Look at this guy.

He achieved zero losing years over 3 decades.

He delivered over 30% yearly returns by defying conventional wisdom.

Discover 7 key strategies that cemented his iconic status:

(No. 7 is sheer genius) 🧵

He achieved zero losing years over 3 decades.

He delivered over 30% yearly returns by defying conventional wisdom.

Discover 7 key strategies that cemented his iconic status:

(No. 7 is sheer genius) 🧵

This is Stanley Drukenmiller:

• Made $1B shorting the pound

• 30% CAGR over 30 years

• 0 losing years

Here's the Drukenmiller algorithm:

• Made $1B shorting the pound

• 30% CAGR over 30 years

• 0 losing years

Here's the Drukenmiller algorithm:

1. Exit losers quickly. Go all-in on winners.

While many spread their bets thin, Druckenmiller focuses intensely.

With a strong belief, he amplifies positions.

If mistaken? He bails without hesitation.

He commits to opportunities, not attachments.

While many spread their bets thin, Druckenmiller focuses intensely.

With a strong belief, he amplifies positions.

If mistaken? He bails without hesitation.

He commits to opportunities, not attachments.

2. Entry point trumps the idea itself.

Accuracy alone won't cut it.

You need precision in timing.

His wisdom: “Superior returns come from safeguarding capital and swinging for fences... not consistent singles.”

This isn't passive growth.

It's calculated boldness.

Accuracy alone won't cut it.

You need precision in timing.

His wisdom: “Superior returns come from safeguarding capital and swinging for fences... not consistent singles.”

This isn't passive growth.

It's calculated boldness.

3. Steer clear of popular opinions.

When it's common knowledge, the edge is gone.

Druckenmiller's top wins came from unique perspectives...

...backed by bold execution on scale.

The toughest moves often yield the best rewards.

When it's common knowledge, the edge is gone.

Druckenmiller's top wins came from unique perspectives...

...backed by bold execution on scale.

The toughest moves often yield the best rewards.

4. Big-picture economics first.

Unlike stock pickers, Druckenmiller starts with the macro view. He examines:

• Rate movements

• Money supply dynamics

• Policy shifts

• Global risks

Only after that does he hunt for positions.

Unlike stock pickers, Druckenmiller starts with the macro view. He examines:

• Rate movements

• Money supply dynamics

• Policy shifts

• Global risks

Only after that does he hunt for positions.

5. “Markets breathe on liquidity.”

Druckenmiller's core advice: “Avoid battling the flow of money.”

He argues capital availability shapes prices more than basics.

Abundant funds → inflated assets.

Scarce funds → shrinking values.

Druckenmiller's core advice: “Avoid battling the flow of money.”

He argues capital availability shapes prices more than basics.

Abundant funds → inflated assets.

Scarce funds → shrinking values.

Monitor capital trends, beyond quarterly numbers.

We've seen it play out (especially in recent cycles):

2020: Flood of cash → soaring markets.

2022: Squeeze on funds → widespread drops.

We've seen it play out (especially in recent cycles):

2020: Flood of cash → soaring markets.

2022: Squeeze on funds → widespread drops.

6. Turn setbacks into lessons.

He doesn't dodge errors... He dissects them.

“Any major slip-up stemmed from overcommitment to a view... without trimming losses promptly.”

Failures aren't foes.

Stubbornness is.

He doesn't dodge errors... He dissects them.

“Any major slip-up stemmed from overcommitment to a view... without trimming losses promptly.”

Failures aren't foes.

Stubbornness is.

7. When everything lines up, stake it all.

Back in 1992, Druckenmiller teamed with Soros to challenge England's central bank.

They pocketed $1B shorting the pound.

How?

Flawless analysis met ideal conditions.

“Spot the flawless opportunity, then strike decisively.”

Back in 1992, Druckenmiller teamed with Soros to challenge England's central bank.

They pocketed $1B shorting the pound.

How?

Flawless analysis met ideal conditions.

“Spot the flawless opportunity, then strike decisively.”

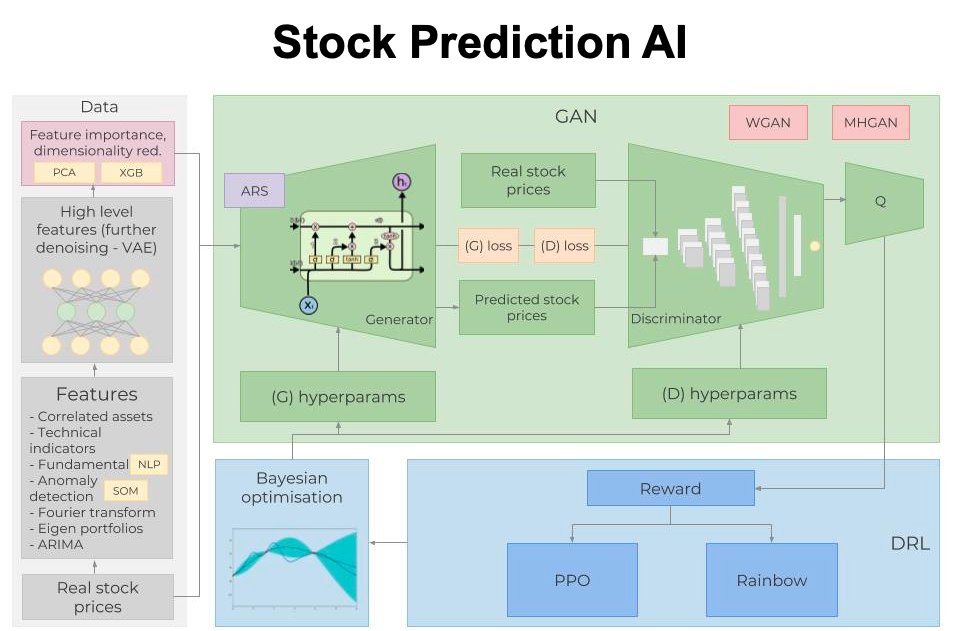

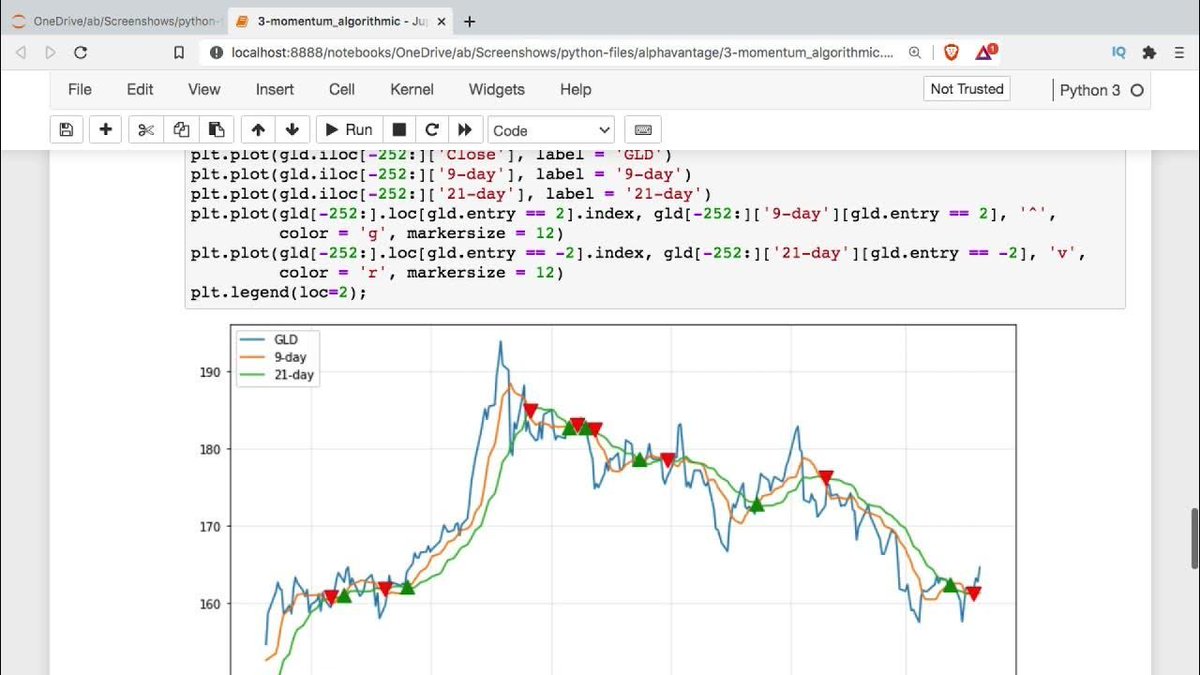

Can Drukenmillers' "Algorithm" be codified?

Yes - in Python.

Want to learn how?

Yes - in Python.

Want to learn how?

🚨 Python Algo Trading Workshop: Learn how we built our hedge fund

• QSConnect: Build your quant research database

• QSResearch: Research and run machine learning strategies

• Omega: Automate trade execution with Python

👉 Get the system: learn.quantscience.io/become-a-pro-q…

• QSConnect: Build your quant research database

• QSResearch: Research and run machine learning strategies

• Omega: Automate trade execution with Python

👉 Get the system: learn.quantscience.io/become-a-pro-q…

That's a wrap! Over the next 24 days, I'm sharing my top 24 algorithmic trading concepts to help you get started.

If you enjoyed this thread:

1. Follow me @quantscience_ for more of these

2. RT the tweet below to share this thread with your audience

If you enjoyed this thread:

1. Follow me @quantscience_ for more of these

2. RT the tweet below to share this thread with your audience

https://twitter.com/1683526993059430411/status/1953792185280651726

P.S. - Want Algorithmic Trading with Python tutorials every Sunday?

Register here to join our Sunday Quant Scientist Newsletter (it's free): learn.quantscience.io/quant-scientis…

Register here to join our Sunday Quant Scientist Newsletter (it's free): learn.quantscience.io/quant-scientis…

• • •

Missing some Tweet in this thread? You can try to

force a refresh