How to find new investments?

Small-cap focused blogs are some of the best hunting grounds for idea generation.

Here are 10 new blogs I’ve been tracking over the past year 👇

Small-cap focused blogs are some of the best hunting grounds for idea generation.

Here are 10 new blogs I’ve been tracking over the past year 👇

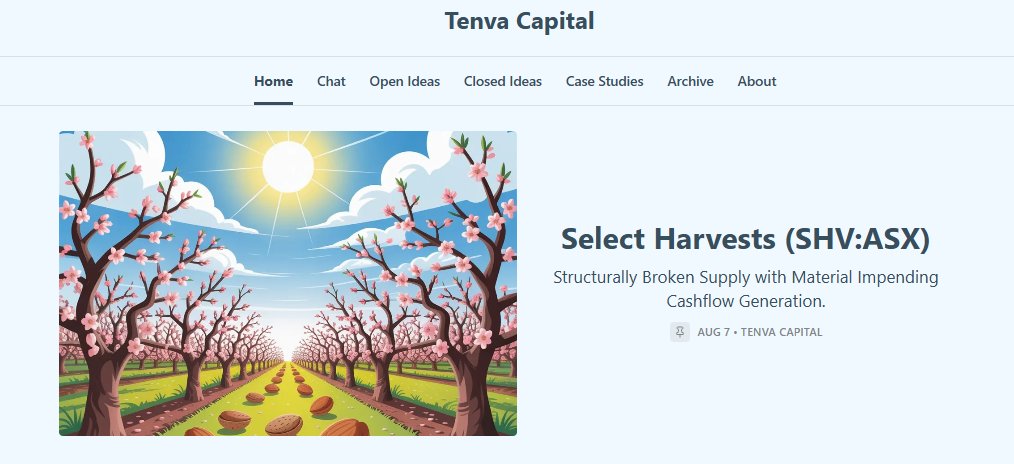

1/ @TenvaCapital's blog is a great source of deep-dive writeups on small & mid-cap Australian names.

Posts are research-heavy, clearly structured, and focused on undervalued companies with strong earnings momentum.

Posts are research-heavy, clearly structured, and focused on undervalued companies with strong earnings momentum.

Recent posts on Tenva Capital:

$PNC.AX: Turnaround on the cusp of a major step-change in earnings, driven by improving industry fundamentals.

$SHV.AX: Only listed almond pure play, benefiting from reshaped S&D as California’s groundwater cuts hit 76% of global supply.

$PNC.AX: Turnaround on the cusp of a major step-change in earnings, driven by improving industry fundamentals.

$SHV.AX: Only listed almond pure play, benefiting from reshaped S&D as California’s groundwater cuts hit 76% of global supply.

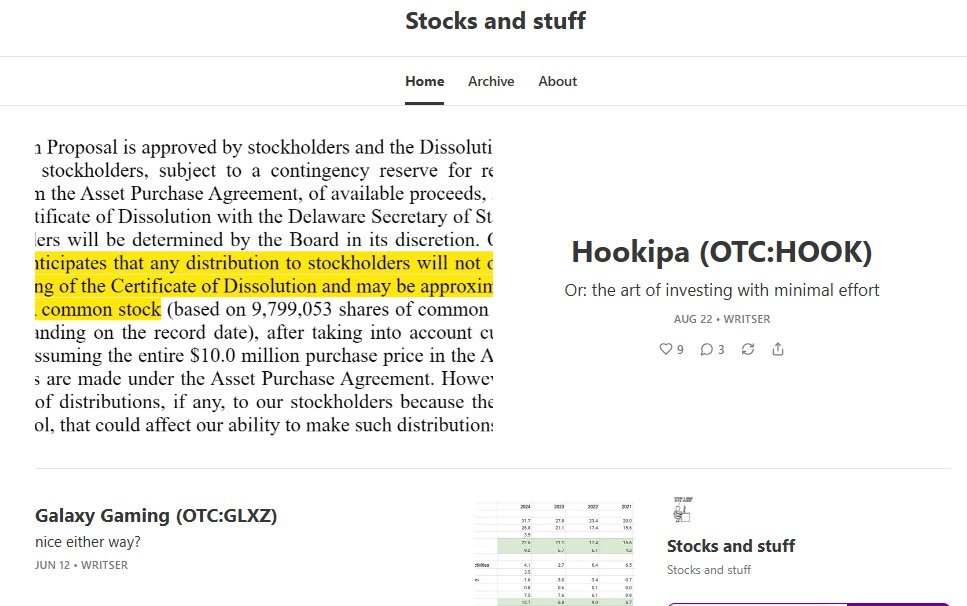

2/@thewritser's recently launched a special-situations focused blog.

He is a sharp event-driven investor with a long history on fintwit. His blog writeups are short, clear, and easy to follow.

He is a sharp event-driven investor with a long history on fintwit. His blog writeups are short, clear, and easy to follow.

Recent posts on Stocks and Stuff:

$GLXZ – Merger arb with Evolution AB; antitrust risk priced in, but strong IP licensing model + debt refi make standalone attractive.

$HOOK – Liquidation play; assets sold to Gilead, delisting/illiquidity create mispricing with 15–20% IRR.

$GLXZ – Merger arb with Evolution AB; antitrust risk priced in, but strong IP licensing model + debt refi make standalone attractive.

$HOOK – Liquidation play; assets sold to Gilead, delisting/illiquidity create mispricing with 15–20% IRR.

3/ @Mike10947310 frequent deep dives on stocks with 2-year upside potential.

Special emphasis on event-driven, reflexive, and microcap situations.

Special emphasis on event-driven, reflexive, and microcap situations.

Recent posts on Multibagger Monitor:

$FEIM: US PT&F leader; LEO + “Golden Dome” tailwinds; early quantum-sensing foothold; trades at multi-year low multiples.

$AMPG – ORAN 5G LNAs/radios; $118M LOIs from 2 Tier-1s; trading at 1x NTM EV/Revs despite 125% growth

$FEIM: US PT&F leader; LEO + “Golden Dome” tailwinds; early quantum-sensing foothold; trades at multi-year low multiples.

$AMPG – ORAN 5G LNAs/radios; $118M LOIs from 2 Tier-1s; trading at 1x NTM EV/Revs despite 125% growth

4/ @310Value shares deep-dive writeups on undervalued Canadian and US stock.

Transformation stories with a catalyst and classic value stocks. Long form write ups with easy to follow structure.

Transformation stories with a catalyst and classic value stocks. Long form write ups with easy to follow structure.

Recent post on 310 Value’s Newsletter

$SES.TO: Secure Waste Infrastructure (ex-Secure Energy). Repurchased 25%+ of stock, attracted new investors, and re-rated, yet still at 7.9× 25E EBITDA vs waste peers in teens. Few catalysts remain potential upside 70%.

$SES.TO: Secure Waste Infrastructure (ex-Secure Energy). Repurchased 25%+ of stock, attracted new investors, and re-rated, yet still at 7.9× 25E EBITDA vs waste peers in teens. Few catalysts remain potential upside 70%.

5/ @adriantford write ups on the smallest, most illiquid, and least-followed public companies globally.

Value stocks as well as special sits. Short to the point pitches every other month.

Value stocks as well as special sits. Short to the point pitches every other month.

Recent post on Overlooked and Undervalued:

$ULT.L: UK consumer goods group (Salter, Beldray, Russell Hobbs license). Capital-light, founder-led, history of growth. Trades ~7× EBIT. European expansion + efficiency gains offer upside, insiders own >40%.

$ULT.L: UK consumer goods group (Salter, Beldray, Russell Hobbs license). Capital-light, founder-led, history of growth. Trades ~7× EBIT. European expansion + efficiency gains offer upside, insiders own >40%.

6/ @ppinvest shares value + momentum-driven writeups on overlooked small caps.

No industry or geography limits: focus is on growth and inflection stories.

No industry or geography limits: focus is on growth and inflection stories.

Recent post PPinvest:

$NURS.V / $HYDTF: “Uber for Nurses.” Revenue grew from $3M ’22 → $16M ’24, now profitable. Scalable SaaS telehealth platform (VSDHOne) positions it for explosive growth; multibagger upside already starting to work out.

$NURS.V / $HYDTF: “Uber for Nurses.” Revenue grew from $3M ’22 → $16M ’24, now profitable. Scalable SaaS telehealth platform (VSDHOne) positions it for explosive growth; multibagger upside already starting to work out.

7/ @AnotherBio busted/overlooked biotech focused investor.

Catalyst-heavy US biotech deep dives. Clearly structured writeups. We cross paths on plenty of busted biotech, that's for sure.

Catalyst-heavy US biotech deep dives. Clearly structured writeups. We cross paths on plenty of busted biotech, that's for sure.

Recent post on BiotechBonanza:

$PTGX: Peptide developer (JNJ/Takeda partners); 2 FDA-bound drugs (high PoS); cash-secure, no dilution risk; JNJ drug alone > EV, rest is free optionality with a clear path to 3x returns in 18 to 36 month.

$PTGX: Peptide developer (JNJ/Takeda partners); 2 FDA-bound drugs (high PoS); cash-secure, no dilution risk; JNJ drug alone > EV, rest is free optionality with a clear path to 3x returns in 18 to 36 month.

8/ @RohanSoor shares deep dives on overlooked stocks without industry or geography focus.

Mostly microcap value stocks as well as special situations.

Mostly microcap value stocks as well as special situations.

Recent post on Central Tendency:

$BGO.L: Leading payments co trading at ~7.5× EBITDA; profits inflecting as SaaS subs (+100% YoY) scale; long runway, recent integration drag fading.

$BGO.L: Leading payments co trading at ~7.5× EBITDA; profits inflecting as SaaS subs (+100% YoY) scale; long runway, recent integration drag fading.

9/ @RealAssetsValue focused on US & Canada REITs.

Primarily value plays, but also catalyst-driven setups. Deep real estate market understanding with detailed and clear financial modeling.

Primarily value plays, but also catalyst-driven setups. Deep real estate market understanding with detailed and clear financial modeling.

Recent post on Real Assets, Real Value

$VRE: NJ waterfront apartment REIT trading at >25% discount to NAV, 1/5 of portfolio sold or under contract, potential M&A target.

$VRE: NJ waterfront apartment REIT trading at >25% discount to NAV, 1/5 of portfolio sold or under contract, potential M&A target.

10/ Triple S Special Situations focused on distressed equity and special sits, with a recent skew toward international arbitration bets.

Mostly deep dives, without a specific geographical focus.

Mostly deep dives, without a specific geographical focus.

Recent post on Triple S Special Situations Investing:

$EQX.AX: Australian miner turned into a litigation play; $30m mcap vs. $529m–$2B Congo ICSID claim (95% to shareholders, no funder). Final hearing Nov ’25; potential Guinea claim is free upside.

$EQX.AX: Australian miner turned into a litigation play; $30m mcap vs. $529m–$2B Congo ICSID claim (95% to shareholders, no funder). Final hearing Nov ’25; potential Guinea claim is free upside.

End/ That’s it for today. Thanks for reading.

Part 2 is likely coming soon, as I’ve left out a few more blogs worth mentioning.

And of course, any hints on other candidates are always welcome.

Part 2 is likely coming soon, as I’ve left out a few more blogs worth mentioning.

And of course, any hints on other candidates are always welcome.

• • •

Missing some Tweet in this thread? You can try to

force a refresh