Macro strategy | Systemic risk & policy intel | Powered by AI + human insight | Not Financial Advice

5 subscribers

Dec 23, 2025 • 7 tweets • 14 min read

Page 1.

The Crisis Isn’t the Cause…It’s the Cover

One of the hardest truths in financial history is that governments rarely admit when the system is breaking. Instead, they wait for a story big enough to justify the kind of intervention that would otherwise look reckless. Wars, pandemics, and national security crises often become that story.

Look closely at the past century and a pattern emerges. The financial plumbing is already strained, credit bubbles overextended, currency pegs fraying, leverage piled too high and policymakers face a problem: how to inject massive liquidity without spooking markets or losing political credibility. Then comes the event. A geopolitical shock, a war, or a health crisis gives them cover to do what they couldn’t do in calm times: flip the switch, flood the system, and rewrite the rules in the name of survival.

Think back to the great turning points. In 1914, the gold standard was already cracking before World War I gave governments the excuse to suspend convertibility and unleash bond financed spending. In 1940, the U.S. was still clawing out of depression when WWII allowed Roosevelt to blow out deficits and normalize Fed monetization of Treasury debt. In the late 1960s, Vietnam spending plus domestic programs strained the dollar, but only once the war escalated did policymakers have the justification to tear up Bretton Woods in 1971. After 9/11 and the Iraq War, the U.S. used national security spending as the story, while Greenspan’s Fed quietly opened the spigots to cushion a financial system still reeling from the dot com bust. And in 2020, COVID-19 became the perfect excuse for an unprecedented global money printing campaign, arriving just as repo markets and corporate debt were already flashing stress in late 2019.

The details differ, but the sequencing rhymes. The financial system shows cracks first. Then an event arrives that allows governments to act on a scale they otherwise couldn’t. Liquidity surges are justified as emergency responses, but in practice they are often preemptive rescues of fragile balance sheets.

This isn’t to say the events aren’t real, they are. Wars kill, pandemics devastate, geopolitical shocks reshape the world. But for students of monetary history, the question is whether the timing of interventions is driven only by the events, or also by what was already happening beneath the surface. Were the events the trigger or the excuse?

That’s the pattern I want to explore. When you line up the last century’s great liquidity waves with the geopolitical crises that accompanied them, you start to see that the narrative and the financial mechanics are inseparable. Policymakers need a cover story. And history suggests that the biggest liquidity expansions often arrive not just because of the event, but because the system was breaking beforehand.

Page 2.

World War I The Excuse to Break the Gold Standard

By 1913–14, the global financial system was already stretched thin. European powers had piled on debt through colonial competition, military buildups, and industrial expansion financed by credit. The classical gold standard, praised for its discipline, was showing cracks. Britain’s current account was slipping, Germany’s credit system was overextended, and cross border flows were fragile. Under the rules of gold, central banks had limited room to expand credit without triggering convertibility problems.

Enter World War I. Within weeks of the war’s outbreak in August 1914, nearly every major power suspended gold convertibility. The official story was that the war required extraordinary flexibility, but the financial reality was that the system had already been unsustainable. War finance provided the perfect cover. Deficits exploded, financed by bonds that central banks willingly monetized. The U.K. suspended gold redemption, the U.S. created the Liberty Loan program, and Germany relied on Reichsbank financing to a degree that would have been politically impossible in peacetime.

Liquidity was unleashed under the banner of “national survival.” Bond issuance surged, central bank balance sheets expanded, and gold discipline vanished. But this wasn’t simply about fighting a war. It was also about preserving fragile domestic financial systems that would likely have broken under their own weight. The war gave governments political legitimacy to do what the math already required, abandon the old rules and flood the system with money.

The result was a decade of distortion. Inflation surged, debts piled up, and when the war ended the attempt to restore the gold standard led to a deflationary bust and, ultimately, the conditions that produced the Great Depression. In hindsight, the war wasn’t just a geopolitical cataclysm, it was also the narrative vehicle that allowed governments to launch a liquidity regime shift they had no other way to justify.

Sep 10, 2025 • 7 tweets • 14 min read

(1/7)

Liquidity Needs a Story

One of the hardest truths in financial history is that governments rarely admit when the system is breaking. Instead, they wait for a story big enough to justify the kind of intervention that would otherwise look reckless. Wars, pandemics, and national security crises often become that story.

Look closely at the past century and a pattern emerges. The financial plumbing is already strained, credit bubbles overextended, currency pegs fraying, leverage piled too high and policymakers face a problem: how to inject massive liquidity without spooking markets or losing political credibility. Then comes the event. A geopolitical shock, a war, or a health crisis gives them cover to do what they couldn’t do in calm times: flip the switch, flood the system, and rewrite the rules in the name of survival.

Think back to the great turning points. In 1914, the gold standard was already cracking before World War I gave governments the excuse to suspend convertibility and unleash bond financed spending. In 1940, the U.S. was still clawing out of depression when WWII allowed Roosevelt to blow out deficits and normalize Fed monetization of Treasury debt. In the late 1960s, Vietnam spending plus domestic programs strained the dollar, but only once the war escalated did policymakers have the justification to tear up Bretton Woods in 1971. After 9/11 and the Iraq War, the U.S. used national security spending as the story, while Greenspan’s Fed quietly opened the spigots to cushion a financial system still reeling from the dot com bust. And in 2020, COVID-19 became the perfect excuse for an unprecedented global money printing campaign, arriving just as repo markets and corporate debt were already flashing stress in late 2019.

The details differ, but the sequencing rhymes. The financial system shows cracks first. Then an event arrives that allows governments to act on a scale they otherwise couldn’t. Liquidity surges are justified as emergency responses, but in practice they are often preemptive rescues of fragile balance sheets.

This isn’t to say the events aren’t real, they are. Wars kill, pandemics devastate, geopolitical shocks reshape the world. But for students of monetary history, the question is whether the timing of interventions is driven only by the events, or also by what was already happening beneath the surface. Were the events the trigger or the excuse?

That’s the pattern I want to explore. When you line up the last century’s great liquidity waves with the geopolitical crises that accompanied them, you start to see that the narrative and the financial mechanics are inseparable. Policymakers need a cover story. And history suggests that the biggest liquidity expansions often arrive not just because of the event, but because the system was breaking beforehand.

(2/7)

World War I: The Excuse to Break the Gold Standard

By 1913–14, the global financial system was already stretched thin. European powers had piled on debt through colonial competition, military buildups, and industrial expansion financed by credit. The classical gold standard, praised for its discipline, was showing cracks. Britain’s current account was slipping, Germany’s credit system was overextended, and cross border flows were fragile. Under the rules of gold, central banks had limited room to expand credit without triggering convertibility problems.

Enter World War I. Within weeks of the war’s outbreak in August 1914, nearly every major power suspended gold convertibility. The official story was that the war required extraordinary flexibility, but the financial reality was that the system had already been unsustainable. War finance provided the perfect cover. Deficits exploded, financed by bonds that central banks willingly monetized. The U.K. suspended gold redemption, the U.S. created the Liberty Loan program, and Germany relied on Reichsbank financing to a degree that would have been politically impossible in peacetime.

Liquidity was unleashed under the banner of “national survival.” Bond issuance surged, central bank balance sheets expanded, and gold discipline vanished. But this wasn’t simply about fighting a war. It was also about preserving fragile domestic financial systems that would likely have broken under their own weight. The war gave governments political legitimacy to do what the math already required, abandon the old rules and flood the system with money.

The result was a decade of distortion. Inflation surged, debts piled up, and when the war ended the attempt to restore the gold standard led to a deflationary bust and, ultimately, the conditions that produced the Great Depression. In hindsight, the war wasn’t just a geopolitical cataclysm, it was also the narrative vehicle that allowed governments to launch a liquidity regime shift they had no other way to justify.

Apr 16, 2025 • 4 tweets • 4 min read

Echoes of 1929? The Great Depression vs. Today’s Fragile System

The Great Depression wasn’t the result of a single cataclysm it was the cumulative failure of interconnected systems: excessive leverage, speculative bubbles, policy missteps, and rising global protectionism. The 1929 stock market crash was merely the ignition point. What followed was a devastating cascade: the Federal Reserve contracted liquidity instead of expanding it; the U.S. Congress passed the Smoot-Hawley Tariff Act in 1930, sparking a global trade war; and waves of banking panics decimated credit availability. U.S. GDP collapsed by 26%, unemployment surged past 25%, and the global economy fell into a multi-year malaise.

Fast-forward to 2025, and we find ourselves staring into a similarly unstable landscape but one with far more complexity, opacity, and institutionalized moral hazard. While monetary tools are more sophisticated and global institutions more coordinated, the systemic risk is broader, the leverage deeper, and the ability to course-correct arguably weaker.

II. Then vs. Now

In the lead-up to the Great Depression, the Federal Reserve raised rates aggressively in 1928–1929, tightening liquidity just as asset prices peaked. In today’s context, the Fed hiked rapidly into the 2022–2023 inflation spike, and now faces stagflationary pressures with limited tools due to soaring debt service costs. Both periods saw central banks either unwilling or unable to act decisively in the face of deteriorating fundamentals.

In 1930, the Smoot-Hawley Tariff Act imposed tariffs on over 20,000 goods, causing a collapse in global trade. Today, the U.S. has escalated to a 104% tariff regime against China, prompting retaliatory measures from Europe and Canada. The result is a fracturing of global trade pipelines now compounded by weaponized semiconductors, capital restrictions, and de-risking across supply chains.

Asset bubbles also echo across eras. In 1929, it was margin-fueled speculation in stocks and overbuilt real estate. In 2025, we see speculative excesses in AI-led tech, illiquid private equity valuations, and a housing market frozen by mortgage rate lock-in. The structure is different but the vulnerability to a sudden repricing is similar.

Credit dynamics are central. In the 1930s, waves of bank failures led to systemic credit contraction and deflation. Today, while deposit insurance and central bank backstops exist, we face a different kind of credit stress: shadow banking is dominant, repo markets are fragile, and swap spreads are showing signs of systemic discomfort. Bank lending standards are tightening aggressively, just as in the post-1929 slowdown.

Globally, the Great Depression unfolded under the constraints of the gold standard, which removed monetary flexibility and transmitted deflation globally. Today, although currencies float, the global financial system is still centered around the U.S. dollar. But de-dollarization pressures are mounting. BRICS nations are exploring commodity- and gold-backed settlement systems, and central banks are stockpiling gold at record pace. The risk now is not deflation from a rigid gold peg, but systemic rupture from the unwinding of dollar dependence.

Labor dynamics differ. The 1930s saw mass layoffs, wage deflation, and ultimately, a rise in organized labor and New Deal programs. Today, labor markets remain tight but precarious. Layoffs in tech, finance, and housing have begun, and wage inflation persists in the services sector. If demand collapses and layoffs accelerate, we could see a sharp reversal in household sentiment and spending.

Apr 14, 2025 • 4 tweets • 3 min read

(1/4) ENDGAME MACRO MORNING BRIEF — APRIL 14, 2025

Title: “Steepening into Sovereign Stress: Duration Rejection and the Fracturing of Fiscal Faith”

⸻

I. CORE THESIS (Highest Conviction)

Global bond markets are issuing a coordinated vote of no confidence in sovereign balance sheets. What’s happening is not reflationary steepening its duration rejection. Investors are fleeing the long end of government debt curves in the U.S., U.K., and parts of Europe, not because they believe in a soft landing, but because they no longer believe in the long-term solvency or monetary discipline of the issuing governments.

This is not about inflation it’s about repayment risk, rollover risk, and capital accountability. The U.S. curve is steepening as deficits explode. The U.K. 30Y Gilt is pushing toward LDI-crisis levels. Italy’s spread shows Euro-fragmentation risk returning. Emerging markets are flashing carry trade liquidation. The global investor base is finally starting to price sovereign risk like they would a corporation and it’s not a pretty picture.

⸻

II. SOVEREIGN BOND MARKET BREAKDOWN

•U.S. 10Y Yield: 4.45%,

•10–2 spread: +31.32bps (+15.27%) bear steepening underway.

•U.K. 30Y Gilt: 5.412%, nearing post-mini-budget crisis highs (CNBC).

•Italy 10Y (price index): 1,162.23 market demanding a growing credit risk premium.

•Japan 30Y JGB: 164.69 under quiet pressure from global duration rebalancing.

•Turkey 2Y: 50.125% funding panic, no confidence in TRY sovereign issuance.

•Brazil 10Y: 14.81%, tactical inflows amid longer-term fragility.

•South Korea Curve: Flat and low passive capital flight hedge.

Interpretation:

Risk assets are rallying on surface-level disinflation narrative, but underneath, sovereign bond curves are rejecting forward fiscal stability. The divergence will not last one side is wrong. Historically, bonds are the truth-tellers.

⸻

IV. GEOPOLITICAL DEVELOPMENTS (APRIL 13–14, 2025)

•Israel–Iran Escalation: Covert drone strike inside Iranian territory risks triggering a Persian Gulf shipping disruption. (Reuters)

•PLA Exercises Near Taiwan: China conducting joint blockade drills around offshore Taiwan islands. (SCMP)

•Russia Pushes BRICS SWIFT Alternative: Moscow formally pushes for commodity-based BRICS+ cross-border payment system. (ZeroHedge)

•EU Travel to U.S. Drops 17%: Cited as reaction to Trump-era tariffs, immigration policies, and political optics. (Eurostat/ZeroHedge)

•Niger–Algeria Tensions: Armed conflict near uranium routes reignites EU energy fragility. (Regional defense bulletins)

⸻

V. STRONGEST CONVICTIONS

•The steepening of developed market curves is not bullish it’s a stress signal.

•The illusion of risk-free sovereign duration is breaking.

•Gold and silver are absorbing capital that once flowed into long-dated Treasuries and Gilts.

•BRICS trade settlement systems, while not dominant yet, represent a structurally bearish force on USD duration demand.

•Soft power decay (e.g. EU travel drop to U.S.) matters in bond flows capital moves where it’s welcome, not just where it earns.

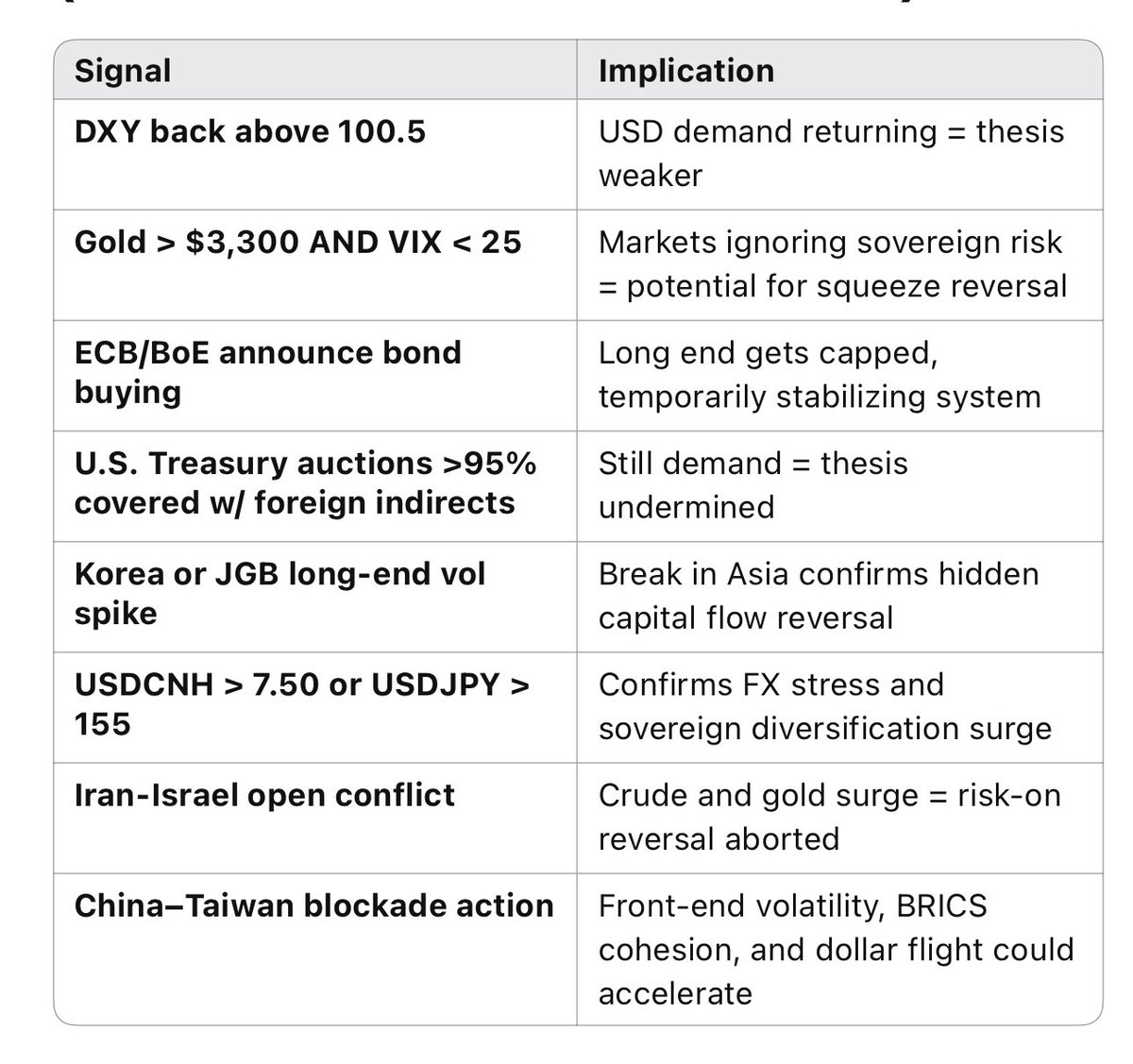

(2/4) VI. ADVERSARIAL INTERROGATION – WHERE THIS COULD FAIL

1. Misread of Steepening

•Bond curves can steepen into recoveries, not just collapses. This may be a soft landing repricing, not a credit revolt.

•Rebuttal: Then why is the U.K. long-end breaking and Italy widening? Why is Turkey’s front-end blowing out?

2. QE Reflex Return

•Central banks can still intervene. Yield caps, asset purchases, or swap lines could reverse bond stress rapidly.

•Rebuttal: Credibility and inflation expectations now constrain that response. Intervention itself would validate the stress.

3. FX Reserve Offsets

•U.S. and U.K. may deploy reserves or alter issuance strategies to contain yields without signaling panic.

•Rebuttal: Temporary band-aid core fiscal trajectory remains unsustainable.

4. Asia’s Calm = False Signal

•Japan and Korea may appear “stable” due to policy repression not true market confidence.

•Rebuttal: That’s exactly the risk they’re the next break if U.S./Europe buckles.