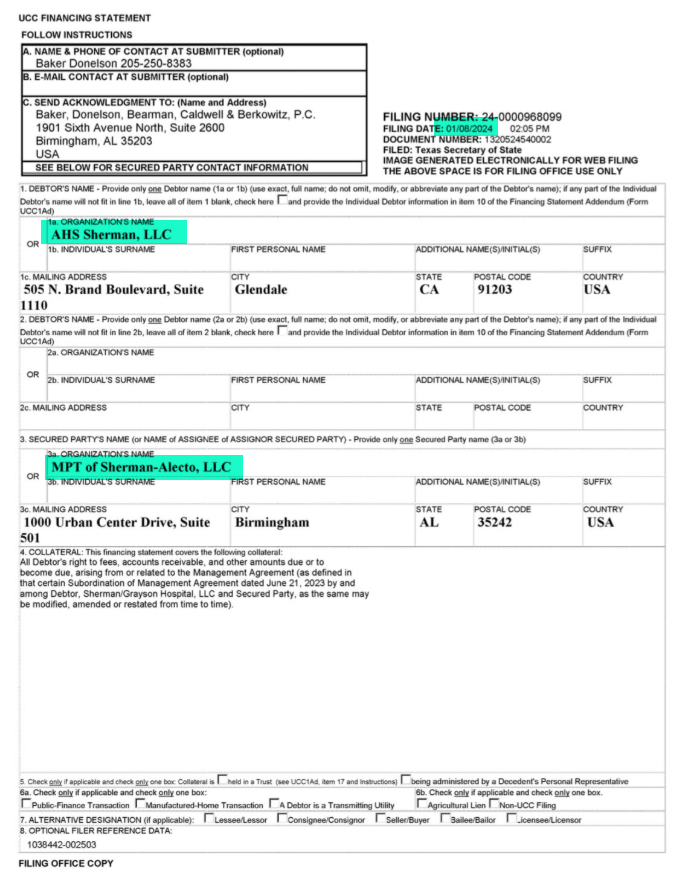

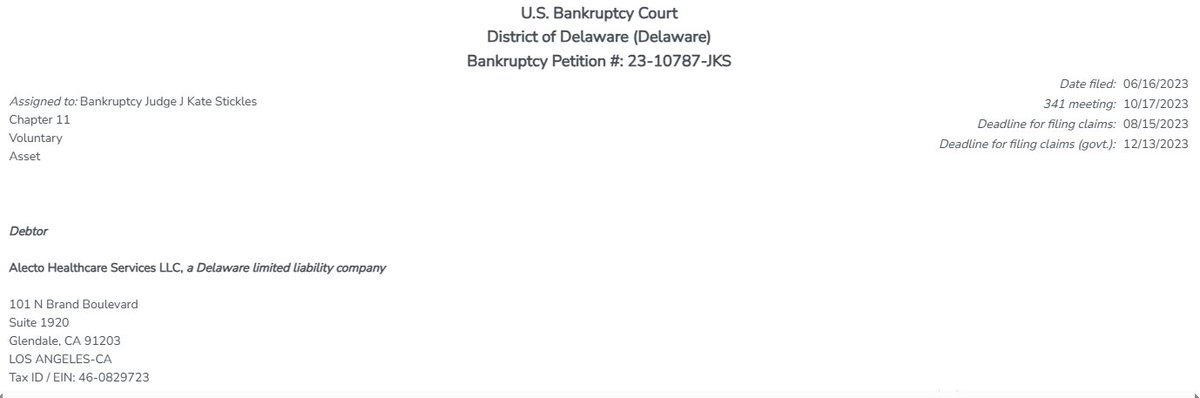

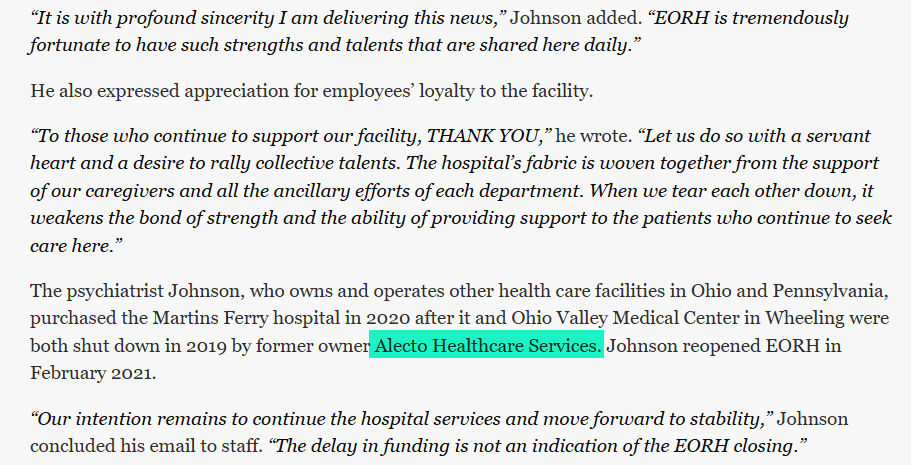

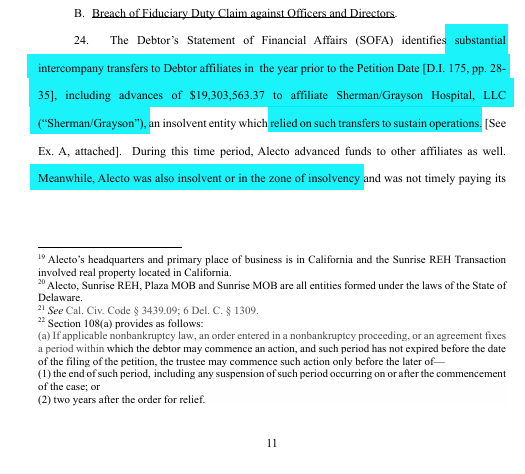

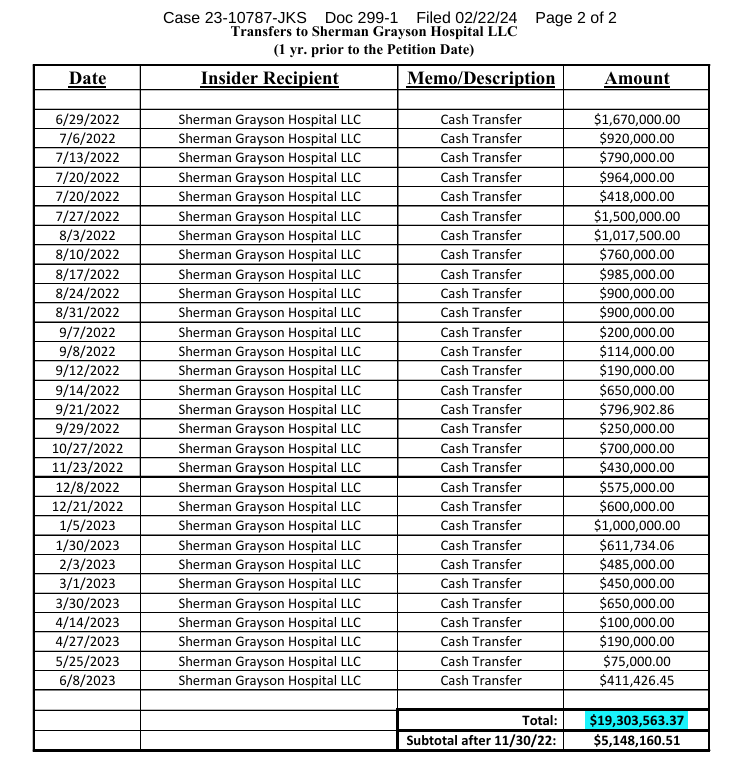

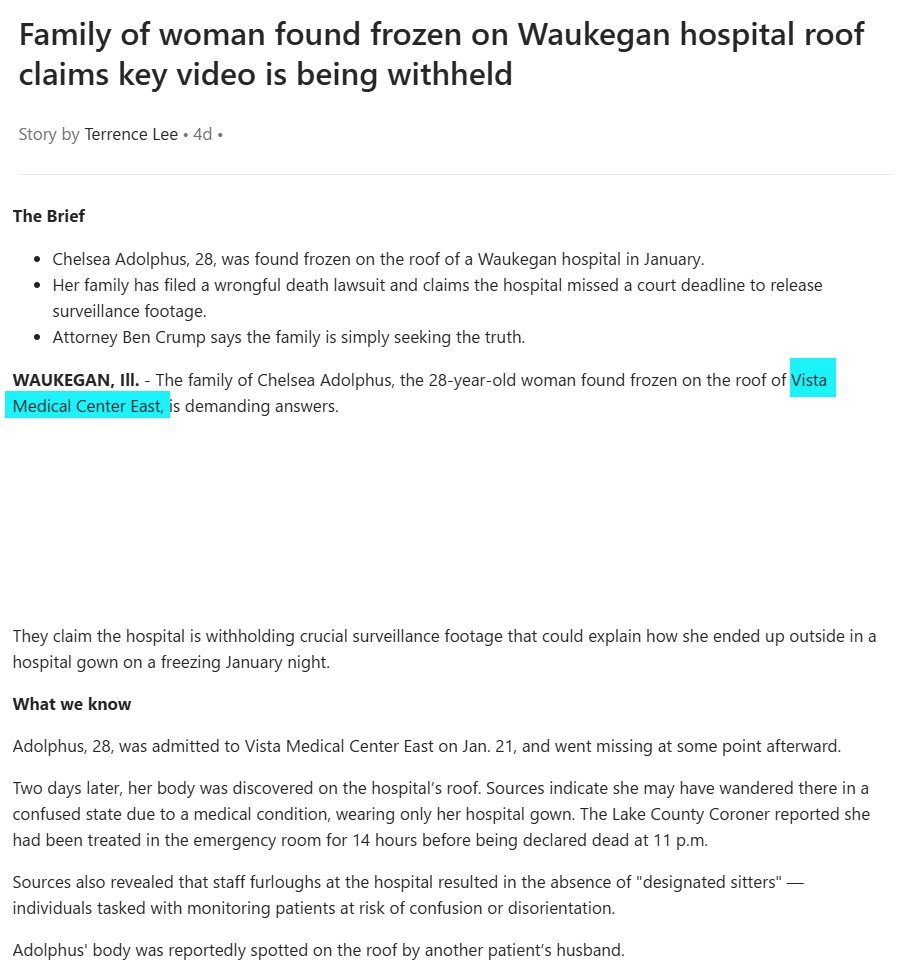

AHS (or is it MPT "quality operator" HSA?) took over operations of MPT-owned Wilson Jones (Sherman/Grayson Hospital, LLC) from bankrupt Alecto in 2023. Alecto was one of the original fraudulent progeny of "OG" MPT operator Prime, to be followed later by HSA/AHS.

Pre-Alecto petition there were $19MM of arguably fraudulent transfers out of an insolvent Alecto to "sustain operations" of Alecto Sherman during 2022.

Since HSA/AHS took over the hospital, it has transferred funds out of Vista MC East in Waukegan, IL (not MPT-owned), also to sustain operations of an insolvent/uneconomic MPT-owned hospital in Sherman.

Vista East lost its trauma center designation for a time in 2024, and now... things aren't great.

"Quality operator" HSA/AHS operates $1.3BN GBV of former Steward hospitals.

Actually "MPT is here..."

AHS (or is it MPT "quality operator" HSA?) took over operations of MPT-owned Wilson Jones (Sherman/Grayson Hospital, LLC) from bankrupt Alecto in 2023. Alecto was one of the original fraudulent progeny of "OG" MPT operator Prime, to be followed later by HSA/AHS.

Pre-Alecto petition there were $19MM of arguably fraudulent transfers out of an insolvent Alecto to "sustain operations" of Alecto Sherman during 2022.

Since HSA/AHS took over the hospital, it has transferred funds out of Vista MC East in Waukegan, IL (not MPT-owned), also to sustain operations of an insolvent/uneconomic MPT-owned hospital in Sherman.

Vista East lost its trauma center designation for a time in 2024, and now... things aren't great.

"Quality operator" HSA/AHS operates $1.3BN GBV of former Steward hospitals.

"MPT was here..." $MPW

Except "MPT is here!"

One wonders if Trumbull employees consider Insight Health to be a "quality operator," when they aren't receiving their paychecks...

References: wfmj.com/clip/15505836/…

wfmj.com/story/52640004…

Except "MPT is here!"

One wonders if Trumbull employees consider Insight Health to be a "quality operator," when they aren't receiving their paychecks...

References: wfmj.com/clip/15505836/…

wfmj.com/story/52640004…

"MPT was here..." $MPW

How did this claim work out? Twice in the past two years with its largest U.S. tenants, MPT was forced to subordinate its claims. Twice it provided "junior DIPs." Twice it actually was compelled to negotiate. Twice it took MASSIVE losses.

If you have limited liquidity, you cannot lend to operators endlessly or control sizeable DIPs. If your rents are dramatically above-market and unaffordable, you cannot compel new operators to assume those leases.

And if you commit blatant fraud, you lose all of your leverage...

How did this claim work out? Twice in the past two years with its largest U.S. tenants, MPT was forced to subordinate its claims. Twice it provided "junior DIPs." Twice it actually was compelled to negotiate. Twice it took MASSIVE losses.

If you have limited liquidity, you cannot lend to operators endlessly or control sizeable DIPs. If your rents are dramatically above-market and unaffordable, you cannot compel new operators to assume those leases.

And if you commit blatant fraud, you lose all of your leverage...

"MPT was here..." $MPW

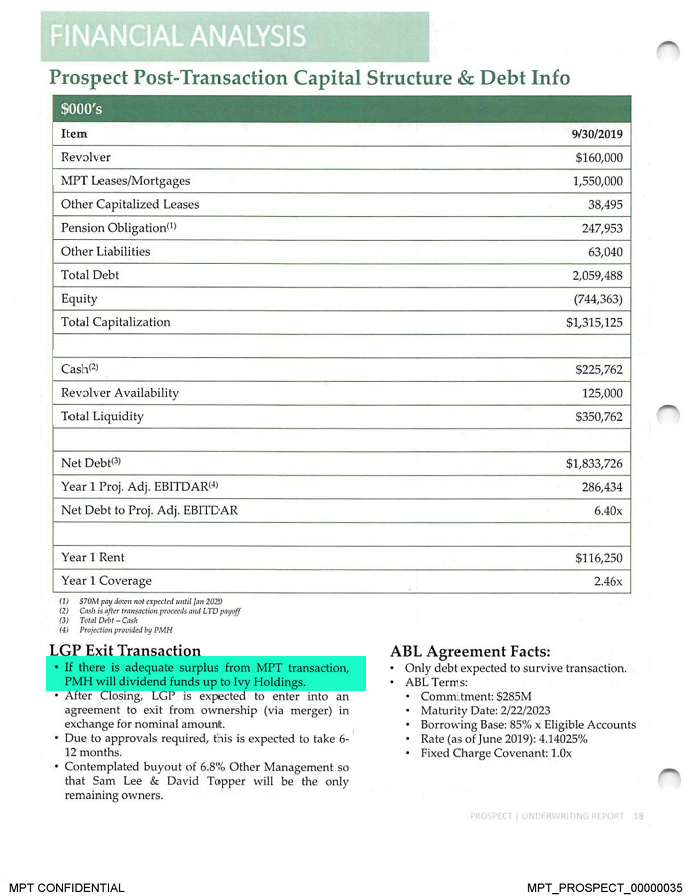

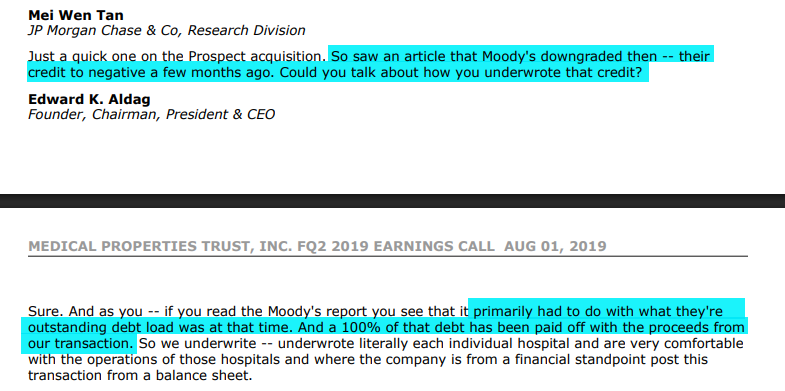

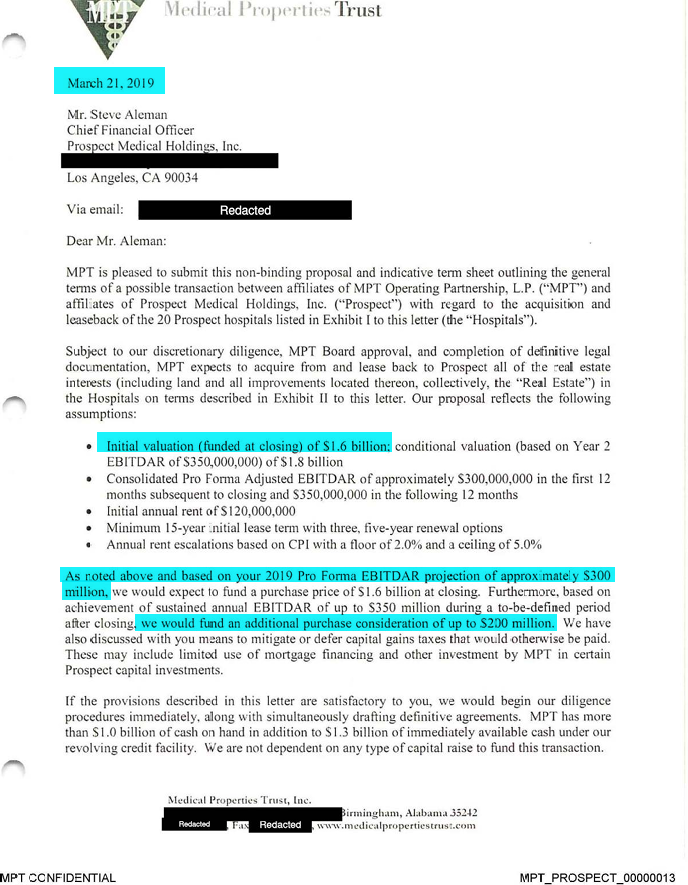

Why would MPT invest in a company with these results? Well, in the case of Prospect, MPT did it anyway after demonstrating the"strength of underwriting the real estate."

- First Aldag dropped an all-timer, admitting on the Q2:19 earnings call that MPT was taking the credit risk (that had just caused a Moody's DG) onto MPT's balance sheet,

- Hamner on 21/3/19 showed an early willingness to fund the operator later/act as a private equity sponsor with a potential "earnout" of $200MM (from a landlord to a triple-net tenant?),

- The same memo predicated an already-inflated valuation on PF 2019 EBITDAR of $300MM,

- MPT's own underwriting report and projections from 23/8/19 showed that Prospect was missing that $300MM target (hint: it would never get there!), and then

- MPT funded the $1.6BN anyway!

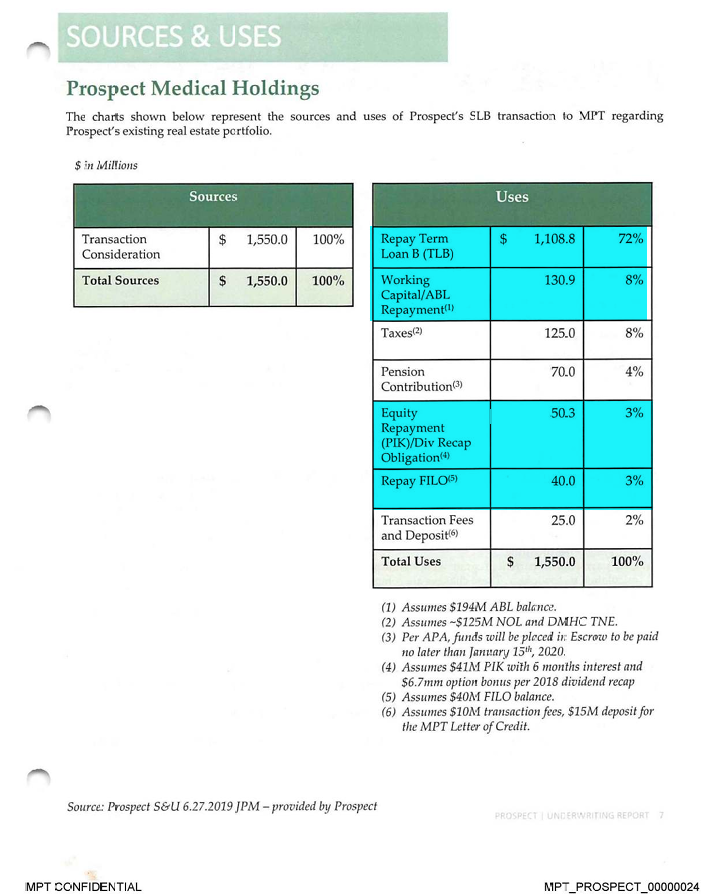

Included in that $1.6BN was repaying recent Prospect dividend recap debt, infusing Prospect with work capital equal to >1 year of rent + interest and repaying the Lee/Topper emergency loans from early-2019.

And if that were not enough, MPT funded Prospect's transaction fees/expenses on top!

Why would MPT invest in a company with these results? Well, in the case of Prospect, MPT did it anyway after demonstrating the"strength of underwriting the real estate."

- First Aldag dropped an all-timer, admitting on the Q2:19 earnings call that MPT was taking the credit risk (that had just caused a Moody's DG) onto MPT's balance sheet,

- Hamner on 21/3/19 showed an early willingness to fund the operator later/act as a private equity sponsor with a potential "earnout" of $200MM (from a landlord to a triple-net tenant?),

- The same memo predicated an already-inflated valuation on PF 2019 EBITDAR of $300MM,

- MPT's own underwriting report and projections from 23/8/19 showed that Prospect was missing that $300MM target (hint: it would never get there!), and then

- MPT funded the $1.6BN anyway!

Included in that $1.6BN was repaying recent Prospect dividend recap debt, infusing Prospect with work capital equal to >1 year of rent + interest and repaying the Lee/Topper emergency loans from early-2019.

And if that were not enough, MPT funded Prospect's transaction fees/expenses on top!

"MPT was here..." $MPW

Actually "MPT is here."

And then MPT will not be in that HQ building much longer, assuming it gets done wasting capital on the new $150MM+ HQ down the street.

Reference: wsj.com/articles/ohio-…

Actually "MPT is here."

And then MPT will not be in that HQ building much longer, assuming it gets done wasting capital on the new $150MM+ HQ down the street.

Reference: wsj.com/articles/ohio-…

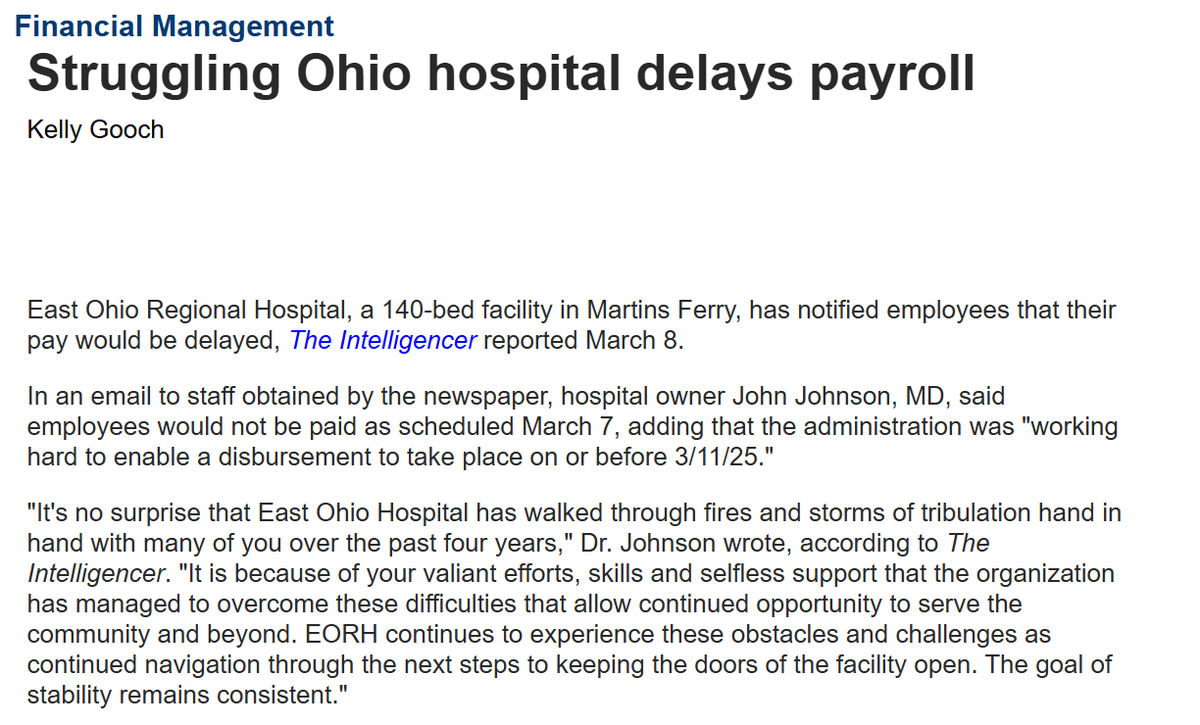

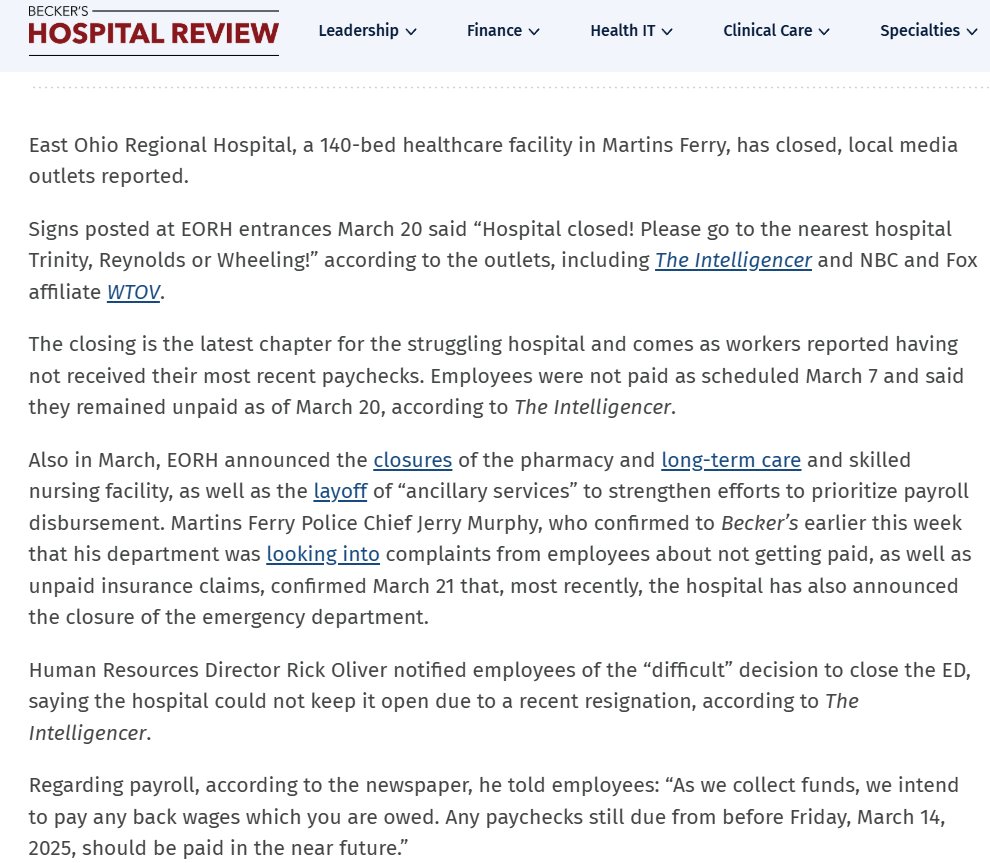

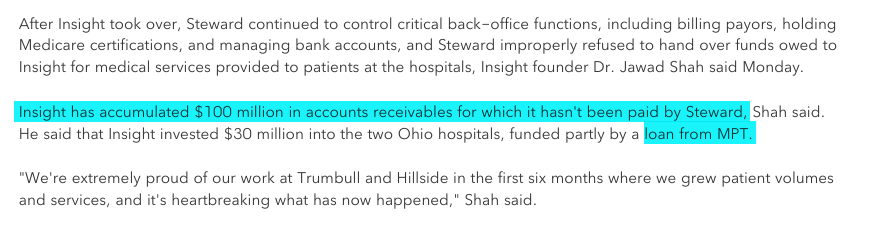

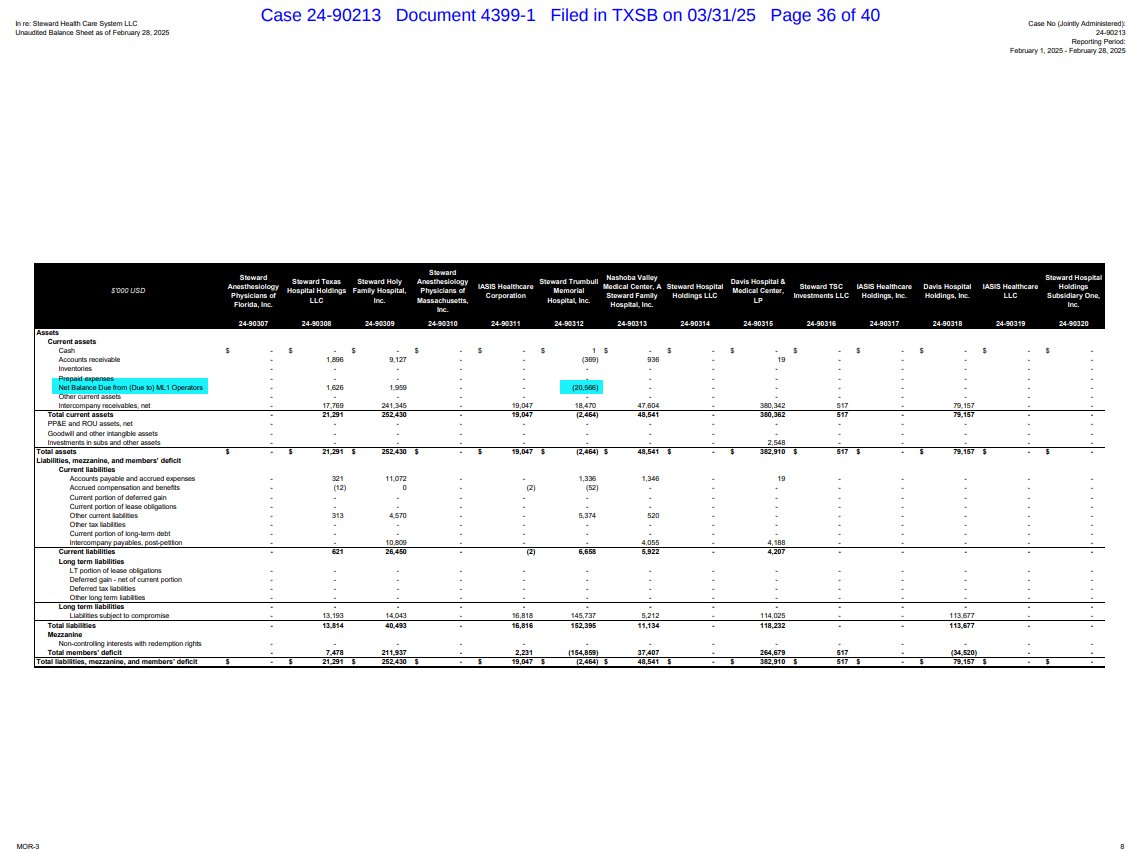

MPT "quality operator" Insight founder Shah claimed in article $100MM A/R due from Steward related to TSA.

But Steward's Feb. MOR shows just $21MM due to new ML1 operators, nowhere near the claimed shortfall.

MPT already loaning to Insight, and not repaid as of 31/12/24. How much more will MPT need to fund, on top of the disaster at fellow "quality operator" AHS/HSA?

Meanwhile two more hospitals close, more patients suffer and more employees don't receive their paychecks... all so that MPT can pretend its assets have not massively declined in value. $MPW

But Steward's Feb. MOR shows just $21MM due to new ML1 operators, nowhere near the claimed shortfall.

MPT already loaning to Insight, and not repaid as of 31/12/24. How much more will MPT need to fund, on top of the disaster at fellow "quality operator" AHS/HSA?

Meanwhile two more hospitals close, more patients suffer and more employees don't receive their paychecks... all so that MPT can pretend its assets have not massively declined in value. $MPW

"MPT was here..." $MPW

Where was the "investment in hospitals" from the MPT / LP SLB transaction? MPT is, after all, a "provider of capital at the very heart of healthcare!" This appears to be just another quasi-LBO sponsor deal.

If you trace the sources and uses it appears that MPT effectively financed the Kindred/Scion transaction once through COVID. And increased total financial leverage in the process. Scion later separated and a mess.

OR it could alternatively be viewed as a subsequent "kickback" ("you scratch my back, I'll scratch yours!;" Paging Deerfield!) for the prior acquisition of Capella by RegionalCare.

Regardless, similar to other "quality operators" CAPX spending at LP was just <3% of revenues post-MPT SLB. Minimum maintenance CAPX spend for acute care hospitals just to keep the lights on is approx. 6-8% of revenues.

Where was the "investment in hospitals" from the MPT / LP SLB transaction? MPT is, after all, a "provider of capital at the very heart of healthcare!" This appears to be just another quasi-LBO sponsor deal.

If you trace the sources and uses it appears that MPT effectively financed the Kindred/Scion transaction once through COVID. And increased total financial leverage in the process. Scion later separated and a mess.

OR it could alternatively be viewed as a subsequent "kickback" ("you scratch my back, I'll scratch yours!;" Paging Deerfield!) for the prior acquisition of Capella by RegionalCare.

Regardless, similar to other "quality operators" CAPX spending at LP was just <3% of revenues post-MPT SLB. Minimum maintenance CAPX spend for acute care hospitals just to keep the lights on is approx. 6-8% of revenues.

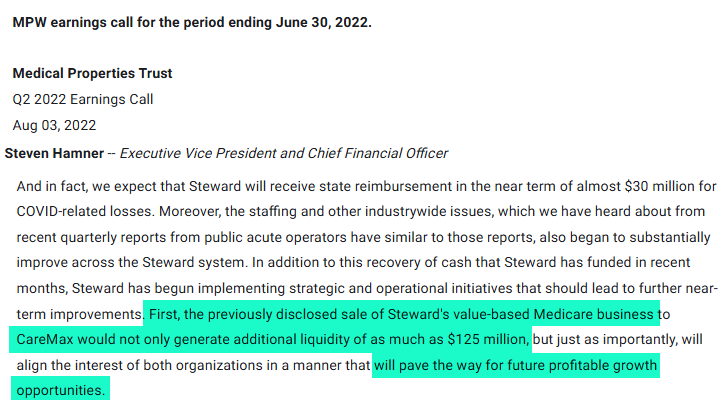

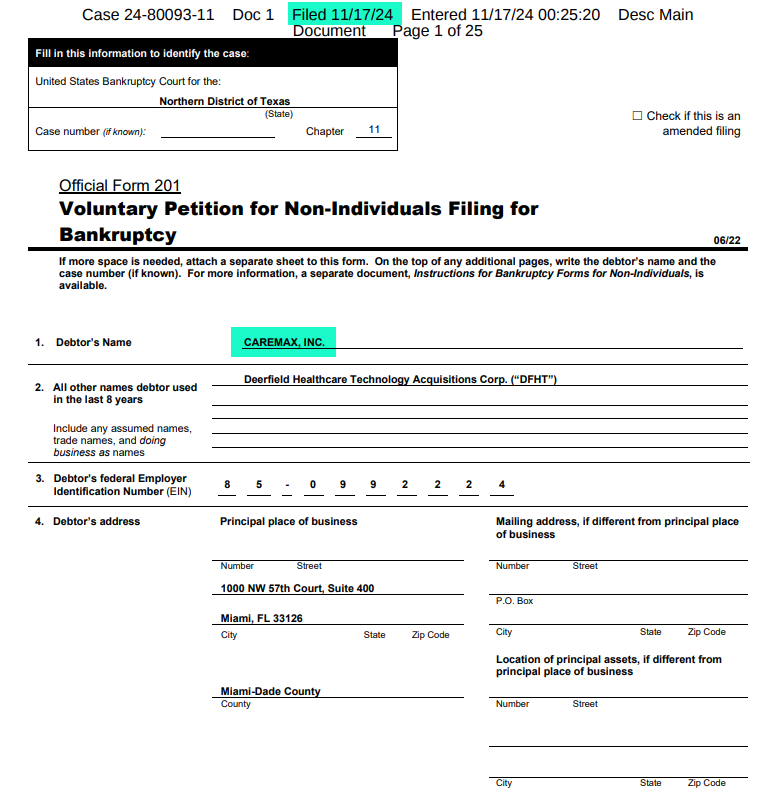

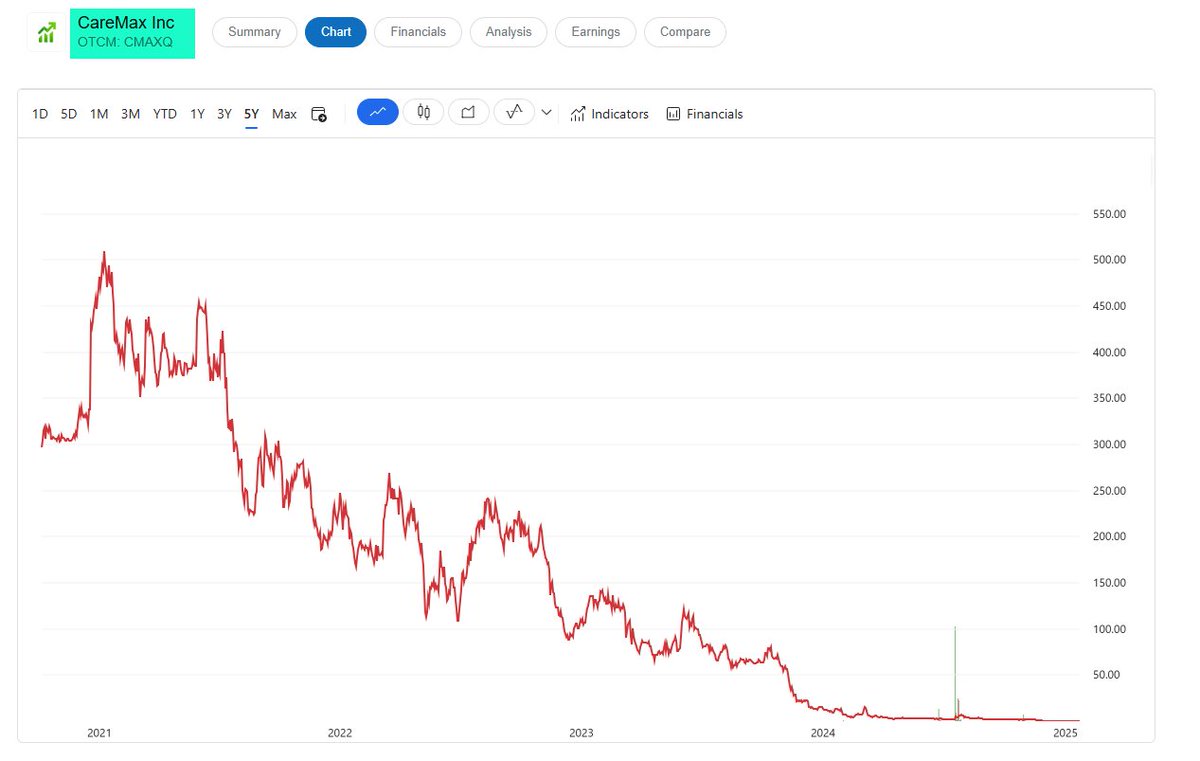

"MPT was here..." $MPW $CMAX $CMAXQ

Remember when the Caremax deal was touted by MPT as the Steward liquidity solution? Both Steward and Caremax filed for Ch. 11.

Everything these guys touch returns to the earth as dust.

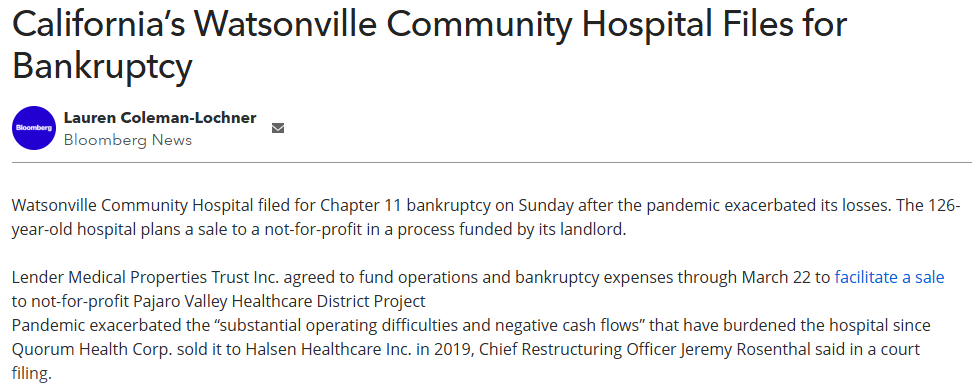

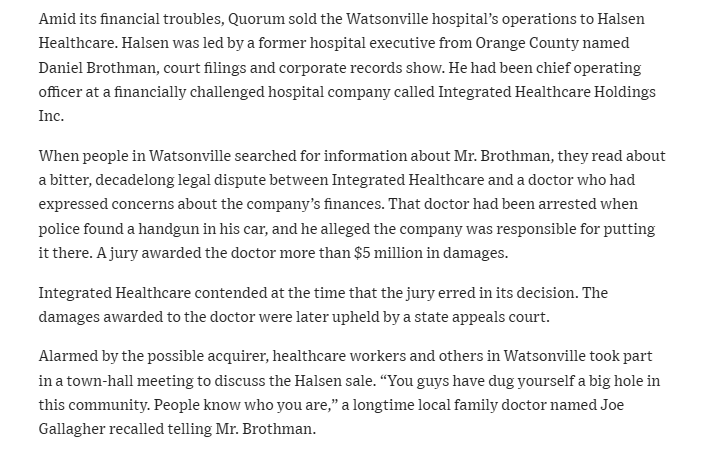

Deerfield was also sponsor and DIP lender in Pipeline BK.

Remember when the Caremax deal was touted by MPT as the Steward liquidity solution? Both Steward and Caremax filed for Ch. 11.

Everything these guys touch returns to the earth as dust.

Deerfield was also sponsor and DIP lender in Pipeline BK.

"MPT was here..." $MPW

MPT was paying for Audere services on behalf of its largest tenant Steward (and itself at the same time?) well-before October 2022, responsible for its 49% share of reimbursement of expenses through the "International Joint Venture.".

References:

wsj.com/livecoverage/s…

occrp.org/en/investigati…

MPT was paying for Audere services on behalf of its largest tenant Steward (and itself at the same time?) well-before October 2022, responsible for its 49% share of reimbursement of expenses through the "International Joint Venture.".

References:

wsj.com/livecoverage/s…

occrp.org/en/investigati…

"MPT was here..." $MPW

Actually "MPT is here!" After it chose AHS/HSA/Michael Sarian/Faisal Gil rather than being subjected to a possible lease re-characterization. All in order to avoid massive required writedowns.

Along with avoiding an Aldag deposition. Steve Hamner, not so lucky!

And now HSA operates $1.3BN of MPT GBV, or roughly 10% of total consolidated GBV. How much has MPT funded?

x.com/BigRiverCapita…

Actually "MPT is here!" After it chose AHS/HSA/Michael Sarian/Faisal Gil rather than being subjected to a possible lease re-characterization. All in order to avoid massive required writedowns.

Along with avoiding an Aldag deposition. Steve Hamner, not so lucky!

And now HSA operates $1.3BN of MPT GBV, or roughly 10% of total consolidated GBV. How much has MPT funded?

x.com/BigRiverCapita…

"MPT was here..." $MPW

FRAUD. Pure and simple.

Throughout 2022 MPT repeatedly (1) denied that Steward would have issues refinancing its ABL facility, (2) denied it would need to lend and/or participate in said refinancing, and (3) denied it had guaranteed or backstopped the debt of its largest tenant.

Management lied about the reasons for the $150MM Tranche 5 loan. The first $75MM advance was made on 12/4/22, BEFORE the HCA/Utah deal was killed. The truth is Steward was experiencing a "liquidity crisis" in late-2021/early-2022 ("we need the money tomorrow...").

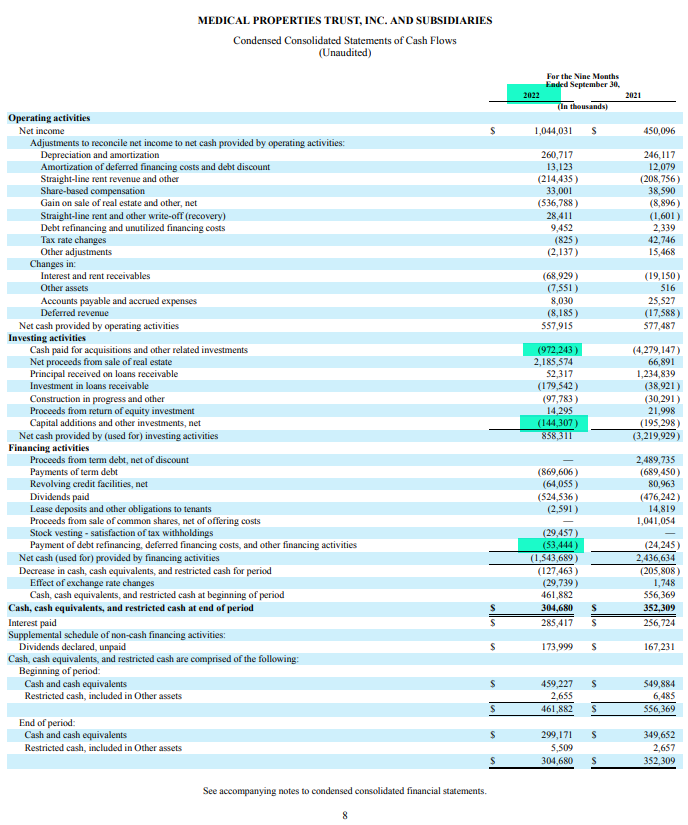

Management lied to investors and analysts about lending to Steward in H2:22, while at the same time claiming it was "strongly cash flow positive." It advanced $35MM to Steward on 30/9/22 and did not disclose it. It made >$100MM of "MPT advances" and did not disclose them. Then, perhaps most egregiously, it advanced the $28mm Tranche 6 promissory note in late-2022. MPT wasn't the lender of last resort, rather the lender of only resort.

When questioned on the Q4:22 earnings call, management lied about making any loans. Beginning with Q4:22 MPT also changed its asset reporting to prevent apples-to-apples comparisons. Then on the Q1:23 earnings call, MPT pretended they did not understand the questions.

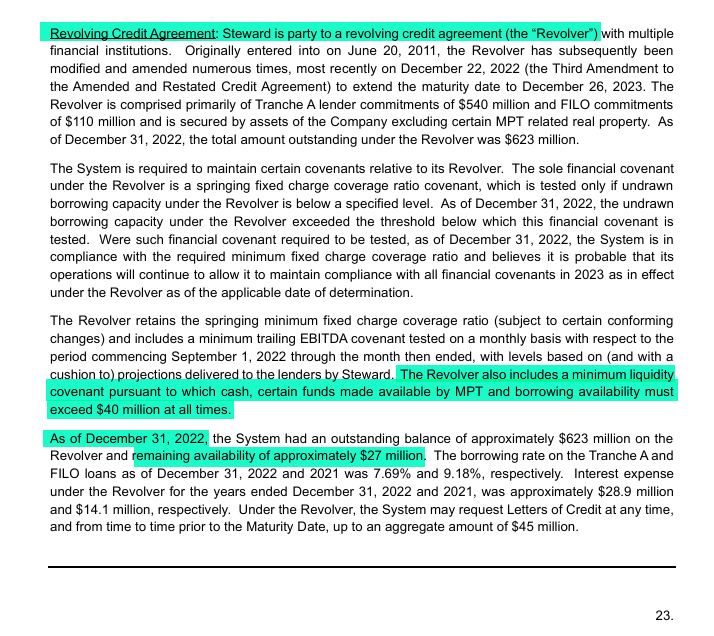

Now we know why! Per Steward's unaudited 2022 financial statements, Steward had a minimum liquidity covenant of $40MM, which included "funds made available by MPT." I.e. MPT had backstopped Steward all along. Consolidation?

Steward 2022 ending cash was $15MM. RCF availability was $27MM. Steward would have defaulted on its credit agreement at year end-2022 without MPT's backstop and liquidity support. Steward would have run out of cash long before that without the approx. $318MM MPT sent over in 2022 (that we know of).

You were all lied to. Egregiously. Where would the stock and bonds have gone if investors knew the truth as MPT management knew it?

Will you continue to allow them to get away with it?

FRAUD. Pure and simple.

Throughout 2022 MPT repeatedly (1) denied that Steward would have issues refinancing its ABL facility, (2) denied it would need to lend and/or participate in said refinancing, and (3) denied it had guaranteed or backstopped the debt of its largest tenant.

Management lied about the reasons for the $150MM Tranche 5 loan. The first $75MM advance was made on 12/4/22, BEFORE the HCA/Utah deal was killed. The truth is Steward was experiencing a "liquidity crisis" in late-2021/early-2022 ("we need the money tomorrow...").

Management lied to investors and analysts about lending to Steward in H2:22, while at the same time claiming it was "strongly cash flow positive." It advanced $35MM to Steward on 30/9/22 and did not disclose it. It made >$100MM of "MPT advances" and did not disclose them. Then, perhaps most egregiously, it advanced the $28mm Tranche 6 promissory note in late-2022. MPT wasn't the lender of last resort, rather the lender of only resort.

When questioned on the Q4:22 earnings call, management lied about making any loans. Beginning with Q4:22 MPT also changed its asset reporting to prevent apples-to-apples comparisons. Then on the Q1:23 earnings call, MPT pretended they did not understand the questions.

Now we know why! Per Steward's unaudited 2022 financial statements, Steward had a minimum liquidity covenant of $40MM, which included "funds made available by MPT." I.e. MPT had backstopped Steward all along. Consolidation?

Steward 2022 ending cash was $15MM. RCF availability was $27MM. Steward would have defaulted on its credit agreement at year end-2022 without MPT's backstop and liquidity support. Steward would have run out of cash long before that without the approx. $318MM MPT sent over in 2022 (that we know of).

You were all lied to. Egregiously. Where would the stock and bonds have gone if investors knew the truth as MPT management knew it?

Will you continue to allow them to get away with it?

"MPT was here..." $MPW

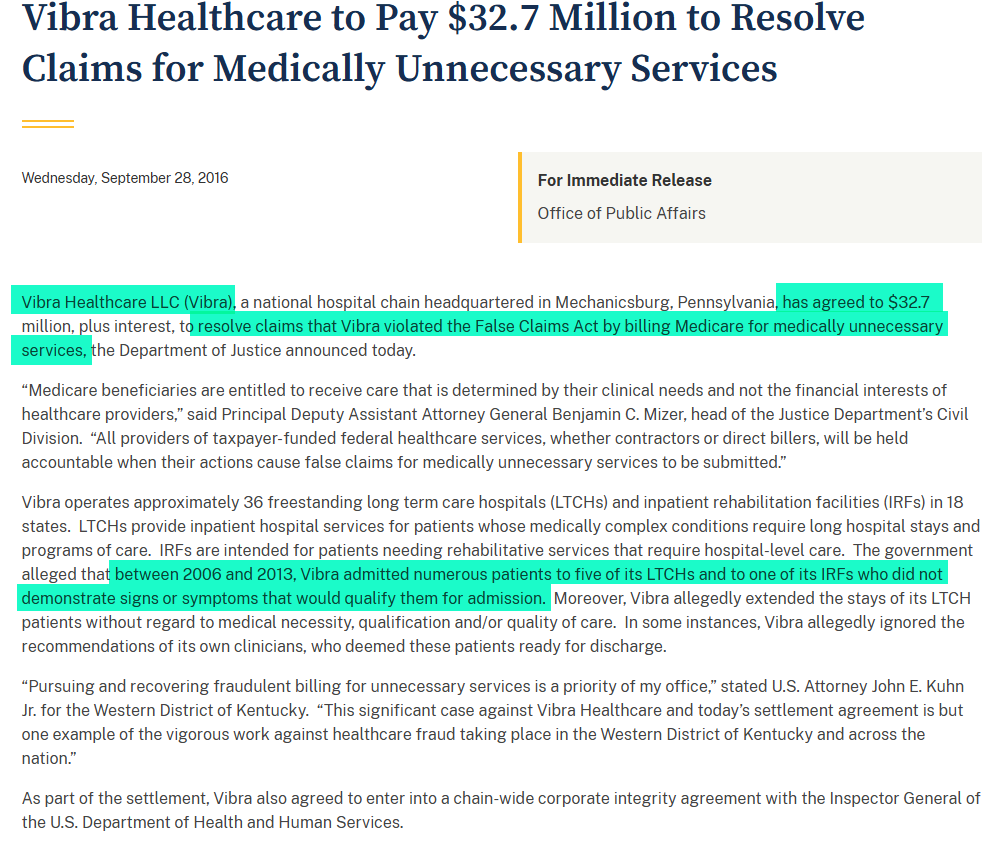

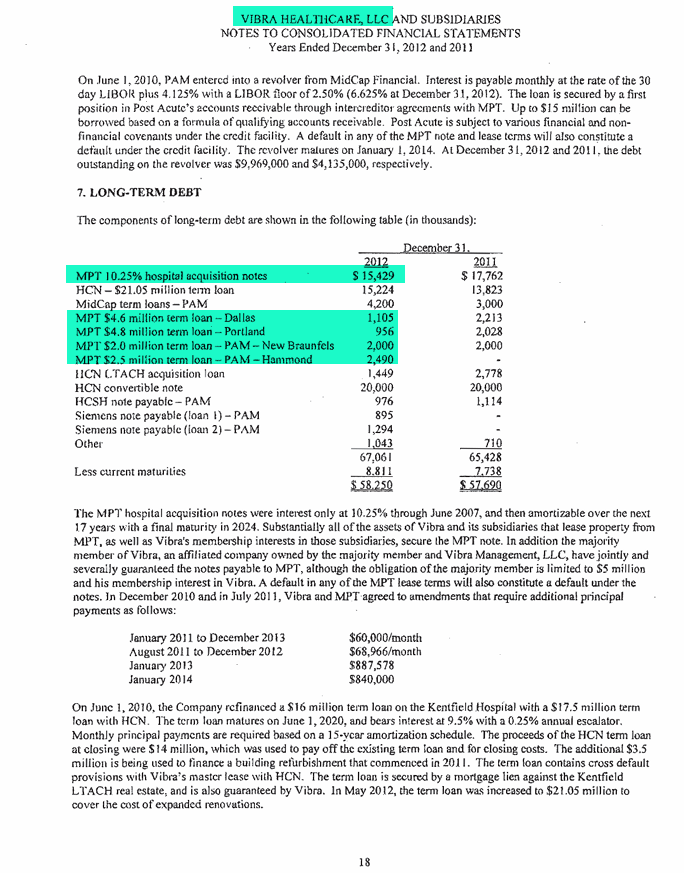

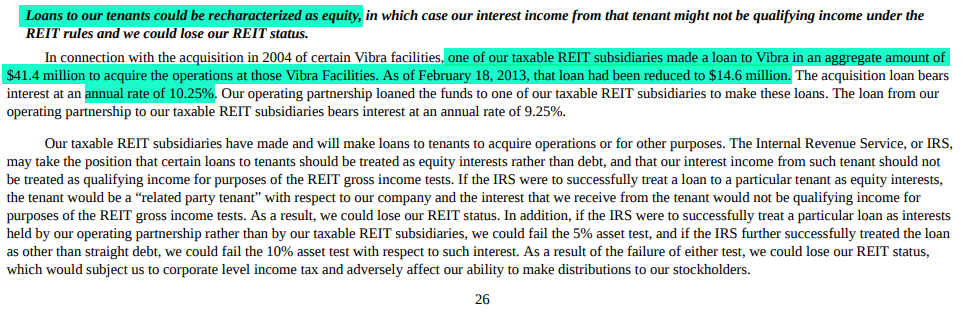

Just been making working capital loans and playing with REIT rules since its origin story, Vibra. Steward was just the latest iteration.

And Vibra just failed and needed to be restructured.

Just been making working capital loans and playing with REIT rules since its origin story, Vibra. Steward was just the latest iteration.

And Vibra just failed and needed to be restructured.

"MPT was here..." $MPW

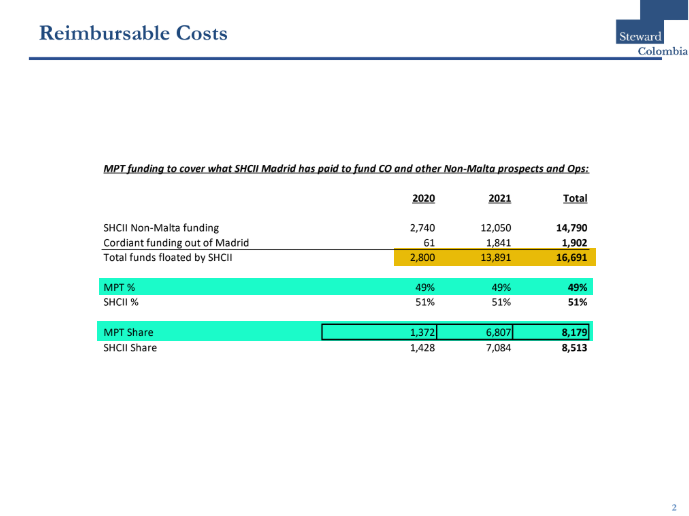

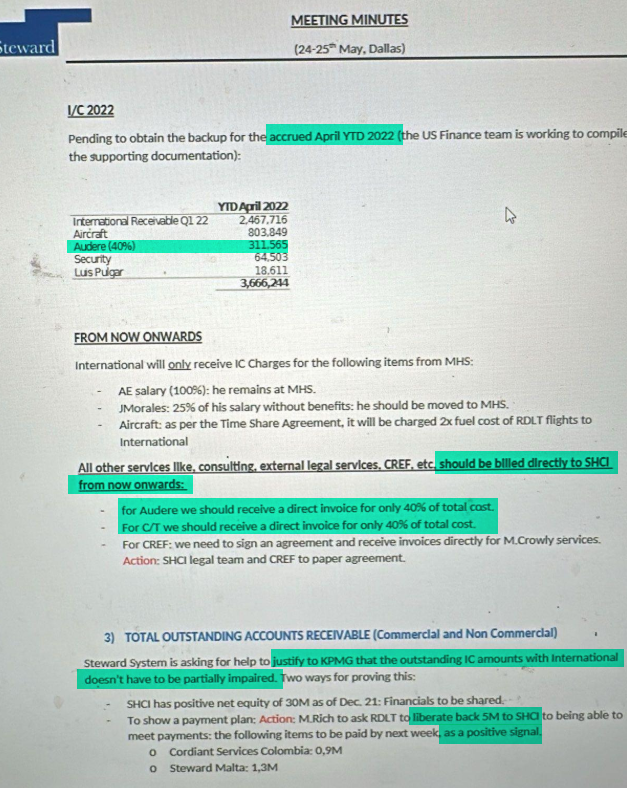

So many issues here:

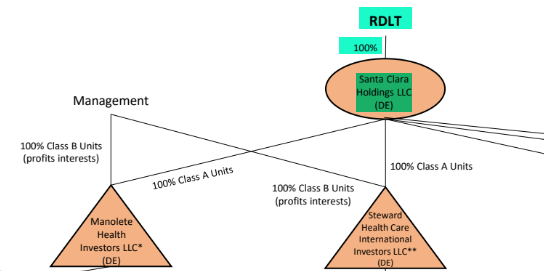

- Audere and CT Group (aka, the criminal surveillance and harassment of critics by a supposed healthcare company) would be billed directly to SHCI / the "International JV" beginning May 2022, which as we know was reimbursed 49% by MPT for their share,

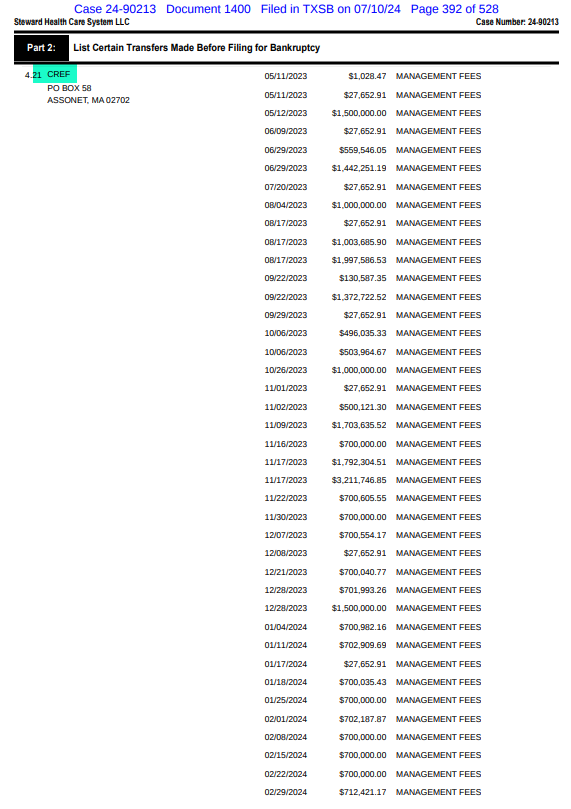

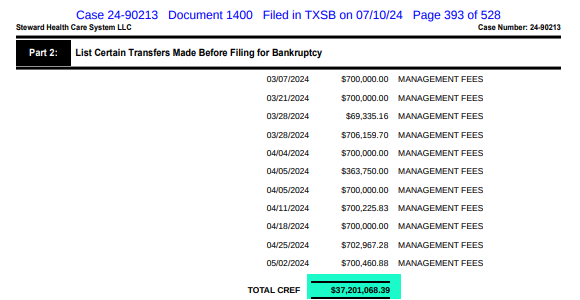

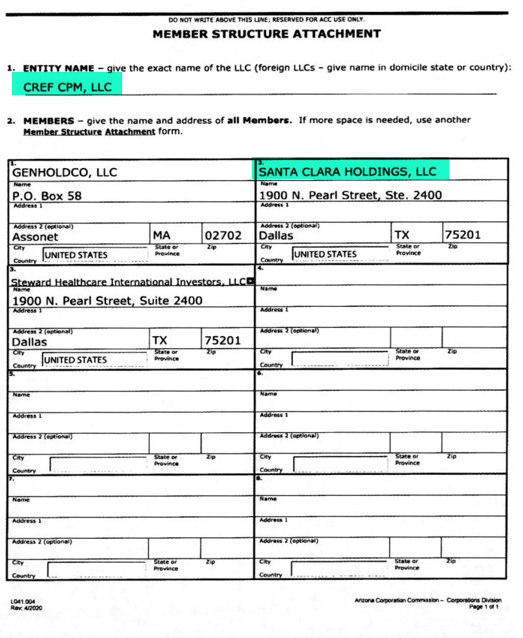

- MHS keeps popping up (where all the skeletons kept, along with CREF?),

- Steward US (SHCS) trying to hide/move CREF billing offshore,

- SHCS and SHCI clearly not separate arm's length companies (shared people, shared services, shared billing, shared locations, etc.),

- SHCI was clearly insolvent with now cash flow along with its parent SHCS, yet MPT held its investments in the International JV at par until 2024,

- SHCS executives RDLT and Rich taking actions to prop up SHCI.

How is SHCI separate from SHCS? How is Malta, which was managed by SHCI, separate from SHCS?

So many issues here:

- Audere and CT Group (aka, the criminal surveillance and harassment of critics by a supposed healthcare company) would be billed directly to SHCI / the "International JV" beginning May 2022, which as we know was reimbursed 49% by MPT for their share,

- MHS keeps popping up (where all the skeletons kept, along with CREF?),

- Steward US (SHCS) trying to hide/move CREF billing offshore,

- SHCS and SHCI clearly not separate arm's length companies (shared people, shared services, shared billing, shared locations, etc.),

- SHCI was clearly insolvent with now cash flow along with its parent SHCS, yet MPT held its investments in the International JV at par until 2024,

- SHCS executives RDLT and Rich taking actions to prop up SHCI.

How is SHCI separate from SHCS? How is Malta, which was managed by SHCI, separate from SHCS?

"MPT was here..." $MPW

Or "is here..."

Honorable @berniemoreno, we'll happily save you some time on those answers. It's a FRAUD.

U.S. Sen. Bernie Moreno, R-Ohio, has sent a letter demanding answers from Steward Health Care System, Medical Properties Trust, and Insight Health Systems after the abrupt closure of two hospitals in Trumbull County, and what he says is a threat to the county’s 911 dispatch center.

Reference: wfmj.com/story/52672104…

Or "is here..."

Honorable @berniemoreno, we'll happily save you some time on those answers. It's a FRAUD.

U.S. Sen. Bernie Moreno, R-Ohio, has sent a letter demanding answers from Steward Health Care System, Medical Properties Trust, and Insight Health Systems after the abrupt closure of two hospitals in Trumbull County, and what he says is a threat to the county’s 911 dispatch center.

Reference: wfmj.com/story/52672104…

"MPT was here..." $MPW

Financing a straight up theft "at the very heart of healthcare."

Financing a straight up theft "at the very heart of healthcare."

"MPT was here..." $MPW

Ah the old "MPT shuffle!" Otherwise known as a bribe or quid-pro-quo using shareholder and bondholder capital. MPT and Insight clearly tried it with the ML2 assets in MA last July. Then later did so with the former Steward OH hospitals that were "no bid" while encumbered by ML1.

It goes like this --> MPT will lend to you/cover your WC/CAPX needs, so long as you assume the existing lease or strike a new lease on equivalent terms. That way we can avoid necessary writedowns and keep our overstated balance sheet as is.

It only works so long as MPT has liquidity (from investors, btw) to shovel to primarily fly-by-night operators who are insolvent themselves and cannot afford the rent. Operator stuck with lease. MPT out for more money then receives back as "rent," but pretends its earnings!

Then the hospitals run into difficulty again. See Trumbull and Hillside. All to keep an unaffordable lease burden in place. HSA pending - "we received March rent early!" while ignoring out for $62.5MM in WC loans.

Some side plots: Morton "no bid" and non-economic, apparent efforts to keep info from public (surprise!), MPT would have been aware of this situation when it reported Q2:24 results and blamed the gov't for the situation simply bc gov't would not support plan to keep lease in place?

"At the very heart of healthcare!"

Ah the old "MPT shuffle!" Otherwise known as a bribe or quid-pro-quo using shareholder and bondholder capital. MPT and Insight clearly tried it with the ML2 assets in MA last July. Then later did so with the former Steward OH hospitals that were "no bid" while encumbered by ML1.

It goes like this --> MPT will lend to you/cover your WC/CAPX needs, so long as you assume the existing lease or strike a new lease on equivalent terms. That way we can avoid necessary writedowns and keep our overstated balance sheet as is.

It only works so long as MPT has liquidity (from investors, btw) to shovel to primarily fly-by-night operators who are insolvent themselves and cannot afford the rent. Operator stuck with lease. MPT out for more money then receives back as "rent," but pretends its earnings!

Then the hospitals run into difficulty again. See Trumbull and Hillside. All to keep an unaffordable lease burden in place. HSA pending - "we received March rent early!" while ignoring out for $62.5MM in WC loans.

Some side plots: Morton "no bid" and non-economic, apparent efforts to keep info from public (surprise!), MPT would have been aware of this situation when it reported Q2:24 results and blamed the gov't for the situation simply bc gov't would not support plan to keep lease in place?

"At the very heart of healthcare!"

"MPT was here..." $MPW

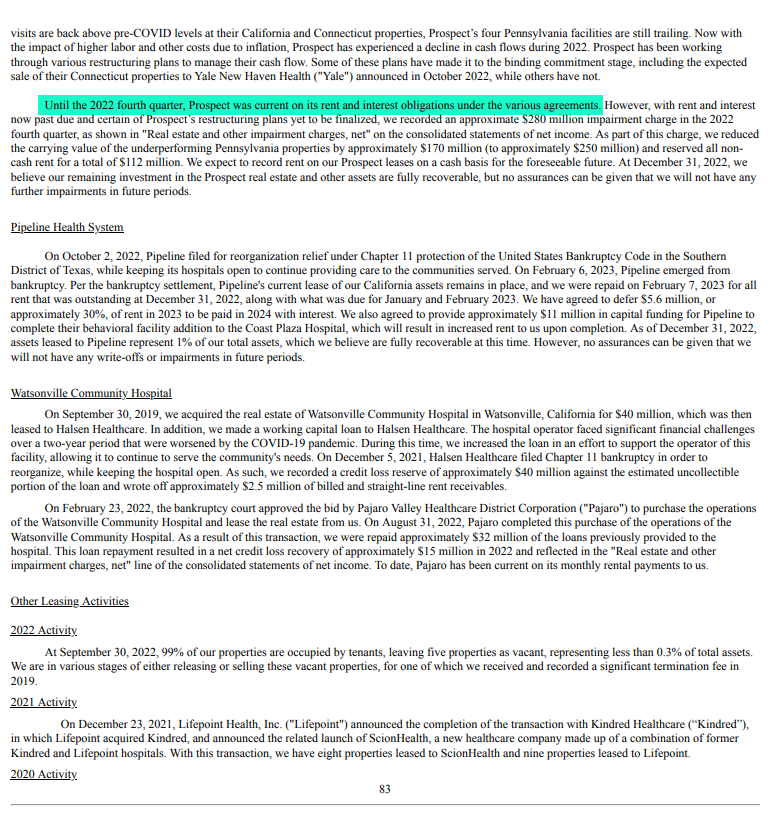

MPT said in its 2023 10-K that Prospect was current on its rent and interest obligations "until the 2022 fourth quarter."

We bet if you gave Matthew Hamner (really Steve) and Larry Portal (who works for Matthew, but doesn't realize it) truth serum, however, they would both tell you that Prospect had unpaid rent and interest of more than $30MM by September 2022. Which at a $35MM quarterly run-rate means Prospect had already missed a full quarter of obligations prior to Q4:22.

All of these amounts were recorded to "AFFO." None of it disclosed for a then 12% tenant.

FRAUD.

MPT said in its 2023 10-K that Prospect was current on its rent and interest obligations "until the 2022 fourth quarter."

We bet if you gave Matthew Hamner (really Steve) and Larry Portal (who works for Matthew, but doesn't realize it) truth serum, however, they would both tell you that Prospect had unpaid rent and interest of more than $30MM by September 2022. Which at a $35MM quarterly run-rate means Prospect had already missed a full quarter of obligations prior to Q4:22.

All of these amounts were recorded to "AFFO." None of it disclosed for a then 12% tenant.

FRAUD.

"MPT was here..." $MPW

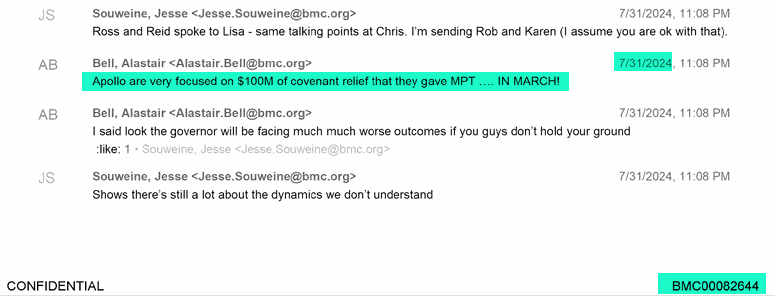

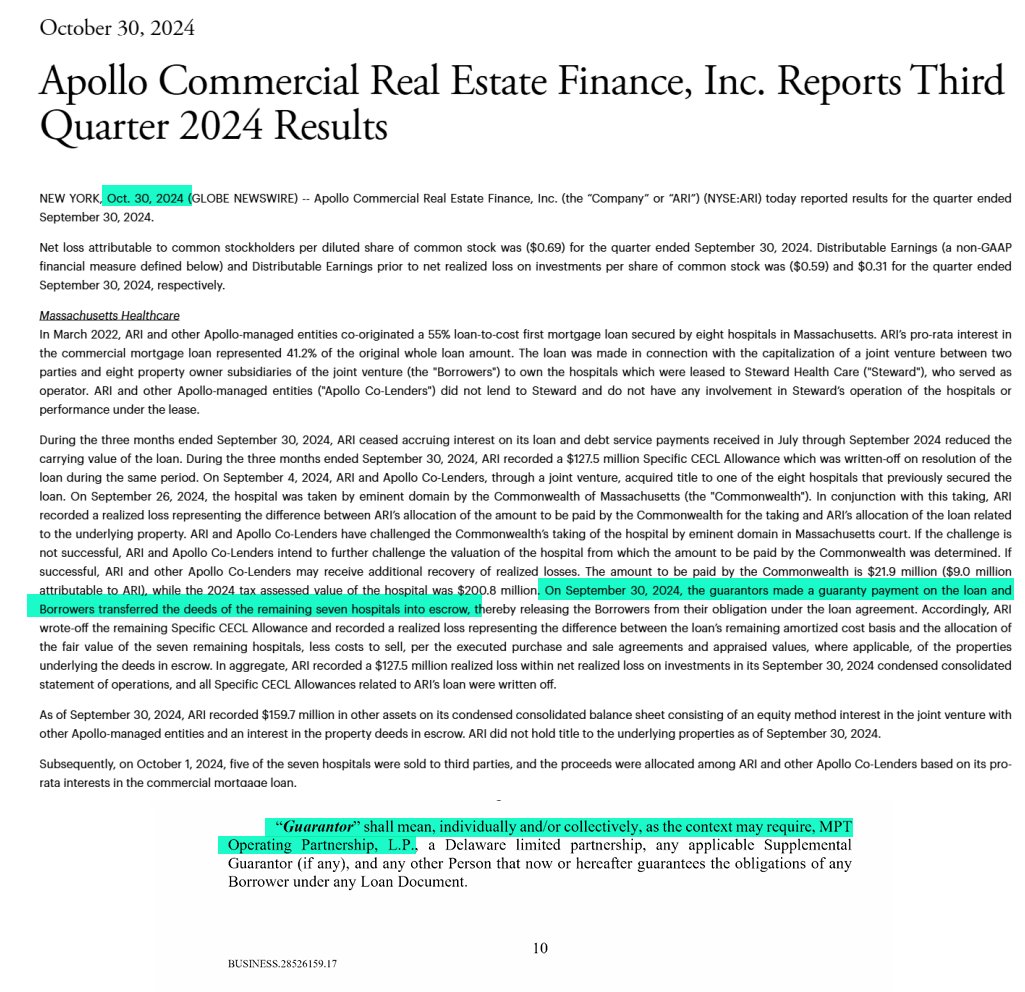

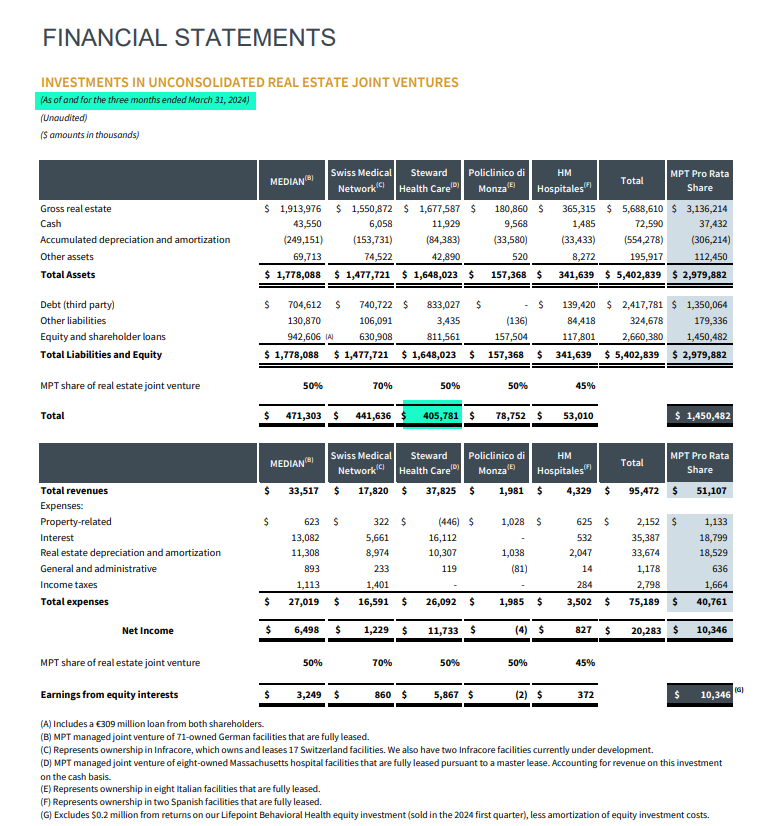

The 50/50 MAM JV (MPT as managing member) apparently was in some form of default of its loan obligations to Apollo in March 2024. $APO gave MPT $100MM "covenant relief" per Apollo eminent domain litigation. Two possibilities there: failure to service mortgage (not likely, see below) or the MPT guaranty of the mortgage debt?

MPT, of course, did not disclose the default or obligations at the time. Rather they originated a further $150MM FILO Bridge loan to Steward (took 50% of he loan, but in process wrote a put on another $60MM + pledged "EPDA" assets) at the end of February. Details not disclosed. Asset pledge later denied by Hamner (he lied) on Q1:24 CC. Rent was "paid" in the quarter.

At same time, however, we eventually learned that MPT was guarantor on what it had described as "nonrecourse" debt. Much more likely that MPT did something to relieve its obligations to Apollo.

Why does this matter? MPT did not have the liquidity at the time to honor the guaranty, nor had it received requisite covenant relief from its own banks (later obtained following CommonSpirit sale and sweep) to absorb impairments. MAM JV equity held at par at the end of Q1:24! Also important as original JV deal was not "clean" and required concessions to Apollo? What did MPT give Apollo for March 2024 "covenant relief?"

FRAUD to deceive investors as to the state of Steward, MPT's obligations to Apollo that were previously undisclosed, and again to prop up MPT balance sheet.

The 50/50 MAM JV (MPT as managing member) apparently was in some form of default of its loan obligations to Apollo in March 2024. $APO gave MPT $100MM "covenant relief" per Apollo eminent domain litigation. Two possibilities there: failure to service mortgage (not likely, see below) or the MPT guaranty of the mortgage debt?

MPT, of course, did not disclose the default or obligations at the time. Rather they originated a further $150MM FILO Bridge loan to Steward (took 50% of he loan, but in process wrote a put on another $60MM + pledged "EPDA" assets) at the end of February. Details not disclosed. Asset pledge later denied by Hamner (he lied) on Q1:24 CC. Rent was "paid" in the quarter.

At same time, however, we eventually learned that MPT was guarantor on what it had described as "nonrecourse" debt. Much more likely that MPT did something to relieve its obligations to Apollo.

Why does this matter? MPT did not have the liquidity at the time to honor the guaranty, nor had it received requisite covenant relief from its own banks (later obtained following CommonSpirit sale and sweep) to absorb impairments. MAM JV equity held at par at the end of Q1:24! Also important as original JV deal was not "clean" and required concessions to Apollo? What did MPT give Apollo for March 2024 "covenant relief?"

FRAUD to deceive investors as to the state of Steward, MPT's obligations to Apollo that were previously undisclosed, and again to prop up MPT balance sheet.

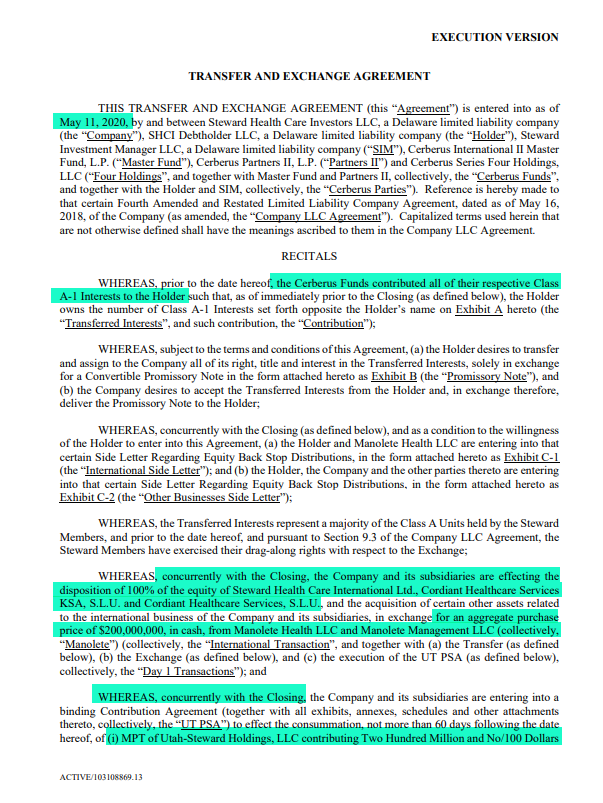

"MPT was here..." $MPW

In April 2020, Ed Aldag and the MPT BoD made clear MPT's intent to "buy out" Cerberus, who was the then owner of the Steward OpCo. This despite being a REIT that could not own more than 35% "by vote or value" of any healthcare operator.

What resulted was the May 2020 "Project Easter" recap, with three "inter-conditional" transactions (meaning that each could only occur so long as the others took place) whereby MPT contributed 100% of the capital:

- $335MM to buyout the Cerberus convert (which had been created to give RDLT + Steward management 89.9% ownership of Steward),

- $200MM for the International Joint Venture, and

- $200MM for the Utah PropCo assets.

= $745MM all together.

MPT fully capitalized the WholeCo. Not the PropCo.

FRAUD.

In April 2020, Ed Aldag and the MPT BoD made clear MPT's intent to "buy out" Cerberus, who was the then owner of the Steward OpCo. This despite being a REIT that could not own more than 35% "by vote or value" of any healthcare operator.

What resulted was the May 2020 "Project Easter" recap, with three "inter-conditional" transactions (meaning that each could only occur so long as the others took place) whereby MPT contributed 100% of the capital:

- $335MM to buyout the Cerberus convert (which had been created to give RDLT + Steward management 89.9% ownership of Steward),

- $200MM for the International Joint Venture, and

- $200MM for the Utah PropCo assets.

= $745MM all together.

MPT fully capitalized the WholeCo. Not the PropCo.

FRAUD.

"MPT was here..." $MPW

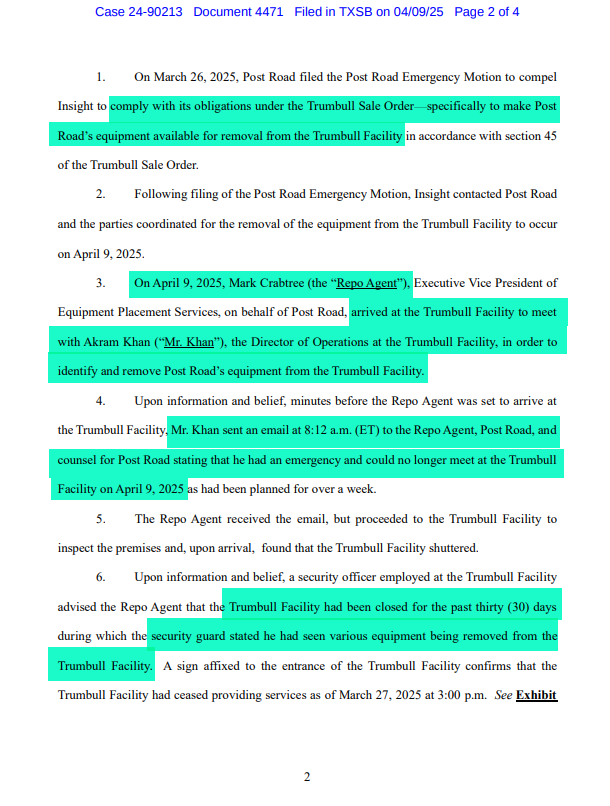

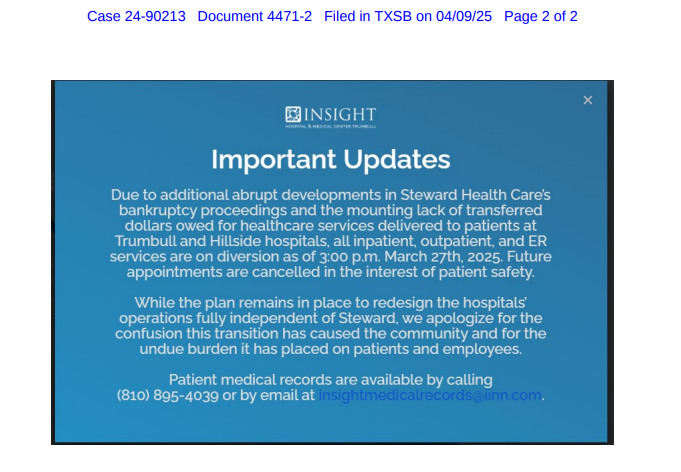

Actually "is here."

Nothing quite like "quality operator" Insight standing up the equipment repo agent. The idea that there needs to be a repo man at all says a lot. No response, of course!

Is Post Road's equipment still there? Hospital closed for past 30 days?

Are Trumbull and Hillside among the "vast majority" of former ML1 hospitals that are "cash flow positive?"

Nothing to see here...

Resource: restructuring.ra.kroll.com/Steward/Home-D…

Actually "is here."

Nothing quite like "quality operator" Insight standing up the equipment repo agent. The idea that there needs to be a repo man at all says a lot. No response, of course!

Is Post Road's equipment still there? Hospital closed for past 30 days?

Are Trumbull and Hillside among the "vast majority" of former ML1 hospitals that are "cash flow positive?"

Nothing to see here...

Resource: restructuring.ra.kroll.com/Steward/Home-D…

"MPT was here..." $MPW

Remember that time MPT accused @WSJ of manipulating the options market in a company press release? That it was somehow in on some grand conspiracy?

How many times did Aldag email internally that various parties "are clearly being paid by the shorts?" Without any basis in fact. We are sure MPT employees probably have many stories to tell about the delusional conspiratorial leanings of its leader. Fed by Babin. Hamner never quite comfortable, but not enough to not play along.

In fact, all of the criticisms were correct. If anything the bears underestimated how bad it was...

Remember that time MPT accused @WSJ of manipulating the options market in a company press release? That it was somehow in on some grand conspiracy?

How many times did Aldag email internally that various parties "are clearly being paid by the shorts?" Without any basis in fact. We are sure MPT employees probably have many stories to tell about the delusional conspiratorial leanings of its leader. Fed by Babin. Hamner never quite comfortable, but not enough to not play along.

In fact, all of the criticisms were correct. If anything the bears underestimated how bad it was...

"MPT was here..." $MPW

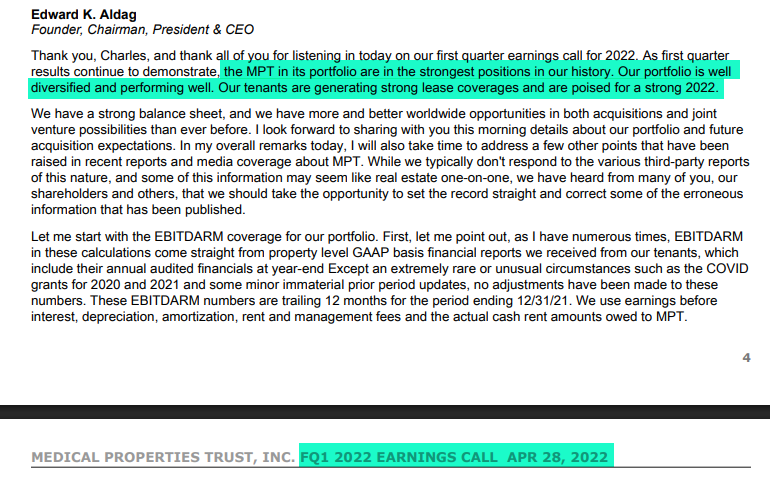

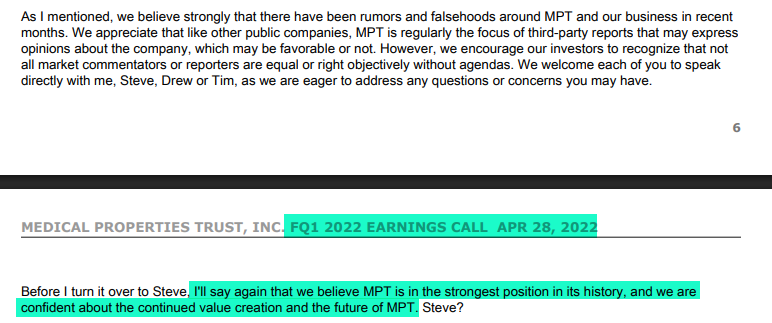

Just a reminder that MPT's coverage metrics and language around tenant profitability are fraudulent, with no informational value other than to deceive. They are designed to promote a narrative and deceive investors, regulators, lenders, etc. into thinking all is well, while behind the scenes MPT lends to the tenant with borrowed money to preserve overstated and unaffordable lease bases:

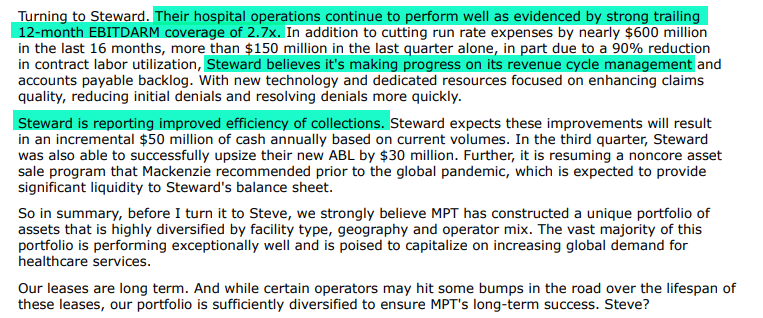

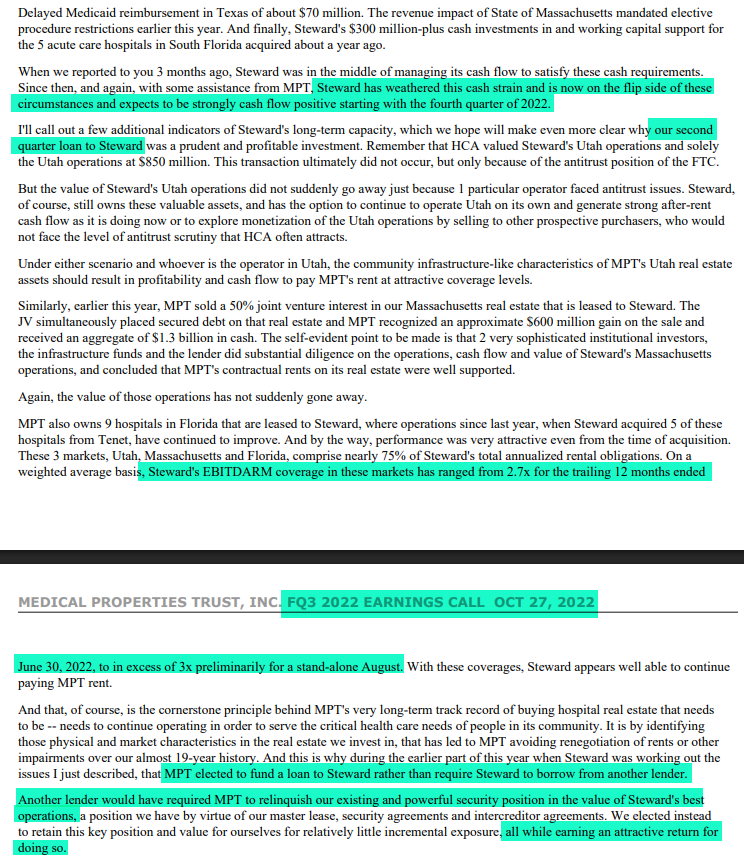

- MPT's August 2022 KPI calculations showed Steward annualizing $184.6MM in positive "free cash flow" for the consolidated company over the May-August 2022 period, and $495.1MM positive for all hospitals over the same period,

- MPT would tout Steward as now "strongly cash flow positive" on the Q3:22 call in October 2022, and

- MPT reported 2.5x "EBITDARM coverage" for Steward in Q3:22, covering April-June 2022 (see below).

However! Steward's unaudited 2022 FS clearly show the following for the full year:

- Net cash from operating activities: -$119.3MM

- Capex: -$169.6MM

- = FCF: -$288.9MM

Entirely fraudulent. Not even remotely close.

Just a reminder that MPT's coverage metrics and language around tenant profitability are fraudulent, with no informational value other than to deceive. They are designed to promote a narrative and deceive investors, regulators, lenders, etc. into thinking all is well, while behind the scenes MPT lends to the tenant with borrowed money to preserve overstated and unaffordable lease bases:

- MPT's August 2022 KPI calculations showed Steward annualizing $184.6MM in positive "free cash flow" for the consolidated company over the May-August 2022 period, and $495.1MM positive for all hospitals over the same period,

- MPT would tout Steward as now "strongly cash flow positive" on the Q3:22 call in October 2022, and

- MPT reported 2.5x "EBITDARM coverage" for Steward in Q3:22, covering April-June 2022 (see below).

However! Steward's unaudited 2022 FS clearly show the following for the full year:

- Net cash from operating activities: -$119.3MM

- Capex: -$169.6MM

- = FCF: -$288.9MM

Entirely fraudulent. Not even remotely close.

"MPT was here..." $MPW

ANOTHER $200-300MM cost to complete Norwood from here, after pouring over $200MM into the "rebuild" already and a lease base of >$420MM.

No DON in place. Means any buyer, to the extent one could even be found, would credit the cost to complete against their gross "value" in coming to any purchase price.

Is this another near-zero? Could be. It's definitely not "par," which is where MPT carries it...

Reference: boston25news.com/news/local/nor…

ANOTHER $200-300MM cost to complete Norwood from here, after pouring over $200MM into the "rebuild" already and a lease base of >$420MM.

No DON in place. Means any buyer, to the extent one could even be found, would credit the cost to complete against their gross "value" in coming to any purchase price.

Is this another near-zero? Could be. It's definitely not "par," which is where MPT carries it...

Reference: boston25news.com/news/local/nor…

"MPT was here..." $MPW

The lying, gaslighting and attempts at defrauding investors by MPT management will never stop. It's clearly Aldag's only option at this point, as the facts are simply not on his side.

The most recent example is the AR published last night before a long holiday weekend, where MPT once again takes the "Ministry of Truth" approach.

MPT management does not get to re-rewrite history. Nor does it get to choose which facts are relevant and which are not after years of lies and fraud, not to mention destroying the company.

"Alternative facts" cannot be invented to hide Aldag's incompetence. Nor can it hide the BoD's involvement and equivalent ineptitude.

So we are "correcting the record" for MPT investors.

The lying, gaslighting and attempts at defrauding investors by MPT management will never stop. It's clearly Aldag's only option at this point, as the facts are simply not on his side.

The most recent example is the AR published last night before a long holiday weekend, where MPT once again takes the "Ministry of Truth" approach.

MPT management does not get to re-rewrite history. Nor does it get to choose which facts are relevant and which are not after years of lies and fraud, not to mention destroying the company.

"Alternative facts" cannot be invented to hide Aldag's incompetence. Nor can it hide the BoD's involvement and equivalent ineptitude.

So we are "correcting the record" for MPT investors.

"MPT was here..." $MPW

"MPT was here..." $MPW

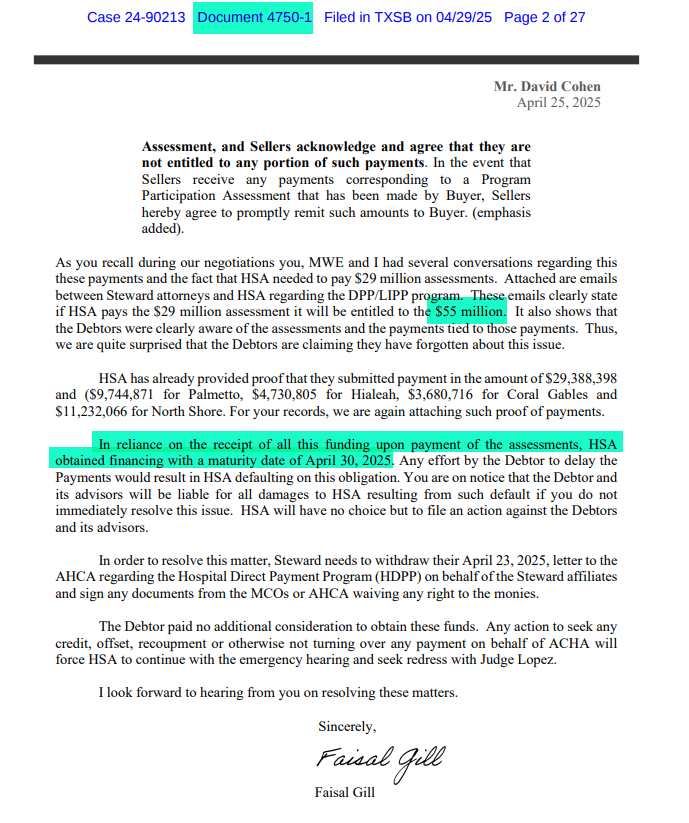

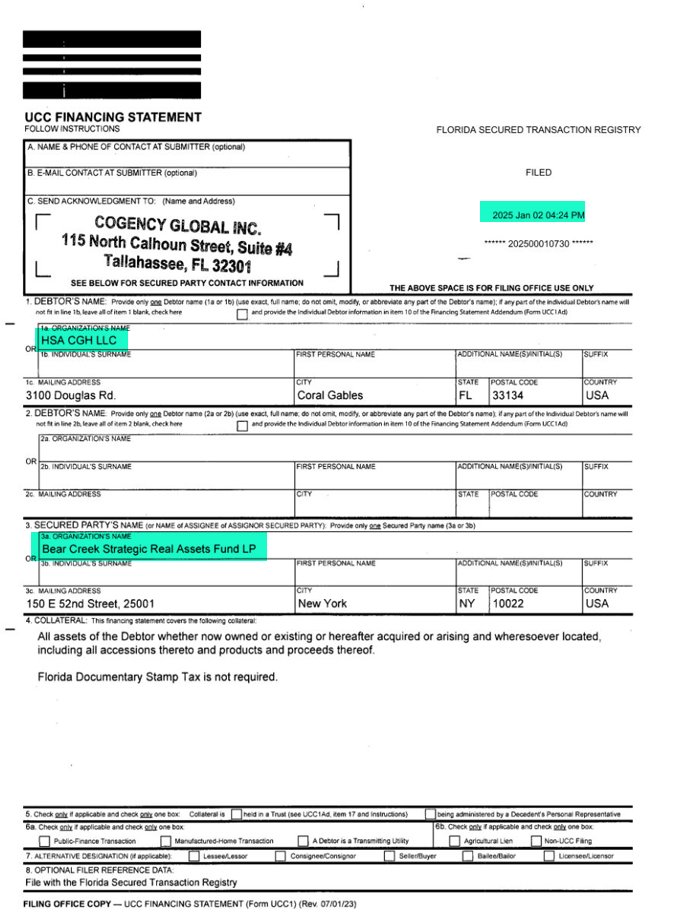

$55MM Florida DPP money was used by "quality operator" HSA/AHS to obtain financing which matures TOMORROW. HSA obtained financing in reliance on ALL $55MM. How much did Steward offer to settle? Is this related to the Bear Creek UCC? Was it used to secure the ~$62.5MM working capital loans made by MPT to HSA as of year-end 2024?

What is the funding hole here? What is the unpaid vendor balance, ~$220MM?

Also, there is Faisal Gill of "Hawthorn Hangar" and other ponzi scheme infamy!

x.com/AmaralPartners…

$55MM Florida DPP money was used by "quality operator" HSA/AHS to obtain financing which matures TOMORROW. HSA obtained financing in reliance on ALL $55MM. How much did Steward offer to settle? Is this related to the Bear Creek UCC? Was it used to secure the ~$62.5MM working capital loans made by MPT to HSA as of year-end 2024?

What is the funding hole here? What is the unpaid vendor balance, ~$220MM?

Also, there is Faisal Gill of "Hawthorn Hangar" and other ponzi scheme infamy!

x.com/AmaralPartners…

"MPT was here..." $MPW

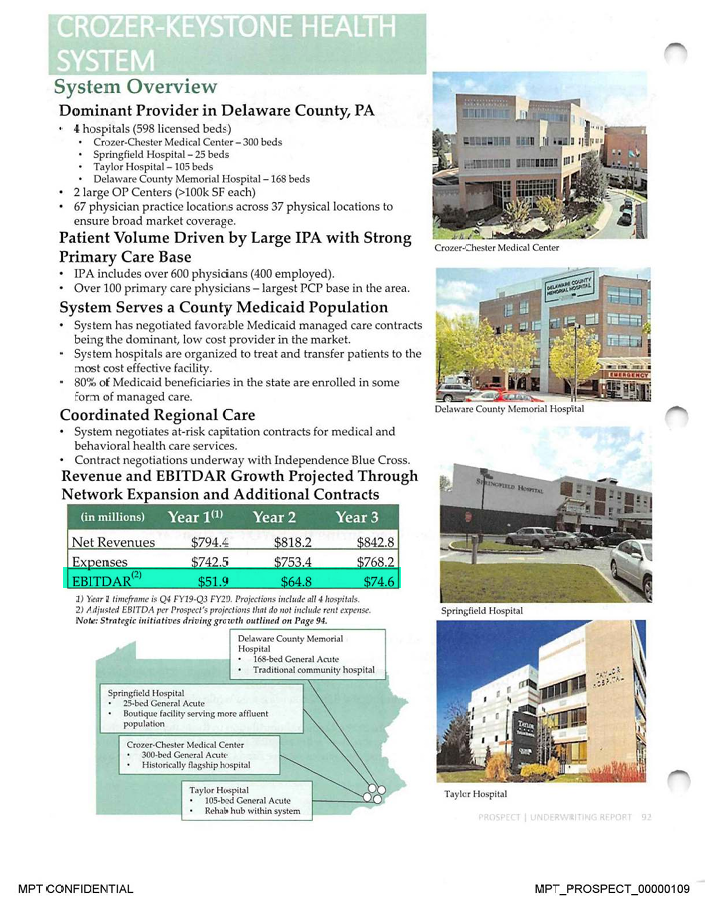

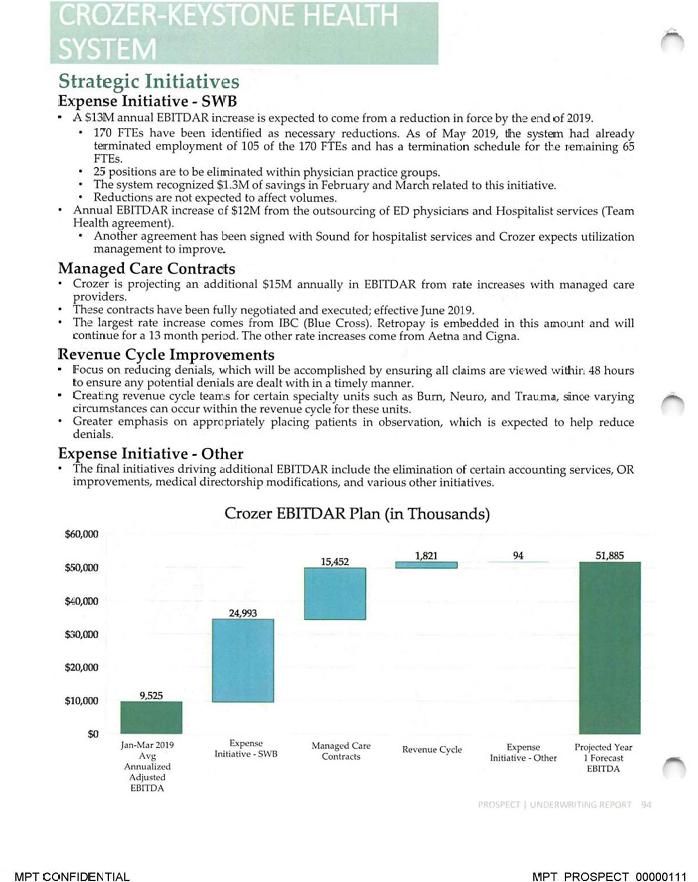

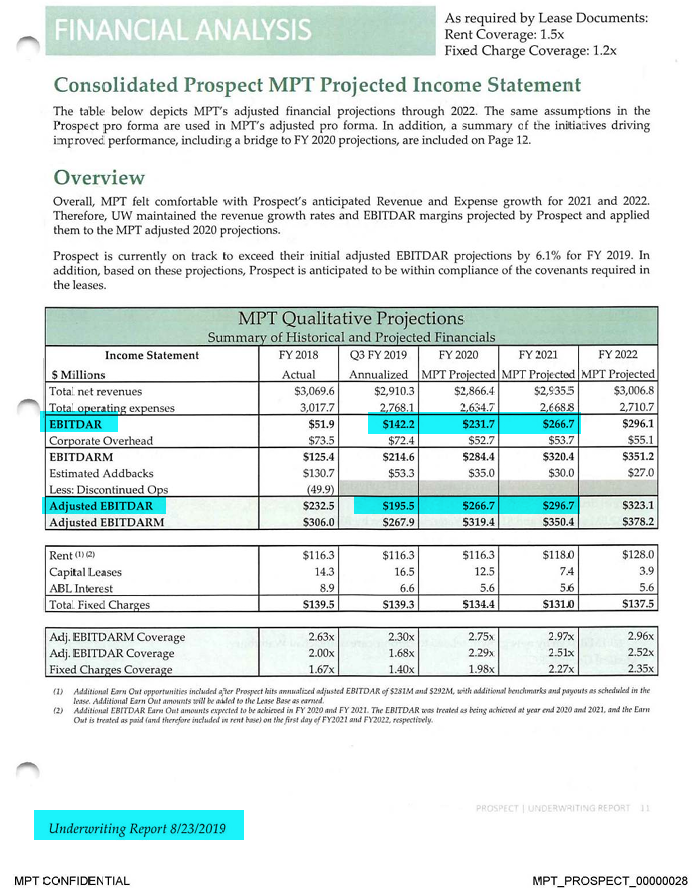

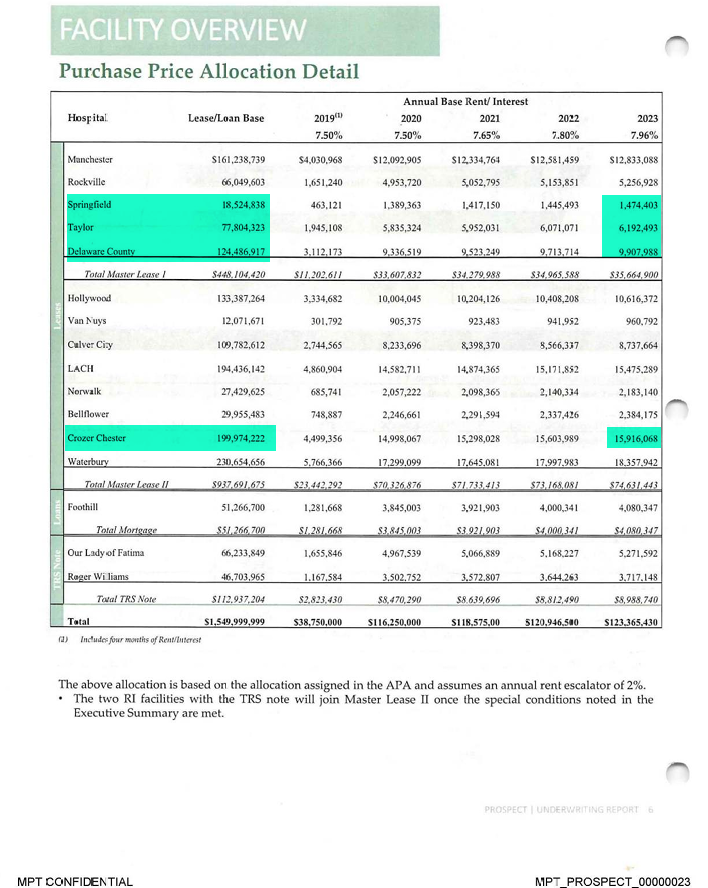

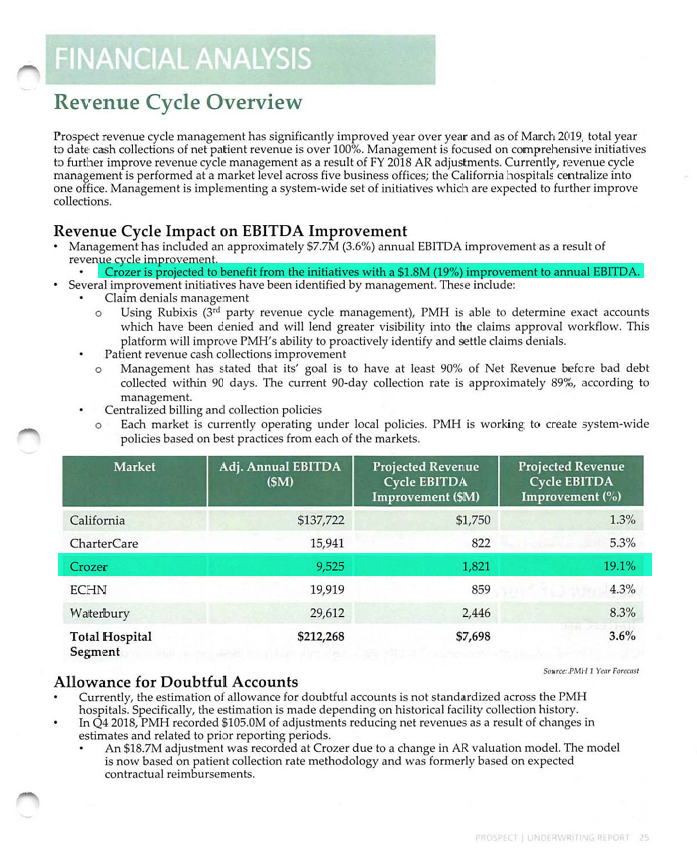

This is how bad MPT's underwriting is, all driven by a desire to increase executive comp and "paper over" prior mistakes (in this case Steward primarily, Adeptus, Alecto and Vibra) with faux "earnings" growth. At the cost of the new operator in question.

MPT paid $421MM for the 4 Prospect PA/Crozer hospitals in 2019. MPT projected Prospect to grow their version of PA "EBITDAR" (before CAPX) by 7x by Year 3 2022 ($74.6MM underwritten vs. ~$10MM base year) in "hockey stick" fashion. The rent by that time would have been ~$33.5MM +/-.

Now about to close, the PA/Crozer hospitals are losing >$150MM per year as per the BK advisors without paying rent. Next three months EBITDAR is budgeted at -$18MM, or > -$200MM annualized, as the hospitals close. MPT has taken a 100% loss as of today on its PA/Crozer investment.

Just a bit outside!

"The strength of our underwriting."

"Validating our values."

"We focus on underwriting the real estate."

"Hospitals will always be needed."

"We hardly ever take a loss on our real estate."

"Our investment is well-secured and fully recoverable."

"We have been doing this for 20 years."

"Our tenants will not miss a dollar of rent."

"The strength of our master leases."

If you ever hear those lines from these guys... run!

This is how bad MPT's underwriting is, all driven by a desire to increase executive comp and "paper over" prior mistakes (in this case Steward primarily, Adeptus, Alecto and Vibra) with faux "earnings" growth. At the cost of the new operator in question.

MPT paid $421MM for the 4 Prospect PA/Crozer hospitals in 2019. MPT projected Prospect to grow their version of PA "EBITDAR" (before CAPX) by 7x by Year 3 2022 ($74.6MM underwritten vs. ~$10MM base year) in "hockey stick" fashion. The rent by that time would have been ~$33.5MM +/-.

Now about to close, the PA/Crozer hospitals are losing >$150MM per year as per the BK advisors without paying rent. Next three months EBITDAR is budgeted at -$18MM, or > -$200MM annualized, as the hospitals close. MPT has taken a 100% loss as of today on its PA/Crozer investment.

Just a bit outside!

"The strength of our underwriting."

"Validating our values."

"We focus on underwriting the real estate."

"Hospitals will always be needed."

"We hardly ever take a loss on our real estate."

"Our investment is well-secured and fully recoverable."

"We have been doing this for 20 years."

"Our tenants will not miss a dollar of rent."

"The strength of our master leases."

If you ever hear those lines from these guys... run!

"MPT was here..." $MPW

How it started.... vs. how it's going!

This is in reference to the EPDA assets that MPT did not (but really did, we had the docs) pledge to the FILO Bridge lenders months before the Q1:24 earnings call and Steward BK. Pledge docs signed by Hamner. Poetic that he just admitted a year later the rights were conveyed to a third-party lender in MPT's then largest tenant.

"... we transferred rights to it well over a year ago.."

vs. "No."

If only there were rules against lying about material issues on earnings calls...

How it started.... vs. how it's going!

This is in reference to the EPDA assets that MPT did not (but really did, we had the docs) pledge to the FILO Bridge lenders months before the Q1:24 earnings call and Steward BK. Pledge docs signed by Hamner. Poetic that he just admitted a year later the rights were conveyed to a third-party lender in MPT's then largest tenant.

"... we transferred rights to it well over a year ago.."

vs. "No."

If only there were rules against lying about material issues on earnings calls...

"MPT was here..." $MPW

Pretty much sums it all up...

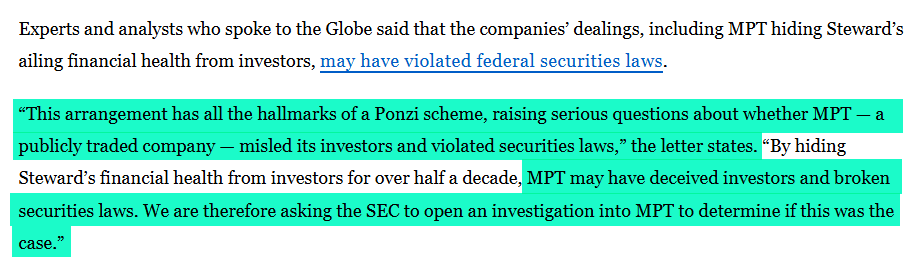

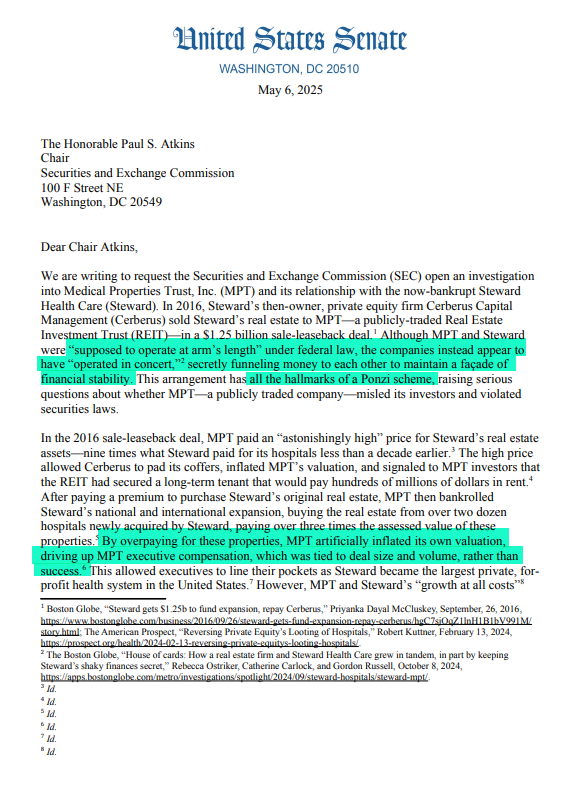

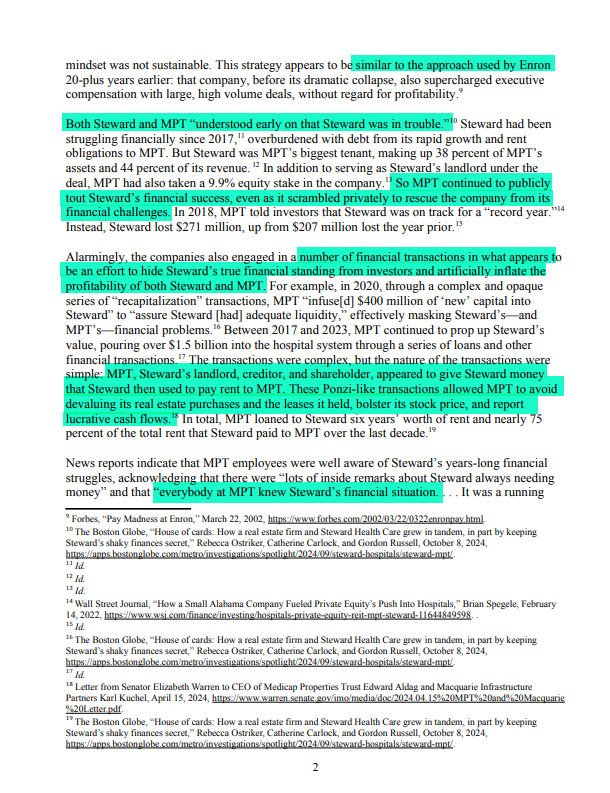

"By overpaying for these properties, MPT artificially inflated its own valuation, driving up MPT executive compensation, which was tied to deal size and volume, rather than success."

"This strategy appears to be similar to the approach used by Enron 20-plus years earlier..."

"The transactions were complex, but the nature of the transactions were simple: MPT, Steward’s landlord, creditor, and shareholder, appeared to give Steward money that Steward then used to pay rent to MPT. These Ponzi-like transactions allowed MPT to avoid devaluing its real estate purchases and the leases it held..."

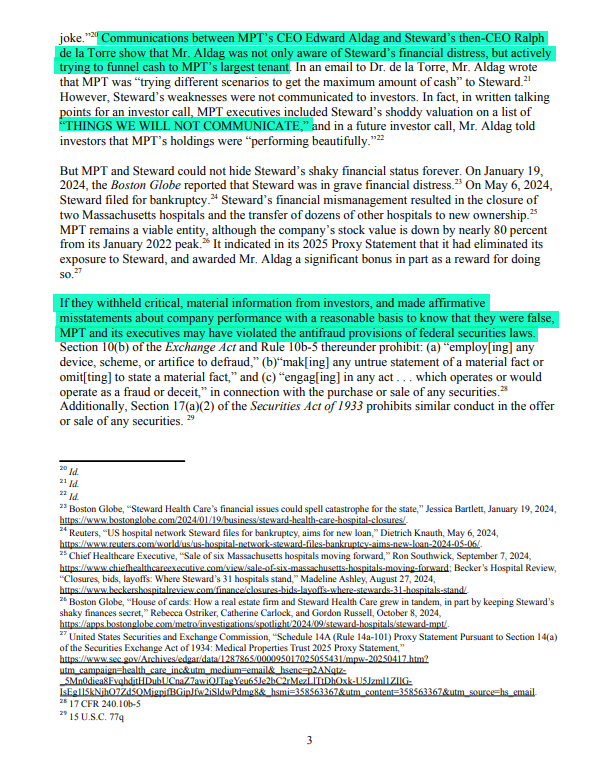

"Communications between MPT’s CEO Edward Aldag and Steward’s then-CEO Ralph de la Torre show that Mr. Aldag was not only aware of Steward’s financial distress, but actively trying to funnel cash to MPT’s largest tenant."

Pretty much sums it all up...

"By overpaying for these properties, MPT artificially inflated its own valuation, driving up MPT executive compensation, which was tied to deal size and volume, rather than success."

"This strategy appears to be similar to the approach used by Enron 20-plus years earlier..."

"The transactions were complex, but the nature of the transactions were simple: MPT, Steward’s landlord, creditor, and shareholder, appeared to give Steward money that Steward then used to pay rent to MPT. These Ponzi-like transactions allowed MPT to avoid devaluing its real estate purchases and the leases it held..."

"Communications between MPT’s CEO Edward Aldag and Steward’s then-CEO Ralph de la Torre show that Mr. Aldag was not only aware of Steward’s financial distress, but actively trying to funnel cash to MPT’s largest tenant."

"MPT was here..." $MPW

Actually "MPT is here." Scion no sufficient operating income to cover rent + interest. Burning cash. Starving hospitals of capital investment at only ~1% of revenues.

Sound familiar? Yup, it's everywhere you look...

Scion in the new secured pool.

Actually "MPT is here." Scion no sufficient operating income to cover rent + interest. Burning cash. Starving hospitals of capital investment at only ~1% of revenues.

Sound familiar? Yup, it's everywhere you look...

Scion in the new secured pool.

"MPT was here..." $MPW

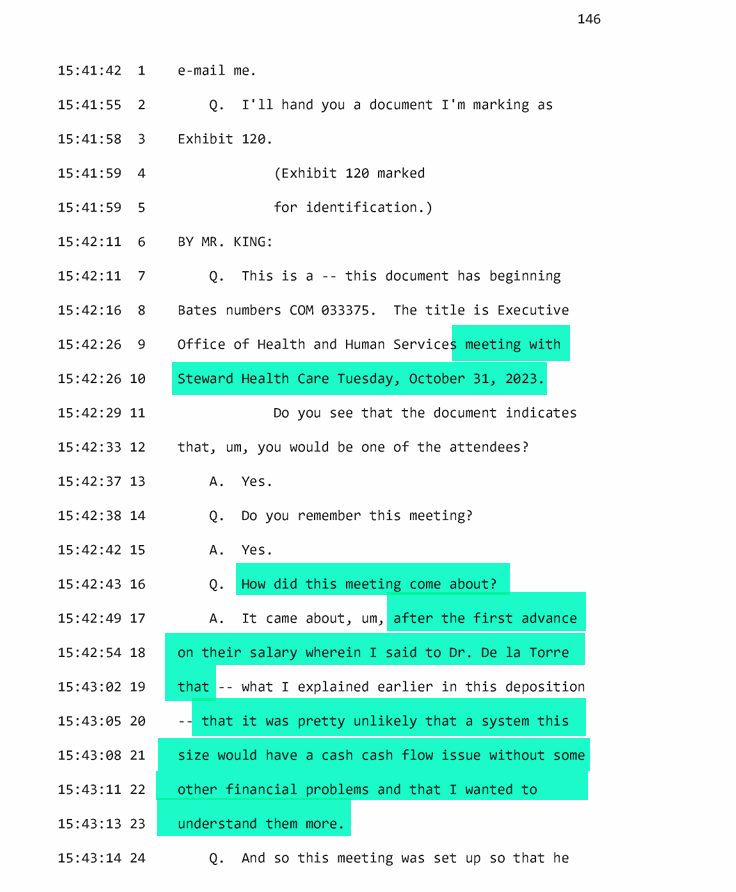

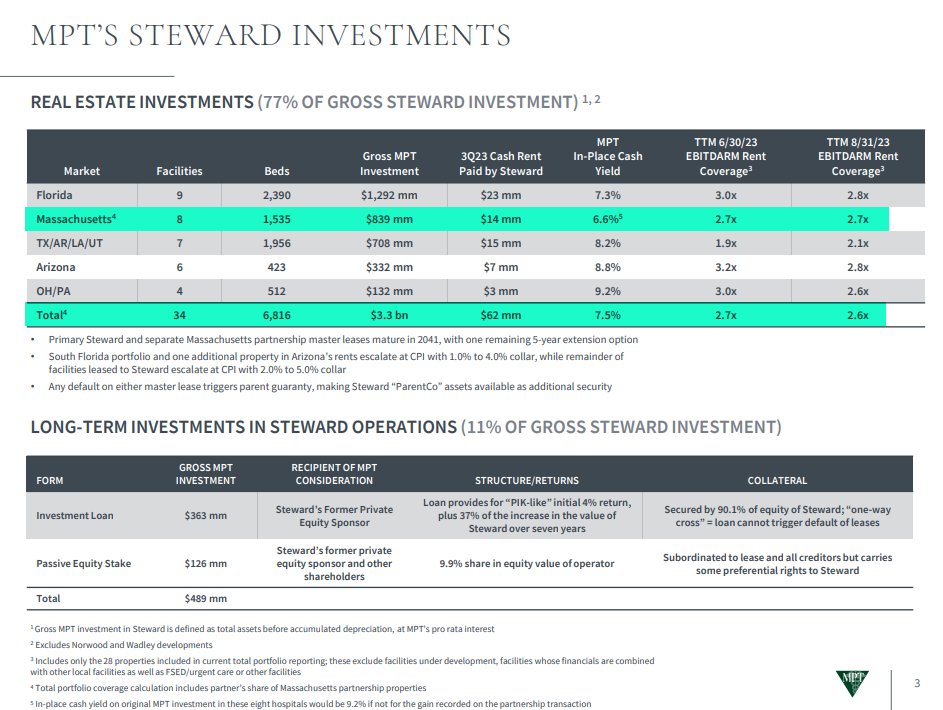

"Series of meetings... after the first advance of their salary... RDLT... October 2023"

Question - How can both of these be true at the same time: (1) Steward operations be "performing well," EBITDARM coverage be ~2.7x, and MA coverage also be ~2.7x in late-October 2023, and also (2) Steward having meetings (plural) in October 2023 with EOHHS and receiving the first (!!) advance on salary in MA the same month?

Answer: It is impossible. These cannot be true at the same time. This shows (1) the lack of credibility and willingness to lie/defraud both in-person and on earnings call by MPT's fraudulent and incompetent management team, and (2) the fraudulent nature of MPT's arbitrary rent "coverage" metrics that do not represent financial reality.

Of course this was not mentioned on the call! Neither was the fact that Steward had completely stopped paying "rent" (not disclosed until Q3:23 10-Q a week later).

Source: $APO eminent domain litigation w/ MA.

"Series of meetings... after the first advance of their salary... RDLT... October 2023"

Question - How can both of these be true at the same time: (1) Steward operations be "performing well," EBITDARM coverage be ~2.7x, and MA coverage also be ~2.7x in late-October 2023, and also (2) Steward having meetings (plural) in October 2023 with EOHHS and receiving the first (!!) advance on salary in MA the same month?

Answer: It is impossible. These cannot be true at the same time. This shows (1) the lack of credibility and willingness to lie/defraud both in-person and on earnings call by MPT's fraudulent and incompetent management team, and (2) the fraudulent nature of MPT's arbitrary rent "coverage" metrics that do not represent financial reality.

Of course this was not mentioned on the call! Neither was the fact that Steward had completely stopped paying "rent" (not disclosed until Q3:23 10-Q a week later).

Source: $APO eminent domain litigation w/ MA.

"MPT was here..." $MPW

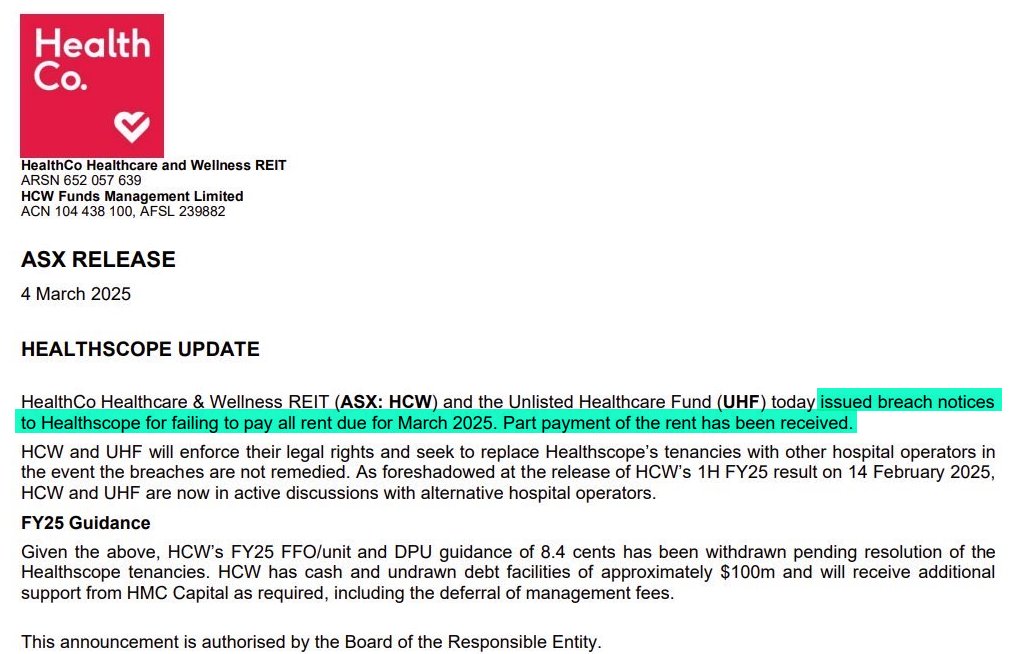

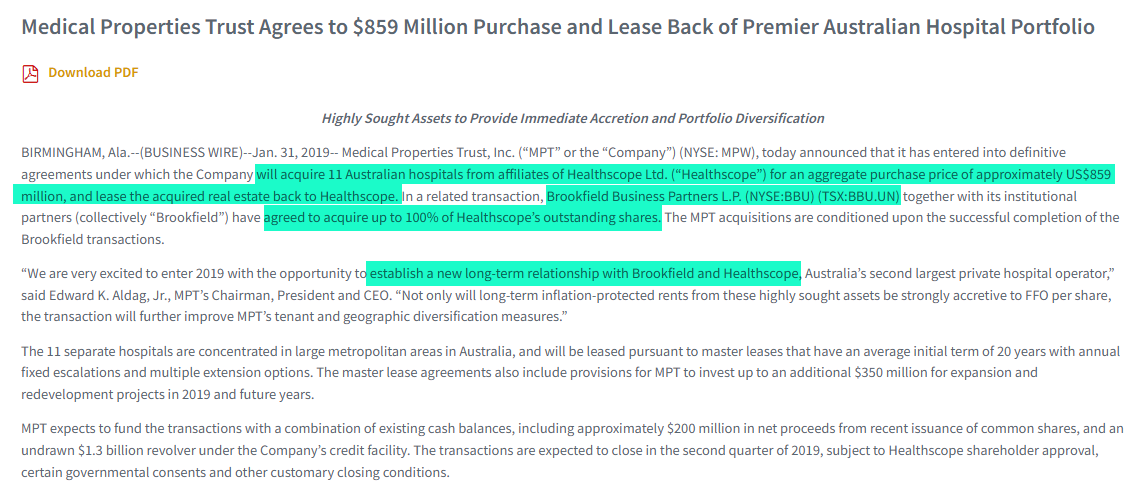

Add one more to the MPT international trail of wreckage. HPA, Vibra, Alecto, Adeptus, Caremax, Watsonville, Steward, Prospect, Steward Int'l/Malta/Colombia... and now Healthscope into receivership.

MPT helped finance the acquisition of the OpCo by $BN back in 2019. Then had to defer rent and grant concessions to new owner to sell RE assets over 2022-2023, and lost money all-in on the deal. OpCo blows up.

Sound familiar? When @PrioryGroup ? When @SwissMedicalNet ?

Link: x.com/Jonathan_Keith…

Add one more to the MPT international trail of wreckage. HPA, Vibra, Alecto, Adeptus, Caremax, Watsonville, Steward, Prospect, Steward Int'l/Malta/Colombia... and now Healthscope into receivership.

MPT helped finance the acquisition of the OpCo by $BN back in 2019. Then had to defer rent and grant concessions to new owner to sell RE assets over 2022-2023, and lost money all-in on the deal. OpCo blows up.

Sound familiar? When @PrioryGroup ? When @SwissMedicalNet ?

Link: x.com/Jonathan_Keith…

"MPT was here..." $MPW

Loot the system. Pay yourselves for doing so, on the back of a fraudulent Ponzi scheme (round-tripping rents via loans). Destroy system financially. Finance remaining "rent" on back of unpaid vendors and starving hospitals of CAPX. Unsecured creditors get nothing.

Move on to next fraudulent scheme (HAS, Insight, etc.).

Complete and total disaster. Remember first day hearing where was said "lots of value here?"

This is MPT's business model.

Loot the system. Pay yourselves for doing so, on the back of a fraudulent Ponzi scheme (round-tripping rents via loans). Destroy system financially. Finance remaining "rent" on back of unpaid vendors and starving hospitals of CAPX. Unsecured creditors get nothing.

Move on to next fraudulent scheme (HAS, Insight, etc.).

Complete and total disaster. Remember first day hearing where was said "lots of value here?"

This is MPT's business model.

"MPT was here..." $MPW

Since Aldag uttered these words in April 2022, the following tenants have filed for BK, receivership or otherwise been restructured/recapped (that we know of):

- Pipeline Health,

- Prospect Medical,

- Alecto,

- Vibra,

- Swiss Medical,

- Steward, and

- Healthscope.

This was roughly ~45% of MPT's consolidated rent roll as of Q1:22, excl. SMN which is a UJV.

Since Aldag uttered these words in April 2022, the following tenants have filed for BK, receivership or otherwise been restructured/recapped (that we know of):

- Pipeline Health,

- Prospect Medical,

- Alecto,

- Vibra,

- Swiss Medical,

- Steward, and

- Healthscope.

This was roughly ~45% of MPT's consolidated rent roll as of Q1:22, excl. SMN which is a UJV.

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh