One small mistake while swiping your card abroad can cost you 5–7% extra 💸

Saw @pk037 break this down so well in his youtube short, had to share here in detail 👇

Saw @pk037 break this down so well in his youtube short, had to share here in detail 👇

When you swipe at a POS in Europe (or anywhere abroad), the machine often asks:

“Pay in Local Currency (EUR, USD, etc.) or INR?”

The choice makes a BIG difference!

“Pay in Local Currency (EUR, USD, etc.) or INR?”

The choice makes a BIG difference!

1️⃣If you choose Local Currency (EUR, USD, etc.)

- Your network (Visa/Master/Amex/Discover) does the conversion

- You pay at near market rate

- Forex markup from your card (1.5–3.5% + GST) applies

- Transparent & cheaper ✅

- Your network (Visa/Master/Amex/Discover) does the conversion

- You pay at near market rate

- Forex markup from your card (1.5–3.5% + GST) applies

- Transparent & cheaper ✅

2️⃣If you choose INR

- Merchant/processor converts it (Dynamic Currency Conversion a.k.a DCC)

- They add hidden margins (3–6% extra 🤦)

- Your bank may still add forex markup

- End result is that you might cost you a lot more!

- Merchant/processor converts it (Dynamic Currency Conversion a.k.a DCC)

- They add hidden margins (3–6% extra 🤦)

- Your bank may still add forex markup

- End result is that you might cost you a lot more!

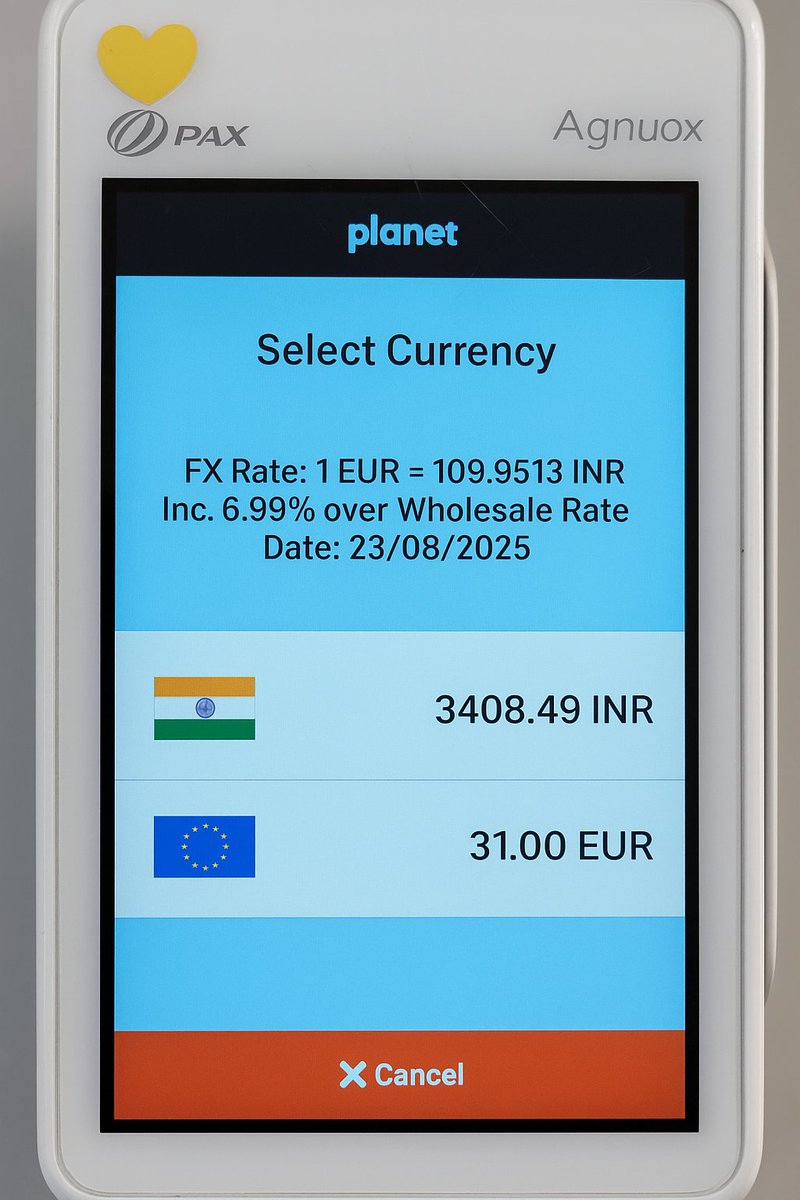

Here’s a real example -

A €31 transaction showed two options -

EUR 31

INR 3408.49 (with a ~7% markup baked in!)

Pick INR here, and you overpay straight away!

A €31 transaction showed two options -

EUR 31

INR 3408.49 (with a ~7% markup baked in!)

Pick INR here, and you overpay straight away!

Always pay in local currency abroad!

Never choose INR/your home currency on the machine.

It’s a small choice that saves you 5–7% every single time.

Credits again: @pk037 for highlighting this! 🔥

Never choose INR/your home currency on the machine.

It’s a small choice that saves you 5–7% every single time.

Credits again: @pk037 for highlighting this! 🔥

@pk037 @threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh