MACRO FLOWS 🧵

Every asset lives on two axes of risk:

Duration risk → how inflation erodes value over time

Credit risk → how growth enables or undermines repayment

These forces connect across the entire risk curve. Understanding them is the foundation of macro attribution

Every asset lives on two axes of risk:

Duration risk → how inflation erodes value over time

Credit risk → how growth enables or undermines repayment

These forces connect across the entire risk curve. Understanding them is the foundation of macro attribution

Duration risk = time.

The longer you wait to be paid, the more exposed you are to inflation and rate shifts.

Credit risk = solvency.

The weaker growth is, the higher the chance of default.

Inflation amplifies duration risk.

Growth amplifies credit risk.

The longer you wait to be paid, the more exposed you are to inflation and rate shifts.

Credit risk = solvency.

The weaker growth is, the higher the chance of default.

Inflation amplifies duration risk.

Growth amplifies credit risk.

Map it to the duration risk curve:

Bills = near zero duration.

Long bonds, growth stocks, real estate = high duration.

When inflation is stable, the curve is flat.

When inflation spikes, the curve steepens violently: long-duration assets underperform.

Bills = near zero duration.

Long bonds, growth stocks, real estate = high duration.

When inflation is stable, the curve is flat.

When inflation spikes, the curve steepens violently: long-duration assets underperform.

Map it to the credit risk curve:

Sovereign bills = near zero credit risk.

IG → HY → EM → equities → alts = progressively higher credit risk.

When growth is strong, spreads compress outward.

When growth stalls, spreads blow out and capital rushes back to safety.

Sovereign bills = near zero credit risk.

IG → HY → EM → equities → alts = progressively higher credit risk.

When growth is strong, spreads compress outward.

When growth stalls, spreads blow out and capital rushes back to safety.

Together, these two curves form a multivariate map of capital flows:

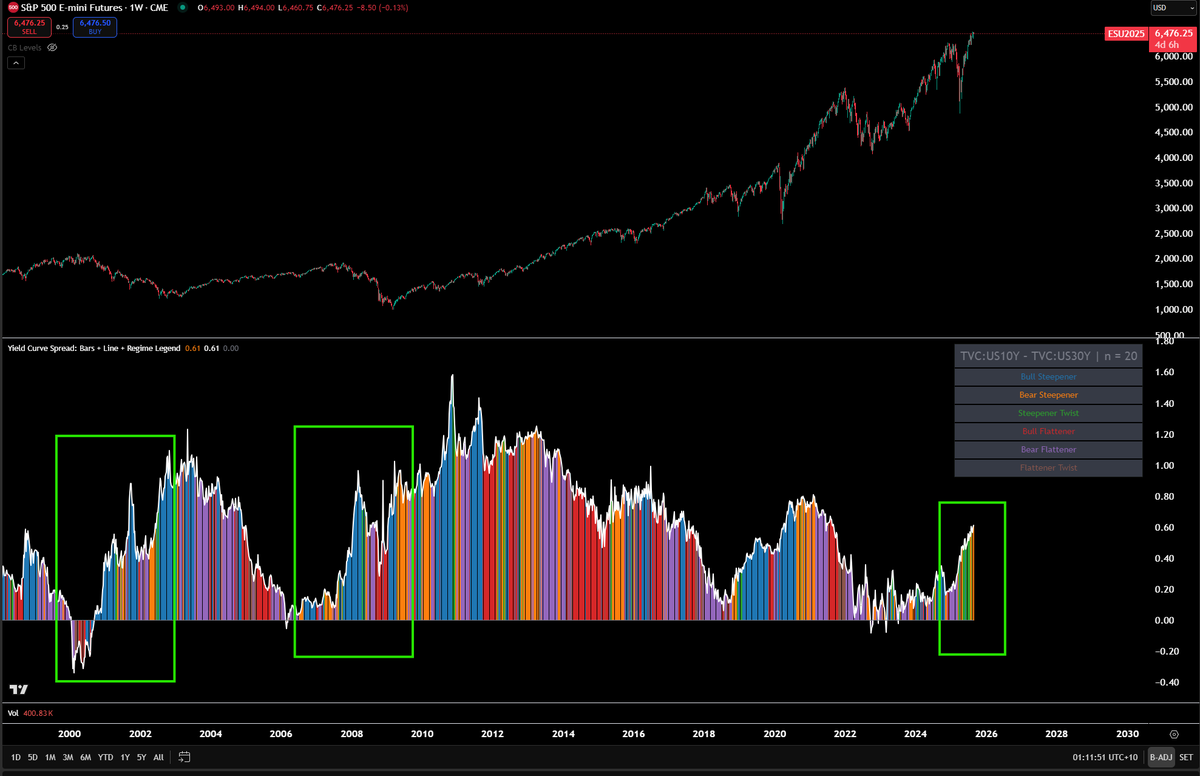

Inflation shock? Duration curve steepens. Bonds and growth equities sell off.

Growth shock? Credit curve steepens. Credit spreads widen, risk assets underperform.

Assets reprice along both curves at once.

Inflation shock? Duration curve steepens. Bonds and growth equities sell off.

Growth shock? Credit curve steepens. Credit spreads widen, risk assets underperform.

Assets reprice along both curves at once.

Attribution analysis means asking:

How much of today’s asset move is duration-driven vs. credit-driven?

Tech stocks falling in 2022 → mostly duration risk repricing.

HY spreads widening in 2020 → credit risk repricing.

2022 stagflation → both curves steepened at once. That’s why nothing worked.

How much of today’s asset move is duration-driven vs. credit-driven?

Tech stocks falling in 2022 → mostly duration risk repricing.

HY spreads widening in 2020 → credit risk repricing.

2022 stagflation → both curves steepened at once. That’s why nothing worked.

The net effect across the risk curve comes from the interaction of the two.

Growth with stable inflation = sweet spot. Duration and credit risks both compressed. All assets rally.

Inflation with weak growth = toxic. Both curves steepen. Correlations go to one.

That’s the macro map.

Growth with stable inflation = sweet spot. Duration and credit risks both compressed. All assets rally.

Inflation with weak growth = toxic. Both curves steepen. Correlations go to one.

That’s the macro map.

This is the simplest framework that explains why assets move together or diverge.

Duration risk maps to inflation.

Credit risk maps to growth.

The balance between the two curves sets the distribution of outcomes across the risk curve.

That’s the core of macro attribution.

Duration risk maps to inflation.

Credit risk maps to growth.

The balance between the two curves sets the distribution of outcomes across the risk curve.

That’s the core of macro attribution.

All the educational primers explaining these forces are free here: capitalflowsresearch.com/p/research-syn…

• • •

Missing some Tweet in this thread? You can try to

force a refresh