Huge moment for Agentic Commerce.

EMVCo (the technical body behind Visa, Mastercard, Amex) is creating global standards for "agentic payments."

This is the biggest change in card payments since "tap to pay"

Here's how it works 🧵

EMVCo (the technical body behind Visa, Mastercard, Amex) is creating global standards for "agentic payments."

This is the biggest change in card payments since "tap to pay"

Here's how it works 🧵

Right now, AI agents are phenomenal at finding things to buy.

- Power users are starting to default to their research

- Can compare complex options and summarize

- And when people click through conversion is 2x to 5x higher

But...

- Power users are starting to default to their research

- Can compare complex options and summarize

- And when people click through conversion is 2x to 5x higher

But...

There's no agreed way for payment to happen

- There's countless protocols

- x402 for agents accessing other tools

- ACP and A2P from Open AI and Google

- Visa and Mastercard have their own approaches

- There's countless protocols

- x402 for agents accessing other tools

- ACP and A2P from Open AI and Google

- Visa and Mastercard have their own approaches

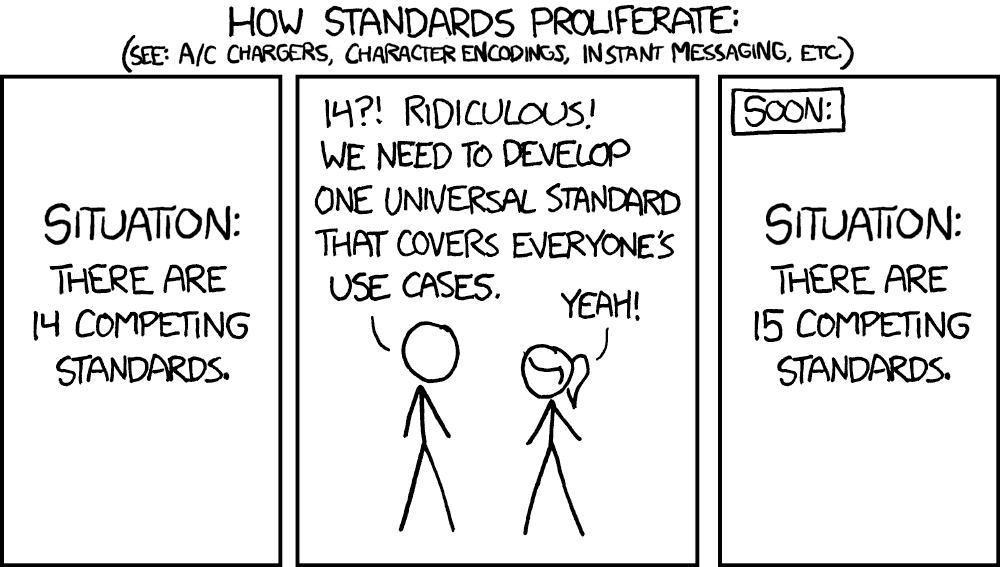

This is the XKCD standards problem playing out in real-time: "There are 14 competing standards.

Let's create a universal standard that covers everyone's use cases. There are now 15 competing standards."

Let's create a universal standard that covers everyone's use cases. There are now 15 competing standards."

EMVCo are the people who set the standards for how debit and credit cards work globally

Now they're creating a "passport" for authenticated agents.

- Use your Face ID

- FIDO token generated (like a passkey)

- Given to agent

Now they're creating a "passport" for authenticated agents.

- Use your Face ID

- FIDO token generated (like a passkey)

- Given to agent

Agents present a uniform cryptographic token that proves "I'm a good bot, authorized to spend."

The merchant firewall and fraud systems see the signature, verifies it came from a legitimate issuer, and lets it through.

The merchant firewall and fraud systems see the signature, verifies it came from a legitimate issuer, and lets it through.

For authentication, they're extending FIDO/SRC standards:

- You authenticate once with your face to "bind" an agent to your card, - Set spending limits, - Then the agent presents a delegated token at checkout. - No 3DS challenge needed (!!!)

- You authenticate once with your face to "bind" an agent to your card, - Set spending limits, - Then the agent presents a delegated token at checkout. - No 3DS challenge needed (!!!)

This prevents the agentic commerce world from fracturing into incompatible silos.

It ensures an agent built on Microsoft/OpenAI can pay a merchant using Adyen, authenticated by an issuer on Marqeta.

It ensures an agent built on Microsoft/OpenAI can pay a merchant using Adyen, authenticated by an issuer on Marqeta.

Critically it creates a new liability framework (!!!)

- If merchants use the EMV standard, issuers take fraud risk.

- If they allow random bots, merchants eat the cost.

- If merchants use the EMV standard, issuers take fraud risk.

- If they allow random bots, merchants eat the cost.

We're about to see a new transaction category emerge: "Agent Present."

- Not card-present.

- Not card-not-present.

- Agent-present.

With its own interchange rates, its own fraud rules, its own liability shifts.

- Not card-present.

- Not card-not-present.

- Agent-present.

With its own interchange rates, its own fraud rules, its own liability shifts.

Are standards boring? Absolutely.

Are they critical?

More than almost anything else happening in payments right now.

PS. Notice the complete lack of stablecoin mentions?

Me too.

Are they critical?

More than almost anything else happening in payments right now.

PS. Notice the complete lack of stablecoin mentions?

Me too.

• • •

Missing some Tweet in this thread? You can try to

force a refresh