📢Economic Growth, Stocks' Return, and Global Debasement - The Long-Term Evidence 📢

Who has grown the fastest in the past 20 years, who has delivered the best returns, and is there a relation?

The answers might surprise you 👇👇

Who has grown the fastest in the past 20 years, who has delivered the best returns, and is there a relation?

The answers might surprise you 👇👇

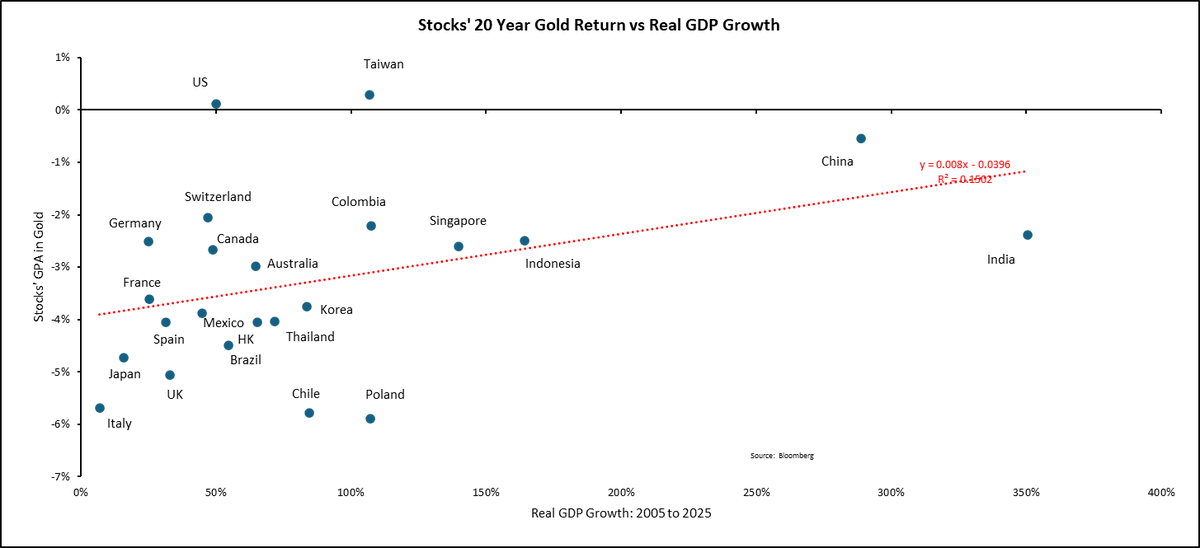

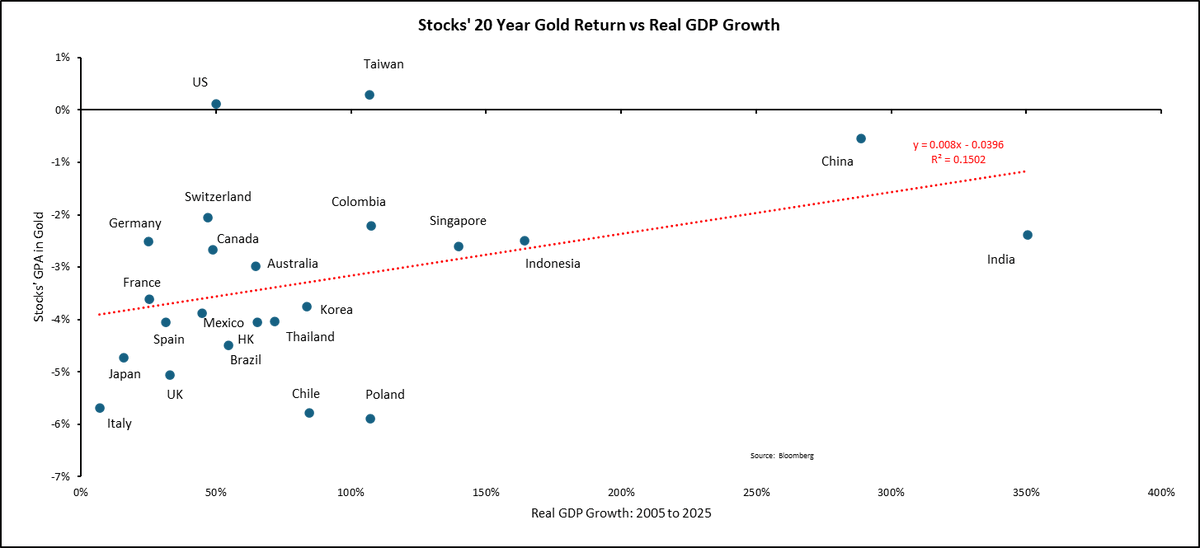

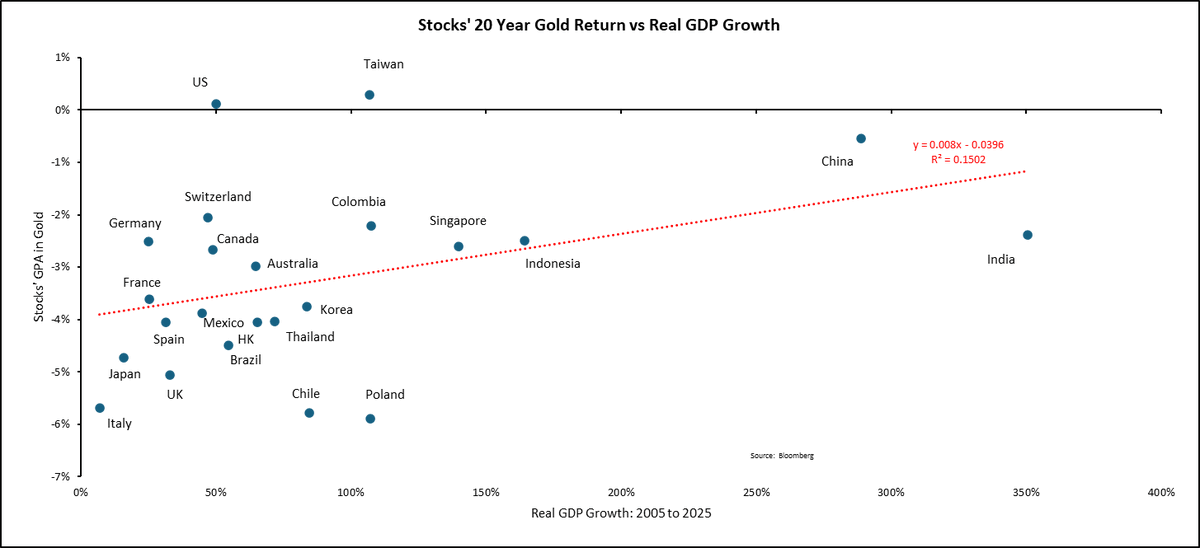

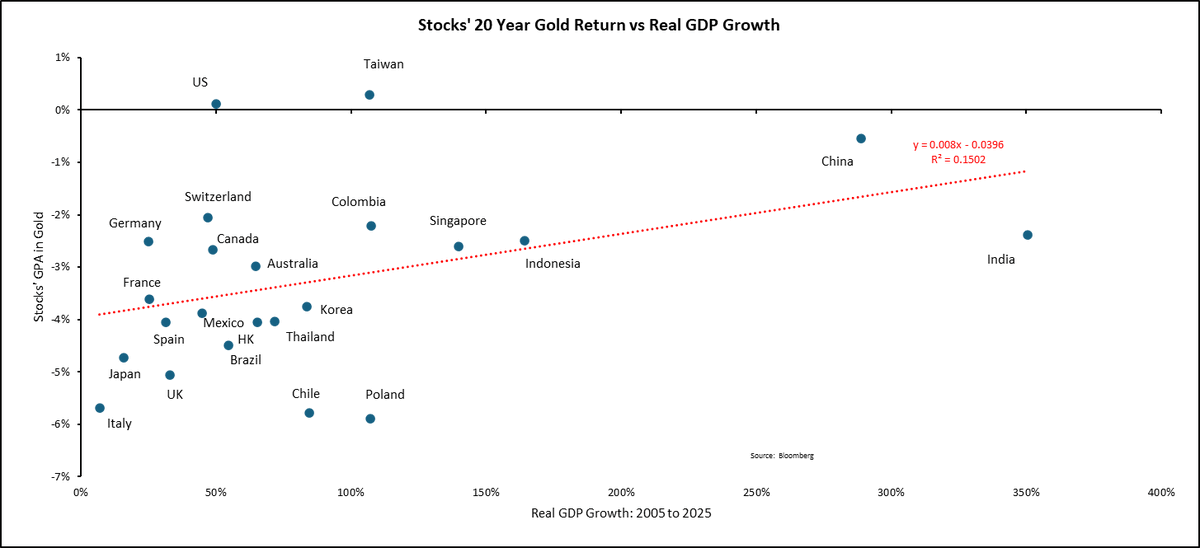

First, there is little relation between economic growth and stocks' return, even over 20 years

GDP growth explains just 15% of stocks' returns

Stocks' returns are driven by margins, dividends, and changes in multiples

Broadly speaking, the BRICS create GDP, the US delivers capital gains, and Europe produces neither

GDP growth explains just 15% of stocks' returns

Stocks' returns are driven by margins, dividends, and changes in multiples

Broadly speaking, the BRICS create GDP, the US delivers capital gains, and Europe produces neither

Second, only two stock markets (barely) outperformed gold in the past 20 years: the US and Taiwan, mostly due to the AI / semi bull market.

Gold has returned 10.7% PA (in USD) since 2005. The combination of soaring gold and a strong USD was too hard to beat for most international stocks.

For the past 20 years, most stocks could not keep up with monetary debasement, despite high nominal gains

Gold has returned 10.7% PA (in USD) since 2005. The combination of soaring gold and a strong USD was too hard to beat for most international stocks.

For the past 20 years, most stocks could not keep up with monetary debasement, despite high nominal gains

Four patterns emerge

- China, India, Indonesia and Singapore balanced high growth with only modest debasement of their stocks vs gold

- Most EMs (Poland, Chile, Korea, Brazil) had decent growth but bad stocks' returns in gold

- Switzerland and the US were the most successful DMs: decent growth and good stocks' returns (due to the Mag 7 in the US and the strong CHF for Switzerland)

- Italy, Japan, and the UK had poor growth and stocks' return (growth looks a bit better on a per capita basis)

- China, India, Indonesia and Singapore balanced high growth with only modest debasement of their stocks vs gold

- Most EMs (Poland, Chile, Korea, Brazil) had decent growth but bad stocks' returns in gold

- Switzerland and the US were the most successful DMs: decent growth and good stocks' returns (due to the Mag 7 in the US and the strong CHF for Switzerland)

- Italy, Japan, and the UK had poor growth and stocks' return (growth looks a bit better on a per capita basis)

Lessons for investors

➡️ The "Stocks for the long run" case is mostly a US-centric nominal argument, benefitting from one exceptional market in an exceptional century.

Stocks do not beat gold in most countries

➡️ GDP growth is not enough! Margins and multiples matter more. I am especially concerned about the large growth premium currently baked into India and US stocks

➡️ Currencies matter: the best-performing markets (the US, Taiwan, Switzerland, China) all had rising currencies

➡️Look for cheap equity indices with depressed margins and potential for currency appreciation for the next 10 years: I would pick Brazil, China, and Korea

➡️ The "Stocks for the long run" case is mostly a US-centric nominal argument, benefitting from one exceptional market in an exceptional century.

Stocks do not beat gold in most countries

➡️ GDP growth is not enough! Margins and multiples matter more. I am especially concerned about the large growth premium currently baked into India and US stocks

➡️ Currencies matter: the best-performing markets (the US, Taiwan, Switzerland, China) all had rising currencies

➡️Look for cheap equity indices with depressed margins and potential for currency appreciation for the next 10 years: I would pick Brazil, China, and Korea

• • •

Missing some Tweet in this thread? You can try to

force a refresh