COATUE East Meet West Deck

102 Pages on Public Markets every investor should read

My highlights 🧵

1/ Tech Trends - higher returns & volatility

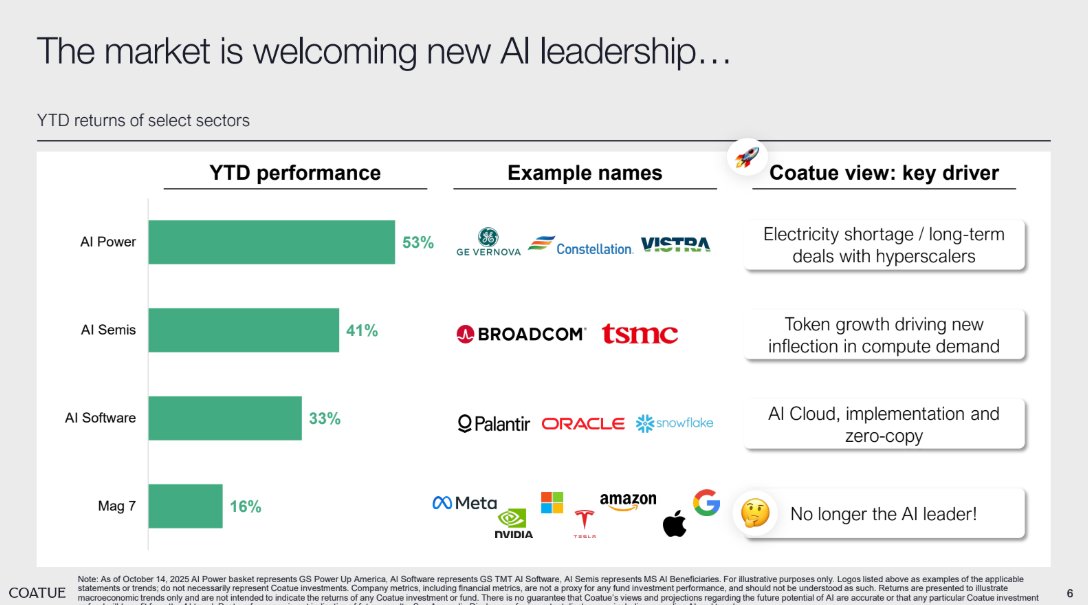

2/ Change in Stock Leadership - hard to stay on top

...

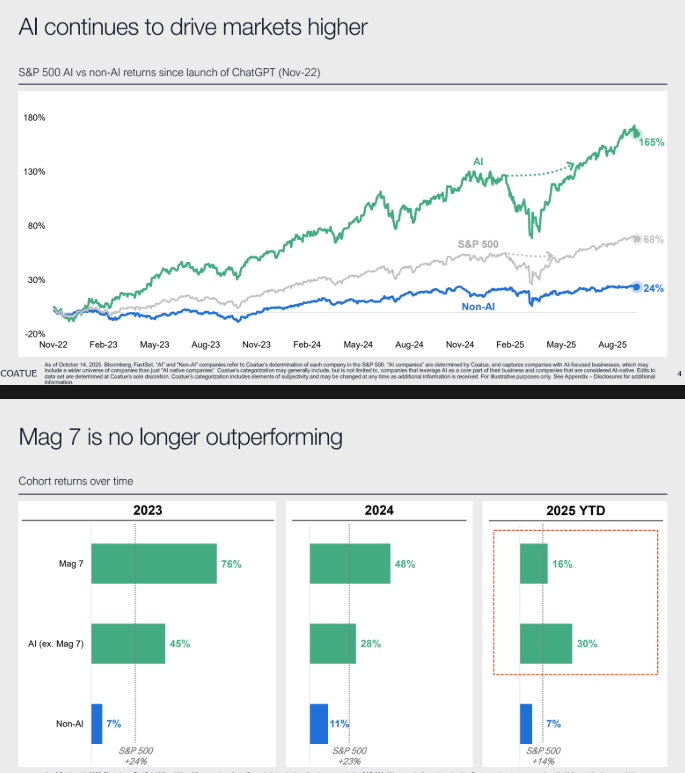

10/ The AI Flywheel

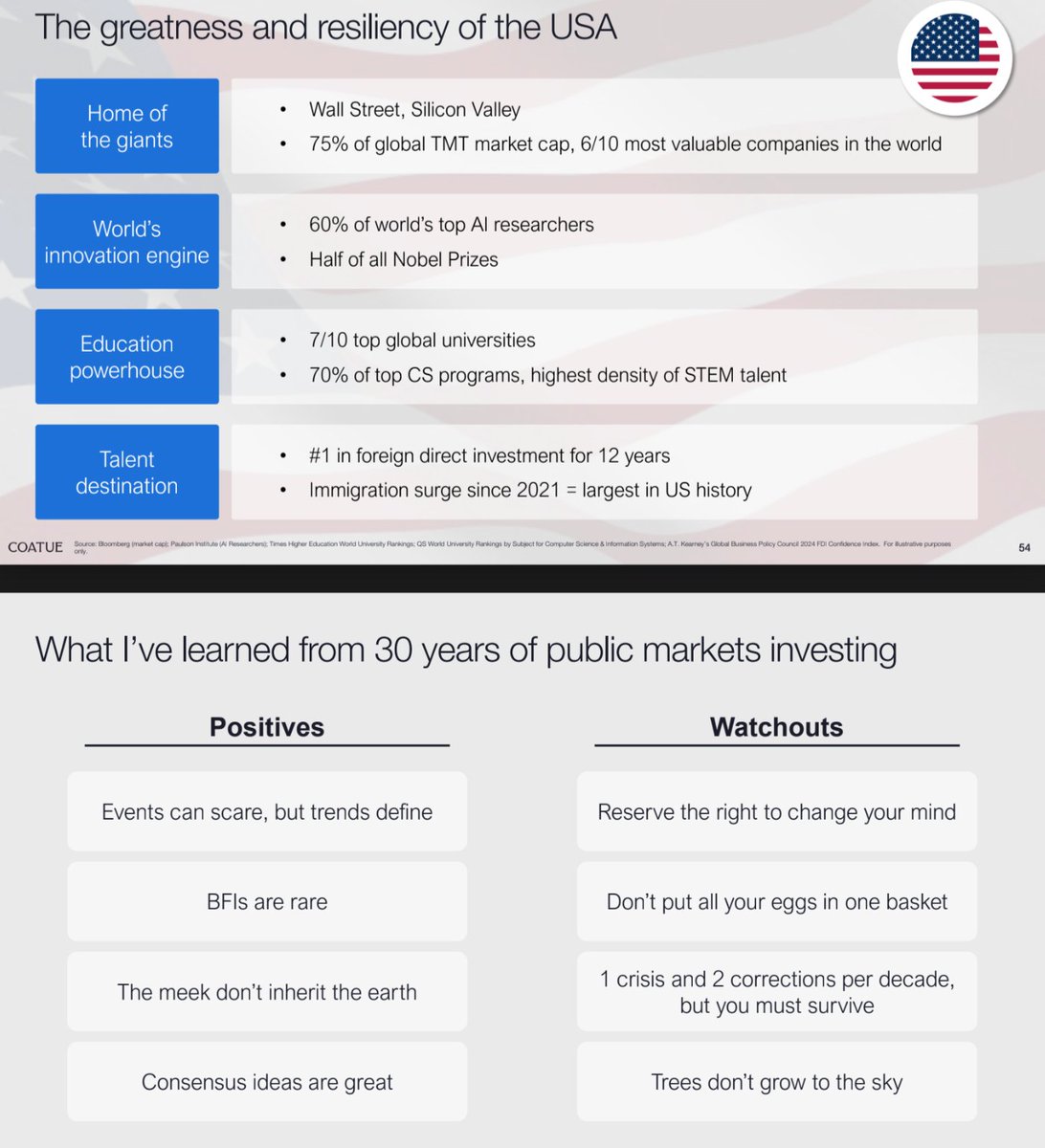

11/ Long the $USA

102 Pages on Public Markets every investor should read

My highlights 🧵

1/ Tech Trends - higher returns & volatility

2/ Change in Stock Leadership - hard to stay on top

...

10/ The AI Flywheel

11/ Long the $USA

1/ Tech Trends - higher returns but more volatility and drawdowns

2/ Change in Stock Leadership - hard to stay on top

3/ What happens to the dropouts?

4/ Are Mag 7 slowing down?

5/ BTC, the new risk / reward opportunity

6/ Hyperscaler Capex and Chat GPT Breakout

7/ AI starting to show its effects on spend and search

8/ Elevated valuations

9/ Studying drawdowns

10/ The AI Flywheel

11/ Long the $USA

• • •

Missing some Tweet in this thread? You can try to

force a refresh