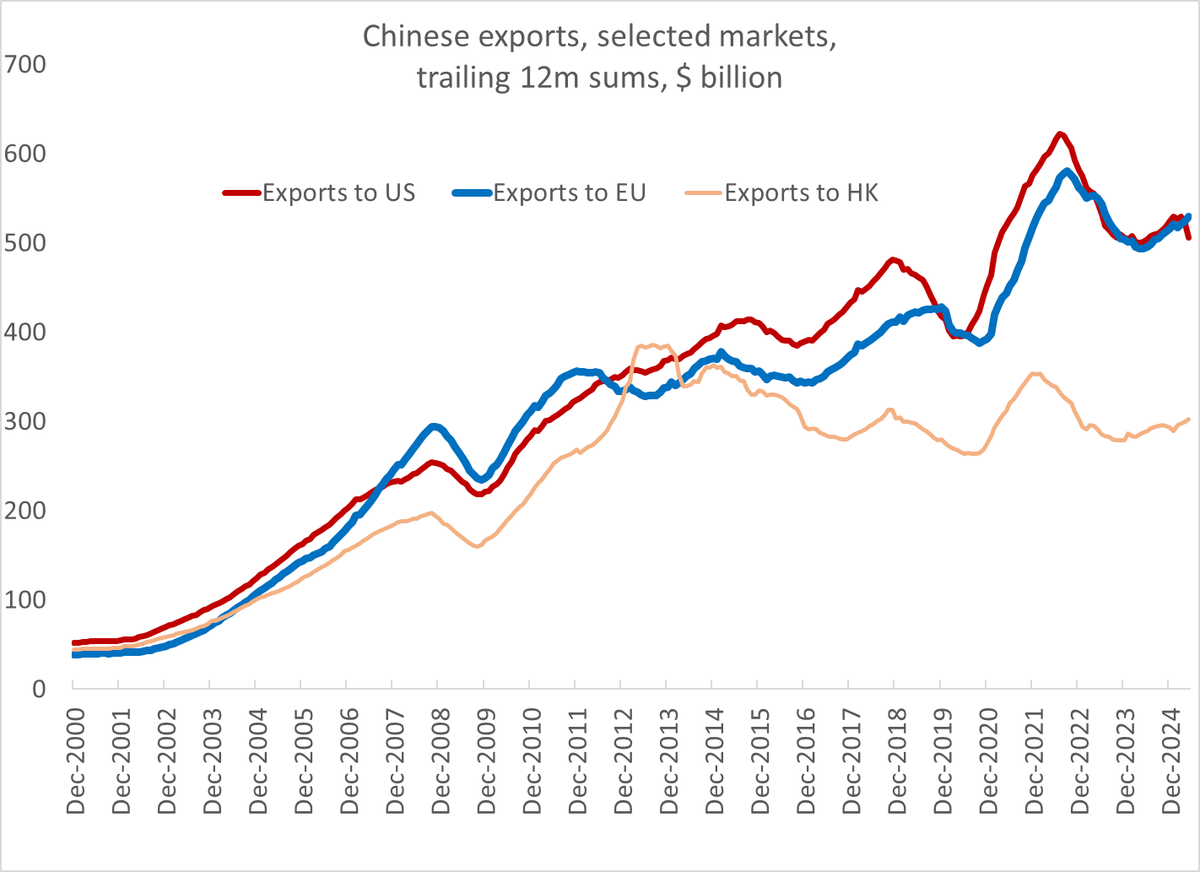

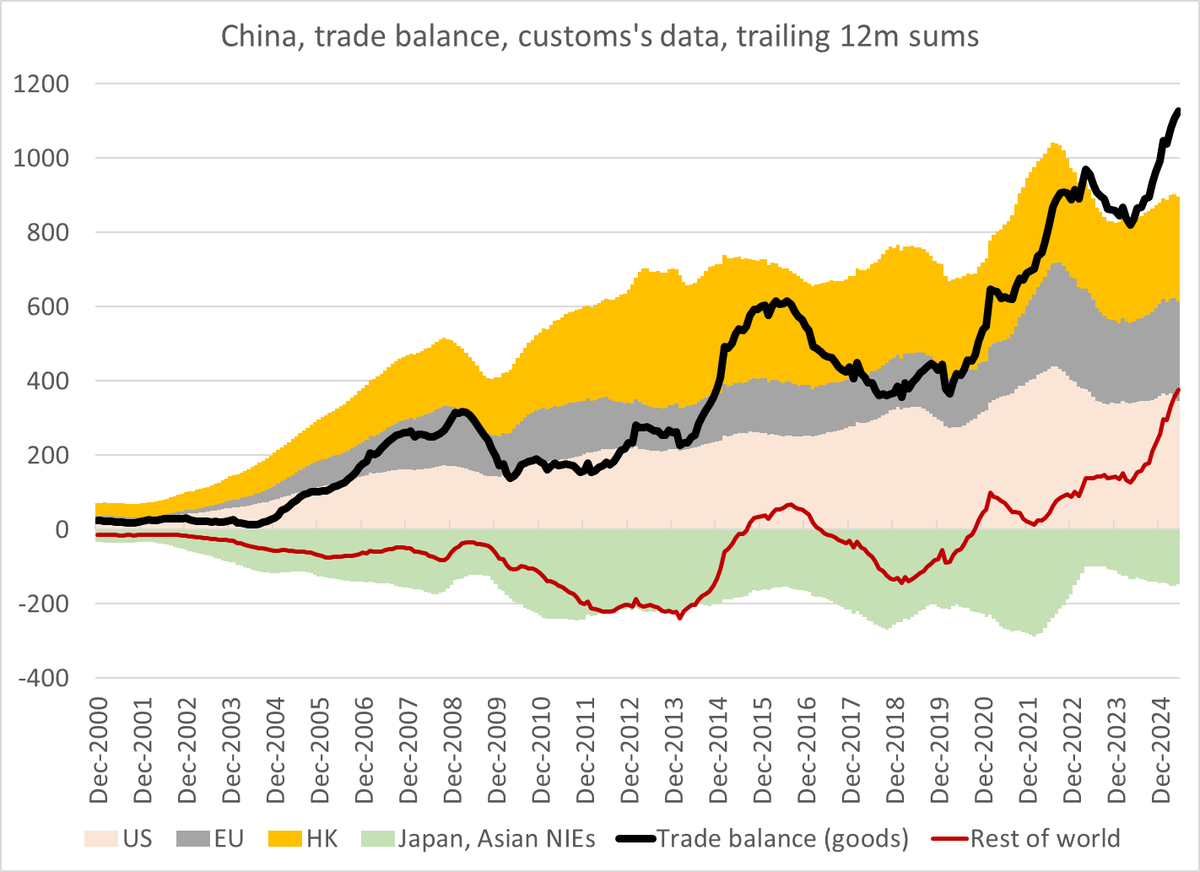

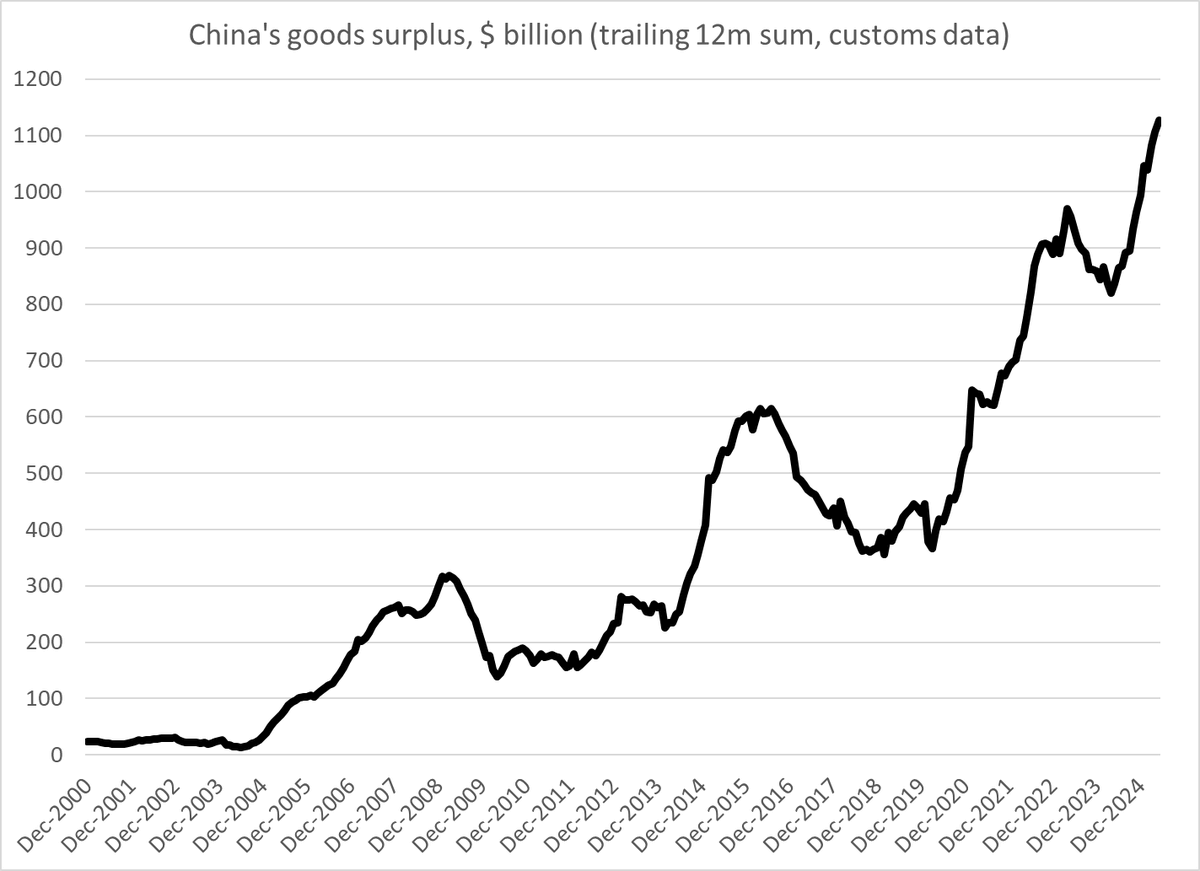

Don't think Xi is feeling that much pressure from Trump's trade war. Exports to the US dipped, but exports to the rest of the world largely offset. The overall monthly goods surplus still topped $100b/ is on track to hit $1.2 trillion (gulp)

1/

1/

Export volume growth dipped to 8% (estimate based on April prices). Import volumes fell 4% (not good).

Net exports are still driving China's economy.

2/

Net exports are still driving China's economy.

2/

The trade war impact is there if you know where to look -- exports to the US were ~ $30b, and they normally would be ~$50b. The trailing 12m of exports to the US isn't tracking exports to Europe (an easy test)

3/

3/

The rise in the overall surplus now is coming from a rising surplus with the emerging world. Lower commodity prices, and a rising surplus with "connector" countries that sell on to the US

4/

4/

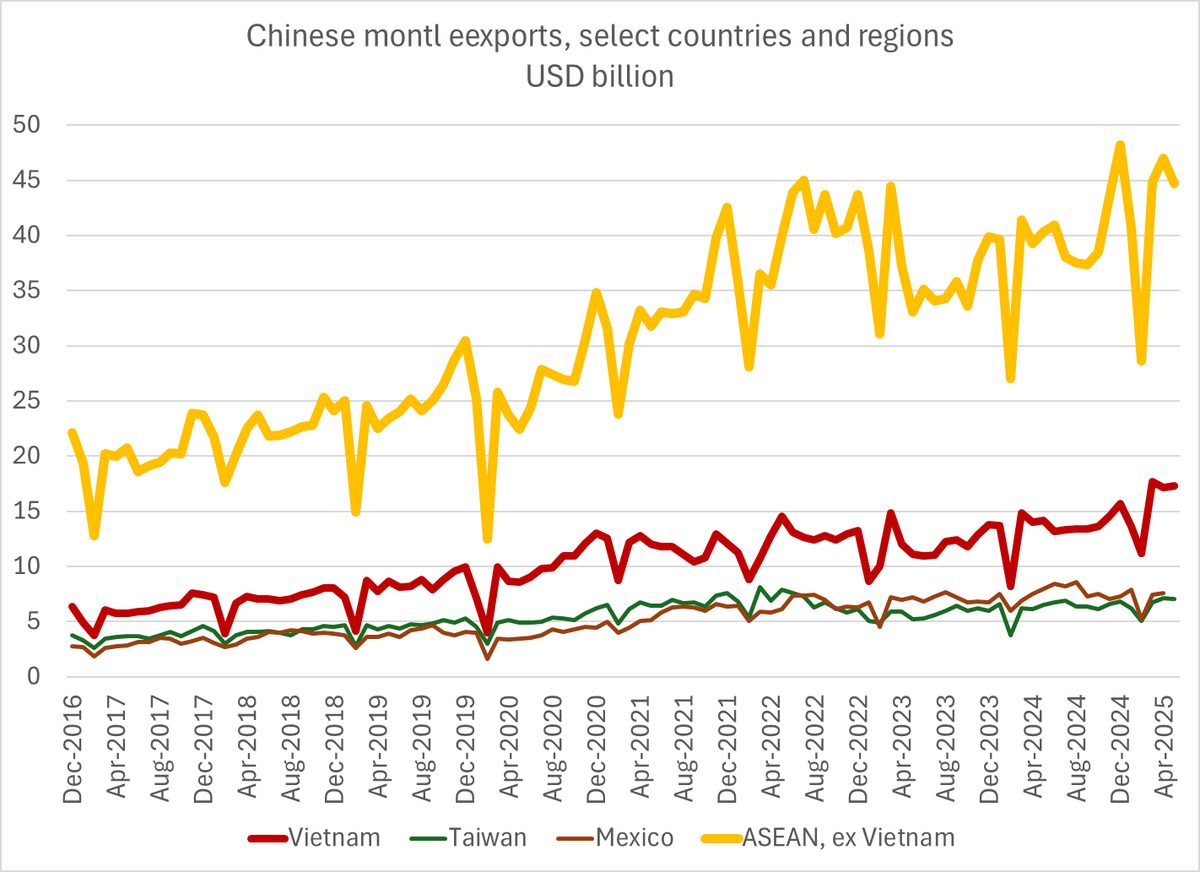

Unsurprisingly, exports to SE Asia are all up y/y

5/

5/

So far there are no real signs that I can see that Trump's go-it-alone tariffs have tamed China's export juggernaut

6/6

6/6

• • •

Missing some Tweet in this thread? You can try to

force a refresh