The Argentine's are pushing for a direct loan (which risks being a bailout for an unsustainable policy regime ... ) from the United States through the Exchange Stabilization Fund

But I suspect the question of what more the IMF can do will also come up ...

1/

But I suspect the question of what more the IMF can do will also come up ...

1/

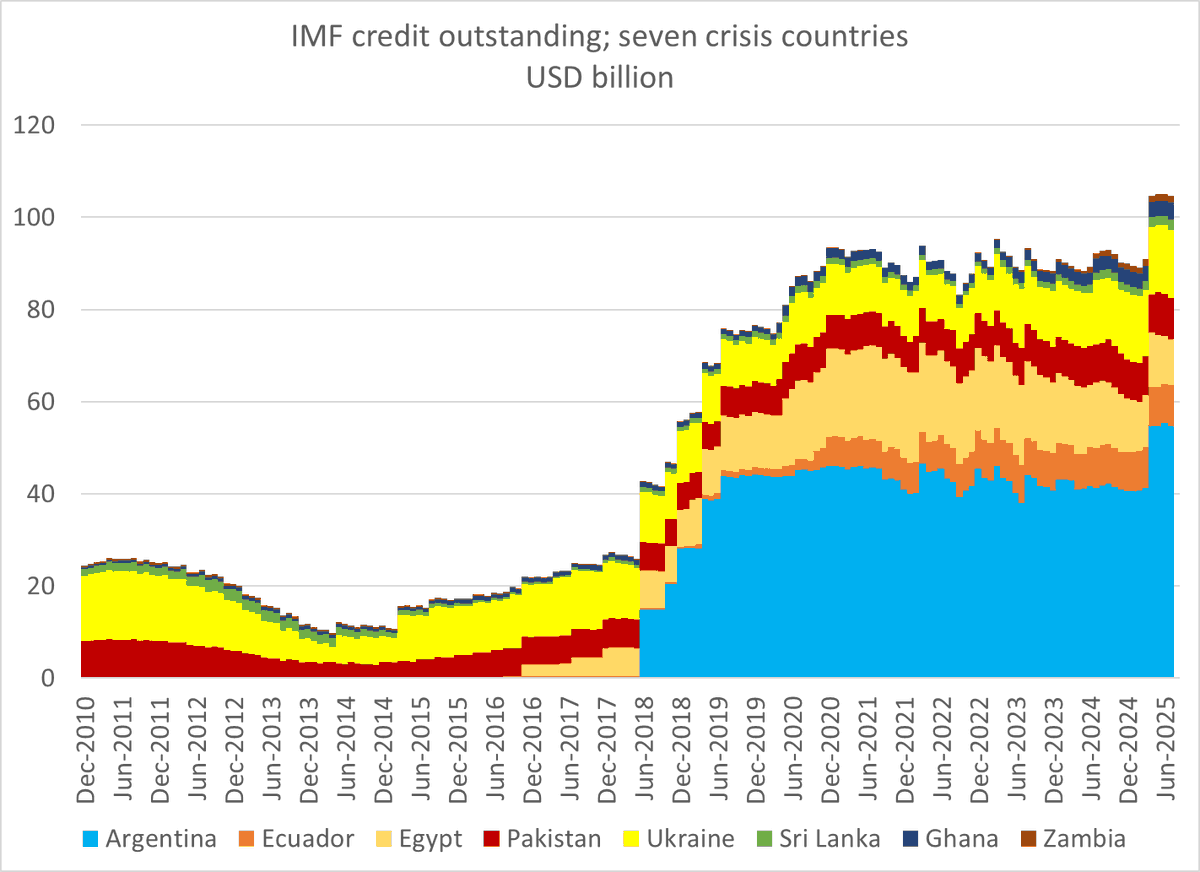

The Fund has only lent out about a quarter of its quota resources, so it has the funds ...

2/

2/

The issue is one of balance sheet concentration -- Argentina is getting close to being about 1/2 of all outstanding non concessional Fund credit ...

3/

3/

As a share of Argentina's GDP, Fund exposure is large -- but it could be raised in extremis ... (note GDP is now inflated by the overvalued peso)

4/

4/

The real issue isn't a balance sheet one (imo) it is a policy one -- namely does it make sense to double down on the current policy framework (including a defense of the peso at the edge of the band that could deplete Argentina's limited reserves) or not ...

5/

5/

My vote is no -- it doesn't make sense to double down on the current program.

But that is the key call.

There are all policy options here (a broader band so more peso depreciation, a bond debt reprofiling, etc)

6/

But that is the key call.

There are all policy options here (a broader band so more peso depreciation, a bond debt reprofiling, etc)

6/

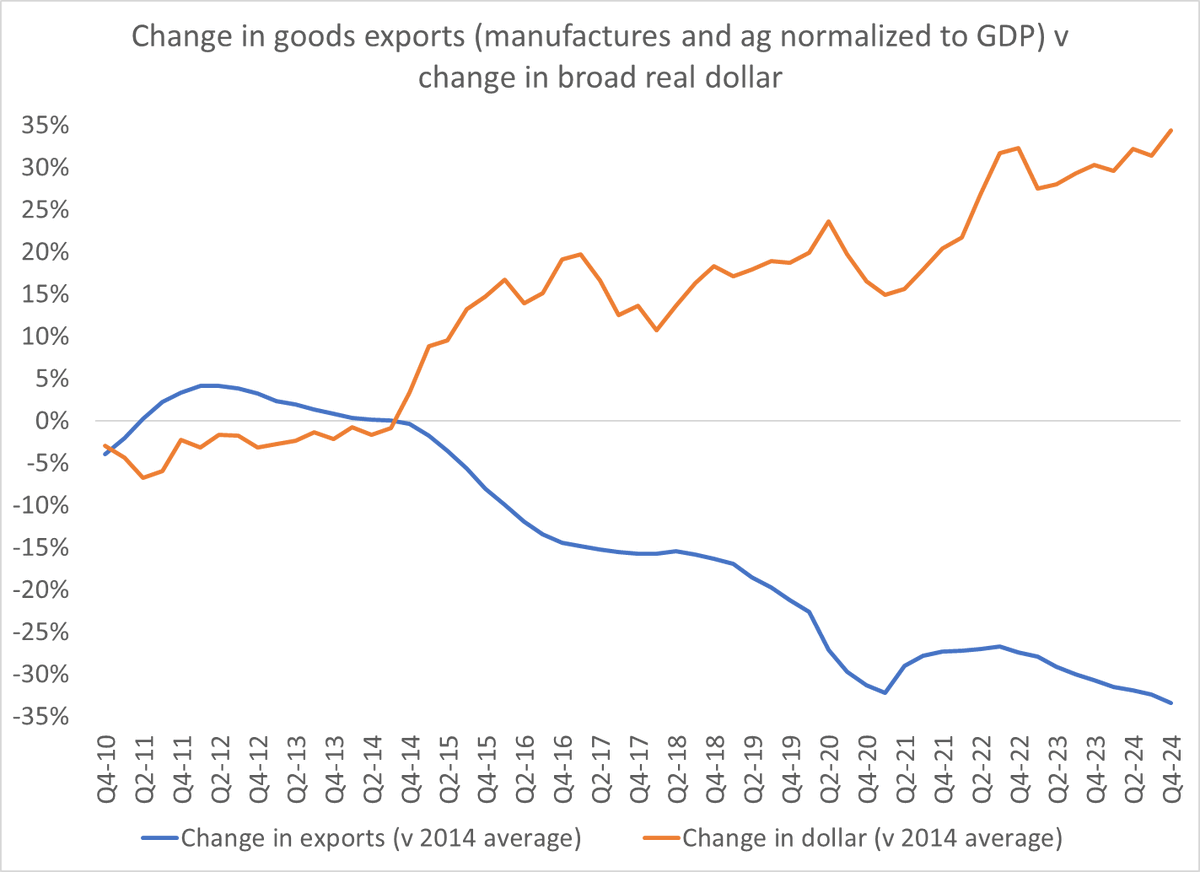

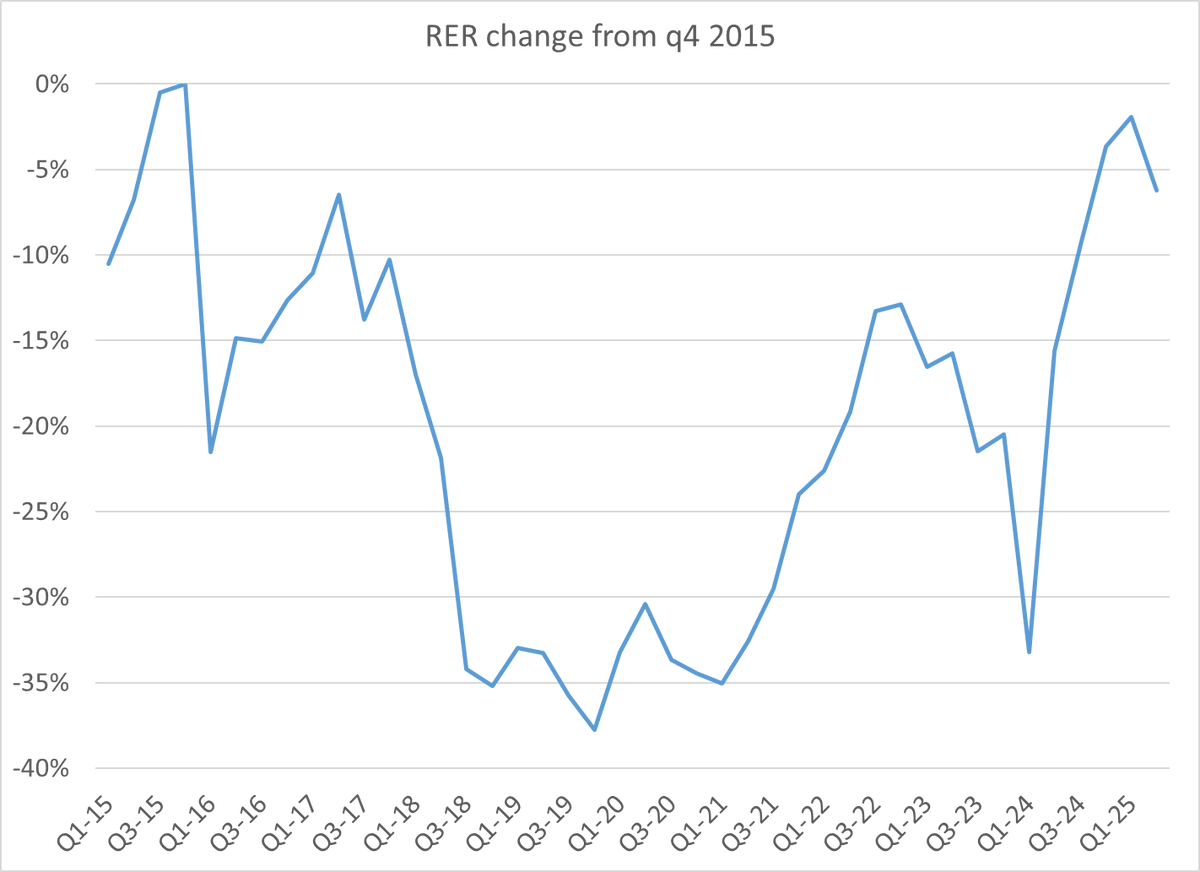

and my personal view is that the peso is still significantly overvalued (last data point in chart is end June) for a country with Argentina's mix of external debt (a lot) and reserves (not many)

7/7

7/7

• • •

Missing some Tweet in this thread? You can try to

force a refresh