1/6

Recessions and financial crises can have a profound and lasting impact on an economy for years to come.

We had both in 2020. This changed the economy.

Change does not mean worse or dystopian. It means different. This economy differs from 2019 (pre-COVID).

🧵

Recessions and financial crises can have a profound and lasting impact on an economy for years to come.

We had both in 2020. This changed the economy.

Change does not mean worse or dystopian. It means different. This economy differs from 2019 (pre-COVID).

🧵

https://twitter.com/BobEUnlimited/status/1962171277403210013

2/6

Following every recession, the tenor of inflation shifts.

The current post-COVID recovery, as shown in blue, indicates inflation has reached a significantly higher level, with more volatility (wider standard deviation) than during the post-financial crisis period.

Following every recession, the tenor of inflation shifts.

The current post-COVID recovery, as shown in blue, indicates inflation has reached a significantly higher level, with more volatility (wider standard deviation) than during the post-financial crisis period.

3/6

Something more may be at play, as larger trends in inflation seem to have shifted with the COVID pandemic.

Something more may be at play, as larger trends in inflation seem to have shifted with the COVID pandemic.

4/6

The 20-year decline in 10-year REAL yields (inflation-adjusted) through the post-9/11 recovery and the financial crisis recovery has ended.

The average is now (blue) higher than it was during the previous recovery, and volatility is significantly greater (Std Dev band).

The 20-year decline in 10-year REAL yields (inflation-adjusted) through the post-9/11 recovery and the financial crisis recovery has ended.

The average is now (blue) higher than it was during the previous recovery, and volatility is significantly greater (Std Dev band).

5/6

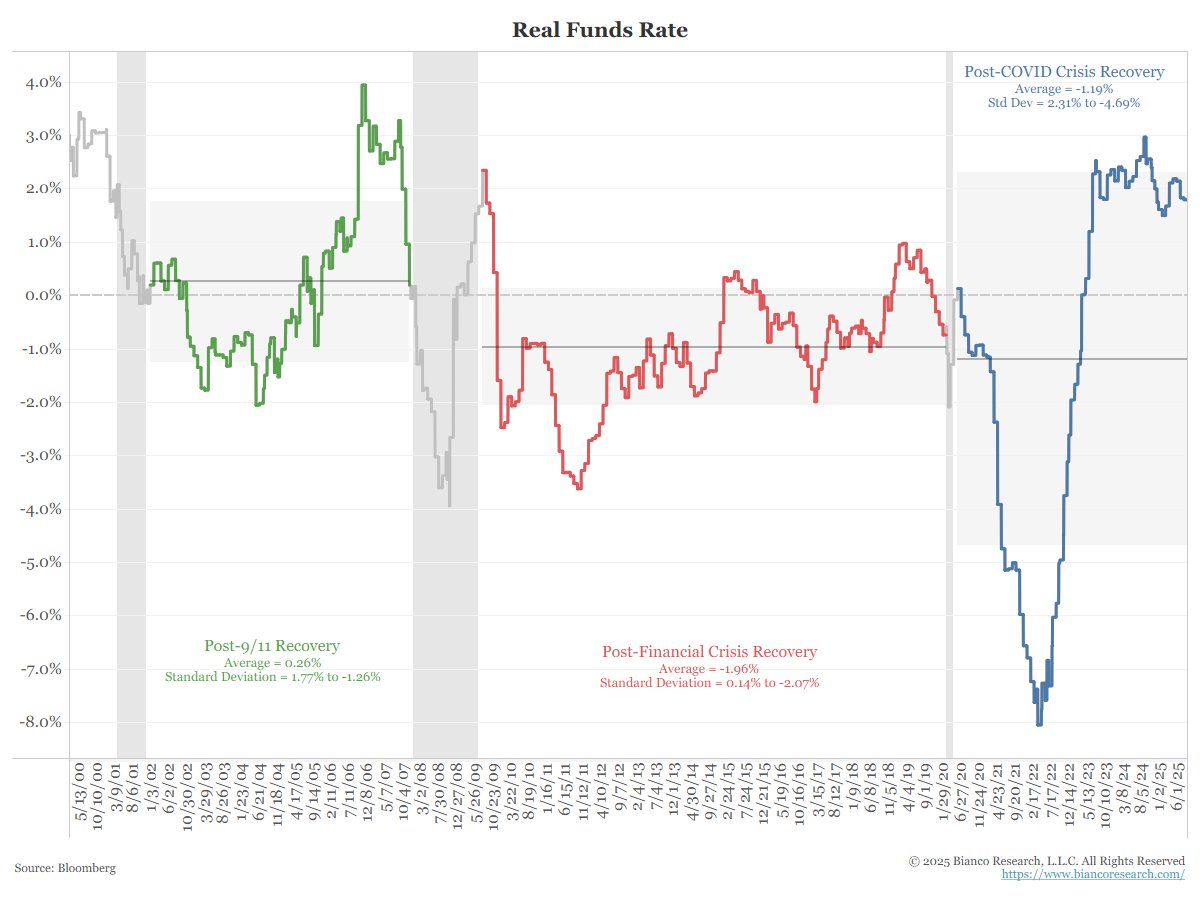

While the real funds rate has been highly volatile in the post-COVID period, it is settling at around 2%.

This would imply a neutral funds rate of at least 4% if the Fed could hit its 2% target.

As the inflation charts above show, the 2% target is not being met.

While the real funds rate has been highly volatile in the post-COVID period, it is settling at around 2%.

This would imply a neutral funds rate of at least 4% if the Fed could hit its 2% target.

As the inflation charts above show, the 2% target is not being met.

6/6

COVID was the biggest economic event of our lifetime. It was bigger than the 2008 financial crisis, 9/11, the Iraq-Kuwait War, and even the Great Inflation of the 1970s and 1980s.

It marked the end of the era of low inflation and zero to negative real interest rates.

COVID was the biggest economic event of our lifetime. It was bigger than the 2008 financial crisis, 9/11, the Iraq-Kuwait War, and even the Great Inflation of the 1970s and 1980s.

It marked the end of the era of low inflation and zero to negative real interest rates.

• • •

Missing some Tweet in this thread? You can try to

force a refresh