1)

April 2025: The Moment of Structural Recognition

As of April 2, 2025, the U.S. macro-financial system is entering a phase of nonlinear fragility, defined by an accelerating convergence of debt rollover constraints, household credit exhaustion, and commercial real estate insolvency. While markets remain technically solvent and rates off their 2023 highs, the underlying momentum is negative and self-reinforcing.

This is no longer a question of soft landing vs hard landing. The high-probability path forward is a deep recession. The only variable is whether the Federal Reserve will act quickly enough to prevent it from becoming disorderly.

Structural Drivers of Recession (Q2 2025–Q2 2026)

1. Sovereign Debt Rollover Constraint

•$9.2 trillion in U.S. Treasury debt matures in 2025, the largest 12-month rollover on record.

•Most of this debt was issued at sub-2% coupons. Current market rates are 4.19% on the 10-year, 4.5–5% on short-dated bills.

•Rolling this debt increases interest expense by $400B–$500B/year, crowding out other federal spending.

•Yield suppression is now a monetary imperative. The Fed must lower rates or trigger a bond buyer revolt.

2. Commercial Real Estate Maturity Cliff

•20% of all CRE debt (~$1 trillion) matures in 2025.

•Office asset values are down 25–40%. Many loans cannot be refinanced without loss recognition.

•Regional banks—who hold over 60% of CRE exposure—face rising credit impairment and shrinking equity buffers.

•CRE is now a contagion vector for the broader credit system.

3. Consumer Credit Stress

•FHA mortgage delinquencies: 11.03%

•VA delinquencies: 4.70%

•Subprime auto loans: 6.1%+ default rate

•Credit card delinquencies are climbing fast. Personal savings rate is near post-pandemic lows.

•Consumers are already underwater—before unemployment has begun to rise.

4. Monetary Policy Constraints

•Fed Funds Rate: 4.25–4.50%. Inflation still above 3% (CPI), core sticky.

•Political environment prevents large-scale QE or fiscal stimulus unless a crisis breaks first.

•Fed balance sheet remains above $7.5 trillion—limited room to absorb another shock without risking USD credibility.

April 2025: The Moment of Structural Recognition

As of April 2, 2025, the U.S. macro-financial system is entering a phase of nonlinear fragility, defined by an accelerating convergence of debt rollover constraints, household credit exhaustion, and commercial real estate insolvency. While markets remain technically solvent and rates off their 2023 highs, the underlying momentum is negative and self-reinforcing.

This is no longer a question of soft landing vs hard landing. The high-probability path forward is a deep recession. The only variable is whether the Federal Reserve will act quickly enough to prevent it from becoming disorderly.

Structural Drivers of Recession (Q2 2025–Q2 2026)

1. Sovereign Debt Rollover Constraint

•$9.2 trillion in U.S. Treasury debt matures in 2025, the largest 12-month rollover on record.

•Most of this debt was issued at sub-2% coupons. Current market rates are 4.19% on the 10-year, 4.5–5% on short-dated bills.

•Rolling this debt increases interest expense by $400B–$500B/year, crowding out other federal spending.

•Yield suppression is now a monetary imperative. The Fed must lower rates or trigger a bond buyer revolt.

2. Commercial Real Estate Maturity Cliff

•20% of all CRE debt (~$1 trillion) matures in 2025.

•Office asset values are down 25–40%. Many loans cannot be refinanced without loss recognition.

•Regional banks—who hold over 60% of CRE exposure—face rising credit impairment and shrinking equity buffers.

•CRE is now a contagion vector for the broader credit system.

3. Consumer Credit Stress

•FHA mortgage delinquencies: 11.03%

•VA delinquencies: 4.70%

•Subprime auto loans: 6.1%+ default rate

•Credit card delinquencies are climbing fast. Personal savings rate is near post-pandemic lows.

•Consumers are already underwater—before unemployment has begun to rise.

4. Monetary Policy Constraints

•Fed Funds Rate: 4.25–4.50%. Inflation still above 3% (CPI), core sticky.

•Political environment prevents large-scale QE or fiscal stimulus unless a crisis breaks first.

•Fed balance sheet remains above $7.5 trillion—limited room to absorb another shock without risking USD credibility.

2)

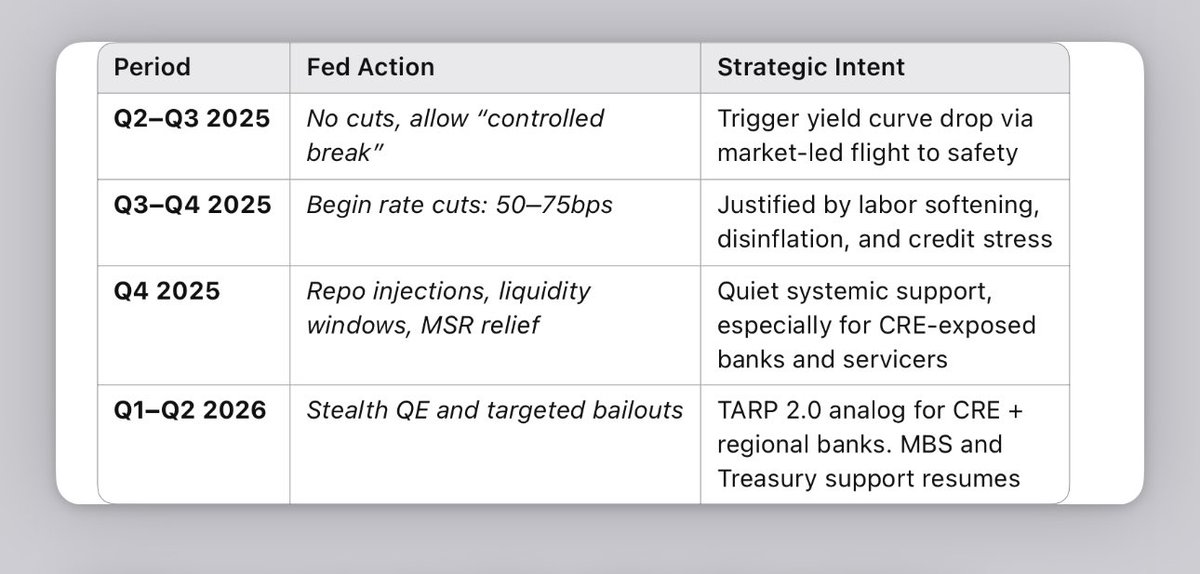

Fed’s Strategic Dilemma: Act or Collapse

Policy Options (Apr 2025–Apr 2026):

Failure to execute this path will result in a disorderly recession and potential financial system freeze.

Fed’s Strategic Dilemma: Act or Collapse

Policy Options (Apr 2025–Apr 2026):

Failure to execute this path will result in a disorderly recession and potential financial system freeze.

3)

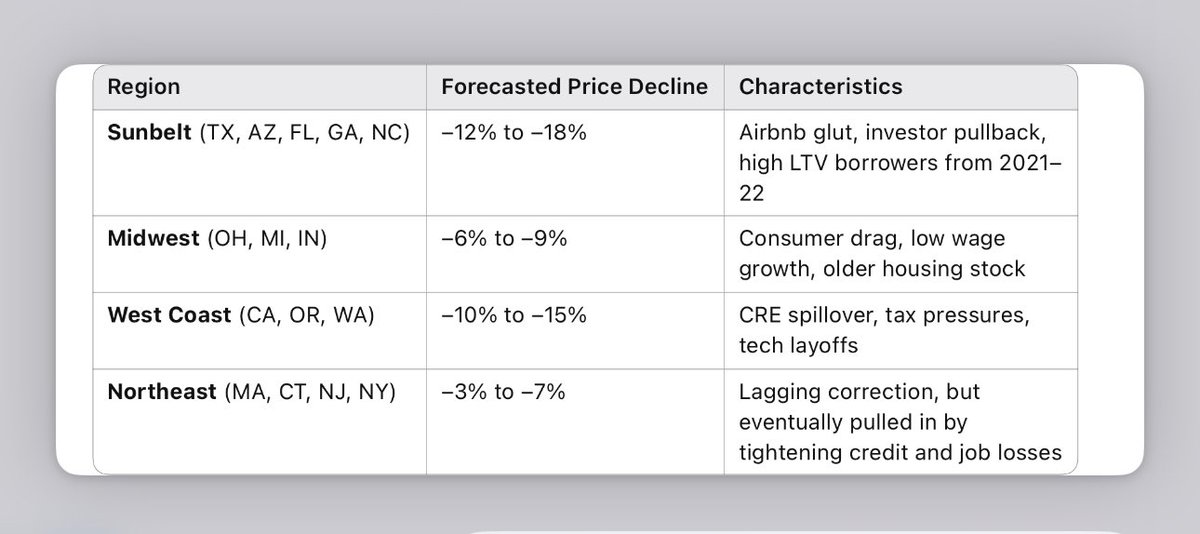

Housing Market Forecast: Q2 2025 – Q2 2026

National Median Home Price Change: –8.5% (Expected Value)

FHA/VA Concentration Zones

•Areas with >25% FHA origination share from 2020–2022 are most at risk for double-digit price drawdowns, forced selling, and rising REO inventory by Q4 2025.

Housing Market Forecast: Q2 2025 – Q2 2026

National Median Home Price Change: –8.5% (Expected Value)

FHA/VA Concentration Zones

•Areas with >25% FHA origination share from 2020–2022 are most at risk for double-digit price drawdowns, forced selling, and rising REO inventory by Q4 2025.

• • •

Missing some Tweet in this thread? You can try to

force a refresh