72% of Americans say they feel stressed about money.

And most think the answer is “earn more.”

And that certainly can help, but for many people, more income just means more confusion.

Here are 4 simple systems that make your money feel less stressful ↓

And most think the answer is “earn more.”

And that certainly can help, but for many people, more income just means more confusion.

Here are 4 simple systems that make your money feel less stressful ↓

The #1 financial emotion in America isn’t greed or excitement.

It’s anxiety.

Even among high earners, money can feel overwhelming.

And the root of the problem usually isn’t income.

It’s lack of clarity.

It’s anxiety.

Even among high earners, money can feel overwhelming.

And the root of the problem usually isn’t income.

It’s lack of clarity.

Stress happens when you don’t know:

- What your money is doing

- Where it’s going

- Whether you’re on track

- What to do next

More income doesn’t fix that.

Systems do.

- What your money is doing

- Where it’s going

- Whether you’re on track

- What to do next

More income doesn’t fix that.

Systems do.

1. Automate everything you can

- Bills

- Savings

- Investments

Use direct deposit + auto-drafts to take the mental load off.

Automation doesn’t just save time - it removes emotion.

And that removes stress.

- Bills

- Savings

- Investments

Use direct deposit + auto-drafts to take the mental load off.

Automation doesn’t just save time - it removes emotion.

And that removes stress.

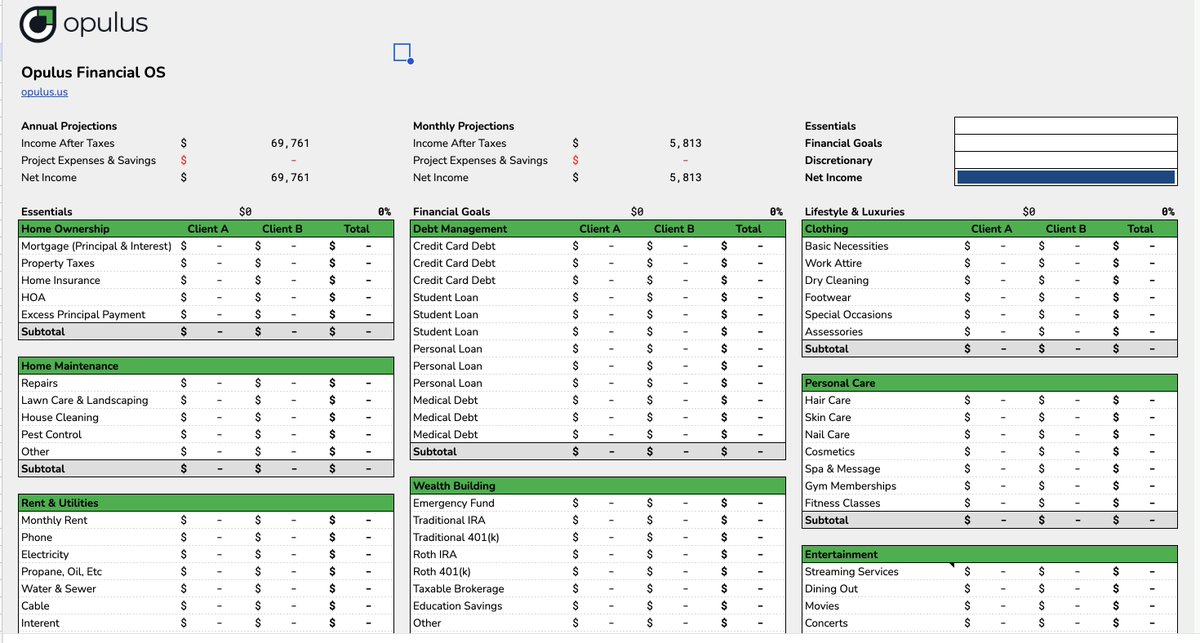

2. Use a bucket system for spending

Create 3 main categories:

- Essentials (needs)

- Financial Goals (savings/investing)

- Lifestyle & Luxuries (guilt-free spending)

Create 3 main categories:

- Essentials (needs)

- Financial Goals (savings/investing)

- Lifestyle & Luxuries (guilt-free spending)

The 50/20/30 rule is a good starting point:

- 50% to needs

- 20% to goals (Min)

- 30% to wants (Max)

As you make more money in life, all boats rise with the tide!

Save a little more, enjoy a little more, etc.

- 50% to needs

- 20% to goals (Min)

- 30% to wants (Max)

As you make more money in life, all boats rise with the tide!

Save a little more, enjoy a little more, etc.

3. Build a financial dashboard

One place that shows:

- Net worth

- Cash flow

- Savings rate

Progress toward goals. Motivation to keep growing.

This turns vague feelings into clear facts.

Knowing where you stand makes decision-making easier - and less reactive.

One place that shows:

- Net worth

- Cash flow

- Savings rate

Progress toward goals. Motivation to keep growing.

This turns vague feelings into clear facts.

Knowing where you stand makes decision-making easier - and less reactive.

4. Schedule regular check-ins

Money stress spikes when you only deal with it during emergencies.

Instead:

- Do a monthly 30-minute review

- Review progress quarterly

- Revisit your big picture yearly

Clarity compounds.

Money stress spikes when you only deal with it during emergencies.

Instead:

- Do a monthly 30-minute review

- Review progress quarterly

- Revisit your big picture yearly

Clarity compounds.

You don’t need more money to feel better about money.

You need more control.

And that starts with structure.

The goal isn’t perfect finances.

It’s peace of mind.

You need more control.

And that starts with structure.

The goal isn’t perfect finances.

It’s peace of mind.

TL;DR - How to Make Money Feel Less Stressful:

- 72% of Americans feel financial stress

- More income doesn’t solve disorganization

- Automate → Buckets → Track → Review

- Control = Confidence

- 72% of Americans feel financial stress

- More income doesn’t solve disorganization

- Automate → Buckets → Track → Review

- Control = Confidence

That's a wrap!

If your income is rising but stress isn't decreasing, it may be time to change your systems.

1. Follow me @FranWalsh73 for more of these

2. RT the tweet below to share this thread with your audience

Disclaimer; This thread is for educational purposes only. The contents expressed are my thoughts alone. You should always consult a qualified tax, legal, or financial advisor before making decisions for your family.

If your income is rising but stress isn't decreasing, it may be time to change your systems.

1. Follow me @FranWalsh73 for more of these

2. RT the tweet below to share this thread with your audience

Disclaimer; This thread is for educational purposes only. The contents expressed are my thoughts alone. You should always consult a qualified tax, legal, or financial advisor before making decisions for your family.

• • •

Missing some Tweet in this thread? You can try to

force a refresh