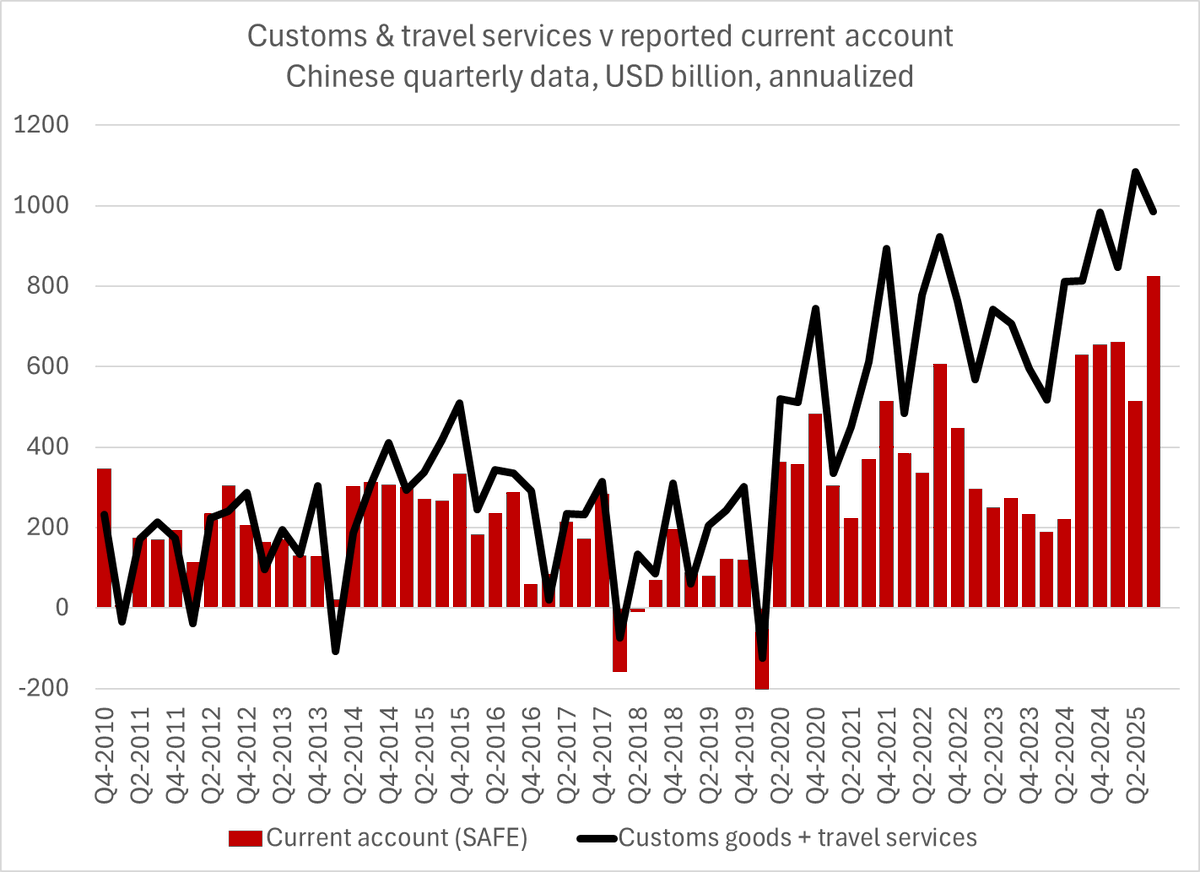

China's goods and services data on a balance of payments basis is now effectively out for q3 (with the September monthly data) -- and on a balance of payments basis, exports jumped up a bit in q3

1/

1/

The q2 surplus using China's (whacky) BoP methodology was well below the q2 customs surplus -- but the q3 BoP surplus is strong, and up v q2 (while the customs surplus is down)

2/

2/

So my estimate for the q3 current account surplus is just over $200b ($800b annualized) -- or well above q2 ...

3/

3/

That would pull the trailing 4q sum of the reported current account surplus to ~ $660b, or (gulp) $300b more than @IMFNews estimated in the External Sector Report (the IMF's current account forecasting needs some work!; look at the lagged RER!)

4/

4/

@IMFNews The q3 jump is a bit fake -- my underlying tracking data suggests q2 was every bit as big. China's new methodology introduces a bit of a randomwalk into the reported data (or a not so random walk if the CA maps to visible financial outflows)

5/

5/

@IMFNews Given China's $1.2 trillion customs surplus, the tourism deficit (~ $200b) and positive net int. investment position, I think the true current account surplus should be around $1 trillion. The q3 surplus may get a bit closer to that number!

6/

6/

@IMFNews And that is not because the underlying data changed, but rather because the gap between the underlying customs surplus and the goods surplus reported using China's balance of payments methodology shrank

7/7

7/7

• • •

Missing some Tweet in this thread? You can try to

force a refresh