Biotech Corner- $GERN 🧬

Speculative Buy

“To one who has faith, no explanation is necessary. To one without faith, no explanation is possible.” — Thomas Aquinas

Friends,

The quote above seems like a fitting description of $GERN’s current situation.

Here’s their story: In Q3/24, the company launched a product called RYTELO for an indication in hematology called lower-risk myelodysplastic syndromes (LR-MDS). Specifically, the drug addresses one of LR-MDS’s most severe complications - anemia.

Why Are We Here?

The product beat forecasts in Q3 and Q4 last year, but then badly disappointed in Q1.

The company explained that penetration into the largest treatment centers had matured, so the rest of the market would grow at a slower pace.

But…

At no point did the company withdraw its peak sales guidance of $1B+ for LR-MDS.

Last week, they reported Q2/25 results: revenues up 24% vs Q1/25 and 7% above consensus.

The market isn’t buying it. It has decided the company is dishonest and the product is junk.

Here’s how we know: With $49M in sales and 24% sequential growth, it’s already clear that the 2025 consensus of $203M is too low.

And with a 2029 sales consensus of $814M, the market is assigning zero probability to RYTELO succeeding in its Phase 3 trial for myelofibrosis (MF), which will have an interim readout in H2/26, despite Phase 2 data showing overall survival (OS) of 30 months vs ~12 months for standard of care.

With too-low consensus estimates and zero credit for MF upside, the stock trades at 2.37× 2029 earnings, a 77% discount to the industry. That’s a lot of upside.

Bears point to patent protection risks. Our answer: $GERN holds $0.48 per share in net cash and expects to burn only another $70M ($0.09/share) before reaching profitability next year. That leaves only $0.89/share to justify and with low consensus forecasts plus zero MF credit, the company could earn $2.51/share by June 2031, the earliest possible U.S. patent expiry. Even after applying a discount rate, it still looks cheap.

In reality, the earliest U.S. patent expiry is June 2031, with European expiry in March 2037. Additional patents extend to August 2037 in the U.S. and November 2038 in Europe plus a next-gen product in preclinical trials with patents into the 2040s.

Scientifically, ~$30% of new RYTELO orders in Q2 were for 1st/2nd-line patients (up from 25% in Q1), likely due to its efficacy in the non-RS subgroup. If uptake continues to shift earlier from 3rd line to 1st/2nd line, the market size could reach into the billions.

For context: The U.S. 3rd-line LR-MDS market is ~4,400 patients/year, vs 7,600 in 2nd line and 16,800 in 1st line. The last major LR-MDS anemia launch into earlier lines was $BMY ’s Reblozyl, which grew 34% in Q2 to an annual run rate of ~$2.3B, with peak sales guidance above $4B.

To accelerate earlier-line adoption, $GERN expanded its sales force by 20% in Q2, expecting to see the impact by year-end:

“We expect that the efforts that are in place today will really play out over the next couple of quarters, and we expect to see long-term consistent growth.”

Two key opinion leaders told us they believe that, due to the progressive nature of anemia in MDS, ~two-thirds of patients will eventually receive RYTELO during their disease course. That’s ~11,200 patients/year in the U.S., at a net price of ~$300K/year, a $3.36B annual market potential in LR-MDS alone.

Outside the U.S., $GERN has no plans to launch independently, which means we could see an ex-U.S. partnership deal in the next year - adding cash, boosting confidence in the product, providing royalties, and further limiting downside.

Bottom line: Quarterly sales may be volatile and patent life finite, but the massive LR-MDS potential, the MF “dream,” the shift to earlier lines, strong Q2 results, and downside protection from DCF on MDS alone are hard to ignore.

Sentiment comes and goes, but value from earnings eventually wins.

Speculative Buy

“To one who has faith, no explanation is necessary. To one without faith, no explanation is possible.” — Thomas Aquinas

Friends,

The quote above seems like a fitting description of $GERN’s current situation.

Here’s their story: In Q3/24, the company launched a product called RYTELO for an indication in hematology called lower-risk myelodysplastic syndromes (LR-MDS). Specifically, the drug addresses one of LR-MDS’s most severe complications - anemia.

Why Are We Here?

The product beat forecasts in Q3 and Q4 last year, but then badly disappointed in Q1.

The company explained that penetration into the largest treatment centers had matured, so the rest of the market would grow at a slower pace.

But…

At no point did the company withdraw its peak sales guidance of $1B+ for LR-MDS.

Last week, they reported Q2/25 results: revenues up 24% vs Q1/25 and 7% above consensus.

The market isn’t buying it. It has decided the company is dishonest and the product is junk.

Here’s how we know: With $49M in sales and 24% sequential growth, it’s already clear that the 2025 consensus of $203M is too low.

And with a 2029 sales consensus of $814M, the market is assigning zero probability to RYTELO succeeding in its Phase 3 trial for myelofibrosis (MF), which will have an interim readout in H2/26, despite Phase 2 data showing overall survival (OS) of 30 months vs ~12 months for standard of care.

With too-low consensus estimates and zero credit for MF upside, the stock trades at 2.37× 2029 earnings, a 77% discount to the industry. That’s a lot of upside.

Bears point to patent protection risks. Our answer: $GERN holds $0.48 per share in net cash and expects to burn only another $70M ($0.09/share) before reaching profitability next year. That leaves only $0.89/share to justify and with low consensus forecasts plus zero MF credit, the company could earn $2.51/share by June 2031, the earliest possible U.S. patent expiry. Even after applying a discount rate, it still looks cheap.

In reality, the earliest U.S. patent expiry is June 2031, with European expiry in March 2037. Additional patents extend to August 2037 in the U.S. and November 2038 in Europe plus a next-gen product in preclinical trials with patents into the 2040s.

Scientifically, ~$30% of new RYTELO orders in Q2 were for 1st/2nd-line patients (up from 25% in Q1), likely due to its efficacy in the non-RS subgroup. If uptake continues to shift earlier from 3rd line to 1st/2nd line, the market size could reach into the billions.

For context: The U.S. 3rd-line LR-MDS market is ~4,400 patients/year, vs 7,600 in 2nd line and 16,800 in 1st line. The last major LR-MDS anemia launch into earlier lines was $BMY ’s Reblozyl, which grew 34% in Q2 to an annual run rate of ~$2.3B, with peak sales guidance above $4B.

To accelerate earlier-line adoption, $GERN expanded its sales force by 20% in Q2, expecting to see the impact by year-end:

“We expect that the efforts that are in place today will really play out over the next couple of quarters, and we expect to see long-term consistent growth.”

Two key opinion leaders told us they believe that, due to the progressive nature of anemia in MDS, ~two-thirds of patients will eventually receive RYTELO during their disease course. That’s ~11,200 patients/year in the U.S., at a net price of ~$300K/year, a $3.36B annual market potential in LR-MDS alone.

Outside the U.S., $GERN has no plans to launch independently, which means we could see an ex-U.S. partnership deal in the next year - adding cash, boosting confidence in the product, providing royalties, and further limiting downside.

Bottom line: Quarterly sales may be volatile and patent life finite, but the massive LR-MDS potential, the MF “dream,” the shift to earlier lines, strong Q2 results, and downside protection from DCF on MDS alone are hard to ignore.

Sentiment comes and goes, but value from earnings eventually wins.

Also note: several hematology players could acquire $GERN - from mid-caps like $JAZZ or $GMAB to big pharma like $ABBV or $NVS. While big pharma may not bite now, strong Phase 3 MF data in H2/26 could change that instantly.

Catalyst

One way or another, Q3 results (due in 3 months) will be key - showing whether Q2 was a one-off or the start of a new growth phase.

Management wouldn’t guide for Q3, but did say:

“We have cautious optimism that we will continue to drive demand and execution going forward.”

If they’re cautiously optimistic, we can be too and give $GERN a spot in our “risk basket.”

Catalyst

One way or another, Q3 results (due in 3 months) will be key - showing whether Q2 was a one-off or the start of a new growth phase.

Management wouldn’t guide for Q3, but did say:

“We have cautious optimism that we will continue to drive demand and execution going forward.”

If they’re cautiously optimistic, we can be too and give $GERN a spot in our “risk basket.”

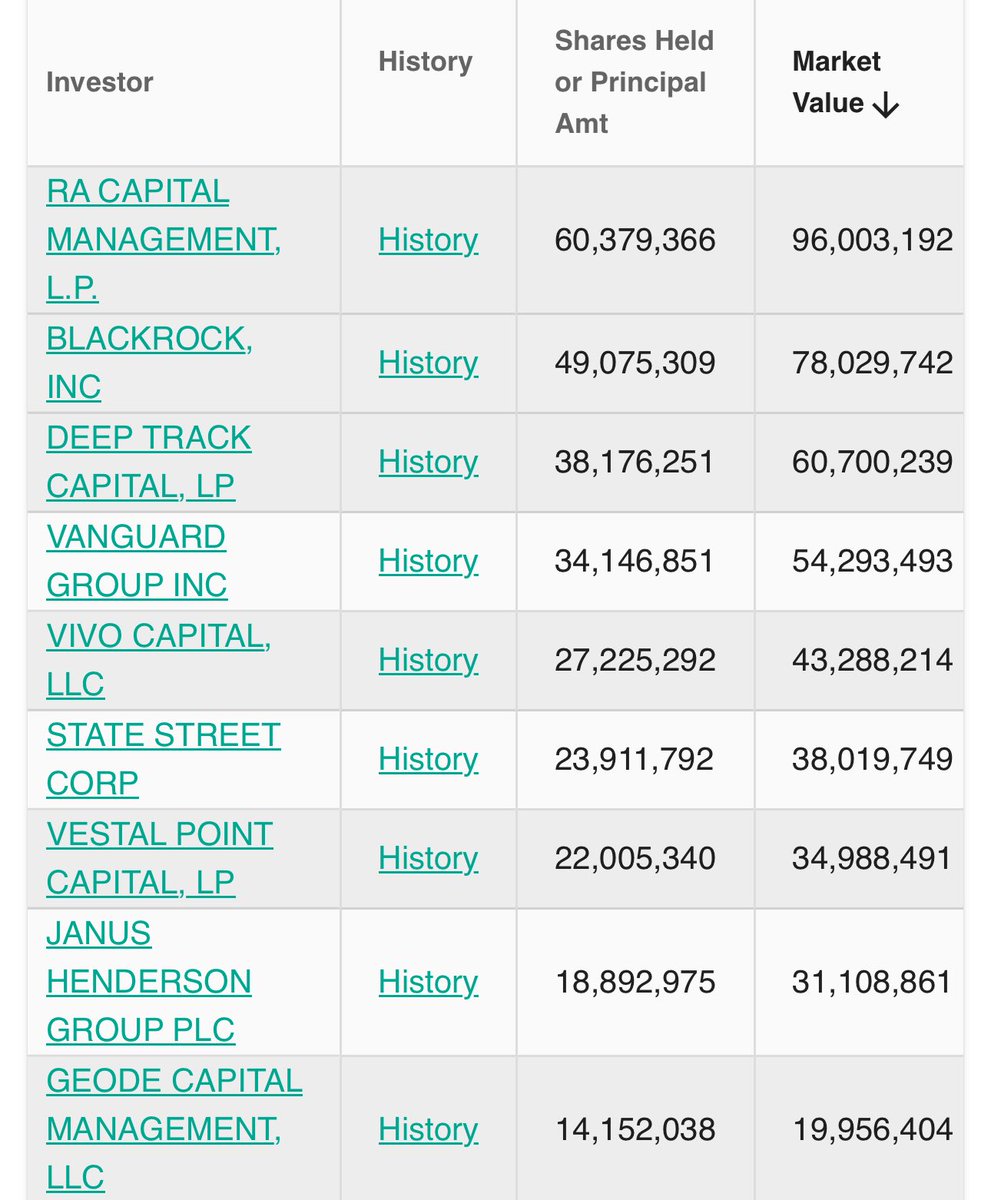

Smart Money

RA Advisors hold ~10% of the company, it is one of the top biotech hedge funds and a long-time $GERN holder since 2020, doubled its position last quarter, signaling strong conviction in the story. Point72 also initiated a small position during the same period.

RA Advisors hold ~10% of the company, it is one of the top biotech hedge funds and a long-time $GERN holder since 2020, doubled its position last quarter, signaling strong conviction in the story. Point72 also initiated a small position during the same period.

• • •

Missing some Tweet in this thread? You can try to

force a refresh