Building an RIA, Talking about finance & fitness: Co-Founder @OpulusLLC ⚡️ | Top 100 Advisor @Investopedia 💰| Not advice

Jun 29 • 15 tweets • 3 min read

More than half of Americans don't understand how tax brackets work.

For a household earning $150k, the gap between what they think they owe and what they actually owe is $10,172.

Here's what's really happening to your income: ↓

Let's kill the #1 tax misconception right now.

The myth: "More income = higher bracket = pay that rate on everything."

The reality: Only the dollars above each threshold get taxed at the higher rate.

Everything below stays taxed at lower rates.

Jun 5 • 9 tweets • 2 min read

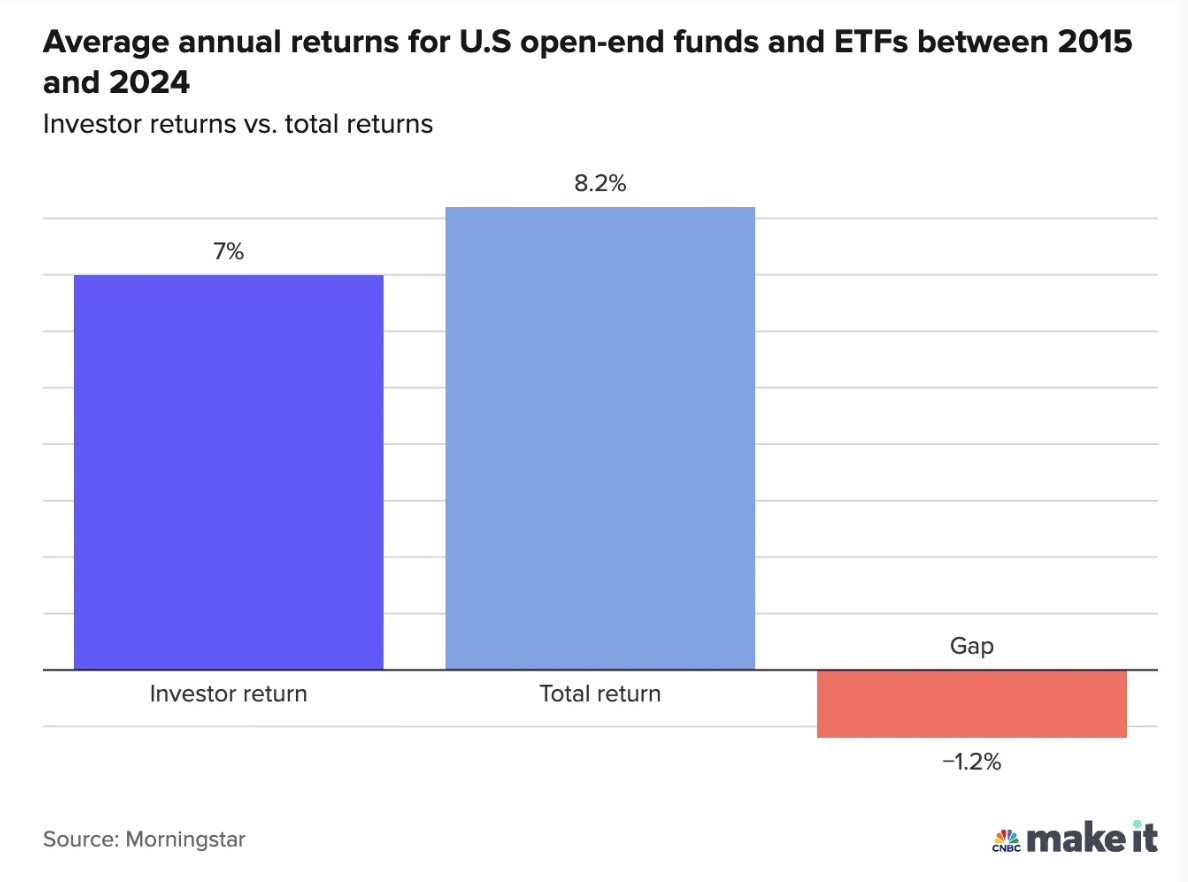

ETFs now hold over $13 trillion in US assets.

Yet most investors can't explain how they differ from mutual funds.

The choice matters - fees, taxes, and flexibility can cost or save you six figures over time.

Here's the full breakdown ↓

The core difference:

ETFs:

- Trade like stocks throughout the day

- Typically lower fees

- More tax-efficient

Mutual Funds:

- Often actively managed, trade once at day's end

- Sometimes higher fees

They look similar on the surface.

The details matter enormously.

May 26 • 17 tweets • 4 min read

A 4-year-old with a maxed Trump Account has ~$2.9M waiting at retirement.

That's not the interesting part.

The interesting part is what happens at 18 - when one tax move may be worth $600,000.

Most parents have no idea this window exists.

Here's how it works: ↓

First, kill the #1 misconception:

"Trump Accounts are only for babies born in 2025."

Wrong.

Any child under 18 can open one.

The $1,000 government seed is for newborns born 2025-2028 only.

The account itself is for every child in America under 18.

May 18 • 15 tweets • 3 min read

You just got $100k.

Inheritance. Bonus. Sold a business.

Everyone says "dollar-cost average it in over 12 months to be safe."

The math says they're wrong 2 out of 3 times.

But the math doesn't account for human behavior.

Here's the system that works: ↓

First, the math.

Vanguard studied this across 90 years of market data.

Lump sum outperformed dollar-cost averaging in roughly 2 out of 3 historical periods.

The reason: markets go up more often than they go down.

Time in the market beats timing the market.

May 11 • 25 tweets • 5 min read

The 1% advisor fee debate has been running for years.

The people winning it online are often selling something.

Here's the fully detailed, honest version - real flaws in every fee model, what good advisors actually add, and the flat-fee reality nobody talks about ↓

Let's be precise about what the argument actually claims.

$1M portfolio. 1% fee. 8% gross → 7% net.

Over 30 years: $7.6M vs. $10.1M.

The math is real. The gap is real.

What the argument leaves out is everything that happens between now and then.

May 2 • 18 tweets • 3 min read

Person A invested $36,000 and retired with $714,000.

Person B invested $175,000 and retired with $714,000.

Same outcome. Nearly 5x more money to get there & 3x the time.

If you have kids - or were never taught this yourself - this thread is for you.

Here's why it matters ↓

Same index fund. Same 8% average annual return.

Neither touches the money until 65.

The only variable: When they started.

Apr 28 • 17 tweets • 3 min read

We review a lot of tax returns.

Filing your taxes isn't the same as optimizing them.

The same five mistakes show up over and over - costing many households $5,000–$10,000+ per year.

None of them require a complicated strategy to fix.

Here's the list ↓

These aren't exotic tax shelters.

They're accounts and elections most people already have access to - and either don't know about, don't use correctly, or set up once and never revisited.

We see these regularly when reviewing returns.

Apr 26 • 22 tweets • 4 min read

Most high earners think the 401(k) limit is $24,500 in 2026.

It's not. That's just the employee contribution limit.

The actual IRS limit is $72,000.

The $47,500 gap? Most people leave it on the table.

Here's how to access it ↓

The IRS sets two separate 401(k) limits.

Limit 1 - Employee contributions: $24,500

(The one most people know.)

Limit 2 - Total plan contributions: $72,000

(Employee + employer match + profit sharing + after-tax combined.)

The gap is the opportunity.

Apr 9 • 16 tweets • 3 min read

Two high earners.

Same income.

Same retirement accounts.

One pays $64,000 to convert $200k to Roth.

The other pays $44,000 for the same conversion.

Same money. $20,000 difference. The only variable: which year they did it.

Here's how to find the right year ↓

Your lifetime tax rate isn't fixed.

It moves up and down - career transitions, parental leave, early retirement gaps, down business years.

Decisions made in low-rate years may determine how much you keep in high-rate years.

The goal is minimizing the lifetime bill.

Apr 2 • 14 tweets • 3 min read

You make too much for a Roth IRA.

Everyone tells you to do the "Backdoor Roth."

Almost nobody explains the part that may cost you thousands if you do it wrong.

Here's how it actually works ↓

Why the backdoor Roth exists.

Direct Roth IRA contributions phase out at:

→ $153k–$168k (single)

→ $242k–$252k (MFJ)

Above those thresholds, the direct path is closed.

The backdoor Roth is the legal workaround.

Mar 29 • 13 tweets • 3 min read

There's a 10-year window between retiring early and Social Security.

No earned income. No RMDs. No reason to pay taxes on investment gains.

Most people don't build toward it. The tax code rewards those who do.

Here's how it works ↓

The U.S. tax code has a 0% long-term capital gains rate.

Not a loophole. Literal tax law.

In 2026, married couples may pay zero federal tax on long-term capital gains if income stays under $98,900.

Add the $32,200 standard deduction - up to $131,100 potentially tax-free.

Mar 24 • 21 tweets • 4 min read

You just accepted a new job offer.

In the next 30 days, you'll make 6 financial decisions that could cost you $50,000+.

Most people get them wrong because nobody tells them what they are.

Here's the full checklist ↓

Why this matters more than people think.

Switching jobs is one of the highest-leverage financial events of your career.

More money can be made or lost in this 30-day window than in years of salary negotiations.

HR gives you a benefits packet. Nobody gives you a plan.

Mar 5 • 12 tweets • 3 min read

The people I know worth $1M+ have something in common.

It's not their income. It's not their investments.

It's that they all ran the same unsexy playbook - for a very long time.

Here's exactly what that looks like ↓

1. Grow your Income.

Your portfolio can't scale what your paycheck can't support.

In your 20s & 30s:

- Build in-demand skills

- Change roles strategically

- Negotiate every offer

- Focus on value creation

A $10K raise beats 99% of side hustles.

Mar 4 • 16 tweets • 3 min read

Two parents. Same income. Same kid's age.

One opens a Trump Account before April 15.

One assumes it's only for newborns.

By retirement:

One has $2.7M.

One has $0.

Most parents don't know this account was built for kids already born.

Here's everything you need to know: ↓

Let's kill the #1 misconception right now:

"Trump Accounts are only for babies born in 2025."

Wrong.

Any child under 18 can open one.

The $1,000 government seed is for newborns only.

The account? It's for every kid in America.

These are two completely different things.

Feb 23 • 17 tweets • 4 min read

Most portfolios look great in a bull market.

The problem? Bull markets don't last forever - and the plans that fall apart are the ones that were never tested.

Here are the 5 scenarios we run on every portfolio - and the ones that expose the biggest blind spots: ↓

Scenario #1: The market drops 40% tomorrow.

Look at your portfolio balance. Now cut it by 40%.

How does that number feel?

If your stomach just dropped, your allocation may be too aggressive for your actual risk tolerance - not the risk tolerance you told yourself you have.

Jan 20 • 15 tweets • 3 min read

Two people retire with $1M each.

Same exact portfolio.

Same withdrawal rate.

Same average returns.

One runs out of money in 18 years.

The other has $1.8M left after 30 years.

The difference? Sequence of returns. The retirement risk no one talks about: ↓

What is sequence of returns risk?

It's the order in which you experience investment returns.

In accumulation phase (while working): Order doesn't matter much.

In withdrawal phase (retirement): Order matters MASSIVELY.

Jan 19 • 18 tweets • 3 min read

Your emergency fund is costing you money.

The traditional "6 months in savings" rule?

It leaves $10,000+ in opportunity cost on the table for the average household.

Most people are either over-saved or under-saved. Both mistakes.

Here's the framework no one talks about ↓

The Traditional Rule Is Outdated

The advice: Save 6 months of expenses in a savings account.

The problem: Too much cash = inflation eats your wealth

Not enough liquidity planning = you tap retirement accounts in emergencies

There's a better way.

Nov 13, 2025 • 16 tweets • 3 min read

Most six-figure earners don’t have a budgeting problem - they have a systems problem.

Wealthy people don’t track every dollar.

They build money systems that run on autopilot.

Here are the 5 systems every high earner needs ↓

1. The Income System:

High earners don’t rise or fall based on discipline. They rise or fall based on distribution.

A real income system routes every dollar through one checking account → then automatically pushes money to bills, investing, and lifestyle buckets.

Sep 11, 2025 • 11 tweets • 2 min read

The average American loses $9,000 every year to hidden financial leaks.

That’s $90K gone every decade.

Here are the biggest leaks draining your wealth - and how to plug them so $9K turns into millions instead ↓

Let’s start with the math.

If you invest $9,000/year at 8%:

- 10 years = $130,000

- 20 years = $440,000

- 30 years = $1.1M

What feels like “small leaks” compounds into generational wealth lost.

Aug 7, 2025 • 14 tweets • 3 min read

Congress just created a new type of IRA for kids.

It's called the “Trump Account.”

It might include $1,000 in free money & open the door to a powerful Roth conversion strategy.

If you’re starting a family or having kids soon - this is for you. Here's what you need to know ↓

Let's start with the free $1,000.

The Treasury may contribute $1,000 to an eligible child’s Trump Account if:

- The child is born between 2025–2028

- The parent elects to open the account

- Funding is available through the Treasury

It’s not automatic - and it’s not guaranteed. But if it happens, basically a $1,000 head start

Jul 29, 2025 • 11 tweets • 2 min read

72% of Americans say they feel stressed about money.

And most think the answer is “earn more.”

And that certainly can help, but for many people, more income just means more confusion.

Here are 4 simple systems that make your money feel less stressful ↓

The #1 financial emotion in America isn’t greed or excitement.

It’s anxiety.

Even among high earners, money can feel overwhelming.

And the root of the problem usually isn’t income.

It’s lack of clarity.