🚀India crossed 110 million credit cards in July 2025

Today, co-branded cards are rewriting how Indians shop, save, and stay loyal.

Let’s unpack the story🧵👇

Today, co-branded cards are rewriting how Indians shop, save, and stay loyal.

Let’s unpack the story🧵👇

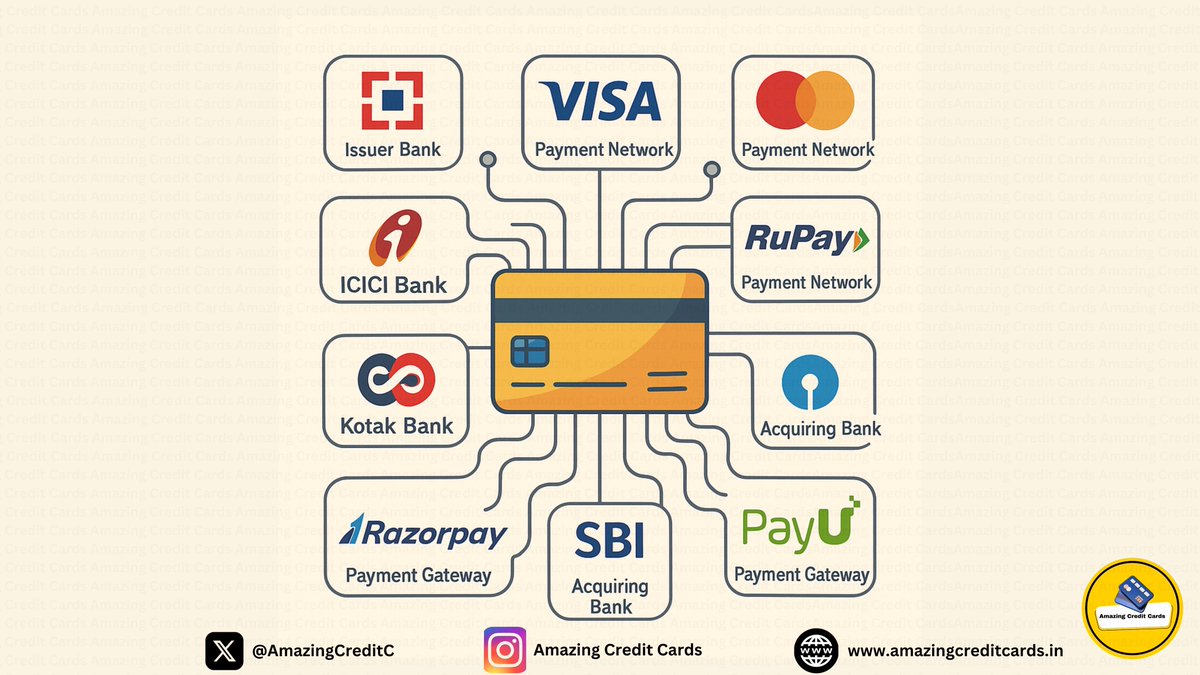

🏦 What Are Co-Branded Cards?

A co-branded credit card (CBCC) is built through a three-way partnership:

🏦Bank (issues & manages credit)

🏬Brand (retailer, airline, telecom, etc.)

🌎Network (Visa, Mastercard, RuPay).

The result: a card that works almost everywhere but gives extra rewards inside the brand’s world.

A co-branded credit card (CBCC) is built through a three-way partnership:

🏦Bank (issues & manages credit)

🏬Brand (retailer, airline, telecom, etc.)

🌎Network (Visa, Mastercard, RuPay).

The result: a card that works almost everywhere but gives extra rewards inside the brand’s world.

📈 Why They’re Exploding

The timing couldn’t be better:

•Spending hit ₹21.16 lakh crore in 2025 up 15% from ₹18.32 lakh crore in FY24.

•CBCCs now makes up a lion share of the incremental cards issued.

The fuel? Digital commerce, UPI adoption, and millions of new-to-credit consumers.

The timing couldn’t be better:

•Spending hit ₹21.16 lakh crore in 2025 up 15% from ₹18.32 lakh crore in FY24.

•CBCCs now makes up a lion share of the incremental cards issued.

The fuel? Digital commerce, UPI adoption, and millions of new-to-credit consumers.

💳 Loyalty, Reimagined

Loyalty today is less about feelings, more about practical value — cashback, discounts, and perks.

Three cards show how differently this works:

•Amazon Pay ICICI → Cashback credited to Amazon Pay balance, pushing you to keep spending on Amazon.

•EazyDiner IndusInd → Extra discounts at restaurants + free membership for food lovers.

•Airtel Axis Bank → Cashback on mobile, broadband and utility bills.

Loyalty today is less about feelings, more about practical value — cashback, discounts, and perks.

Three cards show how differently this works:

•Amazon Pay ICICI → Cashback credited to Amazon Pay balance, pushing you to keep spending on Amazon.

•EazyDiner IndusInd → Extra discounts at restaurants + free membership for food lovers.

•Airtel Axis Bank → Cashback on mobile, broadband and utility bills.

📜 The Rules of the Game

The RBI has stepped in with clear guardrails:

•Brands can’t access customer-level transaction data.

•The bank’s name must be prominent.

This keeps the ecosystem transparent and balanced.

The RBI has stepped in with clear guardrails:

•Brands can’t access customer-level transaction data.

•The bank’s name must be prominent.

This keeps the ecosystem transparent and balanced.

🏦 How The Banks Benefit?

1. Interchange Fees:

Every swipe earns banks a cut (2–3%) as interchange income.

2. Interest on Revolvers:

If users don’t pay in full, banks charge 36–42% APR the biggest profit driver.

3. Fees & Penalties:

Late fees, forex charges, and service fees add extra revenue.

4. Lower Acquisition Cost:

Banks acquire customers through the brand’s base, cutting expensive marketing costs.

5. Cross-Selling:

Cards open doors to pitch loans, insurance, investments, and premium banking products.

1. Interchange Fees:

Every swipe earns banks a cut (2–3%) as interchange income.

2. Interest on Revolvers:

If users don’t pay in full, banks charge 36–42% APR the biggest profit driver.

3. Fees & Penalties:

Late fees, forex charges, and service fees add extra revenue.

4. Lower Acquisition Cost:

Banks acquire customers through the brand’s base, cutting expensive marketing costs.

5. Cross-Selling:

Cards open doors to pitch loans, insurance, investments, and premium banking products.

🛍️ What About The Merchants?

1. Share of Revenue:

They get a cut from annual fees, interchange, or spending commissions.

2. Higher Spending:

Cardholders spend more with the partner brand.

3. Stronger Loyalty:

Cashback and perks keep customers tied to the brand ecosystem.

4. Useful Insights:

Even without individual data, aggregated patterns guide offers and campaigns.

5. Everyday Visibility:

The brand’s logo in a customer’s wallet = constant marketing.

1. Share of Revenue:

They get a cut from annual fees, interchange, or spending commissions.

2. Higher Spending:

Cardholders spend more with the partner brand.

3. Stronger Loyalty:

Cashback and perks keep customers tied to the brand ecosystem.

4. Useful Insights:

Even without individual data, aggregated patterns guide offers and campaigns.

5. Everyday Visibility:

The brand’s logo in a customer’s wallet = constant marketing.

📌 The Shared Win

•Banks → Earn interest, fees, and cross-sales with lower costs.

•Merchants → Boost sales, loyalty, and add a new income stream.

•Consumers → Save money and get credit access.

•Banks → Earn interest, fees, and cross-sales with lower costs.

•Merchants → Boost sales, loyalty, and add a new income stream.

•Consumers → Save money and get credit access.

🏆 Examples Across Sectors

CBCCs now span every corner of daily life:

•E-commerce: Amazon Pay ICICI, Flipkart Axis.

•Telecom: Airtel Axis Bank.

•Mobility: Ola Money SBI.

•Travel: IRCTC SBI, MakeMyTrip ICICI, IDFC Indigo, etc.

•Payment apps: PhonePe SBI & PhonePe HDFC credit cards

•Dining & Fuel: EazyDiner IndusInd, IndianOil Axis.

CBCCs now span every corner of daily life:

•E-commerce: Amazon Pay ICICI, Flipkart Axis.

•Telecom: Airtel Axis Bank.

•Mobility: Ola Money SBI.

•Travel: IRCTC SBI, MakeMyTrip ICICI, IDFC Indigo, etc.

•Payment apps: PhonePe SBI & PhonePe HDFC credit cards

•Dining & Fuel: EazyDiner IndusInd, IndianOil Axis.

⚠️ The Risks in Co-Branded Cards

❌While banks and merchants both win, there are risks on each side:

🏦For Banks,

•Credit defaults: As more “new-to-credit” customers join, chances of missed payments rise.

•Reputational risk: If the merchant delivers poor service, the bank’s name gets dragged along.

•Over-concentration: Too much exposure to one brand segment could hurt if that sector slows down.

❌While banks and merchants both win, there are risks on each side:

🏦For Banks,

•Credit defaults: As more “new-to-credit” customers join, chances of missed payments rise.

•Reputational risk: If the merchant delivers poor service, the bank’s name gets dragged along.

•Over-concentration: Too much exposure to one brand segment could hurt if that sector slows down.

🛍️For Merchants,

•Low adoption: If rewards aren’t attractive, customers won’t sign up, wasting resources.

•Churn risk: Competitors may launch richer offers, pulling customers away.

•Brand dilution: A bad banking partner (poor service, hidden charges) can hurt the merchant’s image.

•Low adoption: If rewards aren’t attractive, customers won’t sign up, wasting resources.

•Churn risk: Competitors may launch richer offers, pulling customers away.

•Brand dilution: A bad banking partner (poor service, hidden charges) can hurt the merchant’s image.

🔮 What’s Coming Next

This wave is only getting stronger:

•Personalized rewards using AI.

•UPI + credit fusion → Pay with a RuPay credit card via QR codes.

•Plug-and-play card platforms (CCaaS) → letting more brands launch cards.

This wave is only getting stronger:

•Personalized rewards using AI.

•UPI + credit fusion → Pay with a RuPay credit card via QR codes.

•Plug-and-play card platforms (CCaaS) → letting more brands launch cards.

That’s the story of co-branded credit cards in India 🤝

If you enjoyed this thread:

❤️Like this thread

🔁 Repost to share it with others

💬 Comment your thoughts below

👤 Follow @AmazingCreditC for more credit card tips, hacks, and insights

If you enjoyed this thread:

❤️Like this thread

🔁 Repost to share it with others

💬 Comment your thoughts below

👤 Follow @AmazingCreditC for more credit card tips, hacks, and insights

https://twitter.com/amazingcreditc/status/1961070923278061896

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh