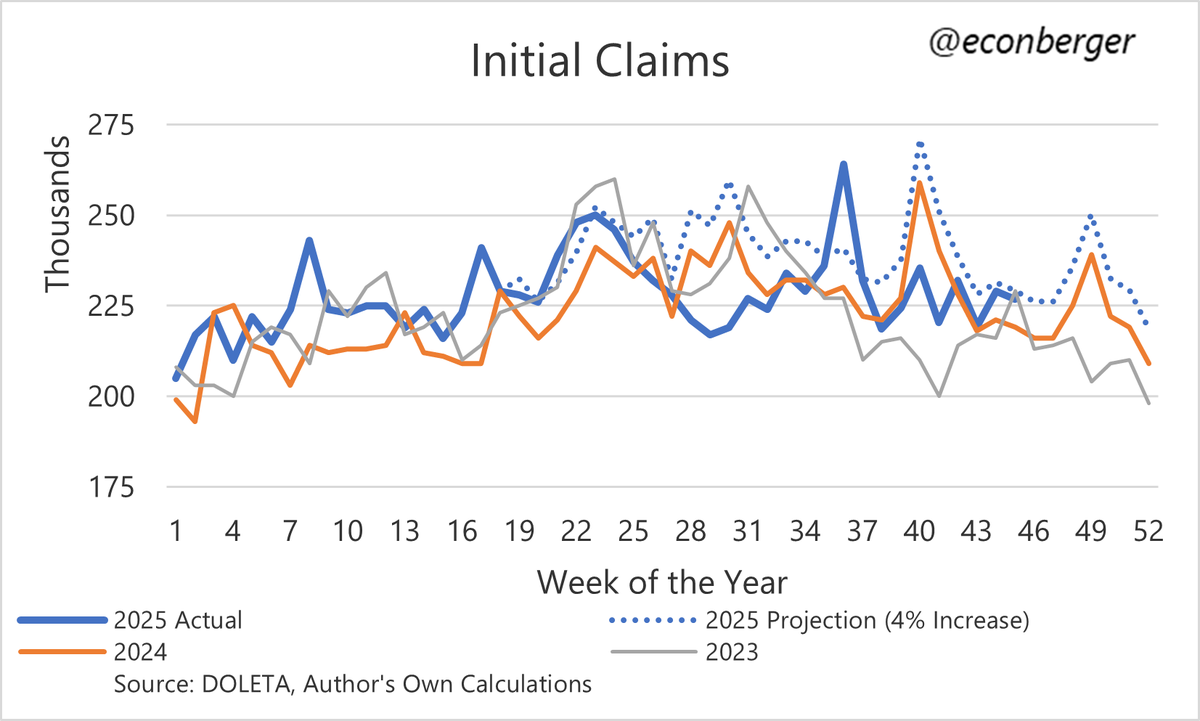

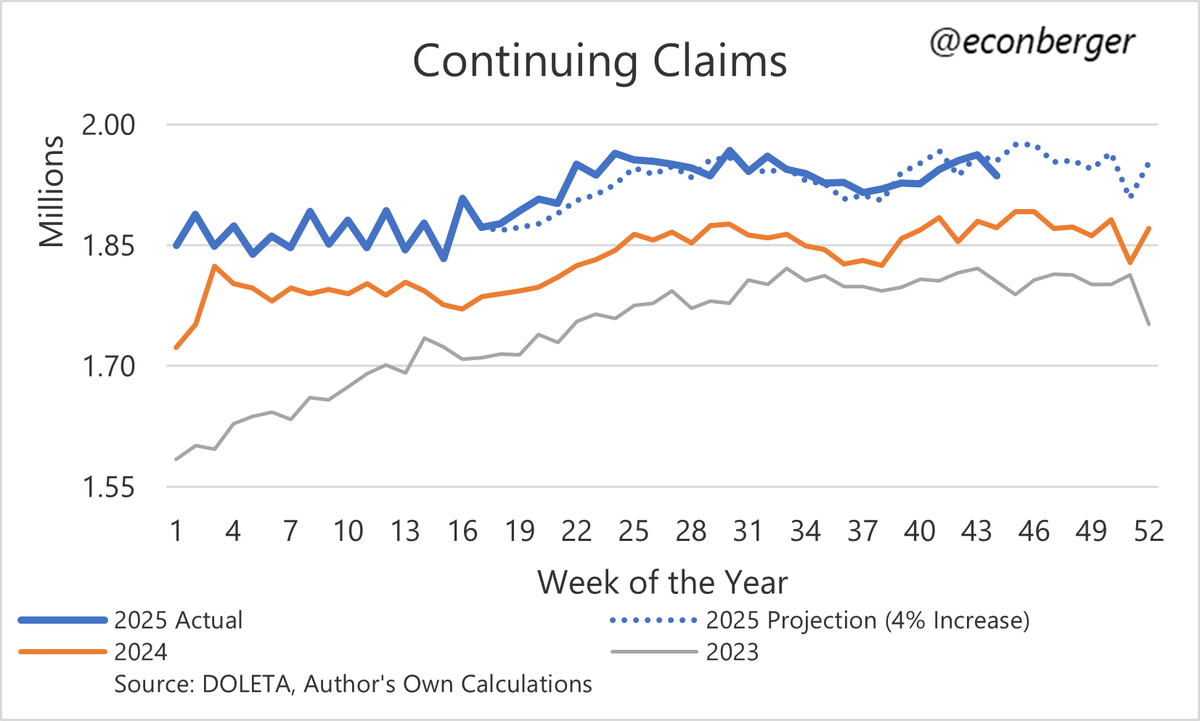

Claims:

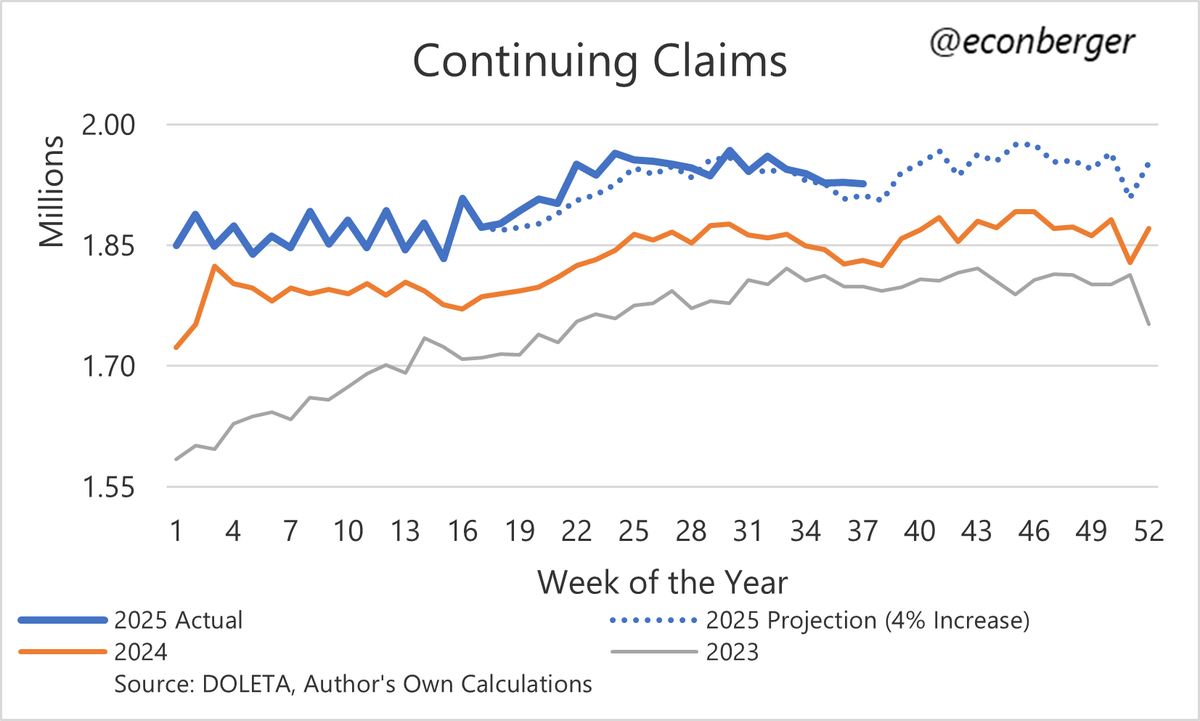

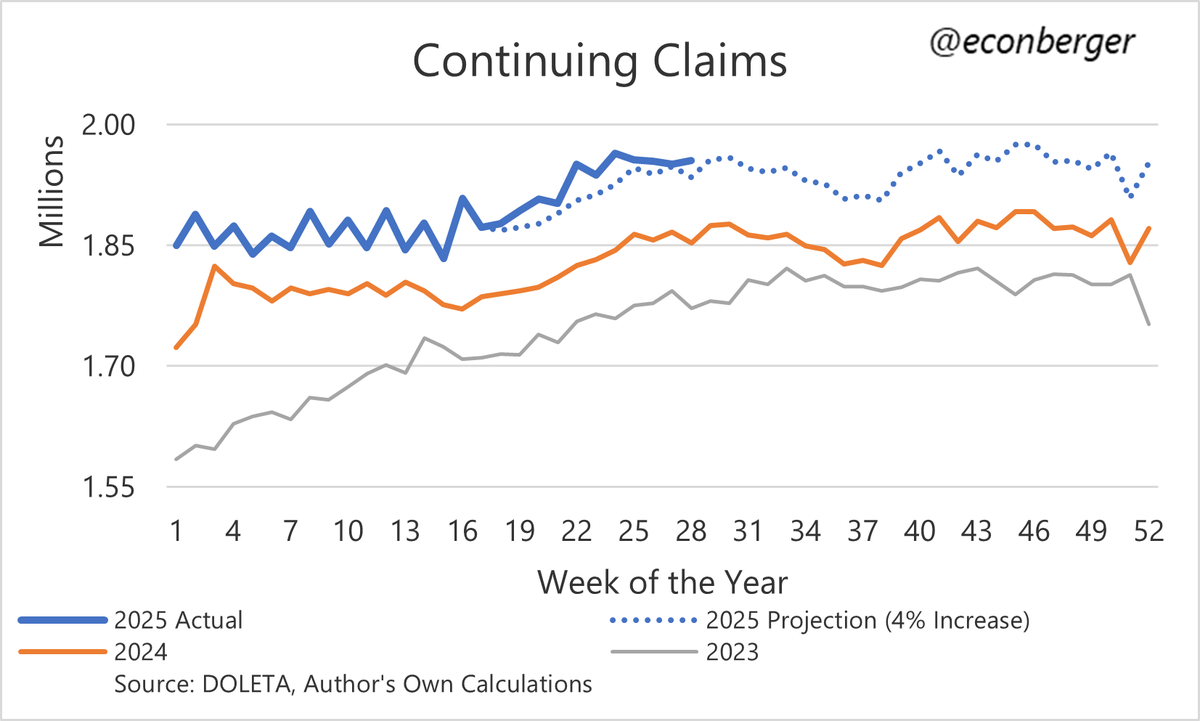

1/ Continuing claims a bit higher than I thought they would be, though still not that concerning.

We're probably going to be on a flattish trajectory in the published series for the remainder of the year due to residual seasonality.

1/ Continuing claims a bit higher than I thought they would be, though still not that concerning.

We're probably going to be on a flattish trajectory in the published series for the remainder of the year due to residual seasonality.

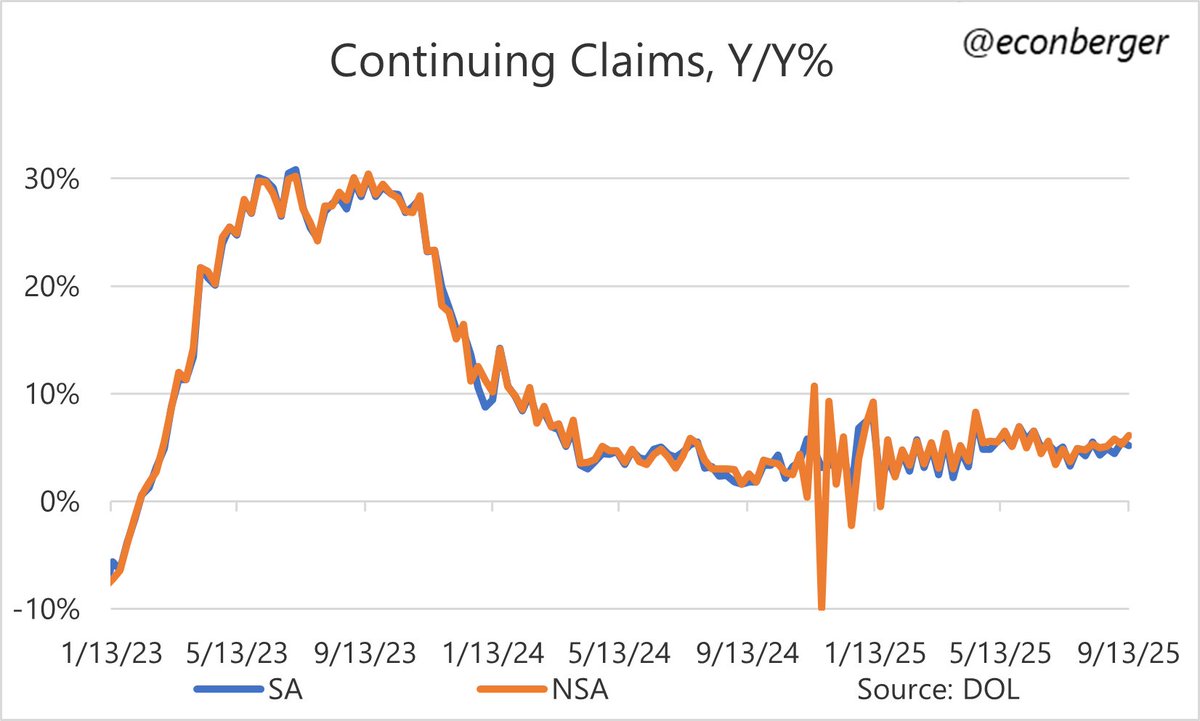

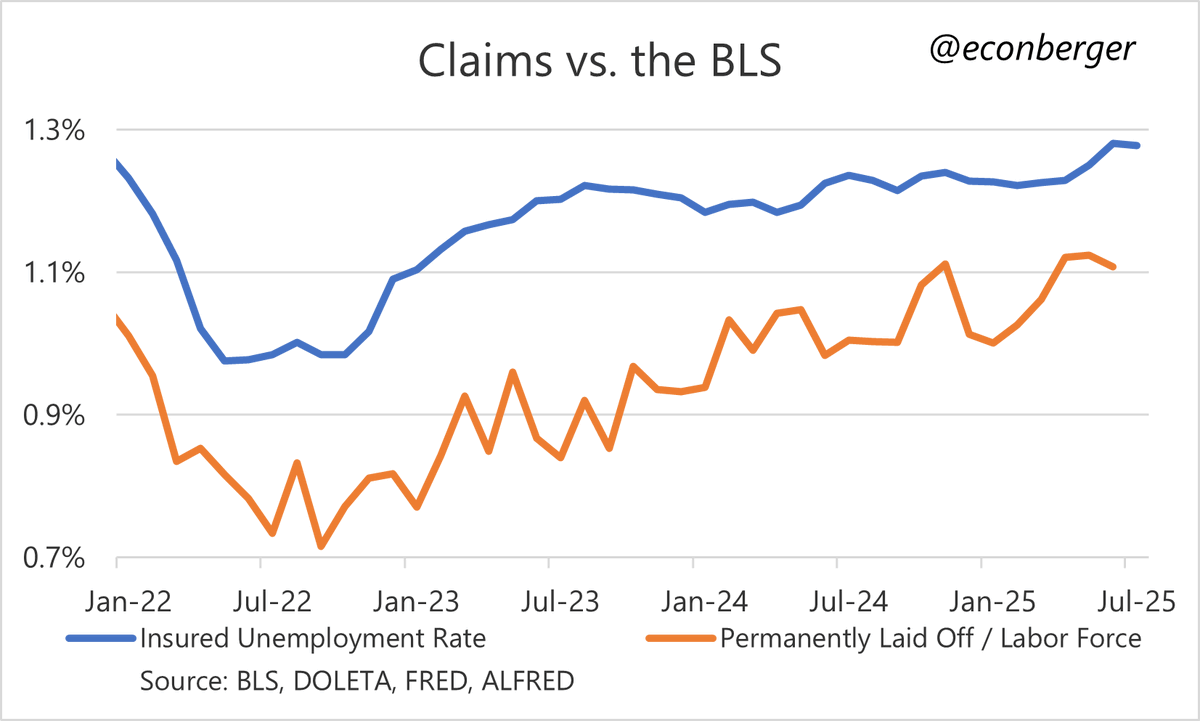

2/ That flattish trajectory in the published series is an overly benign portrayal of what is actually happening in the underlying data, which is an ongoing slow creep upward.

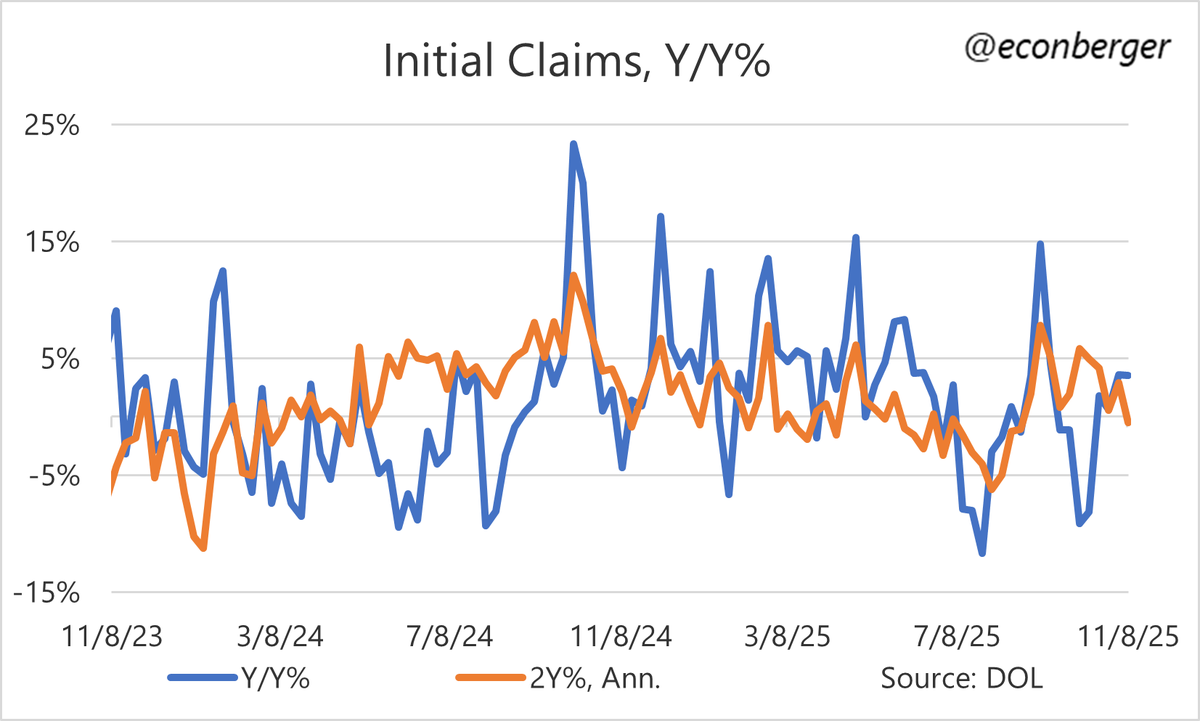

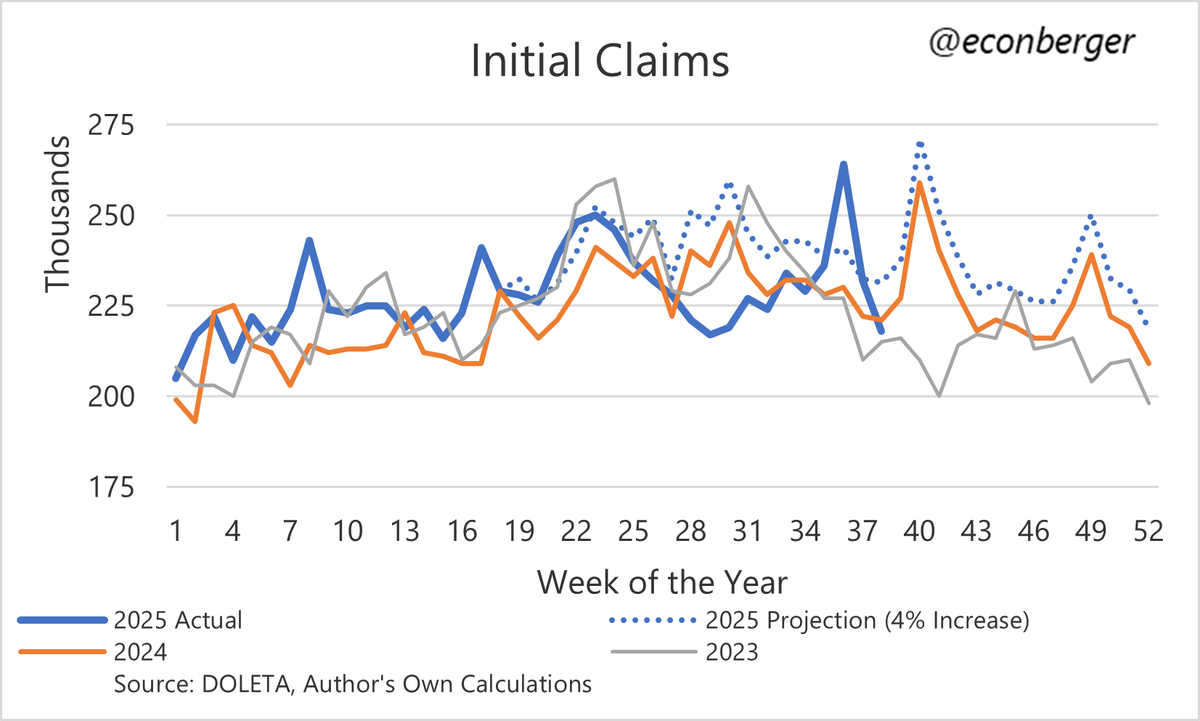

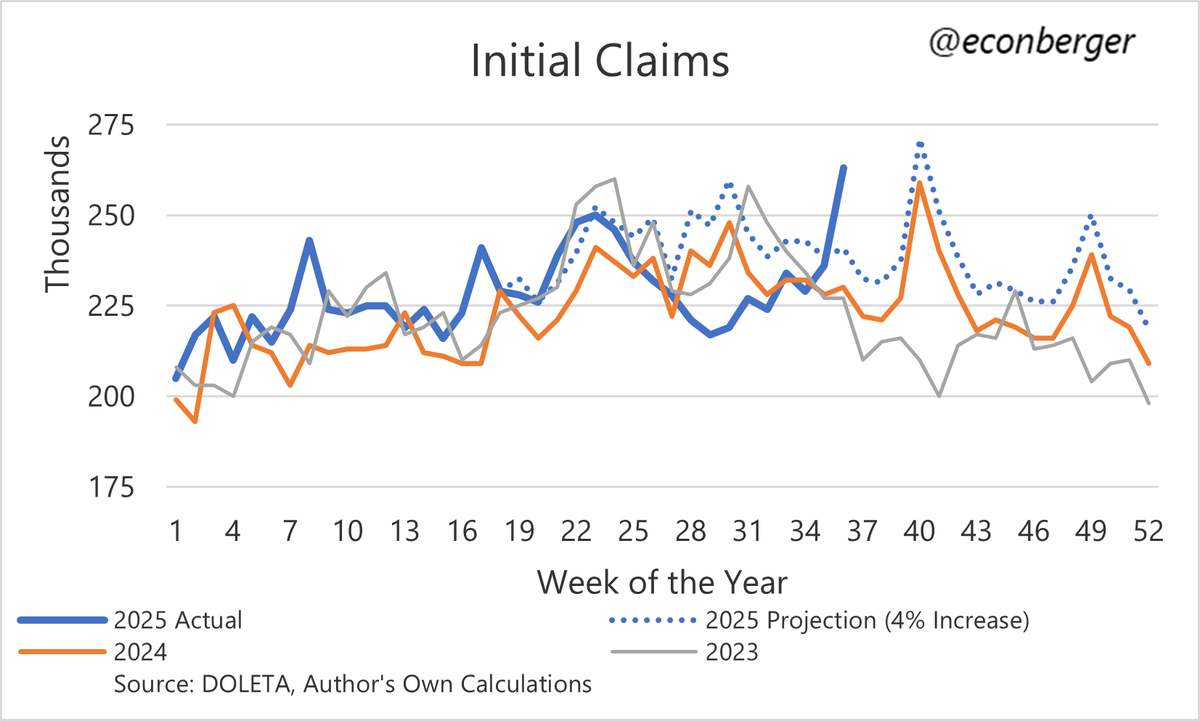

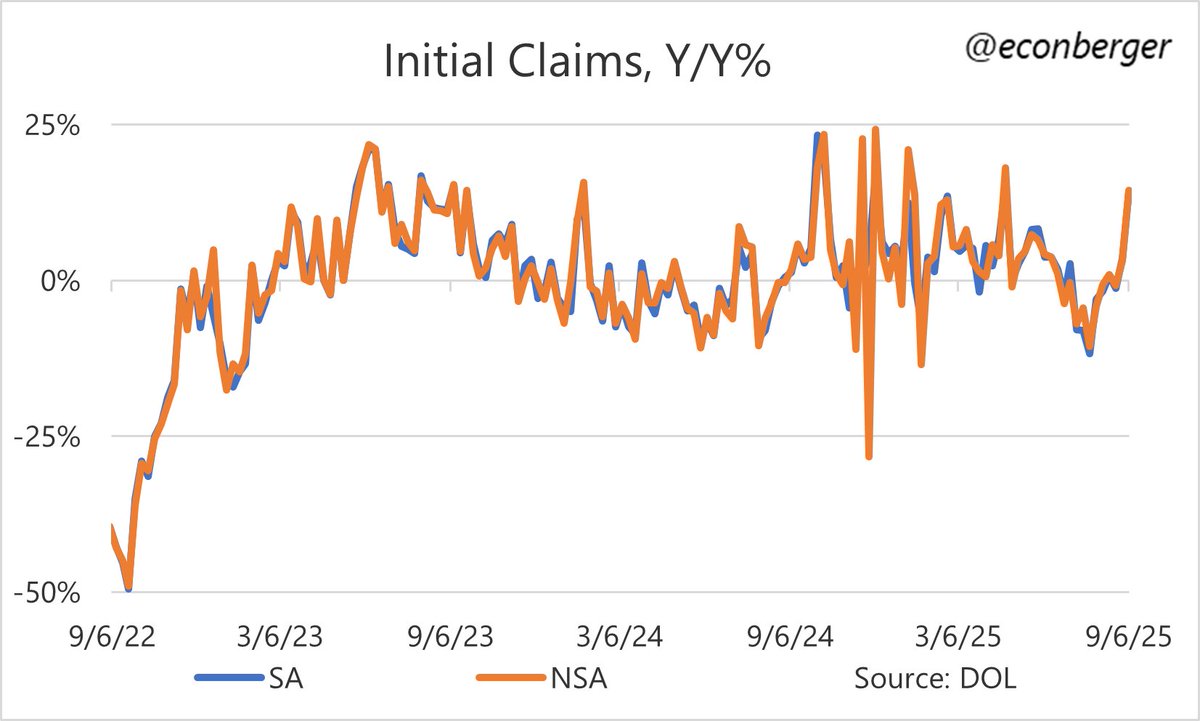

3/ Initial claims continue to run below year-ago levels. We're still in the Hurricane Beryl base effect window so I'll want to wait a little longer before I declare that layoffs are coming down...

4/ ...But we're running below 2023 levels too, not just 2024. It really does seem like the labor market is moving in a different direction than pessimists like me expected.

5/ Claims whiffed in their June nowcast of unemployment-due-to-permanent-layoff, but here's what they're saying for July.

• • •

Missing some Tweet in this thread? You can try to

force a refresh