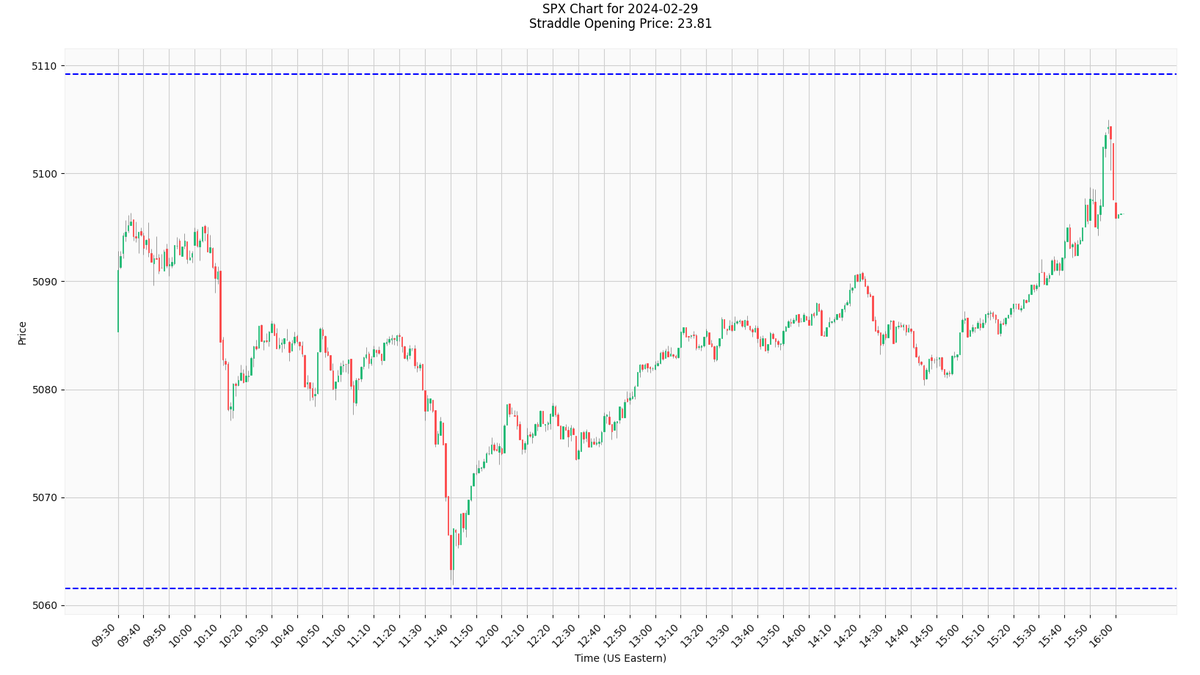

Gamma defines how markets behave,

not which direction they'll move

When dealers are net short options that creates 'negative Gamma'

instead of providing liquidity we have to buy into rising markets and sell into declines

not which direction they'll move

When dealers are net short options that creates 'negative Gamma'

instead of providing liquidity we have to buy into rising markets and sell into declines

When dealers are net long options that creates 'positive Gamma'

we sell rallies and buy dips-

this is the norm for modern markets

we sell rallies and buy dips-

this is the norm for modern markets

It's common for markets to have EXTREME positive Gamma

but very uncommon for markets to have EXTREME negative Gamma

why?

but very uncommon for markets to have EXTREME negative Gamma

why?

When customers sell us options, we mark implied vols lower

All things equal, when you lower the implied volatility of an option, the amount of Gamma it has goes UP

...think about that-

All things equal, when you lower the implied volatility of an option, the amount of Gamma it has goes UP

...think about that-

When customers are selling us options-

we are:

1 - getting long lots of options (more positive gamma)

2 - lowering the implied volatility of the options we are long (even MORE positive gamma)

we are:

1 - getting long lots of options (more positive gamma)

2 - lowering the implied volatility of the options we are long (even MORE positive gamma)

When customers are buying options from us-

we are:

1 - getting short lots of options (more negative gamma)

2 - raising the implied volatility of the options we are short (this REDUCES the gamma per option)

we are:

1 - getting short lots of options (more negative gamma)

2 - raising the implied volatility of the options we are short (this REDUCES the gamma per option)

Read the last two tweets again-

there's an embedded asymmetry in the impact which options can have on the market, from a practical perspective

of course, at times, we are locally short lots of low volatility options and negative Gamma can be extreme

there's an embedded asymmetry in the impact which options can have on the market, from a practical perspective

of course, at times, we are locally short lots of low volatility options and negative Gamma can be extreme

but most of the time the market will benefit from how MMs price options in accordance with inventories

• • •

Missing some Tweet in this thread? You can try to

force a refresh