Career SPX market maker.

See how options move markets with VS3D™ by VolSignals— the only dealer hedging flows platform built entirely by market makers.

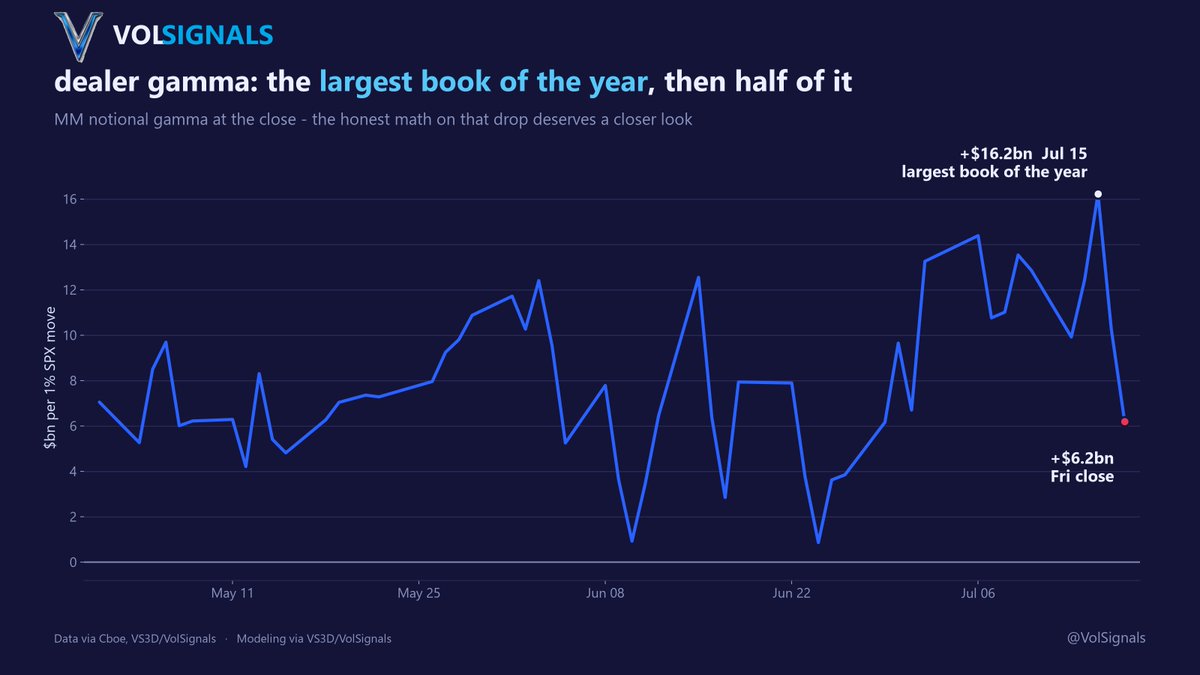

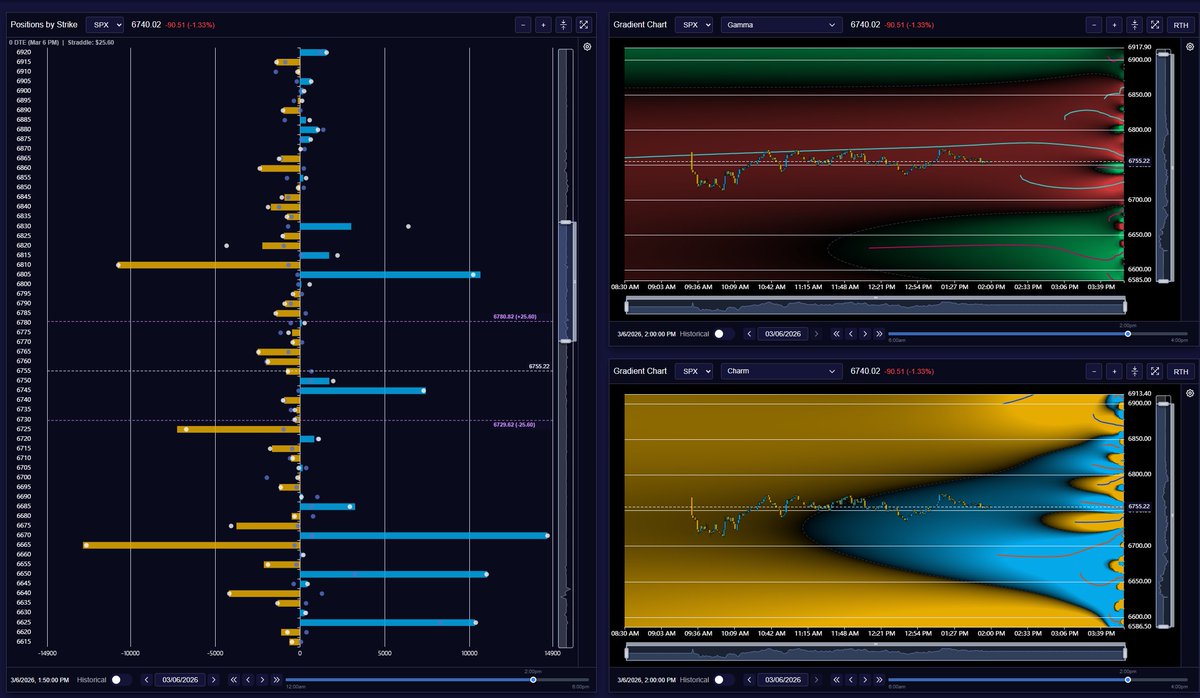

Most people compare headline gamma prints

Most people compare headline gamma prints

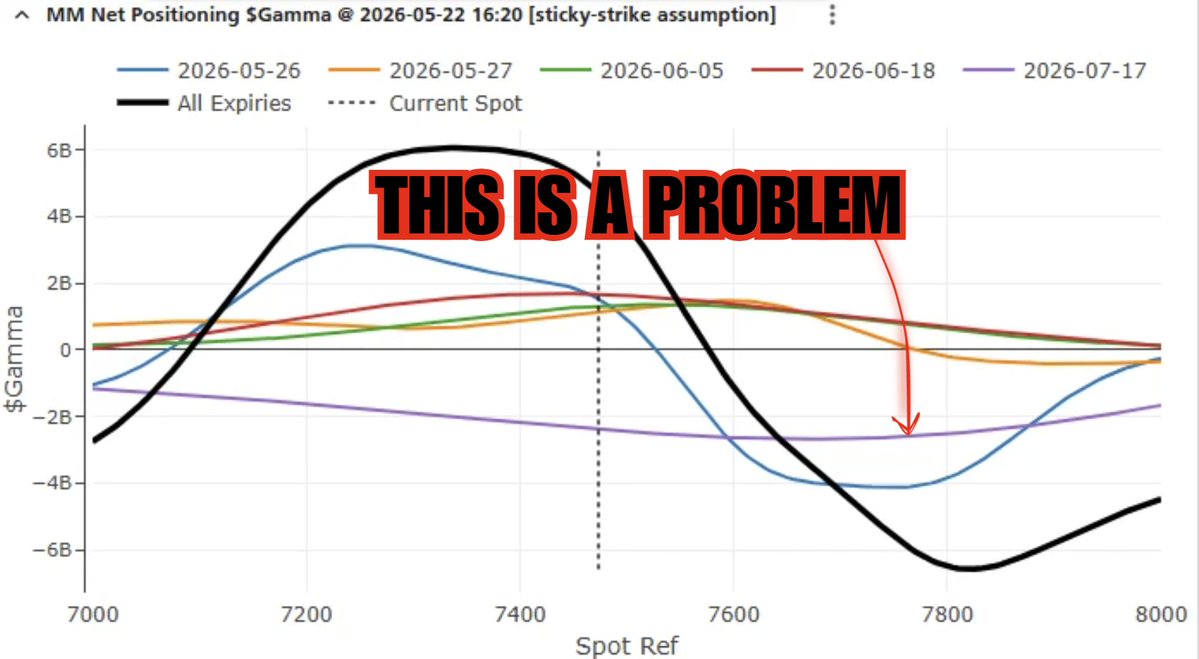

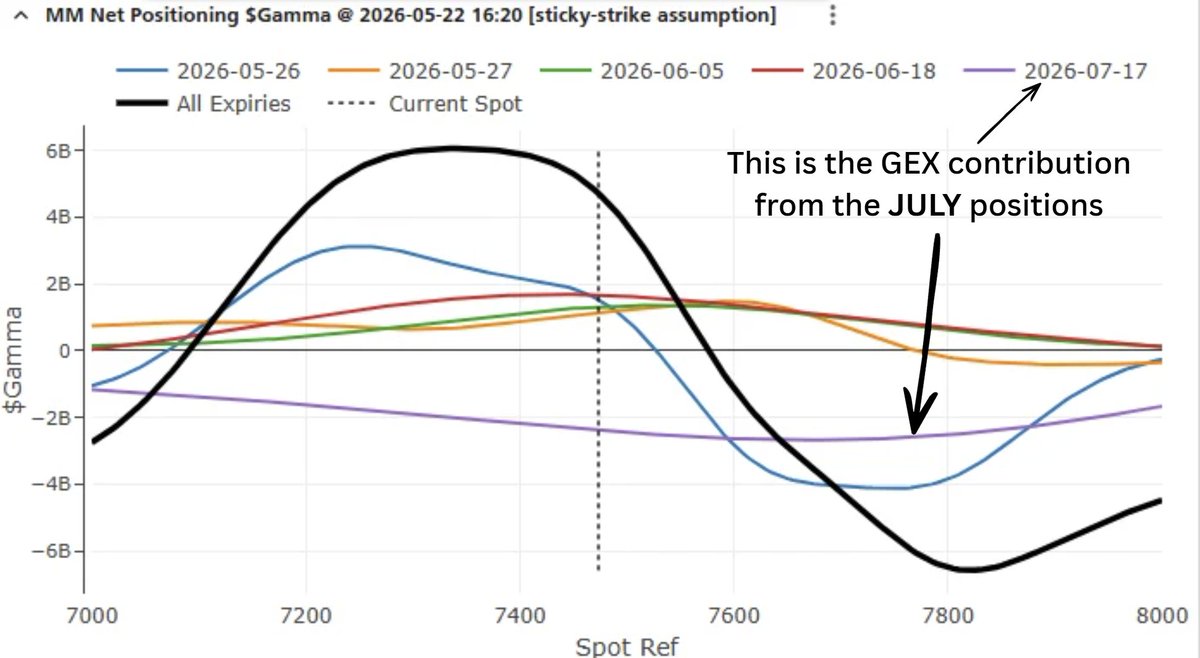

The clue is in the deconstructed GEX profile.

The clue is in the deconstructed GEX profile.

RTM is a premium retail day-trading community and a proprietary algorithmic model known.

RTM is a premium retail day-trading community and a proprietary algorithmic model known.

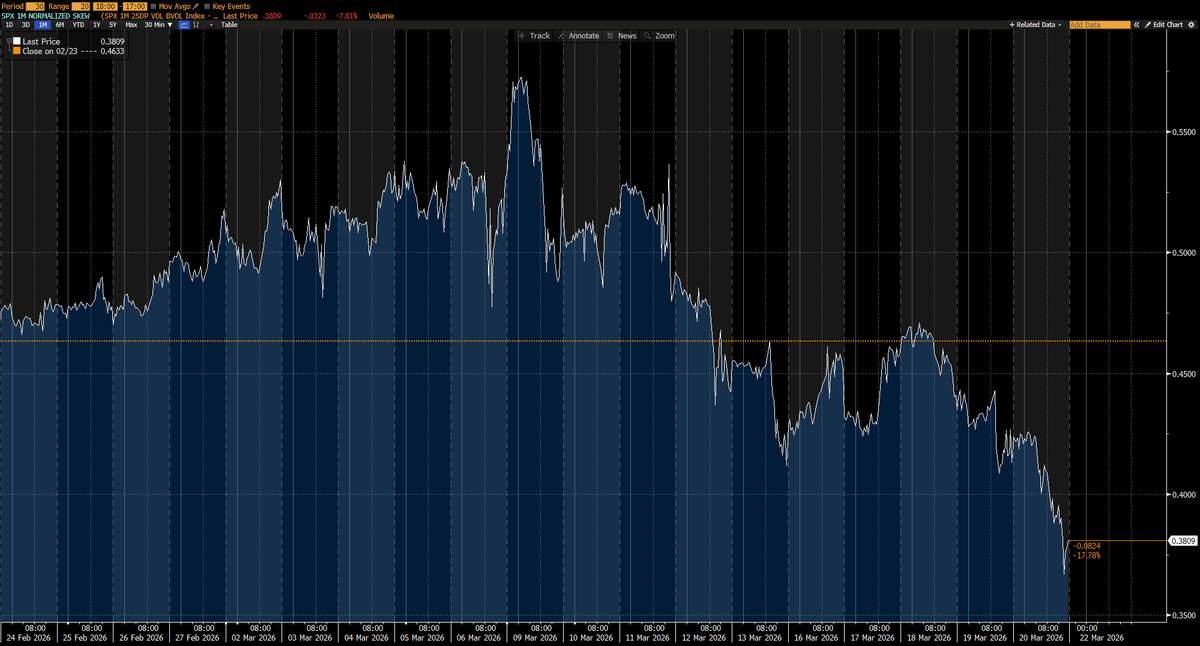

Everyone claims skew crashes because

Everyone claims skew crashes because Price doesn't gravitate towards a near-dated short option the same way it does a long option.

Price doesn't gravitate towards a near-dated short option the same way it does a long option.  Your dashboard is your lens into the REAL options market

Your dashboard is your lens into the REAL options market

Longer tenor options literally have different gamma profiles.

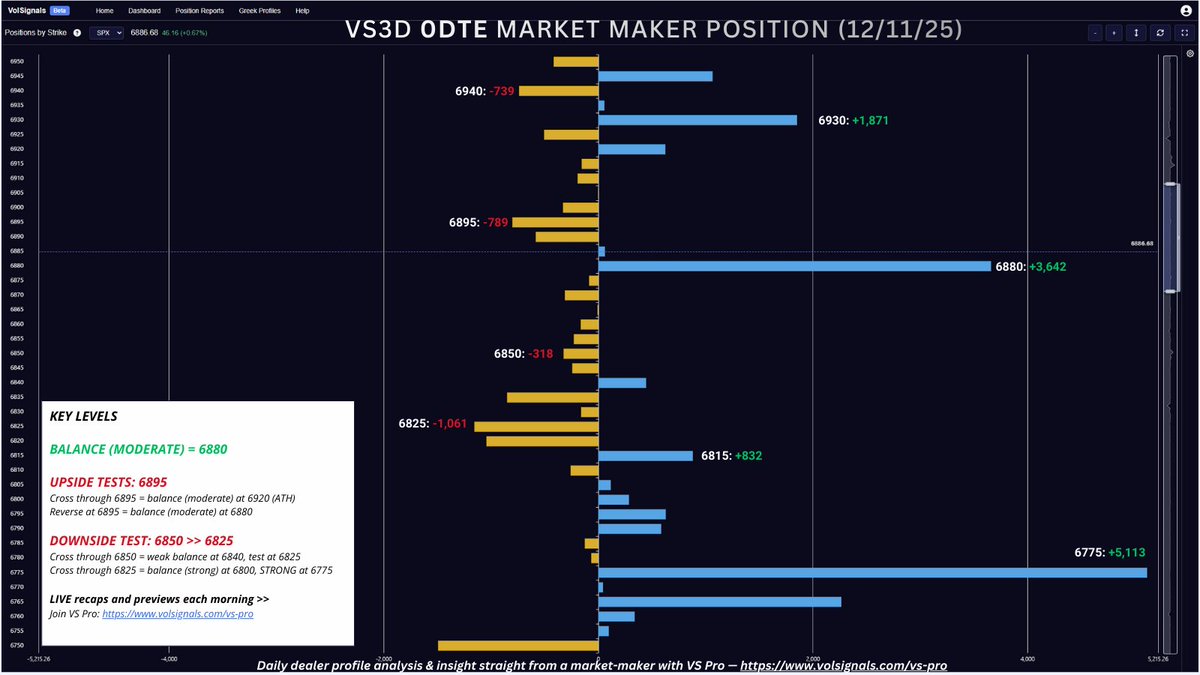

Longer tenor options literally have different gamma profiles. Across the 6800s for Friday's expiry-

Across the 6800s for Friday's expiry- The simple way to understand their behavior -

The simple way to understand their behavior -

First, that figure is Notional Gamma

First, that figure is Notional Gamma First, let's define some things up front:

First, let's define some things up front:

VS3D GAMMA PROFILE

VS3D GAMMA PROFILE

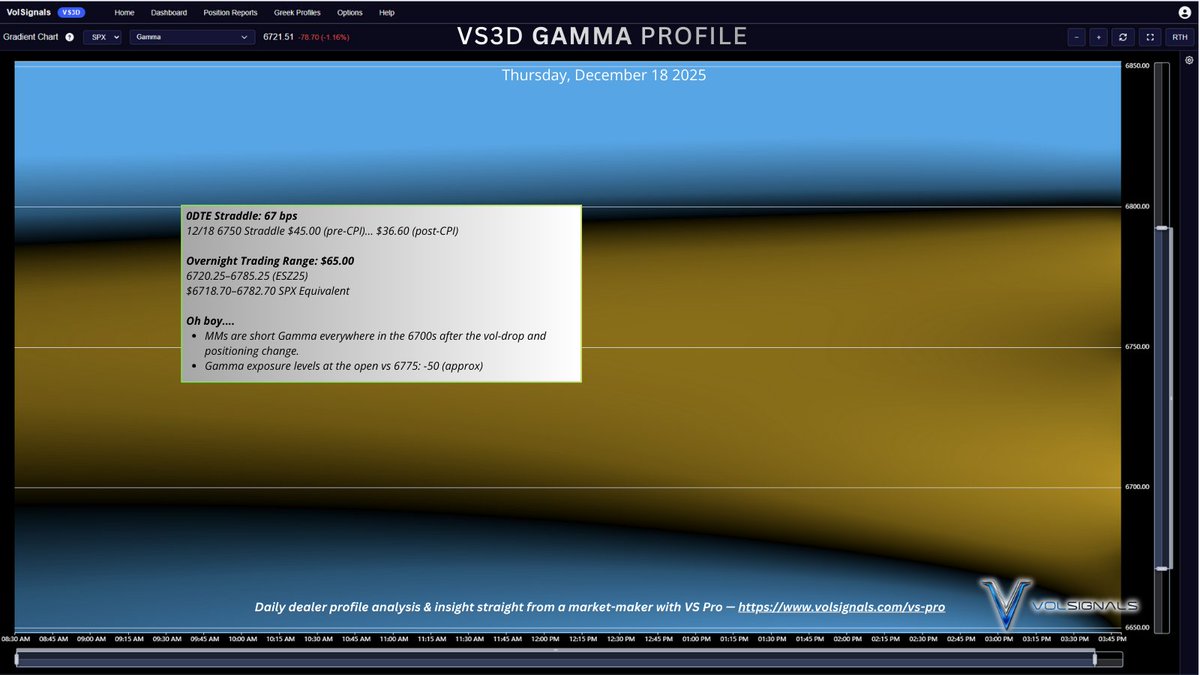

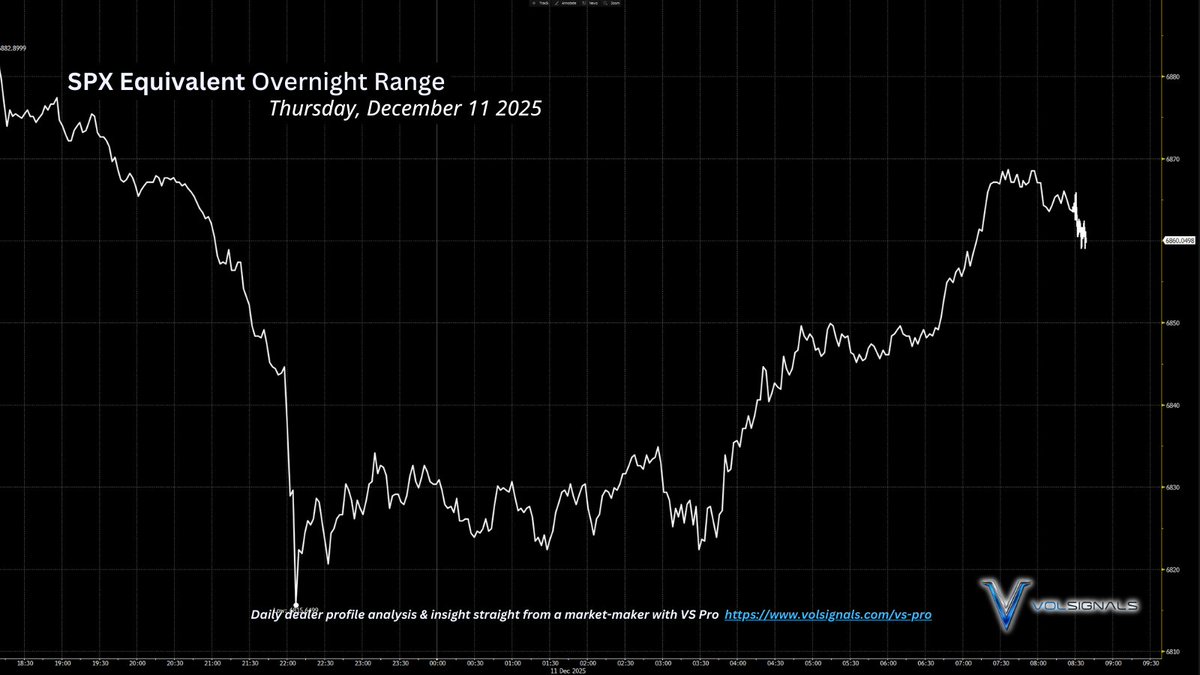

THE OVERNIGHT PRICE ACTION

THE OVERNIGHT PRICE ACTION

What's GAMMA when it comes to option hedging?

What's GAMMA when it comes to option hedging?