Stock–Flow Consistent Formulation of

Kalecki–Young Sectoral Inflation Decomposition (KYSID)

"Recasting KYSID within a stock–flow consistent (SFC) framework clarifies that the inflation process is a balance-sheet outcome."

Kalecki–Young Sectoral Inflation Decomposition (KYSID)

"Recasting KYSID within a stock–flow consistent (SFC) framework clarifies that the inflation process is a balance-sheet outcome."

Core flow-of-funds identity

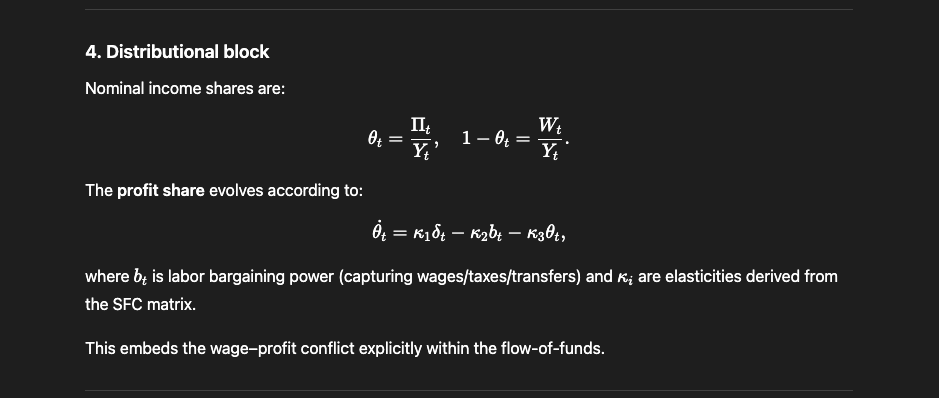

Distributional block

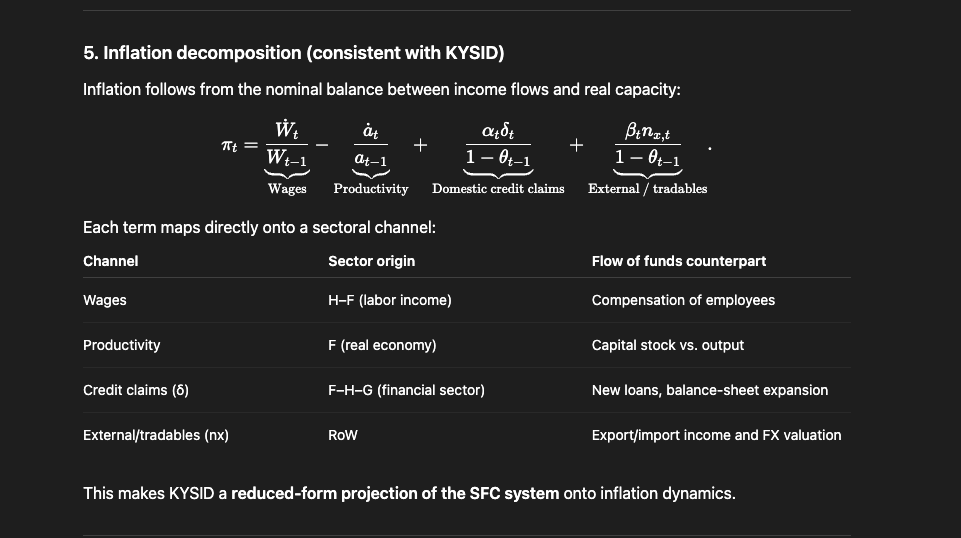

Inflation decomposition (consistent with KYSID)

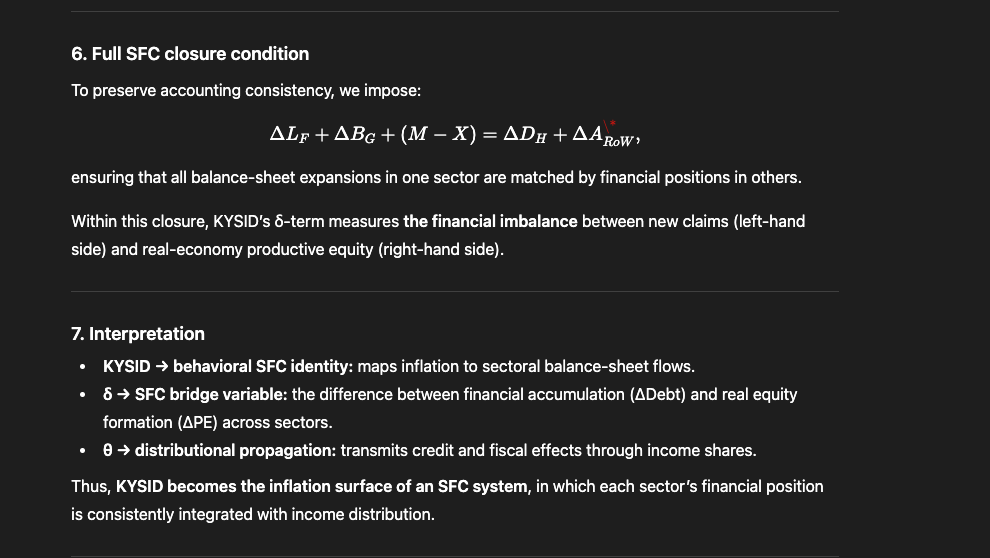

Full SFC closure condition

By embedding the KYSID decomposition within the SFC matrix, the model gains full accounting closure and compatibility with the Post-Keynesian stock–flow tradition, while retaining the analytical tractability of its ratio-based form.

@threadreaderapp

unroll

unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh