According to Ray Dalio, the easiest way to adjust for risk is to seek uncorrelated returns.

Ray's made billions from a simple idea.

Here's how to do it in a few lines of Python code:

Ray's made billions from a simple idea.

Here's how to do it in a few lines of Python code:

Step 1: Collect Stock Data

Run this code to download free stock price data from Yahoo Finance.

Run this code to download free stock price data from Yahoo Finance.

Step 2: Convert Prices to Returns

Using pandas code, we can get returns (just run this code):

Using pandas code, we can get returns (just run this code):

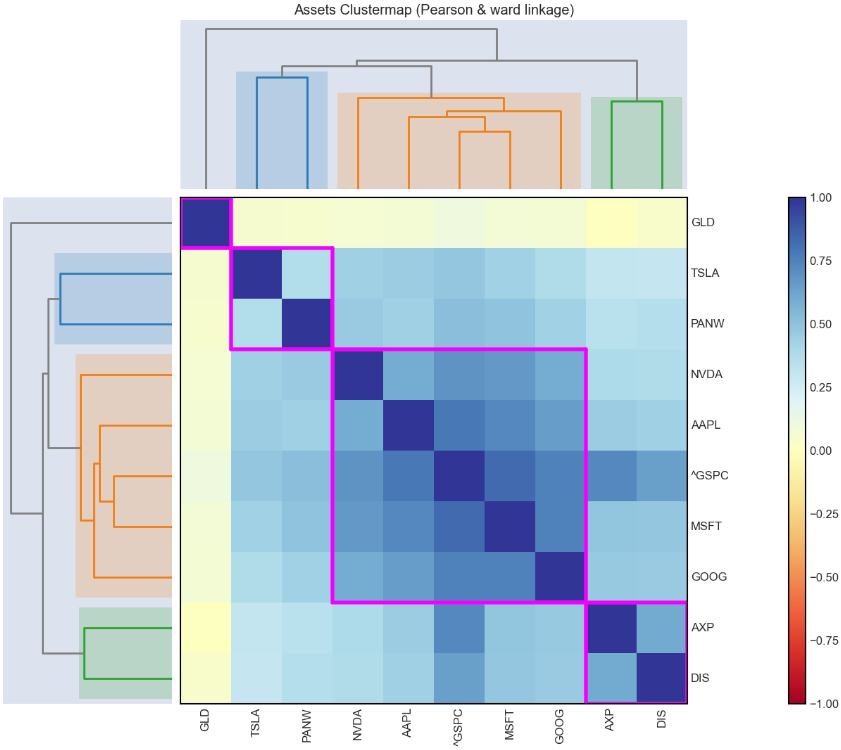

Step 3: Use Riskfolio's Plot Clusters

This function takes our returns and creates a hierarchical dendrogram based on Pearson correlation of the stock returns.

This function takes our returns and creates a hierarchical dendrogram based on Pearson correlation of the stock returns.

Step 4: Analyze the plot

Select Stocks from different buckets that exhibit lower correlation to others in your portfolio.

Example:

GLD, TSLA, NVDA, AXP would be less correlated than AAPL, MSFT, NVDA, GOOG.

Select Stocks from different buckets that exhibit lower correlation to others in your portfolio.

Example:

GLD, TSLA, NVDA, AXP would be less correlated than AAPL, MSFT, NVDA, GOOG.

Step 5: Become a Quant Scientist

Once you realize that trading with algorithms gives you an edge, the next step is to learn how to exploit that edge.

We want to help.

Once you realize that trading with algorithms gives you an edge, the next step is to learn how to exploit that edge.

We want to help.

On March 26th, we are hosting a free workshop to help you get started with algorithmic trading with Python.

Register here (500 seats): learn.quantscience.io/qs-register

Register here (500 seats): learn.quantscience.io/qs-register

That's a wrap! Over the next 24 days, I'm sharing my top 24 algorithmic trading concepts to help you get started.

If you enjoyed this thread:

1. Follow me @quantscience_ for more of these

2. RT the tweet below to share this thread with your audience

If you enjoyed this thread:

1. Follow me @quantscience_ for more of these

2. RT the tweet below to share this thread with your audience

https://twitter.com/1683526993059430411/status/1903418770930200916

• • •

Missing some Tweet in this thread? You can try to

force a refresh