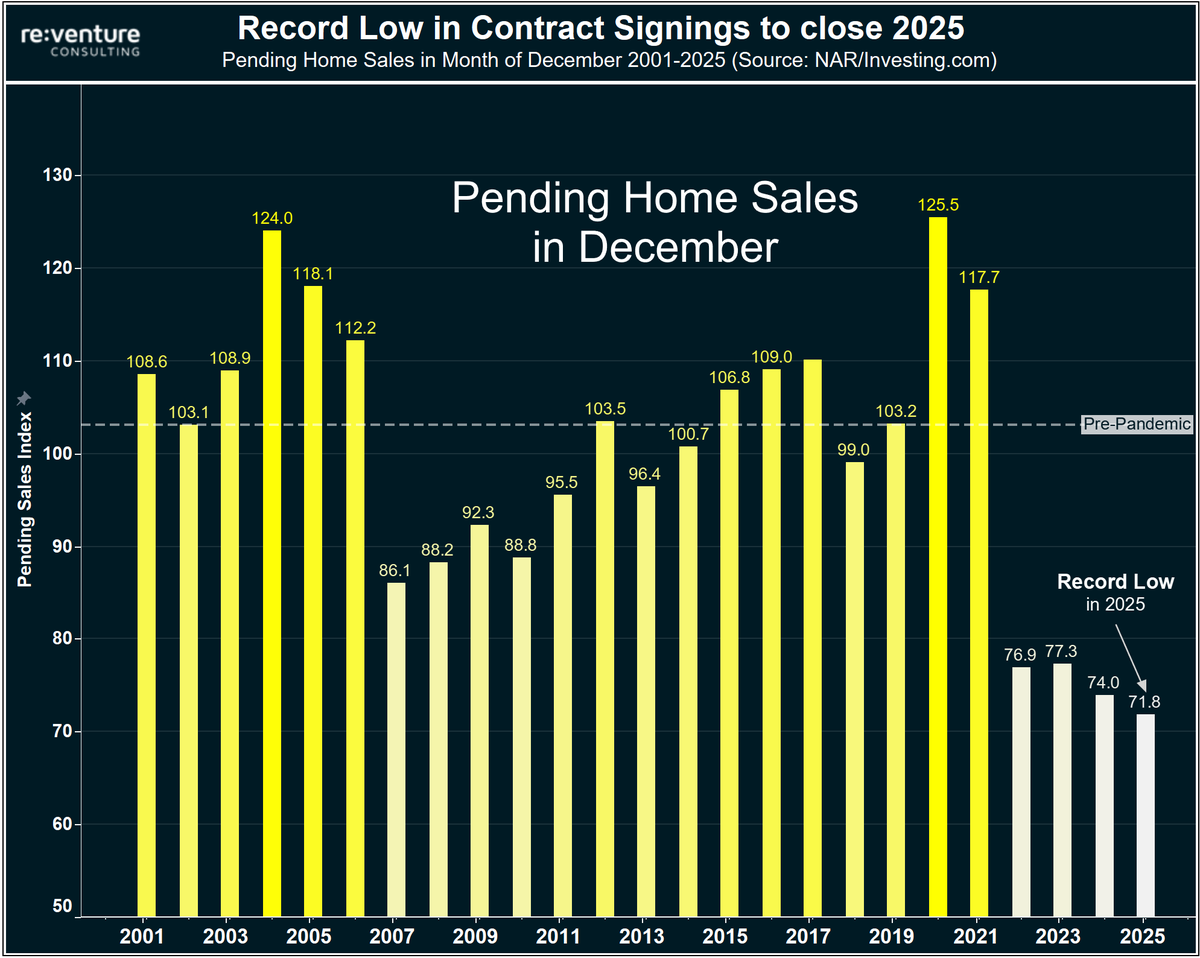

We literally have the worst homebuyer demand on record according to the NAR's pending sales index.

Time for people to wake up and realize prices are the problem.

Time for people to wake up and realize prices are the problem.

1) Fed cut rates almost one year ago, and demand went down.

Think about that. September 2024 was the first rate cut, and the pending sales index back then was between 76-79.

Now it's 72.

Buyer demand dropped after rate cuts.

Think about that. September 2024 was the first rate cut, and the pending sales index back then was between 76-79.

Now it's 72.

Buyer demand dropped after rate cuts.

2) Not only that, though.

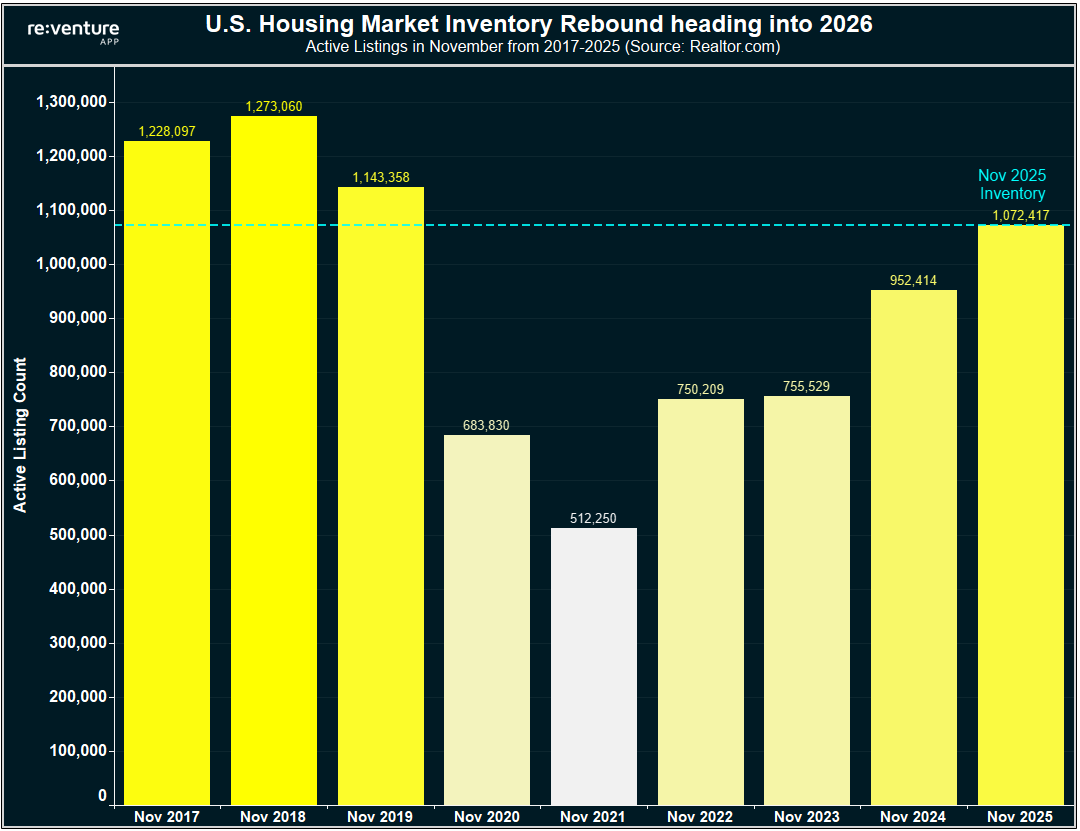

Since the Fed cut rates, we have 30% more inventory sitting on the market, and home values are now dropping in about half the U.S.

So rate cuts + way more inventory + prices dropping...and still no buyer demand improvement.

Since the Fed cut rates, we have 30% more inventory sitting on the market, and home values are now dropping in about half the U.S.

So rate cuts + way more inventory + prices dropping...and still no buyer demand improvement.

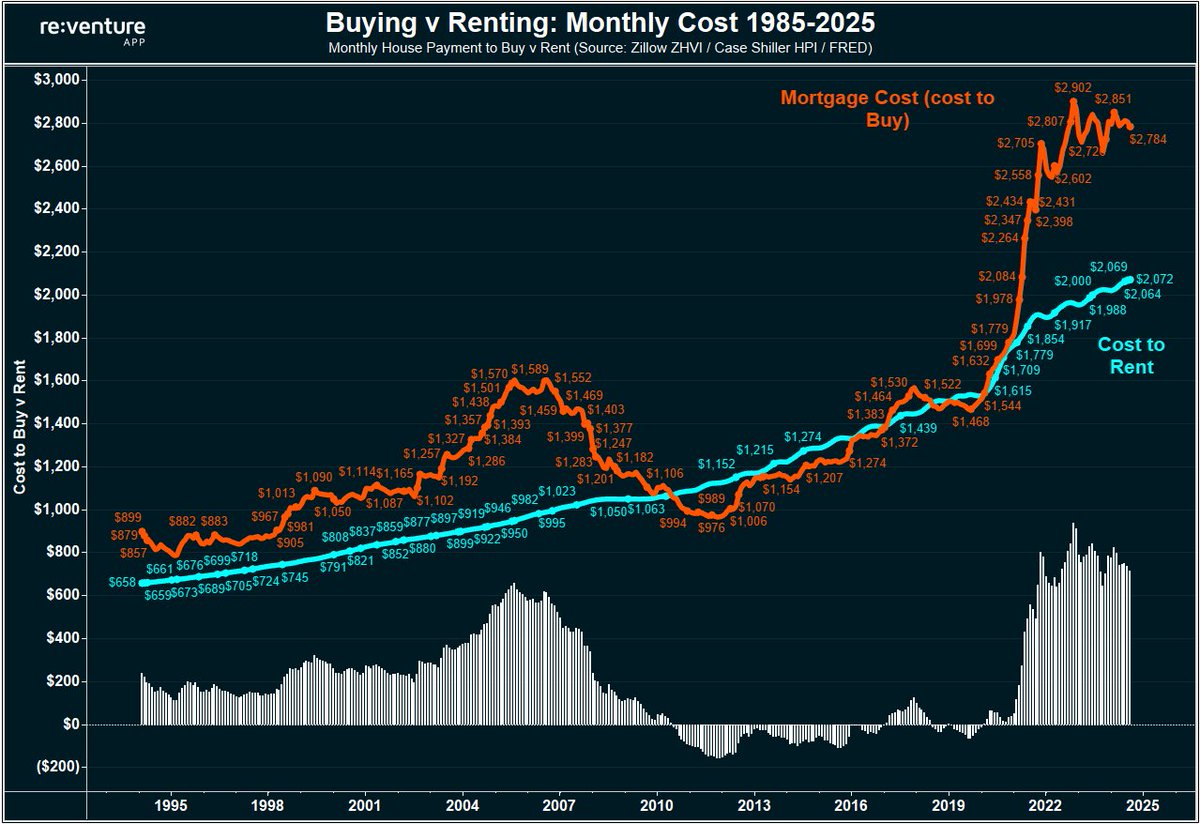

3) One reason for the lackluster buyer demand is the simple math behind buying and renting.

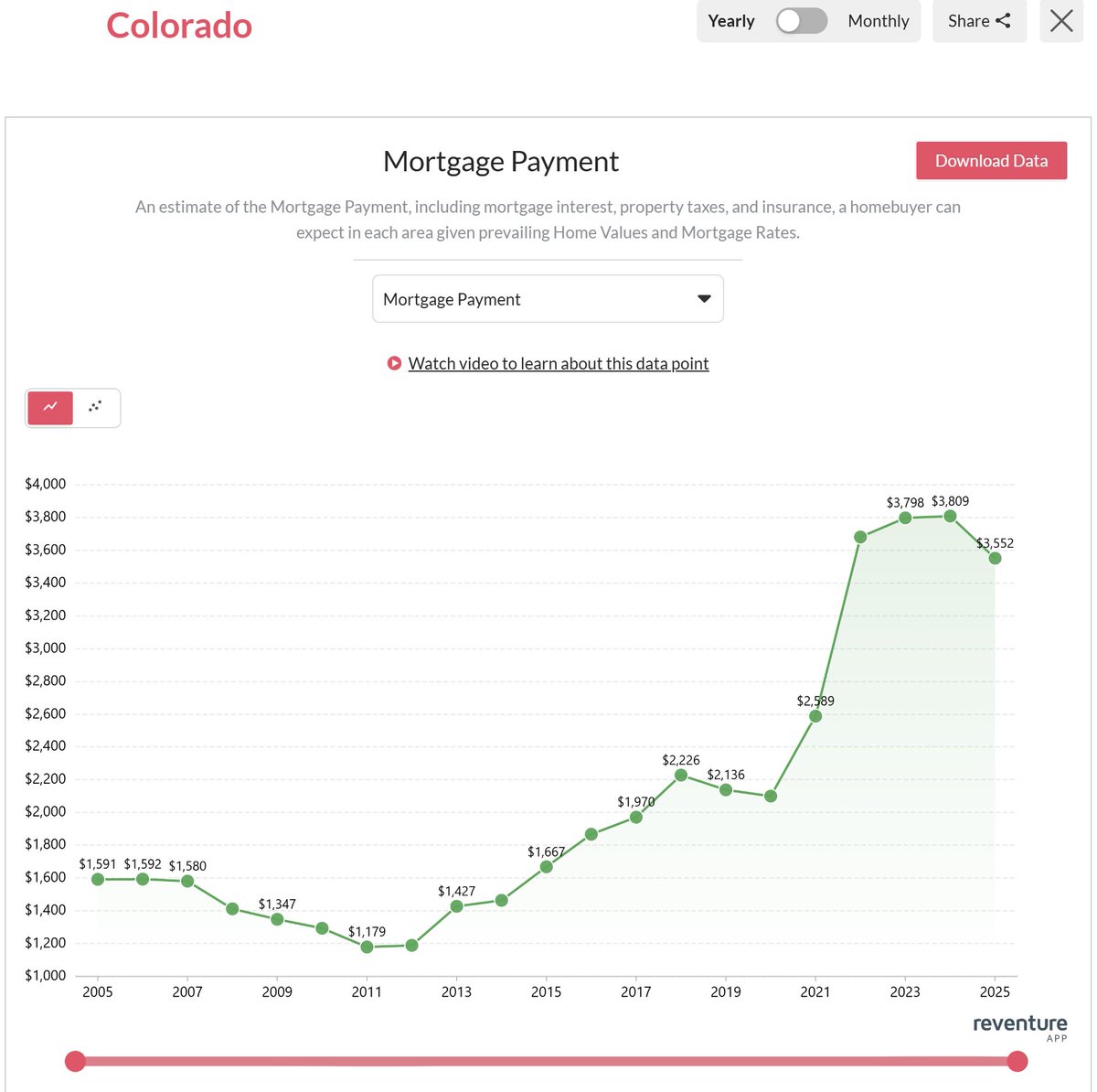

Right now, it costs around $2,800/month to buy a house with a mortgage.

Which is over $700 more per month than the cost to rent.

This math is keeping first-time homebuyers stuck on the sidelines, since it simply doesn't make financial sense to buy in terms of the monthly cost.

Right now, it costs around $2,800/month to buy a house with a mortgage.

Which is over $700 more per month than the cost to rent.

This math is keeping first-time homebuyers stuck on the sidelines, since it simply doesn't make financial sense to buy in terms of the monthly cost.

4) This math between buying and renting is being primarily driven by prices being too high.

Home values, adjusted for inflation, are way above their long-term 130-year average in the U.S.

We've literally never seen anything like this in terms of prices.

Home values, adjusted for inflation, are way above their long-term 130-year average in the U.S.

We've literally never seen anything like this in terms of prices.

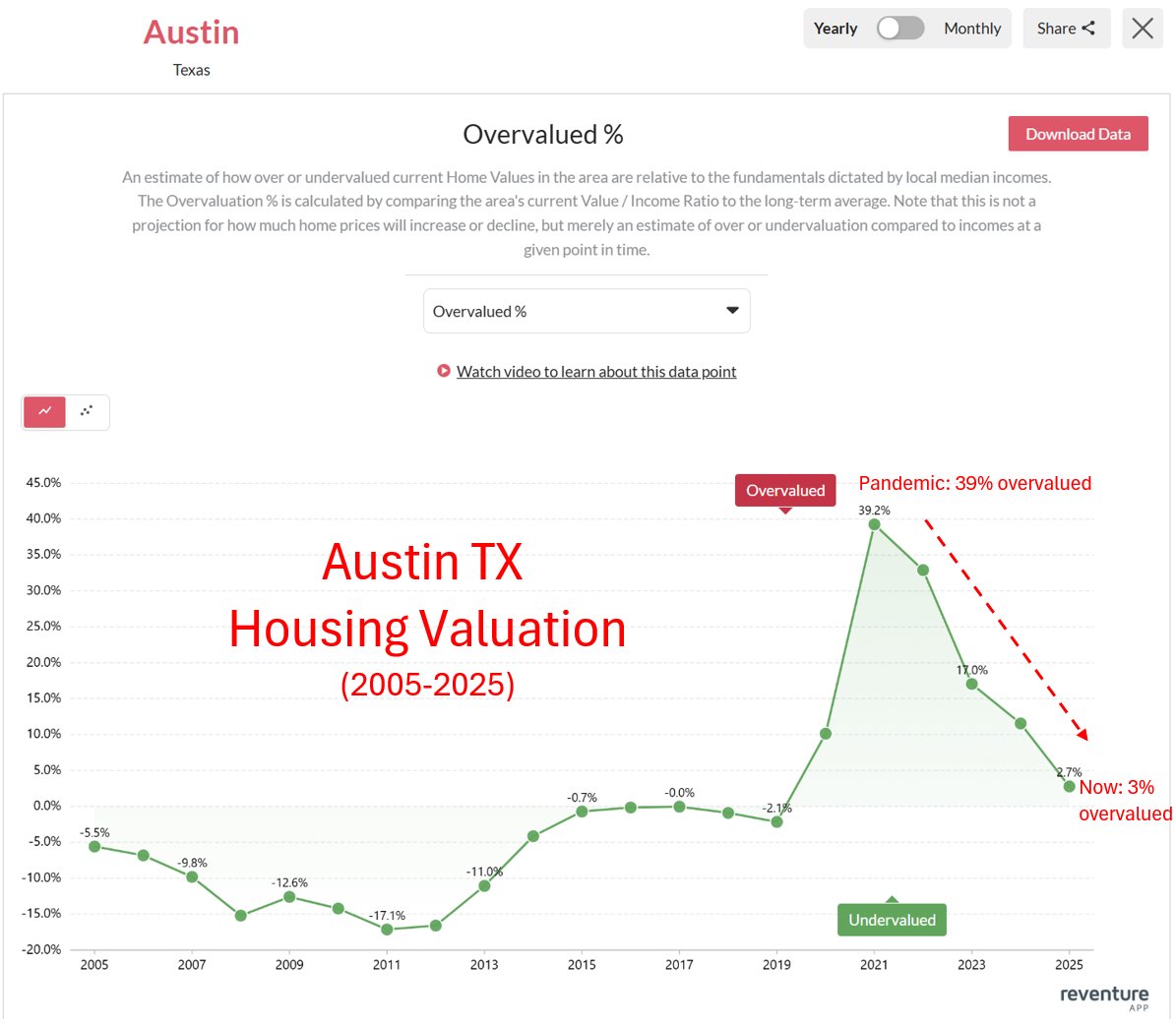

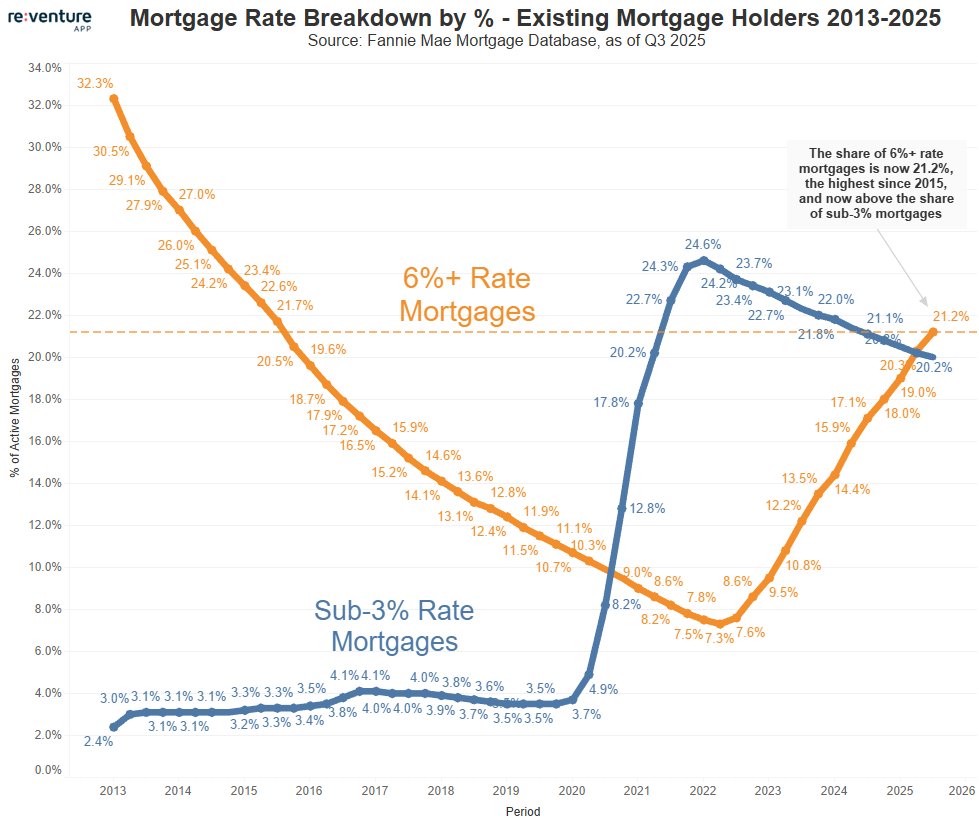

5) And for those who think "mortgage rates" are the problem, check this graph out.

Current Mortgage Rates are very normal in the course of U.S. History.

Current prices are not.

Current Mortgage Rates are very normal in the course of U.S. History.

Current prices are not.

6) The data is so abundantly clear. Buyers are on strike because of prices.

-prices are at all-time highs

-mortgage rates are normal

-buyer demand is at all-time lows

I also polled you here on X, and 71% of you said prices were the problem.

(only 13% said mortgage rates)

-prices are at all-time highs

-mortgage rates are normal

-buyer demand is at all-time lows

I also polled you here on X, and 71% of you said prices were the problem.

(only 13% said mortgage rates)

7) What I am seeing in the market right now is that sellers of existing homes are holding things hostage.

They still want $600,000 for their house, when the market-clearing price is much less.

They saw their neighbor sell for $600,000 3 years ago, and just won't come off that number.

In the end, educating the existing seller population about the true state of the housing market should be the main policy focus of everyone in the housing market.

They still want $600,000 for their house, when the market-clearing price is much less.

They saw their neighbor sell for $600,000 3 years ago, and just won't come off that number.

In the end, educating the existing seller population about the true state of the housing market should be the main policy focus of everyone in the housing market.

8) The worst part about it is that sellers who have this attitude are often in markets that are already declining, and will decline further into the future.

They're shooting themselves in the foot by overlisting their home, and delisting their home, with the misplaced idea that things will improve 6-12 months from now.

They're shooting themselves in the foot by overlisting their home, and delisting their home, with the misplaced idea that things will improve 6-12 months from now.

9) The onus is on local realtors to be the economist of choice and properly educate sellers about where the market is heading.

A more educated seller will list their home better, and attract more buyers, and create more transactions.

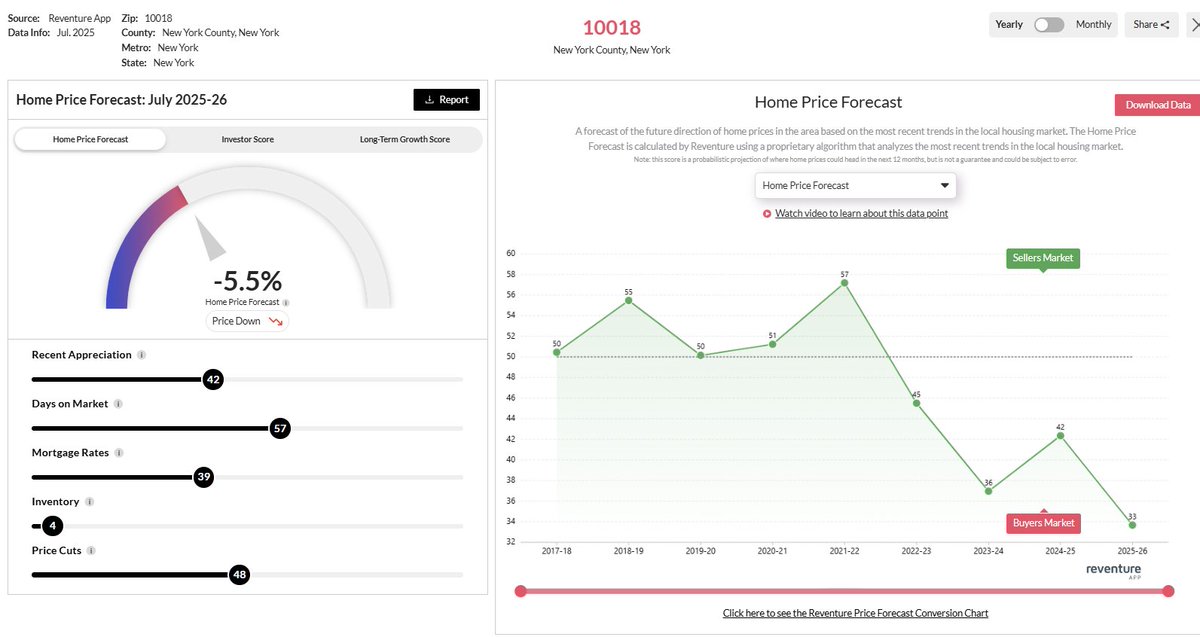

We at Reventure App provide a tool to help with that, with our 12-month price forecast helping ground sellers in reality.

A more educated seller will list their home better, and attract more buyers, and create more transactions.

We at Reventure App provide a tool to help with that, with our 12-month price forecast helping ground sellers in reality.

10) We actually recently added a download market report feature that helps sellers, realtors, and buyers better assess the future direction of their local market and ZIP code.

Access the forecast and download report feature at under a premium plan. Start by typing in your ZIP.reventure.app

Access the forecast and download report feature at under a premium plan. Start by typing in your ZIP.reventure.app

• • •

Missing some Tweet in this thread? You can try to

force a refresh